Prepared for the Canada Revenue Agency

Supplier name: Earnscliffe Strategy Group

Contract Number: # 46575-193626/001/CY

Contract value: $68,935.65

Award date: August 17, 2018

Delivery date: October 19, 2018

Registration number: POR 035-18

For more information on this report, please email media.relations@cra-arc.gc.ca

Ce rapport est aussi disponible en français.

Final Report

Prepared for the Canada Revenue Agency by Earnscliffe Strategy Group

October 2018

This public opinion research report presents the results of focus groups conducted by Earnscliffe Strategy Group on behalf of Canada Revenue Agency. The research was conducted in September 2018.

Cette publication est aussi disponible en français sous le titre : Recherche qualitative sur l’initiative de lettres de prestations pour les non-déclarants.

This publication may be reproduced for non-commercial purposes only. Prior written permission must be obtained from the Canada Revenue Agency. For more information on this report, please contact the Canada Revenue Agency at: media.relations@cra-arc.gc.ca

Catalogue Number:

Rv4-124/2019E-PDF

International Standard Book Number (ISBN):

978-0-660-29595-4

Related publications (registration number: POR 035-18)

Catalogue Number: Rv4-124/2019F-PDF (Final Report, French)

ISBN: 978-0-660-29596-1

© Her Majesty the Queen in Right of Canada, as represented by the Minister of National Revenue, 2018

Table of contents

Earnscliffe Strategy Group (Earnscliffe) is pleased to present this report to the Canada Revenue Agency summarizing the results of the qualitative research on the Non-Filer Benefit Letter Initiative.

The Minister of National Revenue is committed to “Ensuring that the Canada Revenue Agency (CRA) is a client-focused agency that will proactively contact Canadians who are entitled to, but are not receiving, tax benefits.” To meet this commitment, the Department embarked on a letter initiative encouraging low income non-filers to file an income tax and benefit return so that they could receive benefits to which they may be potentially entitled. The CRA wanted to better understand why certain individuals responded to the letter and others did not. The purpose of this research was to better understand whether there are any barriers or motivators to filing and what they are, as well as, changes that could be made to the letters to encourage more people to file. The total cost to conduct this research was $63,391.31, including HST.

The objective of the research was to gauge the effectiveness of, and refine as necessary, the wording of the communication material that is being sent to recipients who have not filed their taxes. The specific objectives were to:

Earnscliffe also set out to explore any barriers; and, if so, what they were, as well as if the information provided in the letter was sufficient or overwhelming for the audience.

To meet these objectives, Earnscliffe conducted a series of eight focus groups in four cities across Canada: Halifax, NS (September 18); Toronto, ON (September 19); Calgary, AB (September 24); and, Montreal, QC (September 27). The focus groups in Montreal were conducted in French.

The focus groups were conducted with Canadians eighteen years of age and older. In each city, one focus group was conducted with participants who received a letter but did not file a return; the other was conducted with participants who received a letter and filed a return. However, given that some of the contact information was outdated, we were required to supplement recruits in Calgary and Montreal with members of the general population. For each group, we tried to ensure a mix of demographics including sexes, ages, and education levels.

It is important to note that qualitative research is a form of scientific, social, policy and public opinion research. Focus group research is not designed to help a group reach a consensus or to make decisions, but rather to elicit the full range of ideas, attitudes, experiences and opinions of a selected sample of participants on a defined topic. Because of the small numbers involved the participants cannot be expected to be thoroughly representative in a statistical sense of the larger population from which they are drawn and findings cannot reliably be generalized beyond their number.

The key findings from the research are presented below.

Political Neutrality Certification

I hereby certify as a Senior Officer of Earnscliffe Strategy Group that the deliverables fully comply with the Government of Canada political neutrality requirements outlined in the Policy on Communications and Federal Identity and the Directive on the Management of Communications. Specifically, the deliverables do not include information on electoral voting intentions, political party preferences, standings with the electorate or ratings of the performance of a political party or its leaders.

Signed:

Stephanie Constable

Principal, Earnscliffe

Date: October 19, 2018

La société Earnscliffe Strategy Group (Earnscliffe) est heureuse de présenter ce rapport à l’Agence du revenu du Canada. Il fait la synthèse des résultats d’une recherche qualitative sur l’initiative des lettres de prestations à l’intention des non déclarants.

La ministre du Revenu national s’est engagée à faire en sorte que l’ARC soit « une agence axée sur la clientèle qui communique de façon proactive avec les Canadiens et les Canadiennes qui ne reçoivent pas les économies d’impôts auxquelles ils ont droit ». Pour respecter cet engagement, le ministère a lancé une initiative en envoyant des lettres aux non déclarants à faible revenu pour les inciter à produire une déclaration de revenus et de prestations afin de se prévaloir des prestations fiscales auxquelles ils pourraient avoir droit. L’ARC voulait mieux connaître les raisons qui ont poussé certaines personnes à répondre ou non à la lettre. Le but de cette enquête était de mieux évaluer s’il y avait des obstacles et des facteurs de motivation pouvant influencer la production d’une déclaration fiscale et à les cerner. De même, elle s’est attachée à déterminer quelles modifications pourraient être apportées aux lettres pour encourager davantage de personnes à soumettre leurs déclarations. Le montant total dépensé pour effectuer cette recherche s’élève à 63 391,31 $ (TVH incluse).

Cette étude visait à mesurer l’efficacité du libellé utilisé dans le matériel de communication envoyé aux destinataires n’ayant pas encore soumis leurs déclarations de revenus et à l’affiner, si nécessaire. Les objectifs précis étaient de :

Earnscliffe a également examiné le matériel pour établir s’il comportait des barrières et, le cas échéant, les identifier. La firme s’est aussi attardée aux renseignements fournis dans la lettre afin de déterminer si le public cible juge qu’ils sont suffisants ou s’il peine à s’y retrouver.

Pour répondre à ces objectifs, Earnscliffe a organisé une série de huit groupes de discussion dans quatre villes réparties dans l’ensemble du Canada, soit à Halifax, N-É (18 septembre); Toronto, ON (19 septembre); Calgary, AB (24 septembre); et Montréal, QC (27 septembre). La rencontre de Montréal s’est déroulée en français.

Les groupes de discussion ont été menés auprès de Canadiens âgés de 18 ans et plus. Dans chaque ville, un groupe de discussion s’est tenu avec des participants qui ont reçu une lettre, mais n’ont pas soumis de déclaration fiscale, et un autre s’est déroulé auprès de participants qui ont reçu une lettre et produit leur déclaration. Cela dit, étant donné que certaines des coordonnées étaient obsolètes, nous avons dû recruter de nouveaux participants à Calgary et à Montréal auprès de la population générale. Dans chaque groupe, nous avons veillé à assurer une représentativité démographique diversifiée, en fonction du sexe, de l’âge et du niveau d’éducation.

Aux fins du présent rapport, il convient de mentionner que la recherche qualitative est une forme de sondage d’opinion publique dont les dimensions sont scientifiques, sociales et politiques. La recherche à l’aide de groupes de discussion n’est pas conçue pour aider un groupe à parvenir à un consensus ou à prendre des décisions, mais vise plutôt à faire le tour complet d’une question et à recueillir auprès des participants un ensemble d’idées, d’attitudes, d’expériences et d’opinions sur un sujet donné. En raison du nombre restreint de personnes interrogées, on ne peut pas s’attendre, sur le plan statistique, à ce que ces dernières soient pleinement représentatives de l’ensemble de la population dont elles proviennent. Les résultats ne peuvent donc pas faire l’objet de généralisations au-delà du nombre de participants.

Les principaux résultats de cette enquête sont présentés ci-dessous.

En tant que représentant d’Earnscliffe Strategy Group, j’atteste par la présente que les produits livrables se conforment entièrement aux exigences en matière de neutralité politique du gouvernement du Canada exposées dans la Politique sur les communications et l’image de marque et dans la Directive sur la gestion des communications. Plus précisément, les produits livrables ne comprennent pas d’information sur les intentions de vote électoral, les préférences quant aux partis politiques, les positions des partis ou l’évaluation de la performance d’un parti politique ou de ses dirigeants.

Signature :

Stephanie Constable

Partenaire, Earnscliffe

Date: 19 octobre 2018

Earnscliffe Strategy Group (Earnscliffe) is pleased to present this report to the Canada Revenue Agency summarizing the results of the qualitative research on the Non-Filer Benefit Letter Initiative.

The Minister of National Revenue is committed to “Ensuring that the Canada Revenue Agency (CRA) is a client-focused agency that will proactively contact Canadians who are entitled to, but are not receiving, tax benefits.” To meet this commitment, the Department embarked on a letter initiative encouraging non-filers to file an income tax and benefit return so that they could receive benefits to which they may be potentially entitled. The CRA wanted to better understand why certain individuals responded to the letter and others did not.

The specific objectives of the research were to gauge the effectiveness of the communication materials that was sent to recipients, including:

To meet these objectives, Earnscliffe conducted a series of eight focus groups in four cities across Canada: Halifax, N.S (September 18); Toronto, ON (September 19); Calgary, AB (September 24); and, Montreal, QC (September 27). The focus groups in Montreal were conducted in French.

The focus groups were conducted with Canadians eighteen years of age and older. In each city, one focus group was conducted with participants who received a letter but did not file a return; the other was conducted with participants who received a letter and filed a return. However, given that some of the contact information was outdated, we were required to supplement recruits in Calgary and Montreal with members of the general population. For each group, we tried to ensure a mix of demographics including sexes, ages, and education levels.

All sessions were approximately two hours in length beginning at 5:30 pm or 7:30 pm across all locations. Participants received a $100 honorarium in appreciation of their time.

Please refer to the Appendix of this report for all relevant screening and qualifications criteria as well as the focus group discussion guide and benefit letters.

It is important to note that qualitative research is a form of scientific, social, policy and public opinion research. Focus group research is not designed to help a group reach a consensus or to make decisions, but rather to elicit the full range of ideas, attitudes, experiences and opinions of a selected sample of participants on a defined topic. Because of the small numbers involved the participants cannot be expected to be thoroughly representative in a statistical sense of the larger population from which they are drawn and findings cannot reliably be generalized beyond their number.

The qualitative report is divided into two sections. The first explores participants’ feelings about income taxes including how they address their taxes each year (if applicable). The second explores specific reactions to the benefits letters in terms of their clarity, credibility, tone, and ability to motivate participants to take action.

Except where specifically identified, the findings in this qualitative report represent the combined results for filers, non-filers and members of the general public in both English and French.

The focus groups began with an initial warm-up discussion to gauge participants’ feelings toward income taxes and their process for completing their taxes every year (if applicable). This conversation provided useful context for understanding how participants viewed the benefit letters.

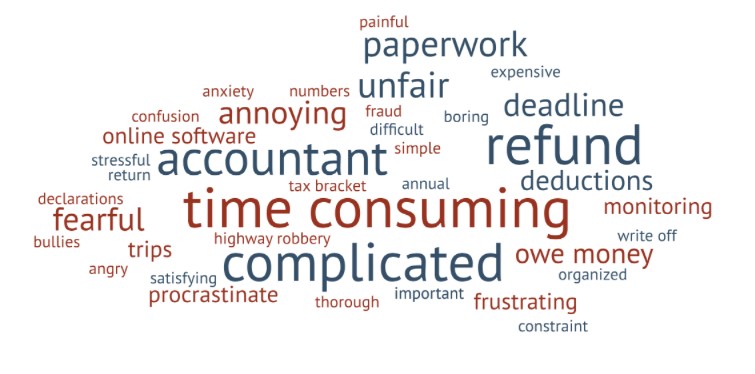

Participants were initially asked to write down one or two things that came to mind as it relates to filing their income taxes. The following diagram illustrates the words that were raised spontaneously. The size of the font depicts the frequency of mention: words represented by larger font were raised more often; those represented by smaller font were raised less often. There is no differentiation to be made by the font colour.

As illustrated in the diagram above, top of mind word associations tended to be more negative than positive.

Negative word associations revolved around:

Interestingly, those who tended to have more neutral to positive word associations were often those who relied on someone else to file their taxes or those who consider themselves to be technology-savvy and comfortable completing their taxes online.

Positive word associations included:

Participants were then asked to discuss the process by which they used to file taxes every year. The following table summarizes the key advantages and disadvantages of each process, discussed in more detail below:

| Accountant/Someone else | Online Software | Paper |

| ✔ Tax experts ✔ Simple, efficient ✔ Transfer of accountability (especially if audited) |

✔ At tax filer’s disposal ✔ Intuitive |

✔ At tax filer’s disposal ✔ Paper record ✔ No cost |

| ✘ Expensive | ✘ Requires a computer and knowledge of income taxes ✘ Cost for software |

✘ Time consuming ✘ Requires knowledge of income taxes |

Those who indicated that they typically rely on someone else, particularly an accountant, to file their taxes explained that they did so for the peace of mind in knowing that their taxes were completed correctly and that any credits/benefits or write offs to which they were eligible were captured. Participants also described it as a shift in responsibility for ensuring the accuracy of the information which they felt would be particularly helpful if they were audited. Participants felt that the toughest part of this process was having to gather up all of the relevant paperwork and booking an appointment to meet to discuss their taxes. The main drawback they offered was that accountants can be “expensive”.

Those who indicated that they usually complete their own taxes using the online software explained that they did so because of the cost savings (as opposed to contracting an accountant) and because they trust themselves better than anyone to know what they are or are not eligible for. Many added that their taxes are fairly straightforward and described the online software as being intuitive – leading the user to the appropriate boxes of information that are required for completion. The main drawbacks participants offered for this filing option included: requirement of a computer; perception that one needed to be tech-savvy to be able to complete their taxes online; and, and knowledge of which credits, benefits, and/or write offs they were eligible for.

Like those who file their own taxes online, those who indicated that they prefer to file their taxes on paper did so primarily because they trust themselves better than anyone to know what they are or are not eligible for. They also praised the fact that there were no costs associated with paper filing and that they had a paper record of their filings (and did not have to rely on electronic submission/records).

Those who do not file taxes every year provided a variety of reasons that were quite specific and individual which suggests non-filers cannot necessarily be generalized. For example, there were a couple of participants for whom it was beyond their control because they had contracted someone new to file their taxes and for whatever reason, that person did not submit their taxes. A couple of participants still had outstanding claims with CRA that they were waiting to resolve and had decided not to file until the claims were resolved. One participant spoke of having been through a stressful series of interactions with CRA in which CRA was requiring them to prove they had children (for whom they had claimed benefits in the past). Finally, there were a handful of participants who indicated that given their personal economic situations, and the fact they were always owed some money, the time and effort required to file taxes did not outweigh the benefit they would receive from CRA.

When asked what the CRA could do to help Canadians with the tax filing process, a number of suggestions were provided, many of which the CRA is currently doing:

The primary focus of the discussions was to gauge participant reactions to the two Benefits Letters. Discussions focused on whether the letters were clear, credible, used an appropriate tone, and were able to motivate participants to take action.

While each letter will be discussed in turn below, we would make the following overarching observations common to both letters.

Very few participants, including both filers and non-filers, remembered having received either letter from CRA. Of the few who did, a number explained that they read the letter quickly, ascertained that they were still in arrears, and did not action the letter. Only one participant across all of the groups indicated that they proceeded to file their taxes as a result of receiving the letter; that it served as a helpful reminder to file their taxes. This participant was one of the non-filers who normally file their taxes but had relied on someone new and was unaware that their taxes were not filed that year until they received the letter.

While recall of these letters was very low, most indicated that when they receive something from CRA, particularly in the mail, they tend to pay attention and assume something is required of them. Participants pointed to and recognized the CRA and Government of Canada logos. There was also a sense that from a visual standpoint, the font and general layout of both letters were typical of Government communications in that they were not all that graphic, colourful, or visually appealing. For these reasons, the letters were deemed credible.

However, there was definitely a sense, across all of the groups, that the letters were a little promotional in their approach which caused many participants to question the credibility. When asked the main message of the letters, participants suggested that the letters were a reminder to file their taxes under the guise of an invitation to earn credit and benefit money. In fact, there was an assumption that CRA was doing this to collect money from non-filers who participants believe are high income earners trying to avoid paying taxes.

This was compounded by a sense that the letters were form letters and not necessarily applicable to most participants. Many of the participants were not necessarily the target audience for the Non-Filer Benefit Letter Initiative given that it targets those with low income and individuals who have children. Filers and non-filers who did not have children and/or were high income earners, and therefore ineligible for either the Canada Child Benefit or GST/HST credit, complained that the form letter approach was impersonal and insincere. In fact, most assumed that CRA knows most of their personal information if for no other reason than previous income tax filings (i.e., what they earn annually and whether or not they have children). However, whether this information is up to date depends on when an individual last filed their tax return. Alternatively, most would have preferred a simple reminder that their taxes had not yet been filed.

Moreover, filers and non-filers with children and/or lower incomes argued that awareness of the Canada Child Benefit and GST/HST credit was high, arguing that people talk about these credits/benefits. Most believed that the proportion of Canadians unfamiliar with these credits/benefits was very low and perhaps limited to newcomers/immigrants, which made the generalized approach impersonal and unsatisfying.

A number of participants also questioned the CRA’s decision not to include what they felt was critical information about reminding letter recipients of both the obligation of filing taxes every year and the repercussions of not doing so (i.e., interest charges, etc.).

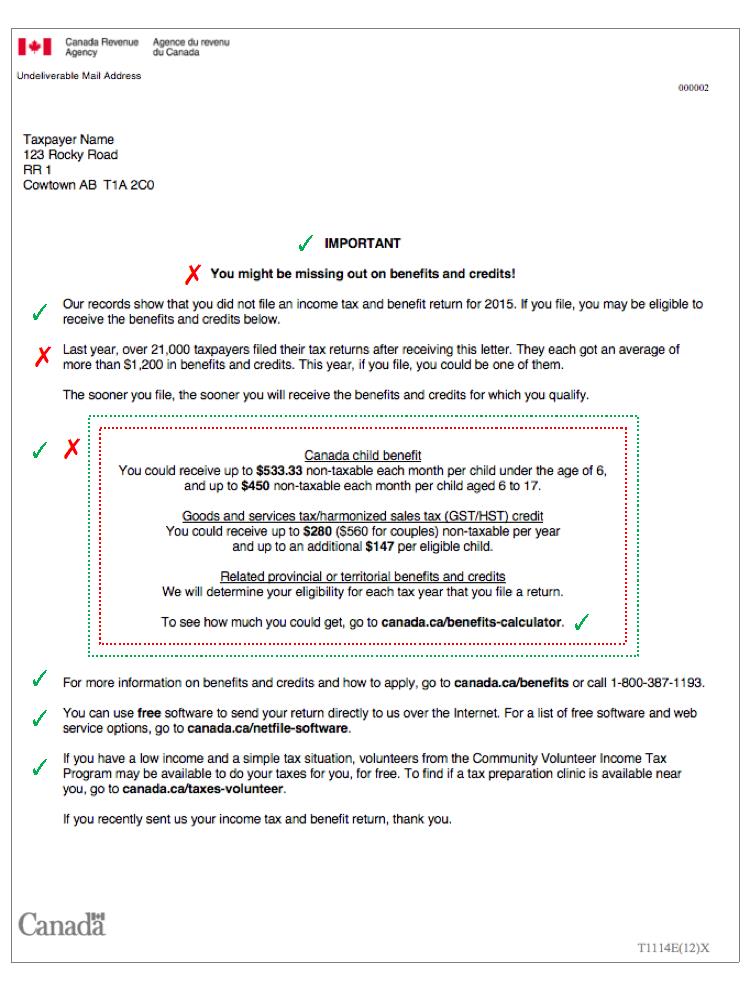

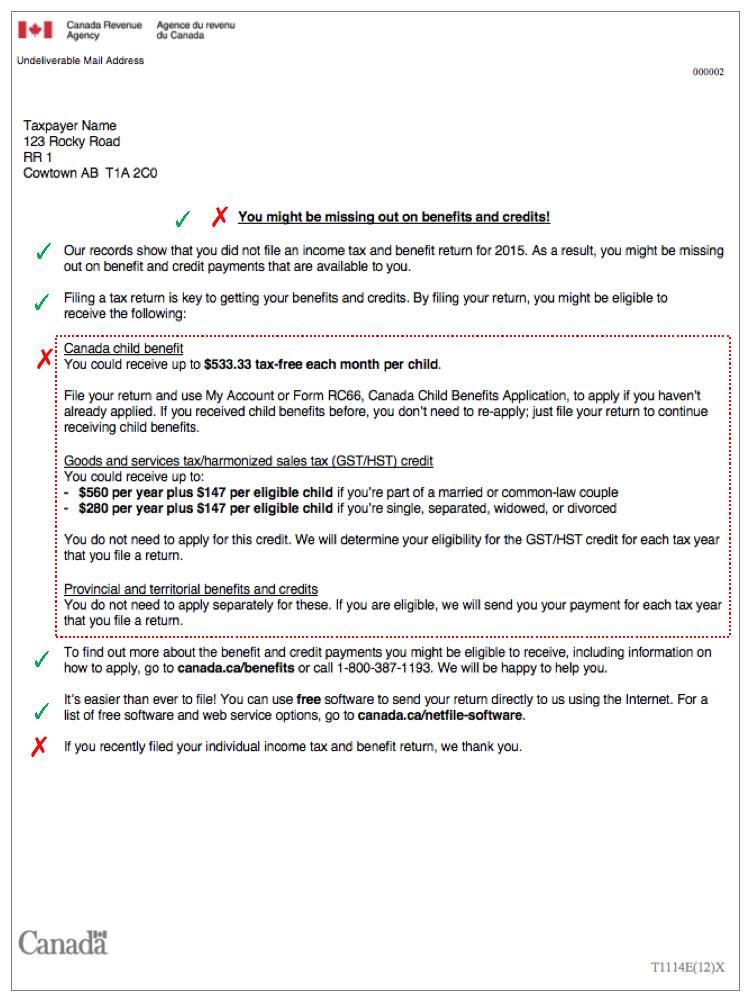

When asked which letter they preferred, most tended to lean towards Letter 2. For this reason, we provide the following specific analysis of each letter beginning with Letter 2.

Letter 2

Overall, participants described Letter 2 as being clearer, inviting to read and visually appealing. Much of this sentiment was attributed to the format of the letter that provided more white space and differentiation allowing viewers to more easily discern the various information points. Participants also felt that the right parts of the letter were accentuated (in bold type).

The image below illustrates the areas participants found helpful (✔), unhelpful (✘), and confusing/unclear (?). Each of these is discussed in detail below.

HELPFUL (POSITIVE REACTIONS)

UNHELPFUL (NEGATIVE REACTIONS)

Letter 1

Overall, reactions to Letter 1 were slightly less positive. It seemed to come off as more of a sales pitch than Letter 2. Participants also had difficulty determining the ‘call to action’ of Letter 1.

HELPFUL (POSITIVE REACTIONS)

UNHELPFUL (NEGATIVE REACTIONS)

Overall, the two benefit letters were met with generally neutral to negative reactions:

While no one questioned the authenticity of the letters – the CRA and Government of Canada were visible and recognized – there were certainly a number of questions related to the credibility. An important element of this view was the perception that the CRA already knows a lot about filers (based on previous filings), especially their annual income and whether they have children or not. The promotional, form letter approach, amplified their negative reactions. In the absence of a more tailored approach, most volunteered they would have preferred a shorter, more direct, reminder to file their taxes.

When asked to choose, participants seemed to prefer Letter 2. It was felt to be a little more visually appealing with helpful differentiation of the benefits/credits and more clarity in terms of eligibility and process for applying for each. Participants struggled to identify the call to action of Letter 1 which seemed to target parents.

Top of mind feelings toward filing taxes tended to be more negative than positive. Those with more positive feelings tended to be those who relied on tax experts which provided peace of mind or those who were tech-savvy and comfortable filing online. Those with more negative feelings tended to complain about a time consuming process, that was confusing (in terms of what can and cannot be claimed), and tense especially if dealing with CRA was required.

There was a lot of confusion as to why there was not an easier system for filing taxes. Participants were pleasantly surprised to learn in Letter 2 that there were volunteer services and free online software to help with tax preparation. These were certainly in line with their suggestions for ways CRA could help improve the process.

Introduction

10 min

Moderator introduces herself and her role: role of moderator is to ask questions, make sure everyone has a chance to express themselves, keep track of the time, be objective/no special interest.

Moderator will go around the table and ask participants to introduce themselves.

Warm-up: general context

30 min

Tonight, we are going to be discussing income taxes. For whatever reason, not everyone files their income taxes every year and while i understand you may or may not be comfortable discussing whether you do or don’t, i’m going to ask you to set aside those insecurities for the purposes of our discussion tonight. Cra works hard to encourage people to file their taxes and we will be looking at some of the materials they have produced to do just that. Now before we look at those documents, i want to start off understanding your views towards income taxes generally.

To begin, on the paper in front of you, i would like you to write down one or two things that come to mind as it relates to filing your income taxes. Feel free to write down anything at all.

MODERATOR TO GO AROUND THE TABLE AND GET PARTICIPANTS TO EXPLAIN WHAT THEY WROTE DOWN.

[FOR GROUPS WITH FILERS]

[FOR THOSE WHO HAVE NOT FILED THEIR TAXES]

Concept testing

70 min

Tonight, we’re going to be reviewing a couple of letters that were sent out to canadians who did not file their taxes for 2015.

MODERATOR TO REVIEW AND DISCUSS EACH LETTER SEPARATELY IN TURN BEGINNING WITH LETTER 1. THE FOLLOWING APPROACH WILL BE THE SAME FOR BOTH LETTERS.

[MODERATOR TO PASS OUT THE PAPER COPY OF THE LETTER AND ASK PARTICIPANTS TO DO AN INITIAL CURSORY REVIEW]

GROUP OF FILERS:

GROUP OF NON-FILERS:

[MODERATOR ASKS PARTICIPANTS TO REVIEW THE LETTER IN MORE DETAIL]

Now I would like you to review the letter in more detail. Please feel free to mark it up. I would ask that you note with a “√” any elements that you find particularly good or interesting (helpful information); note with an “x” any elements that you did not find particularly good or interesting; and, note with a “?” Any elements you find particularly confusing or unclear.

Let’s review how you marked up the letter.

In general…

[FOR LETTER 2] “if you have a low income and a simple tax situation, volunteers from the community volunteer income tax program may be available to do your taxes for you, for free. To find if a tax preparation clinic is available near you, go to canada.ca/taxes-volunteer.” Did you find this information useful? Should it be in the letter?

REPEAT FOR LETTER 2

Wrap-up

Conclusion

10 min

MODERATOR TO CHECK IN THE BACK ROOM AND PROBE ON ANY ADDITIONAL AREAS OF INTEREST.

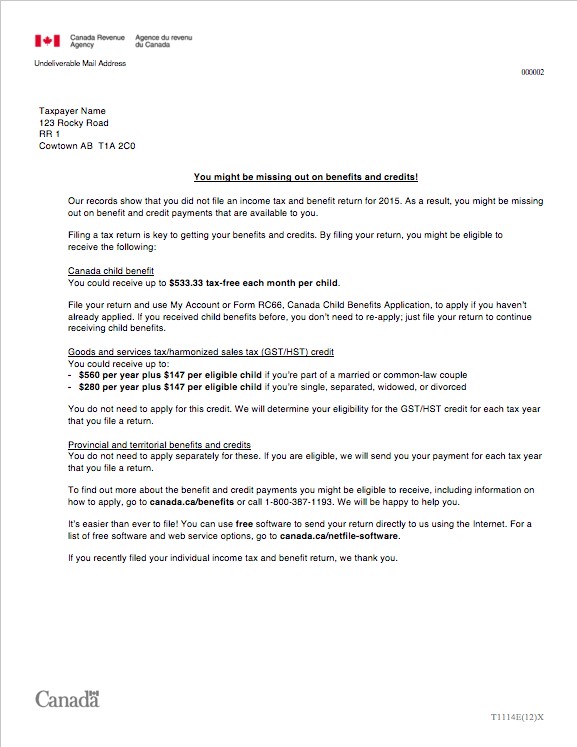

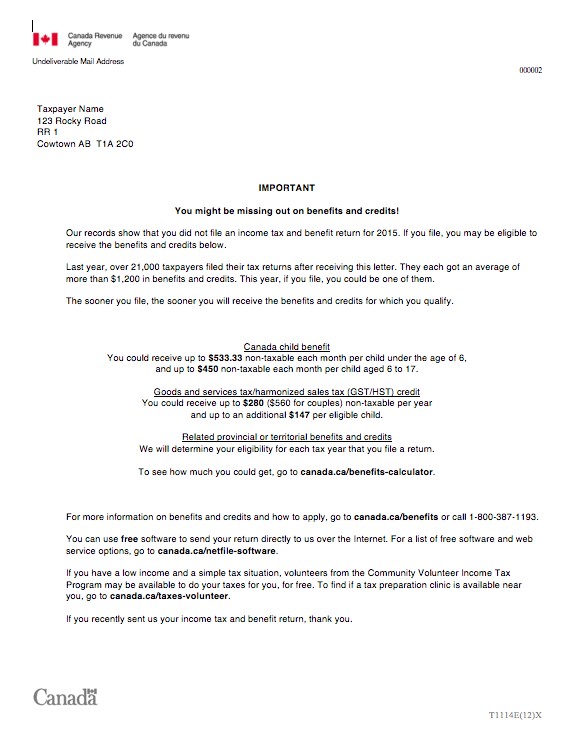

Benefit Letter 1

Benefit Letter 2

Focus group summary

Group 1 /Filed 2015

Group 2 Did not file 2015

| HALIFAX Tuesday, September 18, 2018 | Honorarium: $100 |

| Group 1: Filed 2015 | 5:30pm |

| Group 2: Did not file 2015 | 7:30pm |

| Toronto Wednesday, September 19, 2018 | Honorarium: $100 |

| Group 1: Filed 2015 | 5:30pm |

| Group 2: Did not file 2015 | 7:30pm |

| CALGARY Monday, September 24, 2018 | Honorarium: $100 |

| Group 1: Filed 2015 | 5:30pm |

| Group 2: Did not file 2015 | 7:30pm |

| MONTREAL Thursday, September 27, 2018 | Honorarium: $100 |

| Group 1: Filed 2015 | 5:30pm |

| Group 2: Did not file 2015 | 7:30pm |

| Respondent’s name: Respondent’s phone number: (home) Respondent’s phone number: (work) Respondent’s fax number: Respondent’s email: Sample source: panel random client referral |

Interviewer: Date: Validated: Quality Central: On list: On quotas: |

Hello/Bonjour, my name is _______________ and I’m calling on behalf of the Earnscliffe Strategy Group, a national public opinion research firm. We are organizing a series of discussion groups on behalf of the Government of Canada. The Government of Canada is conducting this research to understand how they could better communicate with Canadians. We received your information from the Government of Canada because you have received a letter from them in the past related to filing taxes.

[IF PROBED] We received your information from the Government of Canada, more specifically the Canada Revenue Agency, which may share information for research purposes in the course of the administration or enforcement of the Income Tax Act.

Would you prefer that I continue in English or French? Préférez-vous continuer en français ou en anglais? [IF FRENCH, CONTINUE IN FRENCH OR ARRANGE A CALL BACK WITH FRENCH INTERVIEWER: Nous vous rappellerons pour mener cette entrevue de recherche en français. Merci. Au revoir].

The purpose of the study and the small group discussion is to better understand barriers and motivators to filing taxes. We are looking for people who would be willing to participate in a discussion group that will last up to two hours. These people must be 18 years of age or older. Up to 10 participants will be taking part and for their time, participants will receive $100.00 for participating in the group discussion. May I continue?

Participation is voluntary. We are interested in hearing your opinions; no attempt will be made to sell you anything or change your point of view. The format is a ‘round table’ discussion led by a research professional. All information collected, used and/or disclosed will be used for research purposes only and the research is entirely confidential. But before we invite you to attend, we need to ask you a few questions to ensure that we get a good mix and variety of people. May I ask you a few questions; this should only take 5 minutes?

READ TO ALL: “This call may be monitored or audio taped for quality control and evaluation purposes.

ADDITIONAL CLARIFICATION IF NEEDED:

S1. Do you or any member of your household currently work for or have you or has any member of your household ever worked for…IF “YES” TO ANY OF THE ABOVE, THANK AND TERMINATE

S2. DO NOT ASK – NOTE GENDER. ENSURE GOOD MIX OF GENDER.

S3. Could you please tell me which of the following age categories you fall into? Are you...ENSURE GOOD MIX OF AGE

S4. What is your current employment status? ENSURE GOOD MIX OF EMPLOYMENT STATUS

S5. Which of the following categories best describes your total household income? That is, the total income of all persons in your household combined, before taxes? [READ LIST]

S6. What is the last level of education that you have completed? ENSURE GOOD MIX OF EDUCATION

S7. Which of the following best describes your current household situation? Are you living…? ENSURE GOOD MIX OF HOUSEHOLD SITUATION

S8. To make sure that we speak to a diversity of people, could you tell me what is your ethnic background? DO NOT READ. ENSURE GOOD MIX OF ETHNICITY

S9. Have you participated in a discussion or focus group before? A discussion group brings together a few people in order to know their opinion about a given subject. (MAX 1/3 PER GROUP, ASK S10, S11, S12)

S10. When was the last time you attended a discussion or focus group?

S11. How many of these sessions have you attended in the last five years?

S12. And what was/were the main topic(s) of discussion in those groups?

IF RELATED TO CRA OR TAXES/TAX BENEFITS, TERMINATE.

INVITATION

S13. Participants in discussion groups are asked to voice their opinions and thoughts. How comfortable are you in voicing your opinions in front of others? Are you… (READ LIST)

S14. Sometimes participants are asked to read text and/or review images during the discussion. Is there any reason why you could not participate?

S15. Based on your responses, it looks like you have the profile we are looking for. I would like to invite you to participate in a small group discussion, called a focus group, we are conducting at [TIME], on [DATE].

As you may know, focus groups are used to gather information on a particular subject matter; in this case, the motivators and barriers with filing taxes. The discussion will consist of 8 to 10 people and will be very informal. It will last up to two hours, refreshments will be served and you will receive $100.00 as a thank you for your time. Would you be willing to attend?

PRIVACY QUESTIONS

Now I have a few questions that relate to privacy, your personal information and the research process. We will need your consent on a few issues that enable us to conduct our research. As I run through these questions, please feel free to ask me any questions you would like clarified.

P1) First, we will be providing the hosting facility and session moderator with a list of respondents’ names and profiles (screener responses) so that they can sign you into the group. This information will not be shared with the Government of Canada department organizing this research. Do we have your permission to do this? I assure you it will be kept strictly confidential.

We need to provide the facility hosting the session and the moderator with the names and background of the people attending the focus group because only the individuals invited are allowed in the session and the facility and moderator must have this information for verification purposes. Please be assured that this information will be kept strictly confidential. GO TO P1A

P1a) Now that I’ve explained this, do I have your permission to provide your name and profile to the facility?

P2) An audio and/or video tape of the group session will be produced for research purposes. The tapes will be used only by the research professional to assist in preparing a report on the research findings and will be destroyed once the report is completed.

Do you agree to be audio and/or video taped for research purposes only?

It is necessary for the research process for us to audio/video tape the session as the researcher needs this material to complete the report.

P2a) Now that I’ve explained this, do I have your permission for audio/video taping?

P3) Employees from the CRA and/or the Government of Canada may be onsite to observe the groups in-person from behind a one-way mirror.

Do you agree to be observed by Government of Canada employees?

P3a) It is standard qualitative procedure to invite clients, in this case, Government of Canada employees, to observe the groups in person. They will be seated in a separate room and observe from behind a one-way mirror. They will be there simply to hear your opinions first hand although they may take their own notes and confer with the moderator on occasion to discuss whether there are any additional questions to ask the group.

Do you agree to be observed by Government of Canada employees?

Invitation:

Wonderful, you qualify to participate in one of our discussion sessions. As I mentioned earlier, the group discussion will take place the evening of [Day, Month, Date] @ [Time] for up to two hours.

Do you have a pen handy so that I can give you the address where the group will be held? It will be held at:

| HALIFAX Tuesday, September 18, 2018 Corporate Research Associates Inc. 7071 Bayers Rd #5001 Halifax, NS B3L 2C2 T: (902) 493-3820 |

Honorarium: $100 5:30 pm 7:30 pm |

| TORONTO Wednesday, September 19, 2018 Consumer Vision 2 Bloor St West, 3rd fl Toronto, ON M4W 3E2 T: 416-967-1596 |

Honorarium: $100 5:30 pm 7:30 pm |

| CALGARY Monday, September 24, 2018 Qualitative Coordination 707 10 Ave SW #120 Calgary, AB T2R 0B3 T: (403) 229-3500 |

Honorarium: $100 5:30 pm 7:30 pm |

| MONTREAL Thursday, September 27, 2018 CRC Research 1610 Rue Ste-Catherine Ouest – Bureau #411 Montreal, QC H3H 2S2 T: 514-932-7511 |

Honorarium: $100 5:30 pm 7:30 pm |

We ask that you arrive fifteen minutes early to be sure you find parking, locate the facility and have time to check-in with the hosts. The hosts may be checking respondents’ identification prior to the group, so please be sure to bring some personal identification with you (for example, a driver’s license). If you require glasses for reading make sure you bring them with you as well. And, please, don’t forget to bring your smartphone as you will not be able to participate without one.

As we are only inviting a small number of people, your participation is very important to us. If for some reason you are unable to attend, please call us so that we may get someone to replace you. You can reach us at [INSERT PHONE NUMBER] at our office. Please ask for [NAME]. Someone will call you in the days leading up to the discussion to remind you.

So that we can call you to remind you about the discussion group or contact you should there be any changes, can you please confirm your name and contact information for me?

First name

Last Name

email

Daytime phone number

Evening phone number

If the respondent refuses to give his/her first or last name or phone number please assure them that this information will be kept strictly confidential in accordance with the privacy law and that it is used strictly to contact them to confirm their attendance and to inform them of any changes to the discussion group. If they still refuse THANK & TERMINATE.