Prepared for the Canada Revenue Agency

Supplier name: Sage Research Corporation

Contract Number: # 46165-203453/001/CY

Contract value: $54,279.55 including HST

Award date: July 30, 2018

Delivery date: February 2019

Registration number: POR 024-18

For more information on this report, please email media.relations@cra-arc.gc.ca

Ce rapport est aussi disponible en français.

Final Report

Prepared for the Canada Revenue Agency by Sage Research Corporation.

February 2019

The Canada Revenue Agency (CRA) commissioned Sage Research Corporation to conduct a qualitative public opinion research study on concepts for an advertising campaign to increase awareness of CRA’s activities to reduce tax evasion and avoidance. The results were used to help determine the most effective type of messaging and proposed creative for this campaign, as well as to test related terminology. Six focus groups were conducted between September 5 and 6, 2018, with two groups in each of Montreal, Toronto and Vancouver. Two focus groups were conducted with each of the following target groups: tax intermediaries, individuals with high net worth, and individuals in the general public who did not meet the criterion for high net worth. This publication reports on the findings of this public opinion research study.

Permission to Reproduce

This publication may be reproduced for non-commercial purposes only. Prior written permission must be obtained from the Canada Revenue Agency. For more information on this report, please contact the Canada Revenue Agency at: media.relations@cra-arc.gc.ca

© Her Majesty the Queen in Right of Canada, as represented by the Minister of National Revenue, 2019

Catalogue Number: Rv4-125/2019E-PDF

International Standard Book Number (ISBN): 978-0-660-29765-1

Cette publication est aussi disponible en français sous le titre : Campagne publicitaire sur l’évasion fiscale et l’évitement fiscal abusif de l’Agence du revenu du Canada de 2018-2019 – mise à l’essai de concepts - Rapport définitif

Table of contents

Tax evasion and aggressive tax avoidance deprive all levels of government of tax revenues that are needed to support essential programs and services to all Canadians, such as healthcare, childcare, education, and various infrastructure projects. The Canada Revenue Agency's compliance activities help preserve public confidence in the fairness and integrity of the tax system, and to accomplish this, the CRA administers a number of programs to deal with suspected cases of non-compliance, including tax avoidance, tax evasion, fraud, and other tax offences.

The CRA developed an advertising campaign to increase awareness of CRA’s activities to reduce tax evasion and avoidance. The campaign involved online banner ads, social media such as Facebook, LinkedIn, Twitter and search engine marketing. The campaign ran between October 15 and November 25, 2018.

The CRA identified the need for public opinion research to determine the most effective type of messaging and proposed creative for this campaign, as well as to test related terminology. The research tested four concepts for banner ads: Dots, Hockey, No Borders and Numbers. The finished version of the ads would be a 15-20 second animated ad with no audio track. The ad concepts were tested in a rough form and were not animated. Instead, each ad was represented by images of three or four frames, and the moderator read a description of the animation along with the text in the ads.

Six focus groups were conducted between September 5 and 6, 2018, with two groups in each of Montreal, Toronto and Vancouver. Two focus groups were conducted with each of the following target groups: tax intermediaries, individuals with high net worth, and individuals in the general public who did not meet the criterion for high net worth.

This research was qualitative in nature, not quantitative. As such, the results provide an indication of participants’ views about the topics explored, but cannot be statistically generalized to the full population. Qualitative research does, however, produce a richness and depth of response not readily available through other methods of research. It is the insight and direction provided by qualitative research that makes it an appropriate tool for exploring reactions to the banner ad concepts.

Overview of Reactions to Ad Concepts

Overall, the Numbers ad concept did not perform well due to considerable confusion over how to understand and interpret the statistics presented in the ad.

Participants ranked the ad concepts on overall likelihood of getting their attention. Preference was split across the other three concepts – No Borders, Hockey and Dots. Of these three concepts, no one concept stood out as the preferred concept among the three.

Participants also rated the likelihood of clicking the link in each ad. Again, the likelihood of clicking was lower for Numbers than for the other concepts, and was similar for Dots, Hockey, and No Borders

However, the three ad concepts were perceived differently:

There was little discernible difference in reactions to the ad concepts across the three target groups. Within each target group there was a lot of variation in preference, and because of that there were not any clear systematic differences in concept preference as a function of target group.

URL Lines

In all four ad concepts, the final line of text on the final frame is a URL line. The URL line consisted of an introductory phrase (in Dots, Hockey, and Numbers), and a URL.

Both parts of the URL line were important:

Introductory phrase: The introductory phrase impacted perceived messaging in two ways:

URL: The URL played an important role in influencing the perceived message of the banner ad, as well as giving some indication (in conjunction with the introductory phrase) of what might be on the website.

There were four different URLs in the English ad concepts, and two different URLs in the French concepts:

Impact of the phrase New and Better Approaches

All of the ad concepts at some point use the phrase new and better approaches.

Participants perceive that dealing with tax evasion is one of the CRA’s core mandates, so an ad talking about this is not perceived as new information. However, the reference to new and better approaches tends to be perceived as news, i.e. that the CRA has developed new methods or technologies to better detect and deal with tax evasion. This helps increase interest in the ad, and increase the perceived impact the ad might have on tax evaders.

Terminology

“Cracking down”: A small number of participants preferred cracking down in a URL because it is perceived to be forceful. However, other participants preferred the CRA use a different phrase for any of several reasons: (a) it does not, by itself, give any indication that the subject matter is taxation, (b) it is perceived to be a generic phrase often used in other unrelated contexts to signal actions to reduce some undesirable behaviour (e.g. drunk driving), or (c) it can imply that the CRA was less strict in the past in enforcing tax rules and is only now enforcing them more strictly.

“Tax cheating”, “Tax evasion”, “Tax evasion and aggressive tax avoidance”: Participants were asked about the meaning and ease of understanding these phrases:

Contract value: $54,279.55 including HST

Political Neutrality Certification

I hereby certify as Senior Officer of Sage Research Corporation that the deliverables fully comply with the Government of Canada political neutrality requirements outlined in the Communications Policy of the Government of Canada and Procedures for Planning and Contracting Public Opinion Research. Specifically, the deliverables do not include information on electoral voting intentions, political party preferences, and standings with the electorate or ratings of the performance of a political party or its leaders.

Signed:

Rick Robson

Vice President

Sage Research Corporation

There was little discernible difference in reactions to the ad concepts across the three target groups. Within each target group there was a lot of variation in preference, and because of that there were not any clear systematic differences in concept preference as a function of target group. Based on this outcome, the results will be discussed based on all participants, rather than separately for each target group.

Overall, the Numbers ad concept did not perform well due to considerable confusion over how to understand and interpret the statistics presented in the ad.

Participants ranked the ad concepts on overall likelihood of getting their attention. Preference was split across the other three concepts – No Borders, Hockey and Dots. Of these three concepts, no one concept stood out as the preferred concept among the three.

However, the three ad concepts were perceived differently:

In all four ad concepts, the final line of text on the final frame is a URL line. The URL line consisted of an introductory phrase (in Dots, Hockey, and Numbers), and a URL.

The URLs were somewhat different in English and French, and so are discussed separately. There were four different URLs in the English ad concepts, and two different URLs in the French concepts:

English concepts

| Ad Concept | Introductory phrase | URL |

| No Borders | [none] | Canada.ca/taxcheating |

| Hockey | Learn how: | Canada.ca/crackingdown |

| Dots | Learn how: | Canada.ca/stoptaxcheating |

| Numbers | Learn more about our new and better approaches at | Canada.ca/payyourshare |

| Ad Concept | Introductory phrase | URL |

| No Borders | [none] | Canada.ca/fraudefiscale |

| Hockey | Apprenez comment : | Canada.ca/fraudefiscale |

| Dots | Apprenez comment : | Canada.ca/fraudefiscale |

| Numbers | Apprenez plus sur nos nouvelles techniques plus efficacies à : | Canada.ca/payezvotrepart |

Overall, both parts of the URL line – the introductory phrase and the URL – were important:

Introductory phrase: The introductory phrase impacted perceived messaging in two ways:

URL: The URL played an important role in influencing the perceived message of the banner ad, as well as giving some indication (in conjunction with the introductory phrase) of what might be on the website. Given the impact the URL can have, consideration should be given to increasing its visual prominence, particularly on the Dots and Hockey concepts.

The first part of all of the URLs is Canada.ca. In the rough text versions of the ad concepts, there was no other element identifying the Government of Canada as the sponsor of the ad, although the plan is to include such an element in the finished ad. Particularly in the discussion of the Hockey ad concept, it emerged that most participants did not perceive Canada.ca as necessarily being a Government of Canada website. This reinforces the importance of the plan to include identification of the Government of Canada in the finished ad.

For each ad concept, participants were asked to rate the likelihood of clicking the link. Overall, the results mirrored the results on likelihood of the ad getting attention: likelihood of clicking was lower for Numbers than for the other concepts, and the likelihood of clicking was similar for Dots, Hockey, and No Borders. Some observations on likelihood of clicking:

English URL Lines

The majority of participants preferred Canada.ca/stoptaxcheating. Some preferred Canada.ca/payyourshare, and a small number preferred Canada.ca/crackingdown. None preferred Canada.ca/taxcheating.

Canada.ca/stoptaxcheating:This was perceived to be simple, direct and easy to understand. Compared to Canada.ca/taxcheating, adding the word stop is perceived to make the URL more forceful, and conveys a clearer message that the ad is about stopping tax cheating.

The interpretation of stoptaxcheating is influenced by the lead-in introductory phrase. As mentioned above, Learn how paired with Canada.ca/stoptaxcheating (in Dots) led some participants to wonder if the focus of the website content would be on telling people what they can do to stop other people from cheating on taxes. In contrast, Learn more about our new and better approaches at (in Numbers) was perceived to indicate that the website content would focus on what the CRA is doing to stop tax cheating.

Canada.ca/payyourshare: Some participants liked this URL, while some others disliked it.

Participants who liked the URL perceived “paying your share” to be a principle that is widely supported in Canada. Associated with this, it is perceived to be a message to all taxpayers, in comparison to “stop tax cheating” which is perceived to be primarily directed to people who may cheat on their taxes.

Several participants favouring the URL commented that they would expect the website to include information on how tax dollars are spent and how this benefits Canadians.

Reasons cited by those who did not like the URL:

Canada.ca/crackingdown: A small number of participants preferred this URL, although more often it was a second choice after Canada.ca/stoptaxcheating.

On the positive side, some see it as more forceful than Canada.ca/stoptaxcheating.

On the negative side, it is perceived as vague. “Stop tax cheating” clearly identifies taxation as the subject domain of the ad. “Cracking down” could be about other things, such as drunk driving or drug abuse. Some perceived it to be a generic phrase used in these other areas as well, and that the banner ad would benefit from using a tax-specific URL rather than what they perceive as a generic phrase applicable and used in a wide variety of non-tax contexts.

Several participants said “cracking down” implies to them that the CRA was less strict in enforcing the rules in the past, and has now decided to start enforcing the rules more strictly. A few commented that this is not consistent with the phrase new and better approaches used in all the ad concepts. New and better approaches implies that the CRA enforced the rules in the past but can now do so more effectively.

French URL Lines

Participants liked Canada.ca/fraudefiscale: it was perceived to be clear, and to be targeting people who may cheat on their taxes.

Some did not like Canada.ca/payezvotrepart for the same reasons some participants in the English language sessions did not like Canada.ca/payyourshare. It was perceived to be accusatory or insulting. Rather than perceiving the URL as targeting tax cheaters, it was perceived to be directed – unfairly – at all taxpayers.

All of the ad concepts at some point use the phrase new and better approaches.

Participants perceive that dealing with tax evasion is one of the CRA’s core mandates, so an ad talking about this is not perceived as new information. However, the reference to new and better approaches tends to be perceived as news, i.e. that the CRA has developed new methods or technologies to better detect and deal with tax evasion. This helps increase interest in the ad, and increase the perceived impact the ad might have on tax evaders. Tax evaders might be interested in going to the website to find out what the new and better approaches are.

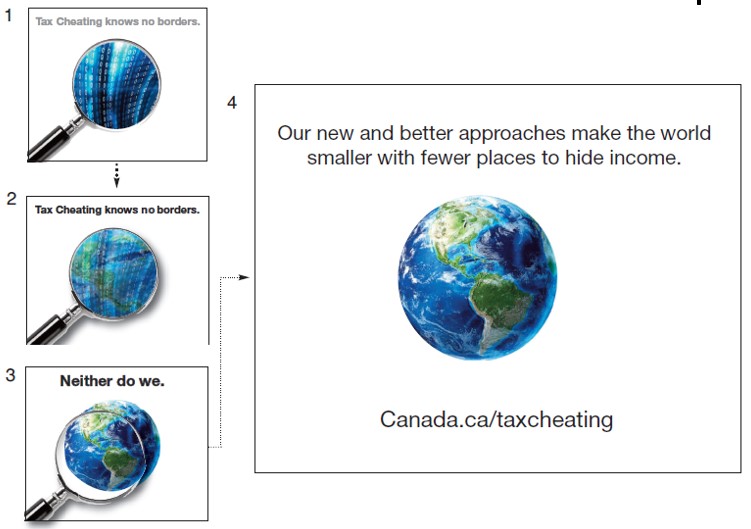

No Borders was perceived relatively positively by many participants. It was also perceived to be very different from Dots and Hockey in one significant respect: No Borders was perceived by most to focus specifically on just offshore tax evasion, while the other two concepts were perceived to be about tax evasion generally and as targeting all Canadian who may cheat on their taxes. This includes offshore tax evasion, but most participants did not specifically refer to offshore tax evasion when talking about either Dots or Hockey.

People engaging in offshore tax evasion are perceived to be very wealthy, which gives them the means and resources to potentially benefit from offshore tax havens. This is perceived to be a very small segment of the population, and none of the participants considered themselves to be in this segment.

There were some different reactions in terms of what targeting this type of tax evasion might mean for interest in the ad:

Perceived Positive Aspects of No Borders

The ad opens with the following headline: Tax Cheating knows no borders. Participants liked that the basic subject matter of the ad – tax cheating – is identified right at the beginning of the ad. This was not done right away in the other ad concepts, and to varying degrees the other concepts were criticized for this.

The message of the ad was perceived to be clear and easily understood.

The text new and better approaches conveys the idea that the CRA is not only devoting effort to address offshore tax evasion, but is also developing better ways of detecting and dealing with it.

The creative approach was usually perceived positively. The execution is perceived to be uncluttered, and this also makes the text easy to read. The large amount of white space with the strongly contrasting blue/green colours of the globe were perceived by many to work well in a banner ad to get attention.

Perceived Issues with No Borders

The only significant issue with No Borders was the URL line in the English concept. There is no introductory phrase, and the URL is Canada.ca/taxcheating. Some participants said the URL line would be more effective if the following changes were made:

Potential Revisions

Choose a more impactful URL, such as Canada.ca/stoptaxcheating, and preface this with an introductory phrase that gives a reason for clicking on the link.

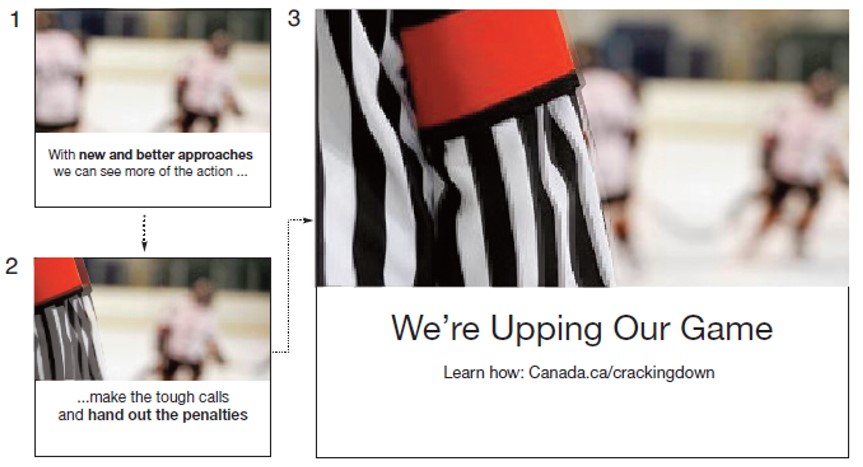

Hockey was in some respects perceived quite positively, but it had one major problem. Namely, quite a few participants said there is no way to tell what the ad is about (note that all participants were informed at the beginning of the focus group that the Government of Canada, and specifically the CRA, would be doing the advertising, so these participants were imagining what their impression would have been had they not been told this). That is, there’s nothing that says this ad is about tax. Even given that the Government of Canada would be identified as the ad sponsor in a finished ad, participants said they would not know this ad is about tax. The ad could be about the government cracking down on drunk driving, or some other problematic behaviour.

Participants said that to address this problem, the ad must clarify that the subject matter is tax cheating. Many said naming the Canada Revenue Agency in the final frame in addition to the Government of Canada would help clarify this.

Providing clarification is provided, the ad is perceived to be about doing more, based on new and better approaches, to deal with tax evasion. Note that this is tax evasion in general, not the narrower perceived focus of No Borders on offshore tax evasion.

As discussed earlier, there was a mixed reaction to the URL, Canada.ca/crackingdown. Some thought it an acceptable URL, but the majority in the English sessions favoured “stop tax cheating.” Also, to the extent people interpret “cracking down” to imply the CRA was more lax in enforcing rules in the past, this can muddy interpretation of We’re Upping Our Game. The CRA could be “upping its game” by virtue of new and better approaches or by being more strict than in the past in enforcing tax rules.

Perceived Positive Aspects of Hockey

The following are perceived positive aspects of Hockey, given a context where it is clear the subject matter of the ad is tax cheating.

Many of the participants, but not all, said the hockey imagery would get their interest in looking at the ad. They perceive hockey as widely popular in Canada, and believe using this them would help get interest in looking at the ad.

Some participants perceive the referee analogy to be a good one for the CRA. A referee is someone whose job is to enforce rules, and to do so in an impartial manner. They noted that one of the CRA’s jobs is to enforce tax rules, and that it is a good thing for the CRA to do so in an impartial manner.

In comparison to Dots, Hockey is perceived by a large majority to have a less aggressive tone. Hockey is perceived to be fairly forceful (make the tough call and hand out the penalties), but as discussed later Dots is perceived to have a harder edge. Some participants, but not all, prefer the softer perceived tone of Hockey over the more aggressive tone of Dots.

New and better approaches, and We’re upping our game: Taken together, this conveys that the CRA is getting better in its methods and technology for detecting and dealing with tax evasion.

Perceived Issues with Hockey

As noted above, the biggest issue with hockey is clarifying that it about tax evasion.

While the hockey theme was attention-getting for many, some who liked it said that people uninterested in hockey might not watch the ad, and a relatively small number of participants said they were not interested in hockey and would not watch the ad.

Some participants who perceived Hockey as having a softer tone than Dots said the tone of Hockey is too soft, and they preferred the more aggressive tone of Dots. These participants said a more aggressive tone is needed to get the attention of tax evaders and to motivate them to change their behaviour.

While the majority described the tone of Hockey as softer compared to Dots, a small number nonetheless perceived it as being too aggressive. This was based on their reaction to a referee “making the tough calls” and “handing out the penalties.”

Several participants said the creative device of the ad starting out blurry/out of focus would cause them not to watch the ad.

Potential Revisions

Clarify that the subject of the ad is tax evasion. This could involve changing the URL, and/or mentioning the CRA.

Consider changing the URL to Canada.ca/stoptaxcheating.

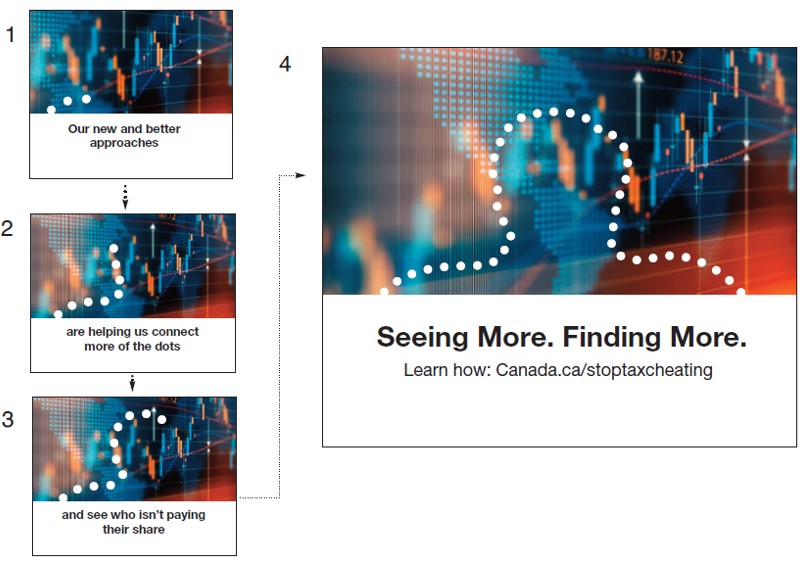

Like Hockey, Dots was perceived to be about the government detecting and dealing with tax evasion generally. Note that this is tax evasion in general, not the narrower perceived focus of No Borders on offshore tax evasion.

The most significant difference between Dots and Hockey was the perceived tone of the ad. Hockey was perceived by many (but not all) to have softer tone, while Dots was perceived by many (again, not all) to have a more aggressive tone. Some participants preferred the perceived softer tone of Hockey, while some others felt that the more aggressive perceived tone of Dots would have more impact on tax evaders.

The more aggressive perceived tone is particularly driven by the line on the final frame, Seeing More. Finding More. This gives the impression that the CRA is actively surveilling people, and doing so effectively. Some participants said the background imagery and colours give the ad a “colder” feeling than Hockey, and this contributes to the perception of a more aggressive tone. The final silhouette of a person’s head and shoulders was perceived by some to convey the personal impact of Seeing More. Finding More. On a more negative note, several participants said the silhouette looked to them like chalk marks around a victim one might see at a crime scene.

Perceived Positive Aspects of Dots

As noted above, some participants preferred the more aggressive tone of Dots over the softer tone of Hockey. A small number of participants perceived Hockey as having a more aggressive tone than Dots, and preferred Dots for that reason.

The text is easy to understand and easy to read.

The URL, Canada.ca/stoptaxcheating contributes to a strong perception that the ad is about stopping tax cheating. Of the four URLs used across the four English concepts, the majority preferred this URL because it is simple, concrete and easy to understand.

Quite a few participants said the growing line of dots would attract their attention to the ad and motivate them to watch it in order to see what the line of dots turns into.

Our new and better approaches conveys that the CRA has new methods or technologies, and this perception is reinforced by the final line, Seeing More. Finding More. Several participants said the background graphics conveyed an impression that the CRA is making greater use of technology.

The text, and see who isn’t paying their share, was perceived positively by some participants, in the sense that “paying your share” is a widely shared value, and it implies the CRA will be fair (i.e. not make someone pay more than their share).

Perceived Issues with Dots

As noted earlier, some preferred Hockey over Dots because they preferred the perceived softer tone of Hockey.

The main perceived issue with Dots is that one does not know for sure that it is about tax evasion until the final frame with the URL Canada.ca/stoptaxcheating. Some participants who were not intrigued by the growing line of dots said they probably would not watch the ad to the end because of not knowing early on what it is about. A few suggested a reference to “tax” should be introduced earlier in the ad.

The URL line is: Learn how: Canada.ca/stoptaxcheating. Some participants raised questions about how to interpret the intent of this line, and therefore were not entirely sure of the message of the ad. The ad is perceived to be about stopping tax cheating, but this URL line could either mean “learn how the CRA is stopping tax cheating”, or “learn what I can do to stop other people from tax cheating.”

Some participants did not like the background graphics. For reference, when the concept was presented to them by the moderator, the moderator said the following with respect to the first frame:

The opening image shows a background of computer codes in various colours, stock graphs, and a blue dotted portion of the map of the world. In the foreground, three white dots being to appear on the left side in a line head upwards and to the right. Text at the bottom says, “Our new and better approaches.”

The moderator’s script for subsequent frames pertaining to the graphics addressed only the animation of the line of dots, with no further reference to the background imagery.

Participants concerned about the background graphics said it was “cluttered”, or that they did not understand how it connected to the text and the overall message of the ad. That is, unlike some other participants, they did not perceive this as implying greater use of technology by the CRA. Also, almost none reacted to the map graphic (which is largely somewhat out of focus), so that did not impact interpretation of the ad.

Potential Revisions

Consider introducing the topic of “tax” earlier in the ad.

Decide what the intended focus of the introductory URL phrase should be in terms of implications for what will be on the website: information on what a person can do to stop other people from tax cheating, or information on what the CRA is doing to deal with tax cheating.

When finalizing the background graphic: (a) be careful not to let it distract from attending to the dots, and (b) if possible, conveying an impression that the CRA is using technology can help support the new and better approaches message.

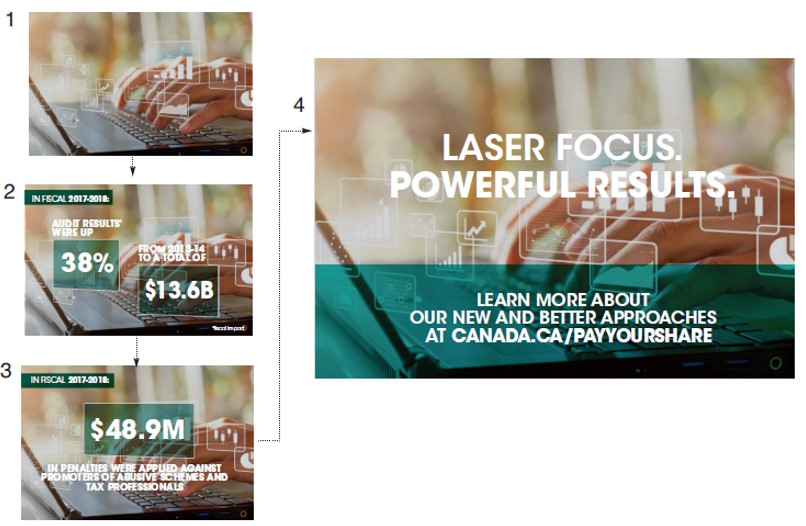

The Numbers ad concept did not perform well, primarily because there was considerable confusion over how to understand and interpret the statistics presented in the ad.

Some participants said they liked the underlying idea of giving some statistics, but none of these participants liked the actual statistics given in the ad. They did not perceive the statistics to be either clear or impressive. They said a statistic should be easily understandable by a lay person, and give information that people would be interested in. An example mentioned by one participant was to give the amount of lost tax revenue caused by the underground economy. Another example mentioned by a participant was a statistic showing how much money the CRA has recovered from tax evaders – and a large number would be impressive (the statistics in the ad were not perceived to give this information in a clear, understandable fashion).

Some participants said that seeing any numbers at all would probably cause them not to watch the ad – that is, they are simply not interested in reading quantitative statistics.

There were two frames with statistics, and there were perceived problems with both:

Some participants commented that given the 15-20 second duration of the ad, it would be hard to read and assimilate these statistics as they pass by on the screen, especially given that these are perceived to be complicated and hard to understand statistics.

Other issues with Numbers that were mentioned:

Potential Revisions

The statistics presented need to be substantially revised or replaced with something easier for people to understand, and that they would care about.

Revise the background graphics to make it easier to read the statistics.

Participants were asked a general question about terminology that might be used in the finished ad concepts or the website referred to in the ads. They were given a sentence frame with three different endings, and asked which they thought was most appropriate given their impressions of the ad concepts, and the meaning and ease of understanding the different sentence endings.

English

The CRA is combatting…

French

L’Agence du revenu du Canada lutte contre …

English Terminology

Participants in all three target groups were split between preferring tax cheating or tax evasion. Only a few participants preferred tax evasion and aggressive tax avoidance.

With regard to tax evasion and aggressive tax avoidance, many participants either said that tax evasion and aggressive tax avoidance seem to mean the same thing, or they did not know what the difference in meaning was. Given this the phrase was perceived as too wordy. A few participants said the phrase is appropriate because aggressive tax avoidance expands into “grey areas”. One participant said they thought that combatting aggressive tax avoidance meant that the CRA would be working to make rule changes to close certain tax “loopholes” that are currently legal.

Participants perceived both tax cheating and tax evasion to refer to breaking the rules. Quite often, though, the phrases were perceived to have a somewhat different slant.

Tax cheating: Participants who preferred this phrase liked it because it is simple, concrete language that everyone would understand.

Tax evasion: Quite a few participants perceived tax evasion to refer to more serious rule-breaking. This led some participants to prefer this phrase over tax cheating. In this view, tax evasion is a subset of tax cheating. Participants preferring tax evasion felt that tax cheating also includes small-scale rule-breaking, and felt that the CRA should be focused on more serious rule-breaking.

French Terminology

Fraude fiscale was perceived to be all illegal activities to avoid paying taxes, and was the preferred phrase by most participants, while a small number preferred évasion fiscal.

Évitement fiscal aggressif was seen as hard to understand. In the General Public group it was perceived as not having any clear meaning. In the Tax Intermediary group, participants thought it probably refers to grey areas in tax law, but did not consider it to be a well-defined phrase.

There were varying interpretations of évasion fiscale:

Number and Location of Focus Groups

Six two-hour focus groups were conducted September 5-6 2018, as follows:

| Total | Montreal (Fr) | Toronto | Vancouver | |

| High net worth Canadians | 2 | 1 | 1 | |

| General population | 2 | 1 | 1 | |

| Tax intermediaries | 2 | 1 | 1 | |

| Total | 6 | 2 | 2 | 2 |

Twelve people were recruited for each of the high net worth and general population focus groups, and 11 were recruited for each of the tax intermediary focus groups. There were eight participants in each focus group, for a total of 48.

Participant Qualifications

All participants met the Government of Canada Qualitative Standards for past participation in qualitative research: (a) not attended a qualitative research session within the past six months, and (b) not attended five or more qualitative research sessions in the past five years.

None of the participants were employed in the following industries: marketing research, media, advertising agency or graphic design firm, public relations, federal government, a provincial or local government department related to taxes or finance.

The following are additional qualifications for each of the three target groups.

High net worth Canadians

General Population

Tax Intermediaries

The sample used for recruiting tax intermediaries was purchased from infoCanada, a list vendor.

The sample was limited to firms with fewer than 50 employees, and included the following SICs:

To qualify, participants had to provide tax advice to individual tax filers. Note that all but one participant provided advice to individual tax filers with an annual income of $200,000 or more.

Participant Honoraria

The participant honoraria were as follows:

Hello/Bonjour, I'm ___________ of [name of recruiting company], a public opinion and marketing research company. First off, let me assure you that we are not trying to sell you anything. We are organizing a research project on behalf of the Government of Canada. I’d like to ask you some questions to see if you would be interested in possibly taking part in this study. This will take about 5 or 6 minutes.

May I continue?

Would you prefer that I continue in English or in French? Préférez-vous continuer en français ou en anglais? [If prefers French, either switch to the French screener and continue, or say the following and then hang up and arrange French-language call-back] Nous vous rappellerons pour mener cette entrevue de recherche en français. Merci. Au revoir.

In this project, an individual like yourself is chosen to sit down with several others and give ideas and opinions in a two-hour discussion session. People who are invited and take part in the group discussion will receive a cash payment honorarium as thanks for their time.

[If prefers to continue in English for the Montreal French-language focus groups, ask:] The discussion will be held entirely in French, and participants will be asked to review and discuss written communication materials written only in French. Would you be comfortable with this?

[If prefers to continue in French for the Toronto or Vancouver English-language focus groups, ask – note that the final screener will use French for this question:] The discussion will be held entirely in English, and participants will be asked to review and discuss written communication materials written only in English. Would you be comfortable with this?

The Government of Canada is planning to run an advertising campaign later this year. They have several alternative ideas for how to do this advertising campaign. In the discussion session, you would be asked to review some of these advertising materials and give your ideas and opinions about these materials.

Your participation is voluntary and confidential. All information collected, used and/or disclosed will be used for research purposes only and administered per the requirements of the Privacy Act. The names of participants will not be provided to the government. Your decision to take part will not affect any dealings you may have with the Government of Canada.

May I continue?

I need to ask you a few questions to see if you fit the profile of the type of people we are looking for in this research.

Note to recruiter: When terminating a call because of their profile say: Thank you for your cooperation. We already have enough participants who have a similar profile to yours, so we are unable to invite you to participate at this time.

1) First of all, do you, or does anyone in your household, work for..? (Read list, If “yes” to any, thank and end the interview.)

2) Have you ever participated in an in-depth research interview or a focus group involving a small group of people where people were asked to discuss different topics?

3a) What topics have you ever discussed?______________________________(If related to advertising or taxation, thank and terminate)

3b) And when was the last time you attended an interview or discussion group?

3c) In the past 5 years, how many in-depth research interviews or discussion groups have you attended? Would you say less than 5 in total, or would you say 5 or more?

4a) We would like to talk to a cross-section of people with different income levels. For 2017, was your total annual household income from all sources before taxes…? (Read List)

4b) And was your total annual household income from all sources before taxes…? (Read List)

4c) And was your total annual household income from all sources before taxes…? (Read List)

Montreal:

Toronto:

Vancouver

5) Record gender:

General Population Quota: 6 male, 6 female, High Net Worth Quota: 8 male, 4 female

6) We would like to talk to people in different age groups. Into which one of the following groups should I place you? (Read list)

General Population – 18-34 = 4; 35-54=4; 55 or over=4; High Net Worth – No quotas

Let me tell you some more about this study to see if you would like to take part.

7) As I mentioned earlier, the research involves taking part in a focus group discussion. In the group discussion, you will be asked to fill in some short questionnaires in English (French). Also, participants in focus groups are asked to express their thoughts and opinions freely in an informal setting with others. Do you feel comfortable doing this?

Terminate if person gives a reason such as verbal ability, sight, hearing, or related to reading/writing ability, or if they think they may have difficulty expressing their thoughts. If respondent wears glasses, remind them to bring them to the session.

Participants in the discussion group will be asked to turn off any electronic devices during the discussion. Would you be willing to do so?

There may be some people from the Government of Canada who have been involved in this project observing the session. However, they will not take part in the discussion in any way, and they will not be given your name. Is this acceptable to you?

The session will be audio-recorded. These recordings are used to help with analyzing the findings and writing the report. Your name will not appear in the research report. Is this acceptable to you?

INVITATION

Thank you. We would like to invite you to participate in one of our group discussions. Refreshments will be provided, and you will be paid $150 in cash for your participation immediately at the end of the group discussion. The discussion will last approximately 2 hours starting at _____, and will be held…..

As I mentioned earlier, this is a research project being done by the Government of Canada. Specifically, this research project is being done by the Canada Revenue Agency. I want to reassure you that your name will not be given to them, nor will your decision about participating affect any dealings you have with the Canada Revenue Agency.

Would you be willing to attend?

| City/Date: | Location: | Type of group: | Time: |

| Montreal Thurs. Sept 6 | General Population | 8:00 – 10:00 pm | |

| Toronto Wed. Sept 5 | High Net Worth | 8:00 – 10:00 pm | |

| Vancouver Thurs. Sept 6 | General Population High Net Worth |

6:00 – 8:00 pm 8:00 – 10:00 pm |

As part of our quality control measures, we ask everyone who is participating in the focus group to bring along a piece of I.D., picture if possible. You may be asked to show your I.D.

As these are small groups and with even one person missing, the overall success of the group may be affected, I would ask that you make every effort to attend the group. But, in the event you are unable to attend, let us know as soon as possible so we can find a replacement. Please call us at [Insert recruiting company phone #]. Please ask for [Insert recruiting company contact name]. Also note that you may not send someone else in your place if you are unable to attend.

Please also arrive 15 minutes prior to the starting time. The discussion begins promptly at [TIME]. People who arrive too late to participate in the focus group will not receive the honorarium.

Someone from our office will be calling you back to confirm these arrangements. May I please have your contact information where we can reach you during the evening and during the day?

Name:_______________________________________________________________

Evening phone:___________________ ; Day time phone:_________________

Email address:_______________________________________________________

Thank you very much!

Recruited by:________________________________________________________

Confirmed by:________________________________________________________

Recruit from list provided for tax and accounting professionals. Recruit a mix of tax professionals and accountants.

Hello/Bonjour, I'm ___________ of [name of recruiting company], a public opinion and marketing research company. First off, let me assure you that we are not trying to sell you anything. We are organizing a focus group research project on behalf of the Government of Canada, and specifically for the Canada Revenue Agency. The focus group is with professionals who provide tax advice and tax preparation services to individual taxpayers. The purpose of the research is to get input on an advertising campaign related to taxation that the Canada Revenue Agency is planning to run later this year.

May I please speak with an individual in your company who provides tax advice or tax preparation services directly to individual tax filers?

When connected, repeat introduction if needed

I’d like to ask you some questions to see if you would be interested in possibly taking part in this study. This will take about 5 or 6 minutes.

May I continue?

Would you prefer that I continue in English or in French? Préférez-vous continuer en français ou en anglais? [If prefers French, either switch to the French screener and continue, or say the following and then hang up and arrange French-language call-back] Nous vous rappellerons pour mener cette entrevue de recherche en français. Merci. Au revoir.

In this project, an individual like yourself is chosen to sit down with several others and give ideas and opinions in a two-hour discussion session. People who are invited and take part in the group discussion will receive a cash payment honorarium as thanks for their time.

[If prefers to continue in English for the Montreal French-language focus groups, ask:] The discussion will be held entirely in French, and participants will be asked to review and discuss written communication materials written only in French. Would you be comfortable with this?

[If prefers to continue in French for the Toronto English-language focus groups, ask:] La discussion se déroulera entièrement en anglais et nous demanderons aux participants de passer en revue du matériel de communication en anglais seulement puis d'en discuter. Seriez-vous à l'aise avec cela?

As I mentioned earlier, the Canada Revenue Agency is planning to run an advertising campaign later this year. They have several alternative ideas for how to do this advertising campaign. In the discussion session, you would be asked to review some of these advertising materials and give your ideas and opinions about these materials.

Your participation is voluntary and confidential. All information collected, used and/or disclosed will be used for research purposes only and administered per the requirements of the Privacy Act. The names of participants will not be provided to the government. Your decision to take part will not affect any dealings you may have with the Government of Canada and the Canada Revenue Agency.

May I continue?

I need to ask you a few questions to see if you fit the profile of the type of people we are looking for in this research.

Note to recruiter: When terminating a call because of their profile say: Thank you for your cooperation. We already have enough participants who have a similar profile to yours, so we are unable to invite you to participate at this time.

1) What is your position in the company? ________________

If an administrative assistant/secretary, ask to speak with someone who provides tax advice or tax preparation services directly to individual tax filers

2a) Do you provide tax advice to individual tax filers?

2b) Do you provide tax return preparation services to individual tax filers?

If “no” to both Q.2a and Q.2b, thank and end interview

3) I’d like to get an idea of the types of individual tax filer clients to whom you provide services. In terms of the total annual household income of your clients, do you have any individual tax filer clients whose total annual household income is…? (Read List)

Recruit at least 6 who say “yes” to “$200,000 or more”

4) Have you ever participated in an in-depth research interview or a focus group involving a small group of people where people were asked to discuss different topics?

5a) What topics have you ever discussed?______________________________(If related to advertising or taxation, thank and terminate)

5b) And when was the last time you attended an interview or discussion group?

5c) In the past 5 years, how many in-depth research interviews or discussion groups have you attended? Would you say less than 5 in total, or would you say 5 or more?

Let me tell you some more about this study to see if you would like to take part.

6) As I mentioned earlier, the research involves taking part in a focus group discussion. In the group discussion, you will be asked to fill in some short questionnaires in English (French). Also, participants in focus groups are asked to express their thoughts and opinions freely in an informal setting with other tax professionals. Do you feel comfortable doing this?

Terminate if person gives a reason such as verbal ability, sight, hearing, or related to reading/writing ability, or if they think they may have difficulty expressing their thoughts. If respondent wears glasses, remind them to bring them to the session.

Participants in the discussion group will be asked to turn off any electronic devices during the discussion. Would you be willing to do so?

There may be some people from the Canada Revenue Agency who have been involved in this project observing the session. However, they will not take part in the discussion in any way, and they will not be given your name. Is this acceptable to you?

The session will be audio-recorded. These recordings are used to help with analyzing the findings and writing the report. Your name will not appear in the research report. Is this acceptable to you?

INVITATION

Thank you. We would like to invite you to participate in one of our group discussions. Refreshments will be provided, and you will be paid $225 in cash for your participation immediately at the end of the group discussion. The discussion will last approximately 2 hours starting at _____, and will be held…..

Would you be willing to attend?

| City/Date: | Location: | Type of group: | Time: |

| Montreal Thurs. Sept 6 | Tax Intermediaries | 6:00 – 8:00 pm | |

| Toronto Wed. Sept 5 | Tax Intermediaries | 6:00 – 8:00 pm |

As part of our quality control measures, we ask everyone who is participating in the focus group to bring along a piece of I.D., picture if possible. You may be asked to show your I.D.

As these are small groups and with even one person missing, the overall success of the group may be affected, I would ask that you make every effort to attend the group. But, in the event you are unable to attend, let us know as soon as possible so we can find a replacement. Please call us at [Insert recruiting company phone #]. Please ask for [Insert recruiting company contact name]. Also note that you may not send someone else in your place if you are unable to attend.

Please also arrive 15 minutes prior to the starting time. The discussion begins promptly at [TIME]. People who arrive too late to participate in the focus group will not receive the honorarium.

Someone from our office will be calling you back to confirm these arrangements. May I please have your contact information where we can reach you during the evening and during the day?

Name:_______________________________________________________________

Evening phone:___________________ ; Day time phone:_________________

Email address:_______________________________________________________

Thank you very much!

Recruited by:________________________________________________________

Confirmed by:________________________________________________________

1) Introduction (15 minutes)

a) Introduce self (Rick Robson/Sylvain Laroche of Sage Research, an independent market research company), and explain purpose of research: This research is being sponsored by the Government of Canada and specifically the Canada Revenue Agency (CRA). The Government is considering running an advertising campaign later this year. They have several alternative ideas for how to do this advertising campaign. What I’ll be doing is showing you the different alternative ideas they have, and asking you for your opinions.

b) Review group discussion procedures:

c) Any questions?

d) Participant self-introductions: First name only

2) Review ad concepts (20 minutes)

a) Overview of procedure: The Government of Canada is planning to run an advertising campaign, and they have developed four alternative concepts for the design of the ads.

I’m going to show you the advertising concepts one at a time, and after each one I’ll ask you to complete a short questionnaire on your reactions to it. After you have seen everything, I’ll ask you for your opinions about the different advertising concepts.

b) Explanation of how ad concepts have been rendered:

c) Present first ad concept (order will be rotated across groups)

d) Present the other three ad concepts, using the above procedure

e) Have participants complete Final Ad Concepts Questionnaire

Rotation system

| Toronto, Sept. 5 | Vancouver Sept. 6 | Montreal Sept. 6 | |

| Group 1 | Tax Intermediaries F – No Place to Hide G – We’re Upping Our Game N – CRA Numbers R – Connecting the Dots |

General Public G – We’re Upping Our Game R – Connecting the Dots F – No Place to Hide N – CRA Numbers |

Tax Intermediatires G – We’re Upping Our Game N – CRA Numbers R – Connecting the Dots F – No Place to Hide |

| Group 2 | High Net Worth R – Connecting the Dots N – CRA Numbers G – We’re Upping Our Game F – No Place to Hide |

High Net Worth N – CRA Numbers G – We’re Upping Our Game F – No Place to Hide R – Connecting the Dots |

General Public N – CRA Numbers F – No Place to Hide R – Connecting the Dots G – We’re Upping Our Game |

Assignment of letters to ads

3) Do vote on ads’ ability to grab attention (5 minutes)

To help me get started, I’d first like to find out what choices you made on the last questionnaire you filled in – that is, which of the four ad concepts is most likely to get your attention? Which one was your second choice? Which one is the least likely to get your attention? And why?

(Do vote and use the voting pattern to decide on order of discussion in Step 4 below)

4) Review campaign concepts (55 minutes)

For each ad concept:

To help me get started, I’d first like to find out how you rated the ad. (Do votes on Q.7 in the self-completion questionnaire for that concept)

Start the discussion with those most positive towards the ad

Probe:

Note to moderator on intended ad campaign objectives:

After all ad concepts have been discussed, project slide showing only the 4 URLs:

I am going to show you a slide with the four different website addresses that were on the ad concepts we have discussed. Show slide with URLs and leave on screen during discussion

Which one of these four do you think the CRA should use in their ad campaign? Why?

Is there one of these four that you think the CRA should not use? Why?

5) Terminology: Tax cheating vs. Tax evasion vs. Aggressive tax avoidance (12 Minutes)

We’re now finished talking about the ad concepts. I now want to get your opinions on certain terminology that might be used in the ads, in the URL, or on the website that you would go to if you clicked on the link in the ad.

I’m interested in this because sometimes tax terminology can be a bit hard to understand. It’s important that the website use language that is clear and easy to understand.

I’m going to pass out a page that shows the three versions of a sentence that might be on the website. The first part of the sentence is the same for all three versions, but last part is different.

(Pass out questionnaire, briefly review, and have participations complete it. Request no talking while they are completing the questionnaire)

(Do vote on which is most appropriate)

For each phrase, discuss:

6) Terminology: Cracking down (7 minutes)

I have another question about terminology to use on the website.

In the exercise we just finished, the sentence you were looking at used the word “combatting.” One alternative would be to use the phrase "cracking down." So, the sentence would be The CRA is cracking down on tax cheating, or The CRA is cracking down on tax evasion.

What do you think of this use of the phrase “cracking down”? What does it mean to you? Is it a good phrase to use in this context, or not really?.

Probe:

7) Attitudes towards Tax Cheating (5 Minutes)

8) Wrap-up (1 minute)

Thank you for coming this evening and giving us your opinions.

Please leave all the papers on the table.

On your way out, please don’t forget to see the host to sign for and receive your incentive envelope.

Group 1: There is another group waiting out there to have this same discussion. So please don’t talk about anything related to what we have done here to make sure they don’t have any more information than you did before our discussion.

1) Please write down any emotion words that describe your reaction to this ad concept:

2) How likely is it that the ad would get your attention?

3) How likely would you be to click on the link to get more information? Please circle a number.

4) What is the ad about?

5) Please write down anything that you particularly like about this ad concept:

6) Please write down anything that you don’t like about this ad concept or anything that you found confusing:

7) Overall, thinking about your reactions to the ad and how the ad is done, would you say the ad is – please circle a number between 1 and 5:

The four ad concepts were F, G, N and R.

1) Which one of these ads is most likely to get your attention. Please write in the letter of the ad concept below:

1b) Why is that?

2) Please write in the letter of the ad concept second most likely to get your attention: ________

3) Please write in the letter of the ad concept least likely to get your attention: ________

4) Each ad has a website link that people might click on. Please write in the letter of the ad concept you would most likely click on to get more information:

Three alternative ways of completing the sentence: The Canada Revenue Agency is combatting _________

Please think about:

Overall, which phrase do you think is the most appropriate ending for the sentence?

1) Please write down any emotion words that describe your reaction to this ad concept:

2) How likely is it that the ad would get your attention?

3) How likely would you be to click on the link to get more information? Please circle a number.

4) What is the ad about?

5) Please write down anything that you particularly like about this ad concept:

6) Please write down anything that you don’t like about this ad concept or anything that you found confusing:

7) Overall, thinking about your reactions to the ad and how the ad is done, would you say the ad is – please circle a number between 1 and 5:

The four ad concepts were F, G, N and R.

1) Which one of these ads is most likely to get your attention. Please write in the letter of the ad concept below:

1b) Why is that?

2) Please write in the letter of the ad concept second most likely to get your attention: ________

3) Please write in the letter of the ad concept least likely to get your attention: ________

4) Each ad has a website link that people might click on. Please write in the letter of the ad concept you would most likely click on to get more information:

Three alternative ways of completing the sentence: The Canada Revenue Agency is combatting

Please think about:

Overall, which phrase do you think is the most appropriate ending for the sentence?