Prepared for the Canada Revenue Agency

Supplier name: Corporate Research Associates Inc.

Contract Number: # 46565-193636/001/CY

Contract value: $64,929.80 (including HST)

Award date: August 22, 2018

Delivery date: December 19, 2018

Registration number: POR 036-18

For more information on this report, please email media.relations@cra-arc.gc.ca

Ce rapport est aussi disponible en français.

Canada Child Benefit (CCB) Application Form Testing Qualitative Research

Final Report

Prepared for the Canada Revenue Agency by Corporate Research Associates Inc.

December 2018

The Canada Revenue Agency (CRA) commissioned Corporate Research Associates to conduct focus groups with Canadians to discuss the revised CCB application form. The aim of this research was to gain feedback on the form to ensure that it can be easily completed while still capturing the necessary information to determine a potential recipient’s eligibility for the CCB. A total of eight (8) in-person focus groups were conducted in four (4) locations from October 3 to 11, 2018. Specifically, in each of Halifax, Montreal, Toronto, and Vancouver. All participants were adult Canadians 19-59 years old who have at least one child under the age of 18 living with them for a total of 59 participants across all the groups. This publication reports on the findings of this qualitative research.

Cette publication est aussi disponible en français sous le titre : Étude qualitative sur le formulaire de demande d’Allocation canadienne pour enfants (ACE) – Rapport final.

Permission to Reproduce

This publication may be reproduced for non-commercial purposes only. Prior written permission must be obtained from the Canada Revenue Agency. For more information on this report, please contact the Canada Revenue Agency at: media.relations@cra-arc.gc.ca

Catalogue Number:

Rv4-122/2019E-PDF

International Standard Book Number (ISBN):

978-0-660-29120-8

Related Publication (Registration Number: POR 036-18):

Catalogue number Rv4-122/2019F-PDF (Final Report, French)

ISBN : 978-0-660-29121-5

© Her Majesty the Queen in Right of Canada, as represented by the Minister of National Revenue, 2018

Table of contents

Corporate Research Associates Inc.

Contract Number: 46565-193636/001/CY

POR Registration Number: POR 036-18

Contract Date: August 22, 2018

As part of ongoing efforts to be more client-focused, the Canada Revenue Agency (CRA) is currently revising the Canada Child Benefit (CCB) application forms (including the RC66, RC66SCH and CTB9 forms) to simplify the application process. Before finalizing the revised form, the CRA wished to obtain feedback from the target audience on a form prototype, to ensure it is user friendly while still capturing the necessary information to determine a potential recipient’s eligibility for the CCB. To achieve this goal, a total of eight (8) in-person focus groups were conducted in four (4) locations from October 3 to 11, 2018. Specifically, in each of Halifax, Montreal, Toronto, and Vancouver.

All participants were adult Canadians 19-59 years old who have at least one child under the age of 18 living with them. In each market, one group was conducted with newcomers (residents who have been in Canada for less than 2 years) and one group with members of the general population who have lived in Canada for at least 3 years, including Indigenous people. A mix of gender, age, employment status, household income, number of children, and marital status were included in each group. Ten individuals were recruited per group with a total of 59 participants attending the focus groups across locations. Discussions each lasted between 1.5 and 2 hours and participants received a $100 honorarium in appreciation for their time.

Caution must be exercised when interpreting the results from this study, as qualitative research is directional only. Results cannot be attributed to the overall population under study, with any degree of statistical confidence. The total contracted value of the research was $64,929.80 (including HST).

Political Neutrality Certification

I hereby certify as a Representative of Corporate Research Associates Inc. that the deliverables fully comply with the Government of Canada political neutrality requirements outlined in the Communications Policy of the Government of Canada and Procedures for Planning and Contracting Public Opinion Research. Specifically, the deliverables do not include information on electoral voting intentions, political party preferences, standings with the electorate or ratings of the performance of a political party or its leaders.

Signed

Margaret Brigley

President & COO

Corporate Research Associates

Date: October 30, 2018

Findings from the Canada Child Benefit (CCB) Application Form Testing Qualitative Research reveal that the new prototypes for forms RC66, RC66SCH and CTB9 are considered an improvement over the existing CCB application forms, notably in terms of being easier to understand and easier to complete without assistance. The simpler language and form layout used, helped create that sense of improvement.

That said, the application form prototypes do not completely address all of the challenges previously identified with the existing documents and further revisions are required. While the citizenship and immigration status section on the revised form RC66SCH was considered straightforward and easy to understand, the term ‘resident’ used across all three form prototypes requires clarification. Indeed, what defines a ‘resident’, ‘new resident’, and ‘non-resident’ must be clarified to differentiate those terms from those used in relation to residency or status of a newcomer. Similarly, the expression ‘returning resident’ caused some confusion, notably in terms of the minimum amount of time that needs to be spent abroad and the timeframe.

While the revised marital status definitions were generally clear and easy to understand, there remains confusion about the interpretation of when a common-law partnership begins (whether it is when couples move in together or twelve months after that time). Despite some confusion with the Shared Custody section of the revised form RC66, improvements have been noted regarding how the concept of shared custody is defined, with the inclusion of time proportions (i.e., 40% to 60%) and the examples of situations being helpful. The start date of the shared custody was also well understood. Likewise, the revised form RC66 provides clarity regarding primary responsibility for the care and upbringing of a child.

Participants’ thorough review of the CCB application form prototypes revealed numerous proposed small edits to enhance clarity, as specified later in the Detailed Analysis and Conclusion sections of this report. Most relate to clarifying CCB eligibility, enhancing instructions to complete the forms, using simpler language for select words, reviewing some of the questions to ensure they are specific, and providing a ‘not applicable’ option where relevant. Of note, there was widespread confusion with the mailing instructions of the application form on all three documents, with clients unaware of where their tax services office was located.

Another area of confusion pertained to the sections where income earned outside of Canada needs to be recorded by newcomers. Questions were raised with respect to which income figure should be used, whether net or gross income was to be reported, what exchange rate should be used for income earned outside of Canada, if monthly or yearly incomes were to be considered, and whether the exact amounts or estimates were to be used.

Overall, research findings show that the CRA is heading in the right direction with the redevelopment of the Canada Child Benefit application form, pending some modifications to enhance clarity.

At the present there are three ways to apply for the Canada Child Benefit (CCB), a tax-free monthly payment made to eligible families to help them with the cost of raising children under 18 years of age. Specifically, individuals can apply via Automated Benefits Application (upon registration of a newborn), My Account (online application), and Form RC66 (CCB Application). As part of ongoing efforts to be more client focused, the Canada Revenue Agency (CRA) is revising the CCB application forms to be easier to understand and complete. Specifically, the CRA is looking to update the RC66, Canada Child Benefits Application, the RC66SCH, Status in Canada / Statement of Income and the CTB9, Canada Child Benefit - Statement of Income forms.

CRA has identified several problematic areas with the current forms, including:

It is understood that the CRA has already started work on the redesign; however, the CRA wished to get feedback from members of the target audience before finalizing. Research is needed to confirm that the changes taking place to produce the new form are client-centric and user friendly while still capturing the necessary information to determining a potential recipient’s eligibility for the CCB. It will also determine any issues with the new form and identify any areas of improvement and change to ensure accuracy when completing the form. This research aimed at assessing not only the language used, but also reactions regarding the revised format, design and layout, as well as identifying areas where further clarity/improvements are needed.

With this in mind, the CRA commissioned Corporate Research Associates to conduct qualitative research. The research aimed to examine the following topics, for three specific forms, as outlined below:

RC66

RC66 SCH

CTB9

This report presents the detailed findings of the focus group discussions, a series of conclusions stemming from the research findings, a high-level executive summary and a description of the detailed methodology used. All working documents are appended to the report, including the recruitment screener, the moderator’s guide, and the form prototypes that were tested.

Given the topic and the target audience under study, a series of traditional, in-person focus groups were conducted. Specifically, a total of eight (8) groups were undertaken, across four (4) locations and including both English and French-Canadian residents. More specifically, two groups took place in each of the following markets: Halifax, NS (Atlantic region), Montreal, QC (Quebec region), Toronto, ON (Ontario region), and Vancouver, BC (Western region).

All participants included Canadian residents, aged 19 to 59 years old who have at least one child under the age of 18 living with them. Further, in each market, one group was conducted with newcomers (those who have been in Canada less than 2 years) and one group with members of the general population who have lived in Canada for at least 3 years, including Indigenous people. Further, each group included:

As is normal practice, all participants had not taken part in qualitative research sessions within the past six months and had taken part in no more than 2 focus groups in the past five years. At the same time, people working in a sensitive occupation, including marketing, market research, media, political party or a federal or provincial government department were excluded from the study.

Ten individuals were recruited in each group, with a total of 59 participants attending the groups across locations. In each location, participants received $100 in appreciation for their time. Each group discussion lasted approximately 1.5 to 2 hours.

Qualitative discussions are intended as moderator-directed, informal, non-threatening discussions with participants whose characteristics, habits and attitudes are considered relevant to the topic of discussion. The primary benefits of individual or group qualitative discussions are that they allow for in-depth probing with qualifying participants on behavioural habits, usage patterns, perceptions and attitudes related to the subject matter. This type of discussion allows for flexibility in exploring other areas that may be pertinent to the investigation. Qualitative research allows for more complete understanding of the segment in that the thoughts or feelings are expressed in the participants’ ‘own language’ and at their ‘own levels of passion.’ Qualitative techniques are used in marketing research as a means of developing insight and direction, rather than collecting quantitatively precise data or absolute measures. As such, results are directional only and cannot be projected to the overall population under study.

Although the RC66 was considered relatively straightforward, participants offered multiple suggestions for enhancing the form’s design.

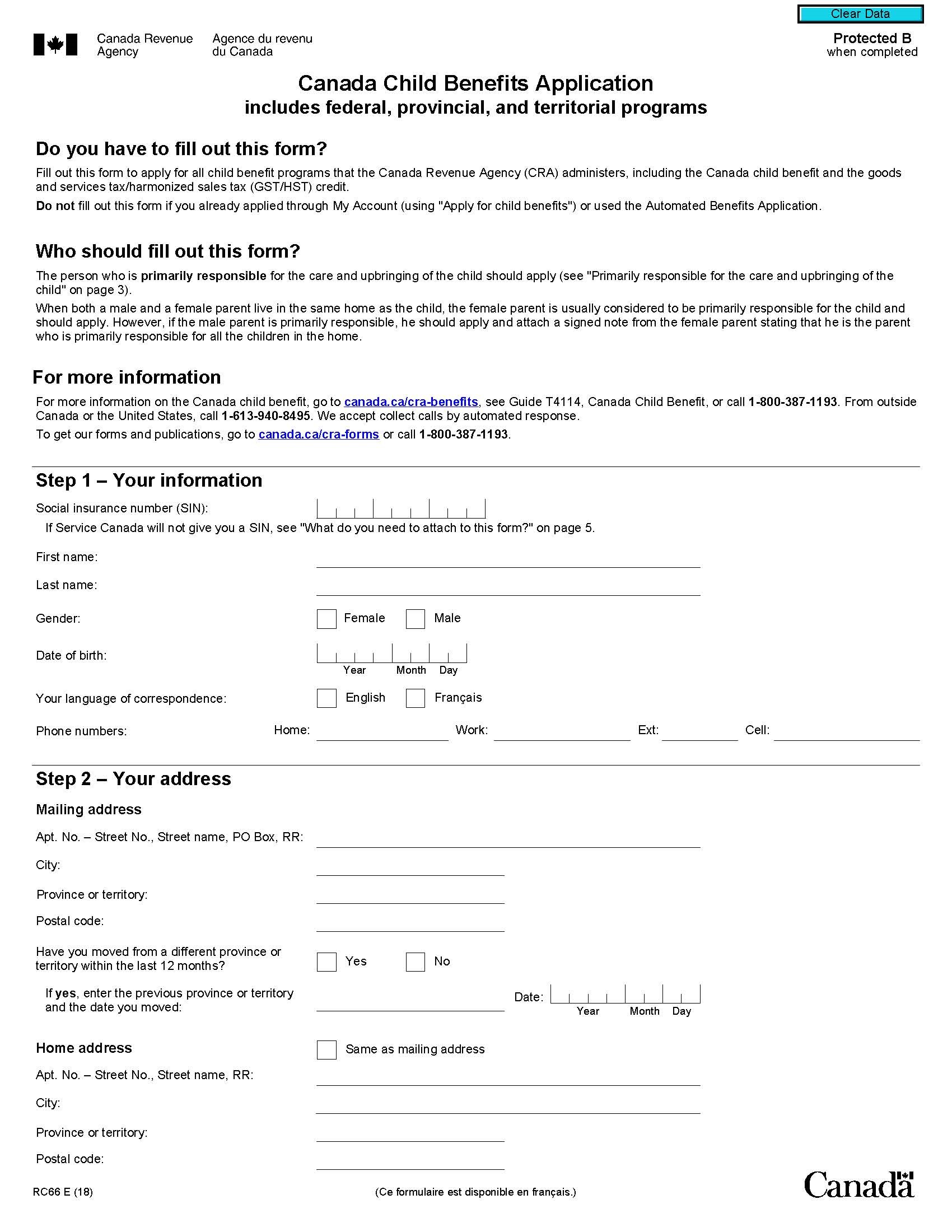

To begin discussions, participants were informed that The Canada Revenue Agency is currently updating and revising a number of its forms to make them easier to understand and complete. Across locations and audiences, participants were provided with a copy of the newly redesigned form prototype for the Canada Child Benefits Application Form (RC66) and asked to complete the form in its entirety, but without providing any personal information. Following form completion, but prior to group discussion, participants shared their overall perceptions of the form via an individual exercise sheet.

The following discusses overall reactions to the RC66 form’s design, as well as input on each of its various sections. For each section, a summary of suggested modifications is provided for consideration, based on the analysis of findings and recommendations from participants.

Overall, across locations and audiences, the form was generally considered easy to understand, straight forward, and something that most could fill out on their own without assistance. That said, newcomers typically experienced a greater level of confusion with the form. In addition, perhaps indicative of the fact that English or French was not their mother tongue, many took notably longer to complete the form during the focus group exercise.

Across audiences, the form was consistently considered as lacking sufficient direction in some areas and a wide range of suggestions were made to improve readers’ comprehension and clarity of the form, as outlined below.

The top sections of the application (Do you have to fill out this form?; Who should fill out this form?; and For more information) were generally understood, but deemed to be lacking. In particular, it was felt the form should clearly outline general eligibility for the Canada Child Benefits under the Do you have to fill out this form section. Across locations, participants questioned who is eligible to receive the benefits, and this was especially of interest to newcomers who may or may not have permanent status in Canada. It was felt that information on eligibility should precede all other information on the form, allowing residents to quickly assess if they could request the benefit.

In both Halifax and Montreal, a few participants believed that some people, notably those new to Canada, may be confused by the statement referencing My Account or the Automated Benefits Application as the statement does not clearly explain what they are, or indicate where to find more information.

When considering ‘Who should fill out this form?’ some participants considered it dated and not necessarily relevant to state that the female parent is usually considered primarily responsible for the child, especially given the diversity of today’s family composition and shared parental responsibilities. In a few instances, participants felt annoyed and to a lesser extent offended with this assumption.

The information provided in ‘For more information’ was generally considered clear and complete, as presented, although one newcomer questioned if there would be someone who could help them through the process, if needed. One participant felt it would be helpful to include the hours that the phone numbers (1-800#) could be called. In a few instances, it was believed that a template for the requested ‘signed note’ should be made available, including a list of what information should appear and acceptable document format (i.e., handwritten).

|

RC66 – Introduction - Suggestions:

|

Steps 1 and 2 were generally considered clear and complete as presented. Across locations, no questions asked in these sections were deemed problematic. That said, a few participants felt there may be merit in including basic instructions for completion prior to Step 1, directing people to print in capital letters, print legibly and perhaps specify to mark a box with an ‘X’. A few newcomers questioned why middle name was not included, given that they were used to having to provide a middle name on most documents. A number of participants suggested to add an ‘other’ or ‘prefer not to say’ response category for the gender.

In both Halifax and Montreal, newcomers were unfamiliar with the term PO Box and the acronym RR and suggested that these be spelled out. At the same time, it was suggested to specify that Canadian provinces or territories were referred to in the question Have you moved from a different province or territory within the last 12 months?, as some felt the word territory referred to a country.

Perhaps due to a lack of instruction, or because it is positioned in the middle of the page on the same level as the sub-section title, a few participants did not select the box ‘Same as mailing address’ to indicate that their mailing address and home address were the same. It was therefore recommended to move this line just below the Home Address section title, or to change the statement to say ‘Select this box if your home address is the same as your mailing address’. Of note, one participant in Montreal mentioned that most forms ask for the home address before the mailing address, thus suggesting they be switched on this form for ease of reference.

|

RC66 – Steps 1 & 2 - Suggestions:

|

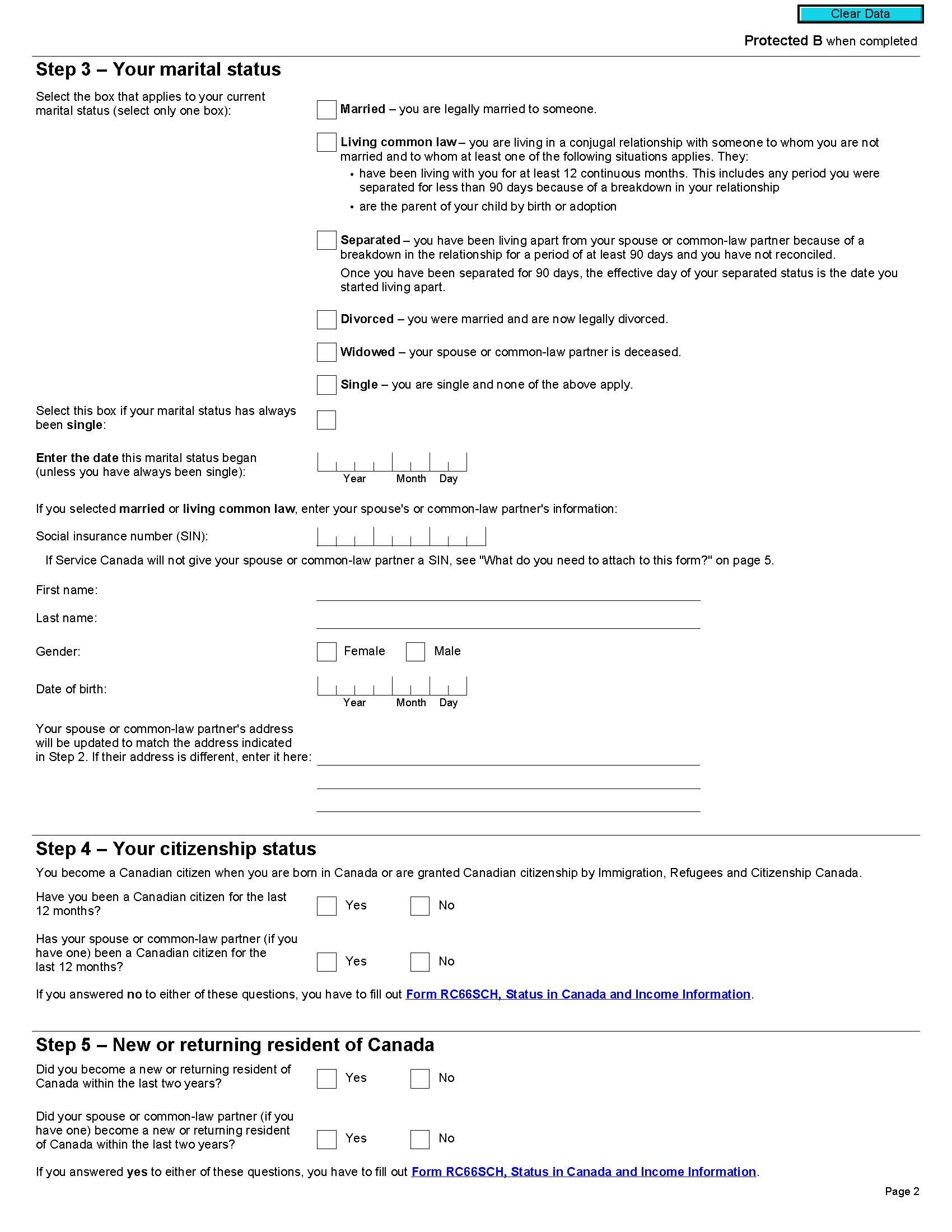

This step on the form presented a number of challenges for participants. To begin, a few participants missed that only one box should be checked to indicate marital status, and when completing the form checked multiple boxes to describe themselves. It was felt that greater prominence should be given to your current marital status, under the title ‘Step 3’ to provide increased clarity.

For most, the categories were clear as outlined and participants typically checked the status that currently describes them. That said, participants were consistently confused as to why two separate boxes were included relating to single status. The second box (shown to the left on the form) was considered redundant, unnecessary, and serving no purpose. It was suggested to move it underneath the ‘single’ paragraph to position it as a follow-up question to the selection of current marital status.

Newcomers whose mother tongue was not English identified a number of words in this section that were problematic, including ‘conjugal’, ‘breakdown’, ‘common-law’, and ‘reconciled’. More simplistic language was needed to ensure greater understandability.

Another problem consistently identified in Step 3 was the question asking for the ‘date this marital status began’. This question caused confusion in that some interpreted ‘marital status’ to mean marriage, regardless of whether or not they were currently married. Accordingly, some who were divorced or widowed included their original date of marriage when completing this question. For greater clarity, it was suggested that the form specify ‘Enter the date of ‘your current status’ (rather than the words ‘this marital’…).

Further, those in a common law relationship were unsure what date to include given that they didn’t have a ‘start’ date much like a marriage. Some entered the date the couple moved in together, while others entered the date twelve months prior to the form being completed, based on the status’ definition.

The final section of Step 3 asked for information on a person’s spouse or common-law partner. For many, this request was not clearly differentiated from the other section of this Step and many provided the information even if not necessary (i.e. if divorced). In multiple locations, it was suggested that this portion should be set in a separate box or shaded area within the Step, with inclusion of a check box that says ‘not applicable’. That will ensure it is skipped when appropriate.

In addition, to provide a greater ease of completion, it was suggested that this inset box should include the information on ‘what do you need to attach to this form’ if Service Canada will not give your spouse or common-law partner a SIN, rather than directing them to page 5 of the form.

|

RC66 – Step 3 – Suggestions:

|

While the questions asked in Steps 4 and 5 were generally understood, participants felt the current design was somewhat confusing and unprofessional as presented.

To begin, use of the terminology ‘if you have one’ in Steps 4 and 5 when asking about a spouse or common-law partner was deemed unprofessional to some. Rather, it was suggested that a ‘not applicable’ or ‘N/A’ option should be included for those questions.

When considering Step 5, many participants questioned what a resident is. This caused confusion for newcomers in particular given that they are used to specific meanings for different types of residency. Some were unsure whether a resident was a landed immigrant, a temporary resident, a permanent resident or a temporary worker. Others felt it would be more simplistic to ask the content of these two steps at the beginning of the form (under a new eligibility section), e.g. ‘are you a Canadian citizen?’, and where the definition of the term ‘resident’ as used in the form would be clearly outlined.

Many were also unsure of who would qualify as a returning resident. Specifically, it was suggested to specify what time period needed to be spent abroad to be considered a returning resident.

Finally, while participants appreciated that the Steps clearly indicated that, depending on their responses, they may need to fill out Form RC66SCH, it did not indicate where they would get the forms. Providing direction on where they can find the forms is needed.

|

RC66 – Step 4 & Step 5 – Suggestions:

|

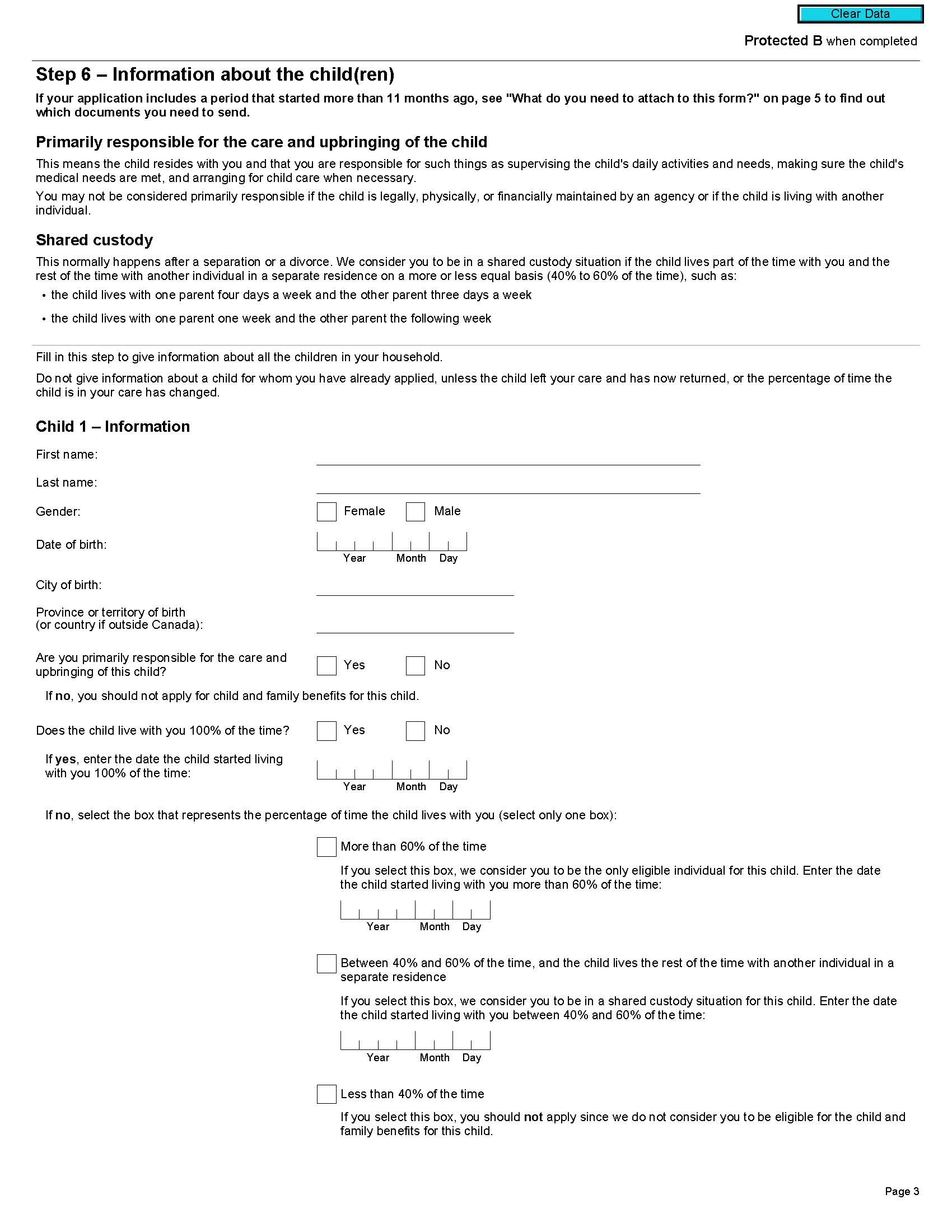

The introduction for Step 6 proved problematic to many. The first sentence ‘If your application includes a period that started more than 11 months ago…’ was confusing to many and participants questioned what it was trying to say. Newcomers were especially confused with the terminology ‘a period that started’ and unsure what it meant. Most felt it could be simplified by stating more than ‘a year ago’, if that is indeed what it is trying to accomplish. It should be noted that confusion was expressed in both English and French groups.

Inclusion of the percentages ‘(40% to 60% of the time)’ was considered helpful to most in explaining what a shared custody situation includes. Some, however, saw those percentages as examples of what ‘more or less equal basis’ would include rather than an accurate definition, particularly given that the words ‘such as’ were included following the percentages. Some were unsure how you would calculate the percentage time of shared custody (days, hours, weeks), although those who were in shared custody situations felt it is clearly understood by those living in that situation. It was suggested to include percentages for each of the two examples provided, thus helping residents to calculate percentages to days/weeks.

Once again, a number of participants across multiple locations questioned why a middle name was not included on the form. This was considered most important among newcomers, as in some cultures, children of the same family have the same given name.

Again, the gender question should provide an option to refuse to answer or an ‘other’ response category.

Inclusion of the question ‘if yes, enter the date the child started living with you 100% of the time’ after asking ‘Does the child live with you 100% of the time’ was confusing as presented. Many felt that to most, the child would likely have started living with parents at birth. Accordingly, they found it redundant to have to record the birth date again. It was suggested that a box be presented as another response option that says ‘from birth’, to simplify form completion.

Including the question ‘are you primarily responsible for the care and upbringing of this child… (if no, you should not apply…)’ caused frustration for some as it was considered too late in the form to provide that direction. Instead, it was felt that should be clearly outlined at the beginning of the form (under who should fill out this form), and should be deleted from Step 6. Similarly, those checking ‘less than 40% of the time’ were directed that they should not apply. This was also considered too late in the form for that advice and participants reiterated that clarity at the beginning of the form would be best.

A few felt that the question asking if they are primarily responsible for the care and upbringing of this child could be confusing for those in shared custody and should be reworded to specify ‘based on the definition provided above’.

In terms of assessing the percentage of the time the child lives with you, it was suggested to specify that the date to be entered should be the date appearing on the custody agreement if one was available.

When considering the provision of information on multiple children on the form, it was felt that the form should allow for more than two children without requiring an additional form. More specifically, it was suggested that the Application be simplified by including a well-designed table on one page of the Application that clearly asks information for four or five children. Such a table would include a column for each child and would reduce paperwork, limit the Application’s length, and eliminate the need for an additional form.

|

RC66 – Step 6 - Suggestions:

|

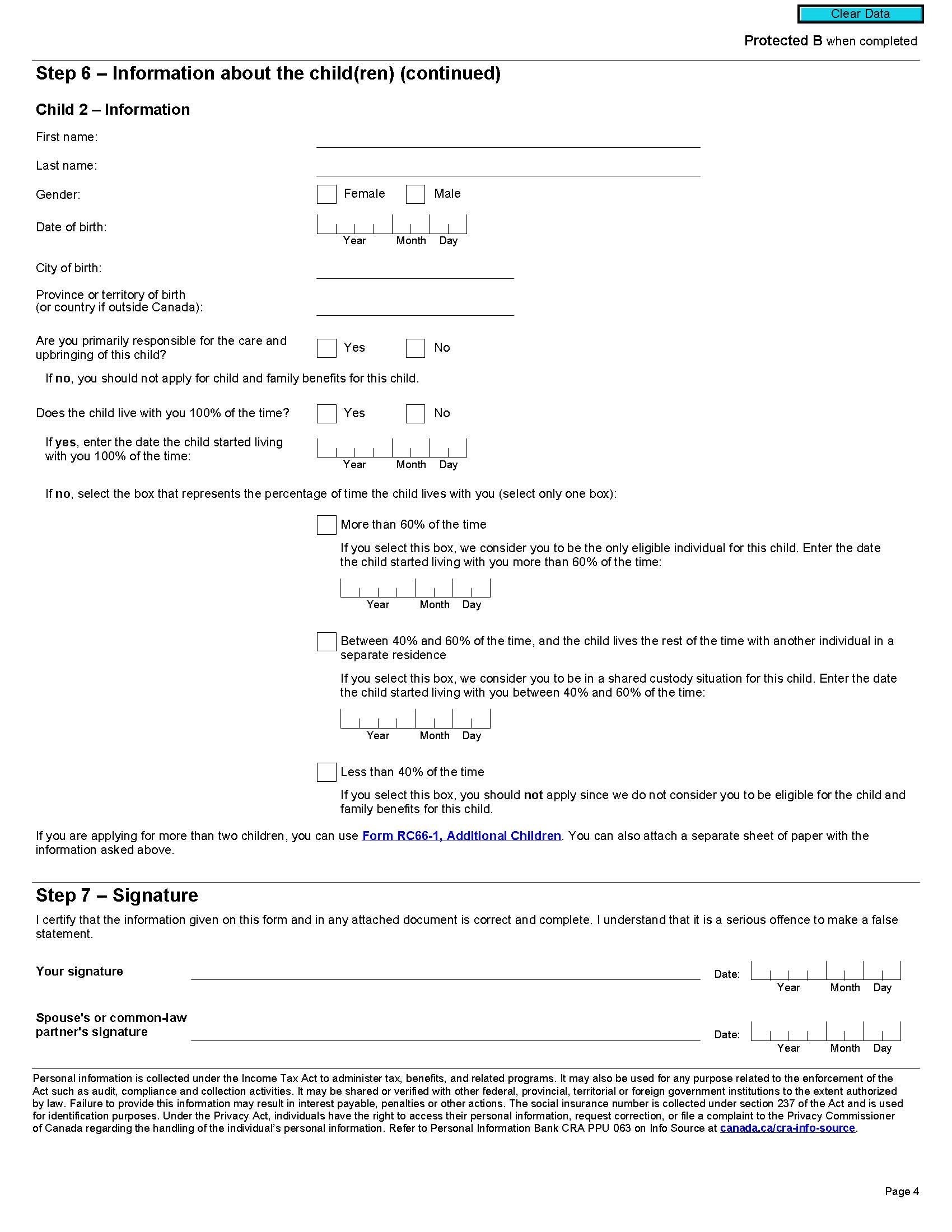

While Step 7 was considered easy to understand for an Applicant, there was some confusion as to when a signature is required for a spouse or common-law partner. Some participants questioned if a signature is required if separated or divorced. Others felt the form was missing a ‘not applicable / N/A’ option next to a spouse’s signature.

|

RC66 – Step 7 - Suggestions:

|

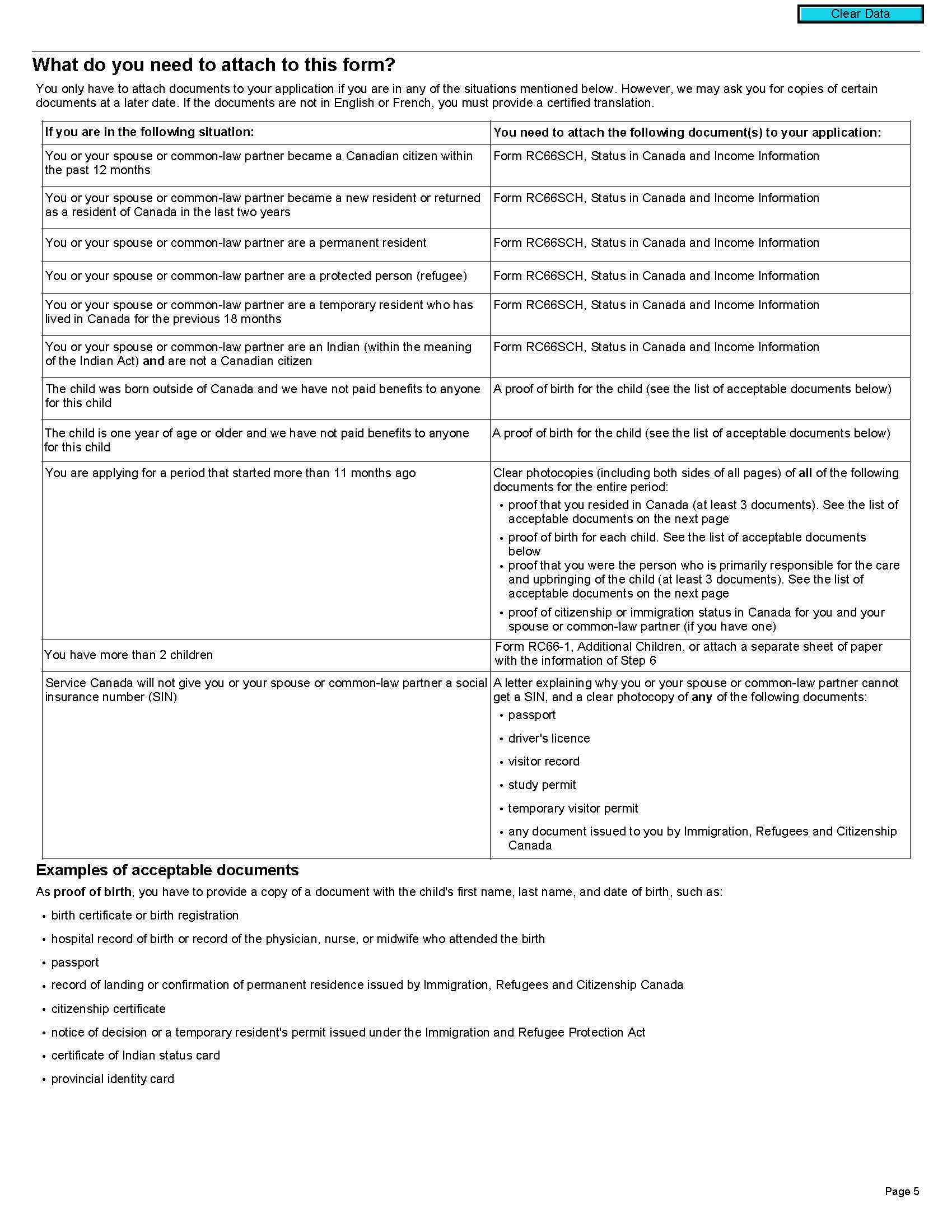

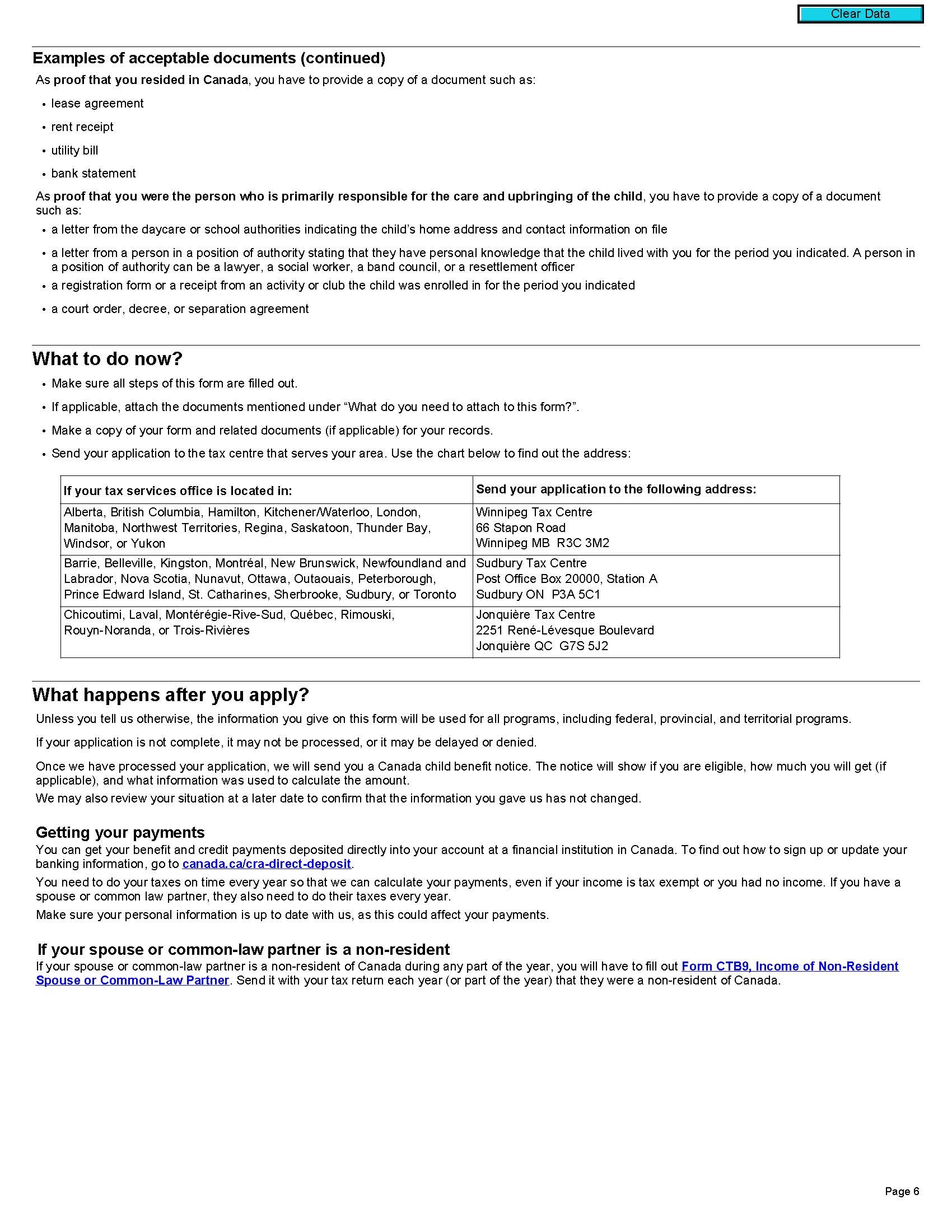

Page five of the Application provides information on what needs to be attached to the form. While participants appreciated having a table that outlines what attachments are required, the table proved problematic as those in the general population group could not easily identify if something was required. A number of participants questioned what is needed ‘for a typical Canadian citizen applying for one child’. Most spent time reviewing the table to see if any of the situations applied. It was felt greater clarity was needed at the top of the table regarding who should consult the information to eliminate the need for unnecessarily going through table in detail. Indeed it was suggested that a situation be listed such as ‘if you are a Canadian citizen applying for the first time for a child that you have full custody of’. Participants wanted to see their situation listed in the table, even if no attachment is necessary. At the same time, there was a desire to have the situations referred to elsewhere in the form listed in the same order in which they appear. For example, the last situation listed in the table on page 5 (SIN missing) is the first to be referrenced on the form at Step 1 and thus should appear at the top of the table on page 5.

The table was criticized by some for a number of inconsistencies or lack of clarity. To begin, participants wondered why examples were included within the table for some situations (i.e. for situations if ‘applying for a period that started more than 11 months ago’ or if ‘Service Canada will not provide a spouse’s SIN’), but not for others (for proof of birth, proof that you resided in Canada or proof that you are primarily responsible for the child). It was felt that examples should be treated consistently.

Further, some of the situations were not clearly understood as articulated. In particular:

When a list of acceptable documents was provided, it was not always clear for participants how many items needed to be attached. This was especially confusing for some newcomers who did not interpret ‘provide a copy of a document’ or ‘a proof’ as only providing one of the listed items. Many indicated that they would attach copies of all available documents as they would not want their application to be returned as incomplete. Further, they were confused when they were unsure what some of the items were (e.g. certificate of Indian status card; provincial identity card in Quebec). In Montreal, the expression ‘reçu de location’ was not well understood and should be replaced by ‘une preuve de paiement de loyer’ or ‘un reçu pour votre loyer’. It was also suggested to clearly indicate what contact information is required on the letter from the daycare or school authorities (e.g., parents’ names, home address, telephone numbers). Some criticized Canada Revenue Agency for being vague in what needs to be attached as a way to delay the process and avoid making payments.

|

RC66 – What do you need to attach to this form - Suggestions:

|

The final page of the form provided information on what applicants do next. Across groups, participants consistently offered a number of comments and suggestions about this section.

Most notably, it was felt that the application would be more user friendly if it provided a simple check list in this section, with boxes for applicants to check. A number of participants referenced how such a summary is provided on passport applications and appreciated that it provided an effective summary and reminder of what they should do next. Adding such a feature would provide for an easy to complete final step, and create a sense of control or certainty for the applicant.

Under ‘what happens after you apply’, a number of participants across audiences felt some key information was lacking. To begin, referencing that information will be used for ‘all programs’ caused some concern for a few applicants, as they were unsure what other programs might be impacted by providing the information. One participant questioned if the form would impact their disability funding. For increased clarity, some felt it would be helpful to outline which programs would be affected, or at least reference where they could find a list of impacted programs. Montreal participants mentioned that the word ‘exonérés’ is not commonly used and newcomers in particular did not know its meaning.

In addition, participants consistently criticized the form for not indicating a timeframe for a response from Canada Revenue Agency. Multiple newcomers commented that in the absence of a timeframe, they would likely follow up within a week to see what progress had been made. While they would not want to push the government inappropriately for a response, having a time period outlined would eliminate premature follow-up. It was suggested that some estimate of response time be provided as a guide. At the very least, participants consistently requested that a receipt notification be sent, thus confirming their application was being processed.

Presentation of where to send your completed form on the application was considered odd in that it outlined addresses by an applicant’s local tax services office. This, in essence, assumed that applicants know or understand where their local tax services office is located. Most concurred that they had no idea where their tax services office is located, as they do not typically deal with it directly. Further, the table, as presented, included both provinces and cities in its layout, which caused some confusion. It was felt that the table would be easier to understand if it based locations on where an applicant lives, rather than where their local tax services office is located.

The final mention on the Application (‘If your spouse or common-law partner is a non-resident’) was considered out of place to some and it was felt that it would be more applicable if included in Step 3.

|

RC66 – – What to do now - Suggestions:

|

Although most newcomers deemed the RC66 SCH easy to understand, clarification is needed related to income.

Newcomer participants were also provided with a copy of the newly designed form prototype for the Status in Canada and Income Information Form (RC66 SCH) and asked to complete it without providing any personal information. Following form completion, but prior to group discussion, participants shared their overall perceptions of the form via an individual exercise sheet.

The following discusses overall reactions to form RC66 SCH’s design, as well as input on each of the form’s various sections. For each section, a summary of suggested modifications is provided for consideration.

Across locations newcomers generally considered the RC66 SCH easy to understand. That said, most felt they would likely seek some assistance in its completion, given that the form required provision of specific income figures that many had questions on (as discussed below).

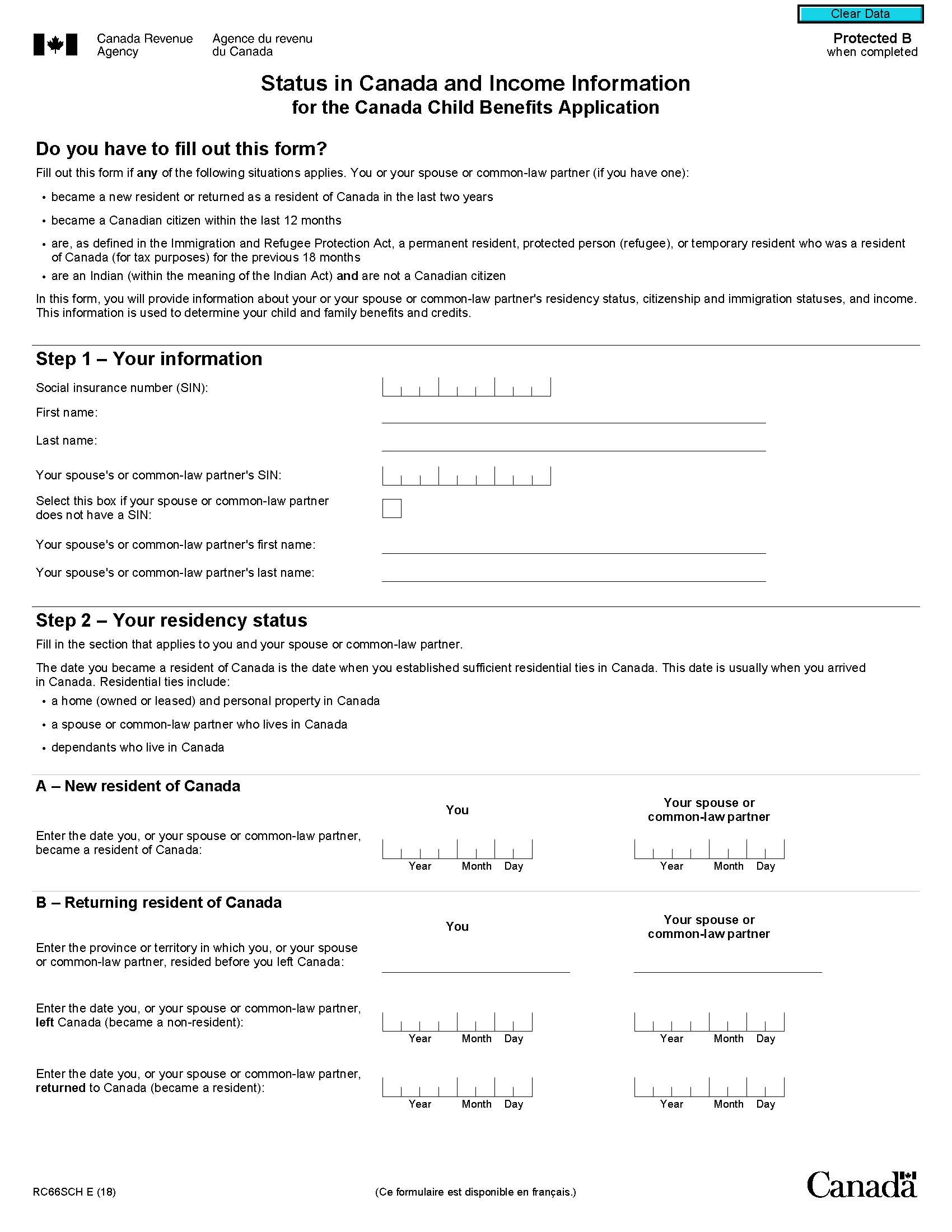

The information included in this section of form RC66SCH generally provided sufficient detail for most newcomers, giving them the necessary background to understand if they needed to complete the form. Only a few questions were raised, namely what is referenced by Indian (i.e. Indian from India or Indigenous), and whether they should complete the form on their own or together with their spouse. As with the RC66 form, a number of participants questioned how new resident and returning residents were defined and expressed a desire for a clear definition.

|

RC66SCH – Introduction - Suggestions::

|

Step 1 on the RC66 SCH was generally considered clear and straight forward. Consistent with comments mentioned relating to the RC66, newcomers suggested that a middle name should be included (given that it is typically required on their passport or other official documents). In addition, it was felt that questions relating to a spouse or common-law partner should be included in an inset box or shaded area where there is a clear option to check ‘if applicable’. As designed, the form assumed that all applicants would have a spouse or common-law partner.

|

RC66SCH – Your Information - Suggestions:

|

When reviewing Step 2 of the form newcomers posed a number of questions. Most notably, participants wanted greater clarity on how a resident is defined. The term resident was considered vague and unclear to many as they were used to more technical terms relating to residency or status. Some questioned if temporary residency, someone who is visiting Canada, or someone who owns property in Canada but lives abroad most of the time would be defined as a resident. Newcomers mentioned that it is common for newcomers to stay with a relative or friend for months or years when arriving, thus they questioned if these people would be defined as a new resident.

Accordingly, some were unsure what date they would enter when asked for the date they became a resident. In particular, they questioned if it was the date they physically arrived in the country or a date when they received some type of formal residency, refugee status or work permit / status, or the date they established residential ties. It was suggested that the statement ask the date ‘you arrived in Canada’ rather than when ‘you became a resident of Canada’ (‘date d’arrivée au Canada’ in French). A few newcomers felt that referring to the landing date would be clearer, as this is often the date requested on other official documentation.

Many were also interested in a clearer definition of what defines a returning resident. It was suggested to clarify if there is a minimum amount of time that needs to be spent abroad and the timeframe it applied to (the fiscal year under consideration or a longer period). This was considered most important as newcomers indicated that in some instances, immigrants return to their home country from time to time to settle their situation before returning to Canada to live permanently. Again, it was suggested to specify under section B that the applicant should consider only Canadian provinces or territories.

Once again, under both sections A and B in Step 2, some participants felt it would be helpful to have a ‘not applicable’ on the form where it asks for information on a spouse or common-law partner.

|

RC66SCH – Your Residency Status - Suggestions:

|

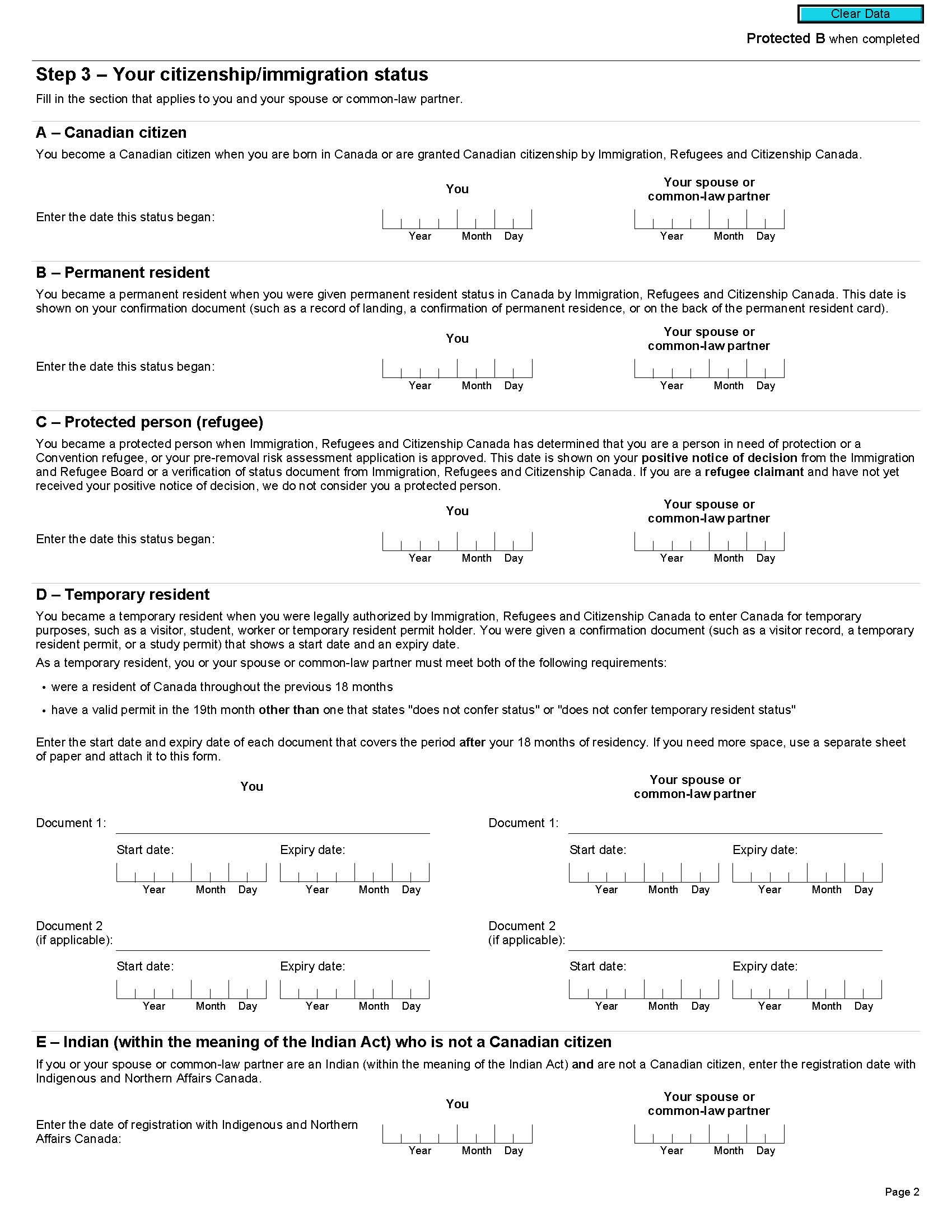

For the most part, newcomers were able to complete Step 3 of the form without problems. That said, across locations participants questioned if they should complete all sections that ever applied to them or only one section that currently applies. Greater clarity is needed in the instructions (i.e. ‘fill in only the section that currently applies to you and your spouse or common-law partner’).

As previously mentioned, newcomers also felt that ‘not applicable’ should be added to any line of questioning asking for information about a spouse / common-law partner.

Finally, in section E, newcomers want clarity as to whether Indian refers to a native Indian (Indigenous) or someone from India.

|

RC66SCH – Your Citizenship / Immigration Status - Suggestions:

|

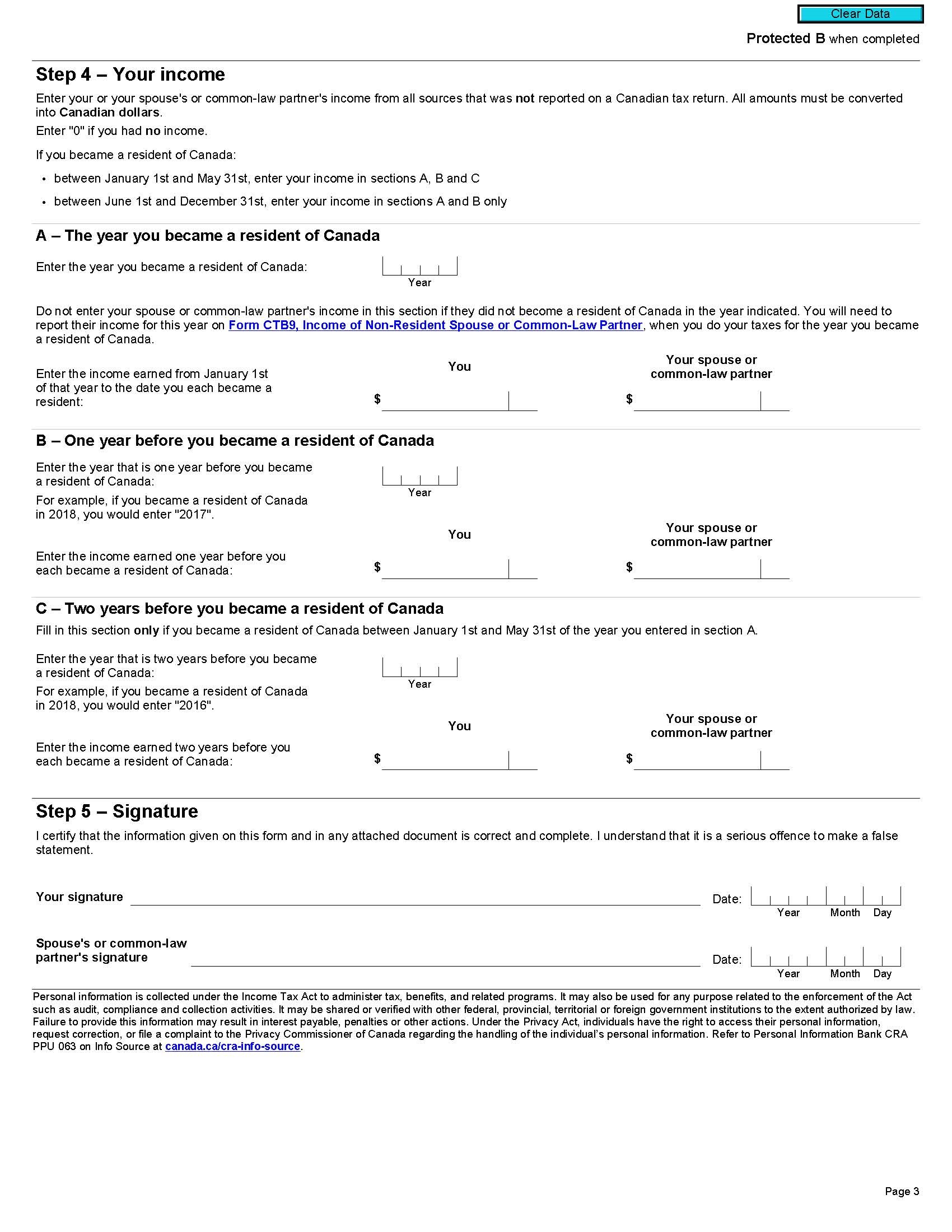

Participants generally understood that the section asked to record income that was not reported on a Canadian tax return. That said, there was some confusion as to how the conversion should be calculated when converting their income into Canadian dollars. In particular, they questioned if the exchange rate would be the current exchange rate or that for the timeframe reported (e.g. one or two years earlier). This was especially important given notable fluctuations in currencies in recent years. At the same time, a few were unclear if the net or gross income were to be recorded, thus suggesting this should be clarified. Of note, some of the newcomers were under the impression that exact amounts were to be recorded, while others felt that an approximation was acceptable. As such, it should be specified if estimates are acceptable.

A few newcomers were unsure how to respond where the form asked them to ‘enter the income earned from…’ and questioned if they should report monthly income or annual income. It was felt that including the word ‘total’ (enter the total income earned…) would provide greater clarity. Further, one participant questioned if proof of income was required. Others felt it would be very difficult in some instances to provide any evidence of income.

Instructions on which sections to complete were clear. That said, a few suggestions were made to make the section easier to complete. Under section A, B, and C, where it asks to enter the income earned, it was recommended to specify that it references income not already reported on a Canadian tax return. Although this is already mentioned at the beginning of the section, it was considered important to include such reminders where relevant.

As previously mentioned, some newcomers felt that a ‘not applicable’ or ‘if applicable’ option should be included whenever information is asked for a spouse or common-law partner.

It should be noted that a few newcomers indicated that the date of Canadian residency can be confusing, with some referring to the landing date and others using the date that appears on their permanent resident card.

|

RC66SCH – Your Income - Suggestions:

|

Consistent with comments outlined on Step 7 of the RC66 form, this step was considered easy to understand for an applicant. That said, as previously mentioned, there was some confusion as to when a signature is required for a spouse or common-law partner. Some participants questioned if a signature is required if separated or divorced. Others felt the form was missing a ‘not applicable / N/A’ option next to a spouse’s signature.

|

RC66SCH – Signature - Suggestions::

|

The final page on this form was generally well understood and considered complete. That said, as previously mentioned, it was suggested that adding a checkbox as a quick completion reference could be helpful.

Once again, presentation of where to send your completed form on the application was considered odd as designed in that it outlines addresses by an applicant’s local tax services office. As previously mentioned, this approach assumes applicants know or understand where their local tax services office is located. Most concurred that they had no idea where their tax services office is located. Further, having the table include both provinces and cities in its layout caused some confusion. As mentioned, it was felt that the table would be easier to understand if it based locations on where an applicant lives, rather than where their local tax services office is located.

Information outlining ‘what do you need to do to get your benefit and credit payments’ and ‘for more information’ was generally well understood and considered clear as presented. No suggestions were made to enhance those portions of the form.

|

RC66SCH – What to do now? - Suggestions::

|

Form CTB9 was generally deemed easy to complete, although further clarification on the definition of resident/non-resident and on the income to report are desired.

Newcomer participants were also provided with a copy of a third form for review, namely the Income of Non-Resident Spouse or Common-law Partner (CTB9) and asked to complete that form without providing any personal information. Following form completion, but prior to group discussion, participants shared their overall perceptions of form CTB9 via an individual exercise sheet.

The following discusses overall reactions to form CTB9’s design, as well as input on the form’s various sections. For each section, suggested modifications are provided for consideration.

Across locations, newcomers generally considered the CTB9 easy to understand and few would require any type of assistance in its completion.

The introduction of the CTB9 was generally considered clear and straight forward. While most understood who needed to fill out the form based on the introduction, a few felt that the terms ‘customarily’ or ‘routinely’ were not easily understood and should be written in simpler language.

There was, however, some discussion as to what is considered a ‘non-resident for tax purposes’, mostly related to the misunderstanding or vagueness of the terms ‘routinely’ and ‘customarily’. Such terms open the door to interpretation which made some newcomers uncomfortable and worried that their application may be denied if they do not answer the question accurately. Throughout the discussion, there was clear evidence that newcomers are looking for clear and precise instructions to assist them in filling out the application.

A few newcomers also suggested it would be helpful to indicate if the form needs to be filled out if a spouse did not have any income earned outside of Canada.

|

CTB9 – Introduction - Suggestions::

|

This first step on the form was clear to most, and no suggestions for improvement were offered. That said, one newcomer asked what months the tax year would specifically be referring to since in some countries the tax year may not be interpreted as the calendar year, as is the case in Canada.

|

CTB9 – Your Information - Suggestions:

|

Step 2 on the CTB9 was considered straightforward and easy to complete. Consistent with comments mentioned relating to the RC66 and RC66SCH, newcomers would like to see space for a middle name included.

When considering the address format presented, once again a few newcomers in most locations were unsure what PO Box and RR means.

|

CTB9 – Your Information - Suggestions:

|

This section was generally considered easy to understand and complete. That said, many were under the impression that non-residents could not have a SIN, thus questioning the relevance of asking for this information. These perceptions go back to a misunderstanding of the definition of a resident/non-resident of Canada under the application process.

|

CTB9 – Your spouse’s or common-law partner’s information - Suggestions:

|

This section was considered somewhat problematic in determining who should be included, what sections to complete (A, B, or C) and what income is to be considered. Again, the same questions regarding the currency exchange rate to use and the type of income (gross or net) to consider were mentioned. At the same time, when asked what income they would consider, it was felt that any source of revenue should be included.

There was also confusion with who should fill out this section, as the third bullet in the section’s introduction mentions that section C should be completed if a spouse or common-law partner became a resident of Canada in the year, yet the instructions at the beginning of Form CTB9 specify that the form must only be completed if a spouse or common-law partner was a non-resident of Canada. As with previous forms, the definition of resident/non-resident of Canada should be clarified.

In a few instances, newcomers were unclear what sections (A, B, C) they needed to completed, and if multiple sections could apply or if only one was to be selected. This confusion may result from the instructions which specify when section A should ‘only’ be completed, but does not specify the same for section B or C. Adding the word ‘only’ for those sections’ instructions would help indicate that only one of the three sections needs to be completed. Alternatively, it should be clarified when more than one section needs to be considered.

As with other forms, there was some confusion with which date to enter, that is identifying when a spouse became a non-resident or a resident.

|

CTB9 – Your spouse’s or common-law partner’s income - Suggestions:

|

As previously discussed, it was suggested that increased clarity could be provided to indicate when a signature is required for a spouse or common-law partner. Further, adding an option of ‘not applicable / N/A’ next to a spouse’s signature was needed given that all those completing the form may not have a spouse / common-law partner.

|

CTB9 – Signature - Suggestions::

|

As previously discussed, the main point of confusion with this section is newcomers’ difficulty in identifying where their tax services office is located, and the tendency to identify a city or province listed that represents where they live.

|

CTB9 – What to do once your form is filled out? - Suggestions::

|

The following conclusions are drawn from the detailed analysis of the study’s findings.

The concepts of new resident, resident and non-resident of Canada and that of a returning resident should be clarified across all forms.

Throughout the application forms, the concepts of new resident, resident and non-resident of Canada and that of a returning resident were found confusing and would benefit from being more clearly defined. The term resident was considered vague and unclear, as the term is typically used on formal documents in the context of residency or status of a newcomer, rather than to define an inhabitant of the country. Even when the term ‘resident’ is understood as someone who lives in Canada, questions were raised as to whether or not temporary residency, someone who is visiting Canada, or someone who owns property in Canada but lives abroad most of the time, would be defined as a resident. Newcomers mentioned that it is common for new arrivals in Canada to stay with a relative or friend for months or years thus they questioned if these people would be defined as a resident or new resident.

Similarly, there is an expressed need for better defining what constitutes a returning resident, notably in terms of clarifying if there is a minimum amount of time that needs to be spent abroad and the timeframe it applies to. Defining those criteria was considered particularly important to newcomers since immigrants can return to their home country multiple times for short trips to settle their situations while in the process of relocating to Canada. Providing clear definitions would remove any potential ambiguity for applicants.

A number of edits to instructions and wording should be considered across all three forms to improve clarity.

For any of the forms, participants were keen to quickly assess benefit eligibility, identify who should fill out the application, and obtain basic instructions on how to fill out the form (e.g., print in capital letters, and mark boxes with an ‘x’). As such, consideration should be given to ensure that the introductory part of all three forms includes this information.

Throughout the forms, some of the instructions should be clarified. For example, where provinces and territories are referenced, it should be mentioned that these are Canadian provinces and territories so as not to be confused with other countries. Where relevant, a ‘not applicable’ or ‘prefer not to say’ or ‘other’ response option should be provided (e.g., gender). In instances where a date is required (date of marital status and date child started living with you), clarification should be provided to ensure consistency in what date is selected.

The level of language used throughout the three forms was generally considered simple and easy to understand. That said, acronyms should be spelled out (e.g., RR, PO Box) and some of the wording simplified for those whose mother tongue is not English or French (e.g., conjugal, breakdown, common-law, reconciled, customarily, routinely). At the same time, the definitions of common-law partner in the RC66 Step 3 – Your Marital Status section should be reworded for added clarity.

Finally, instructions on where to send the completed application was widely misunderstood. Specifically, despite being instructed to look for the location of their tax services office listed in the table, participants consistently looked for the place where they live. This was primarily because the tax services office locations are not well known. As such, instructions need to be clarified, and consideration should be given to inform applicants of how to find out where their local tax services office is located.

Although the RC66 was considered relatively straightforward, participants offered multiple suggestions for enhancing the form’s design.

Across locations and audiences, the redesigned Canada Child Benefits Application Form (RC66) was considered an improvement over the existing form, notably in terms of being easy to understand and easy to complete without assistance. That said, participants offered a variety of suggestions to enhance the form’s design. Below is a summary of recommendations from participants for each of the sections on form RC66, for consideration. These are discussed in the detailed findings section of this report.

Introduction:

Step 1 and 2 – Name and Address:

Step 3 – Your Marital Status:

Step 4 and 5 - Your Citizenship Status / New or Returning Resident of Canada:

Step 6 – Information about the child(ren):

Step 7 – Signature:

Final sections of the form:

Although most newcomers deemed the RC66 SCH easy to understand, clarification is needed related to income.

In general, the RC66 SCH was considered easy to understand although assistance may be required to complete the form, especially to determine which income figures to use. This was one of the most problematic aspects of this form. Questions were raised regarding the type of income to include in the total, whether net or gross income were to be reported, what exchange rate should be used for income earned outside of Canada, and whether the exact income amounts or estimates were to be used. Whether to report monthly or annual income was also unclear and some questioned if proof of income was required, although this was felt to be difficult to obtain in some instances.

Below is a summary of recommendations from participants for each of the sections on form RC66 SCH, for consideration. These are discussed in the detailed findings section of this report.

Introduction:

Step 1 – Your Information:

Step 2 – Your Residency Status:

Step 3 – Your Citizenship / Immigration Status:

Step 4 – Your Income:

Step 5 - Signature:

Final sections of the form:

Form CTB9 was generally deemed easy to complete, although further clarification on the definition of resident/non-resident and on the income to report are desired.

Across locations, newcomers generally considered the CTB9 easy to understand and few would require any type of assistance in its completion. That said, Step 4- Your spouse’s or common-law partner’s income, proved most problematic notably in terms of determining which section to fill out, and how to determine the income to report.

Below is a summary of recommendations from participants for each of the sections on form CTB9, for consideration. These are discussed in the detailed findings section of this report.

Introduction:

Step 1 – Tax Year Information:

Step 2 – Your Information:

Step 3 - Your spouse’s or common-law partner’s information:

Step 4 - Your spouse’s or common-law partner’s income:

Step 5 – Signature:

Final sections of the form:

Canada Child Benefit (CCB) Application Form Testing

Appendix A: Recruitment Screener

Focus groups:

| Toronto, Ontario (ENGLISH) | |||

| Date: | Wednesday, October 3, 2018 | Location: | Quality Response |

| Time: | Group 1 – 6:00 pm (Newcomers - parents) Group 2 – 8:00pm (General Population - parents) |

2200 Yonge Street Suite 903 |

|

| Vancouver, BC (ENGLISH) | |||

| Date: | Thursday, October 4, 2018 | Location: | Vancouver Focus |

| Time: | Group 3 – 6:00 pm (Newcomers - parents) Group 4 – 8:00pm (General Population - parents) |

1080 Howe Street Suite 503 |

|

| Halifax, NS (ENGLISH) | |||

| Date: | Wednesday, October 10, 2018 | Location: | Corporate Research Assoc. |

| Time: | Group 5 – 6:00 pm (Newcomers - parents) Group 6 – 8:00pm (General Population - parents) |

7071 Bayers Road Suite 5001 |

|

| Montreal, Quebec (FRENCH) | |||

| Date: | Thursday, October 11, 2018 | Location: | Ad Hoc Recherche |

| Time: | Group 7 - 6:00pm (Newcomers - parents) Group 8 - 8:00pm (General Population - parents) |

400, boul. De Maisonneuve Ouest Bureau 1200 |

|

Specification Summary:

Hello/Bonjour, my name is____ and I am with Corporate Research Associates, a public opinion and market research firm.

Would you prefer that I continue in English or French? Préférez-vous continuer en français ou en anglais? [IF FRENCH, CONTINUE IN FRENCH OR ARRANGE A CALL BACK WITH FRENCH INTERVIEWER: Nous vous rappellerons pour mener cette entrevue de recherche en français. Merci. Au revoir].

We are conducting a study on behalf of the Government of Canada and are looking for people to take part in a small focus group discussion [DEPENDING ON LOCATION: in English/in French]. All those taking part in this upcoming focus group will receive $100 for their participation. I would like to speak with someone in your household who has a child under the age of 18. May I ask you a few quick questions to see if you are the type of participant we are looking for in this study? This call should take approximately 10 minutes.

Please note, this information will remain completely confidential and you are free to opt out at any time. Thank you.

[IF CRA CONTACT/VERIFICATION NEEDED: Stephanie Jacques-Marhue, Senior Public Affairs Advisor, 613-957-3573]

[IF ASKED WHAT DEPARTMENT SPONSORS STUDY: This research is sponsored by the Canada Revenue Agency. Note that your participation will remain completely confidential and it will not affect your dealings with the Government of Canada, including the Canada Revenue Agency, in any way.]

Gender (By Observation):

1. To begin, are you or anyone in your household currently employed in any of the following sectors?

IF YES TO ANY OF THE ABOVE, THANK AND TERMINATE

2. Into which of the following age groups do you currently fall? Are you…? (Recruit mix of ages.)

3. Including yourself, how many people are currently living in your household? [RECORD] ______

4. [ASK IF 2 OR MORE IN Q3] Do you currently have children under the age of 18 living with you?

5. [ASK IF YES TO Q4] How many children under the age of 18 live with you? Recruit mix.

6. [ASK IF YES TO Q4] Do you have any children who live part of the time with you and the rest of the time with another individual in a separate residence? (Aim for min of 2-3 per group). Recruit mix.

7. Do you currently receive the Canada Child Benefit?

8. Are you currently …? Recruit Mix (1-3); Recruit 4-6 per group (4-7)

9. If employed, ask… What is your current occupation? ____________________________

TERMINATE IF SIMILAR OCCUPATIONS AS IN Q1

10. If employed, ask… in which industry do you currently work? __________________________

TERMINATE IF SIMILAR OCCUPATIONS AS IN Q1

11. Which of the following best describes your marital status? Are you…? Recruit Mix.

12. Which of the following best describes your total household income before taxes last year? Would you say? Recruit Mix.

13. Do you identify yourself as Aboriginal? That is, First Nations, Metis or Inuk (Inuit)? First Nations includes Status and Non-Status Indians under the Indian Act.

14. How long have you lived in Canada? __________ [Newcomers: at most 2yrs; Gen pop: at least 3 yrs)

15.[IF NEWCOMER; LESS THAN 2 YEARS IN Q 14] What do you consider to be your mother tongue or your first language spoken?

16. [ASK ALL] Have you ever attended a group discussion for which you received a sum of money?

17. [IF YES TO Q17] When was the last time you attended a group discussion? _______

18. [IF YES TO Q17] How many groups and interviews have you attended in the past 5 years? _____

IF THEY HAVE BEEN TO A GROUP IN THE PAST 6 MONTHS - THANK & TERMINATE, IF THEY HAVE BEEN TO 3 OR MORE GROUPS IN THE PAST 5 YEARS - THANK & TERMINATE

INVITATION

I would like to invite you to participate in a focus group discussion we are holding at [TIME] on [DATE]. As you may know, a focus group is a research method, which uses an informal meeting to gather information on a particular subject matter, in this case, government programs.

The discussion will include 7 to 10 people and will be very informal. It will last approximately 2 hours; it will begin at [START TIME] and end at [END TIME]. Refreshments [FOR 6:00PM GROUPS: and sandwiches] will be served and you will receive $100 as a thank you for your time. Are you interested in attending?

The group discussion will be recorded for research purposes only. Please be assured your comments are strictly confidential. Are you comfortable with the discussion being recorded?

The discussion will also take place in a focus group room that is equipped with a one-way mirror for observation. There may or may not be observers present, but if there are, they will not know your full name. The purpose is to ensure individuals working on this project are able to hear your thoughts and opinions and take notes without disturbing the group discussion. Would this be a problem for you?

Participants may be asked to read materials and write out responses on their own during the focus group. How comfortable are you in taking part in these activities in (English/French) without assistance if these were part of the focus group? Are you…?

If you require reading glasses, please bring them with you.

Since participants in focus groups are asked to express their thoughts and opinions freely in an informal setting with others, we’d like to know how comfortable you are with such an exercise. Would you say you are…?

We ask everyone who is participating in the focus group to bring along a piece of I.D., picture if possible.

These are small groups and even one person missing will affect the overall success of the group. Once you have decided to attend please make every effort to do so. If you are unable to attend, call_____ (collect) at ________as soon as possible so a replacement may be found. Please do not send anybody to replace you

I would like to remind you that the 2-hour group discussion will begin at [START TIME]. Please arrive 15 minutes prior to the starting time. If you are late, we will not be able to include you in the discussion and you will not receive the $100 gift. The group discussion will end at [END TIME].

Thank you for your time and we look forward to hearing your opinions during the focus group.

ATTENTION RECRUITERS

CONFIRMING

Objectives (not to be shared with participants)

Introduction 10 minutes

Canada Child Benefit Application Form (RC66) 60 minutes

[INCLUDE THIS SECTION IN ALL GROUPS] As you may be aware, the Canada Revenue Agency (CRA) administers a number of child and family benefit programs for residents in Canada, including the Canada Child Benefit and the Goods and Services Tax / Harmonized Sales Tax (GST/HST) Credit. These benefits are non-taxable amounts paid to help eligible families with the cost of raising children under 18 years of age. One thing you all share is that you are a parent or have a child/children living with you.

The Canada Revenue Agency is currently updating and revising a number of its forms to make them easier to understand and complete. Today, I am interested in getting your thoughts on one of the newly designed forms prototype - the Canada Child Benefits application form. I’m going to share with you a draft of this form. Today I’ll be looking for your input to ensure that the form is clear and easy to understand, and that people are able to complete it without difficulty.

Moderator passes out draft form. I’m going to give you about 10-15 minutes to complete the form. As you do, you don’t need to share any personal information – for example if it asks for your Social Insurance Number (SIN number), or your birthdate, you can just make up a number for the purpose of our discussion and the same applies for any information it asks on the form.

Each of you has a highlighter that I’d like you to use. As you fill out the form, if there is something that is confusing or problematic, please highlight it. We’ll use that as your reference when we discuss it in a few moments.

After form is completed: Before we discuss this together, please take a moment and on your exercise sheet, tell me to what extent you agree or disagree with each statement (using a thumb scale). I’ll give you a moment.

Discuss as a group, following the exercise:

Let’s walk through each step of the form:

Step 1 and Step 2 – Name and address

Step 3 – Your marital status

Steps 4 & 5 – Your citizenship status / New or returning resident of Canada

Step 6 – Information about the child(ren)

Step 7 – Signature

Once the form is completed….

Status in Canada and Income Information (RC66 SCH) 30 minutes

[ASK ONLY NEWCOMER GROUPS] As discussed, when completing Form RC66, in Steps 4 and 5, anyone who does not have Canadian citizenship status, or who is a new or returning resident of Canada would have to fill out an additional form – Status in Canada and Income Information.

I’m going to share a draft of that form too, to see if it is clear and easy to understand. Moderator passes out draft form. I’m going to give you about 5-10 minutes to complete this form. As before, you don’t need to share any personal information – for instance when it asks income you can just make up a number for the purpose of our discussion. Once again, as you fill out the form please highlight anything that is confusing or problematic. We’ll discuss in a few moments.

After form is completed: Before we discuss this together, please take a moment and on your exercise sheet, tell me to what extent you agree or disagree with each statement (using a thumb scale). I’ll give you a moment.

Let’s walk through each step:

Step 1 – Your Information

Step 2 – Your residency status

Step 3 – Your citizenship / immigration status

Steps 4 & 5 – Your income / Signature

Income of Non-Resident Spouse or Common-law Partner (CTB9) 25 minutes

[ASK ONLY NEWCOMER GROUPS] In the last form you completed, one other form is referenced – Form CTB9. I’d also like to get your thoughts on that form, to see if it is clear and easy to understand.

Moderator passes out draft form. I’m going to give you about 5-10 minutes to complete this form. As before, you don’t need to share any personal information – you can just make up a number for income for the purpose of our discussion. Again, please highlight anything that is confusing or problematic. We’ll discuss in a few moments.

After form is completed: Before we discuss this together, please take a moment and on your exercise sheet, tell me to what extent you agree or disagree with each statement (using a thumb scale). I’ll give you a moment.

Thanks & Closure

Any final thoughts you would like to share with the Canada Revenue Agency regarding the forms we’ve discussed?

That concludes our discussion. On behalf of the Canada Revenue Agency, thank you for your time and input. Direct them to the hostess to receive the incentive.

Individual Exercise

Form RC66

| This form is easy to understand | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

| I could complete this form without help | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

| It is clear what supporting documentation I need to send | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

| The child information portion (step 6) is clear | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

| I can easily identify the percentage of time the child lives with me | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

| It is clear where I can get more information if I need it | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

| It is clear where I need to send the form once completed | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

Form RC66 SCH

| This form is easy to understand | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

| I could complete this form without help | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

| It is clear where I can get more information if I need it | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

| It is clear where I need to send the form once completed | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

Form CTB9

| This form is easy to understand | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

| I could complete this form without help | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

| It is clear where I can get more information if I need it | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |

| It is clear where I need to send the form once completed | Strongly agree | Somewhat agree | Neither agree nor disagree | Somewhat disagree | Strongly disagree |