Prepared for the Canada Revenue Agency

Supplier name: Earnscliffe Strategy Group

Contract Number: # 46558-205488/001/CY

Contract value: $73,413.03 (including HST)

Award date: January 4, 2019

Delivery date: March 13, 2019

Registration number: POR 100-18

For more information on this report, please email media.relations@cra-arc.gc.ca.

Ce rapport est aussi disponible en français.

Quantitative and Qualitative Research on Tax Scheme Promoters

Final Report

Prepared for the Canada Revenue Agency by Earnscliffe Strategy Group

March 2019

This public opinion research report presents the results of an online survey and focus groups conducted by Earnscliffe Strategy Group on behalf of the Canada Revenue Agency. The research was conducted in February 2019.

Cette publication est aussi disponible en français sous le titre: Recherche quantitative et qualitative sur les promoteurs de stratagèmes fiscaux.

Permission to Reproduce

This publication may be reproduced for non-commercial purposes only. Prior written permission must be obtained from the Canada Revenue Agency. For more information on this report, please contact the Canada Revenue Agency at: media.relations@cra-arc.gc.ca.

Catalogue Number:

Rv4-130/2019E-PDF

International Standard Book Number (ISBN):

978-0-660-30241-6

Related Publication (Registration Number: POR 100-18):

Catalogue number Rv4-130/2019F-PDF (Final Report, French)

ISBN: 978-0-660-30242-3

© Her Majesty the Queen in Right of Canada, as represented by the Minister of National Revenue, 2019

Table of contents

Earnscliffe Strategy Group (Earnscliffe) is pleased to present this report to the Canada Revenue Agency (CRA or The Agency) summarizing the results of the quantitative and qualitative research conducted to help the CRA better understand the issue of tax schemes.

Tax schemes and plans aim to deceive taxpayers by promising to reduce the taxes they owe and are often positioned to appear as legitimate financial products or business opportunities. They are directly advertised to Canadians through direct mail and social media and seem “too good to be true”. Promoters (individuals or corporations) who sell these schemes seek to break or bend the Canadian tax laws, deliberately making false claims to assist their clients in tax cheating, all while obtaining a financial benefit for themselves and their clients.

Research was required to help the CRA address the issue of tax schemes, develop strategies to combat tax avoidance and investigate the effectiveness of current promoter compliance measures, tools, and initiatives. More specifically, this study investigated taxpayers’ awareness and expectations of the Promoter Compliance Program. The CRA believes its ability to communicate about this program and its results in the detection and correction of promoter non-compliance will have an impact on future compliance.

Feedback from this research will help the CRA develop relevant and meaningful communication material with the goal of increasing awareness of tax schemes in general and to enhance the CRA’s Promoter Compliance Program. This study will also help to determine the effectiveness of other compliance tools, measures and initiatives, including Dedicated Promoter Auditors, Tax Alerts and public education ad campaigns. The total cost to conduct this research was $73,413.03 including HST.

To meet these objectives, Earnscliffe conducted a two-part research program.

The research began with the quantitative phase, an online survey of 1,005 Canadians aged 18 years or older. The survey was conducted using our quantitative subcontractor, Leger’s online proprietary panel. The research was conducted from February 4-10, 2019 and the survey took respondents an average of 13 minutes to complete. The data was weighted by age, gender and region.

Following the survey, we conducted a qualitative phase involving a series of six focus groups with two segments of the Canadian population: those with a household income of less than $150,000 and those with a household income of $150,000 or more. The sessions were conducted in: Toronto (February 26); Montreal (February 27); and, Vancouver (February 28). The groups in Montreal were conducted in French.

It is important to note that qualitative research is a form of scientific, social, policy and public opinion research. Focus group research is not designed to help a group reach a consensus or to make decisions, but rather to elicit the full range of ideas, attitudes, experiences and opinions of a selected sample of participants on a defined topic. Because of the small numbers involved the participants cannot be expected to be thoroughly representative in a statistical sense of the larger population from which they are drawn and findings cannot reliably be generalized beyond their number.

Research Firm: Earnscliffe Strategy Group Inc. (Earnscliffe)

Contract Number: 46558-205488/001/CY

Contract award date: January 4, 2019

Statement of Political Neutrality

I hereby certify as a Representative of Earnscliffe Strategy Group that the final deliverables fully comply with the Government of Canada political neutrality requirements outlined in the Communications Policy of the Government of Canada and Procedures for Planning and Contracting Public Opinion Research. Specifically, the deliverables do not include information on electoral voting intentions, political party preferences, standings with the electorate or ratings of the performance of a political party or its leaders.

Signed: Stephanie Constable

Date: March 13, 2019

Principal, Earnscliffe

Earnscliffe Strategy Group (Earnscliffe) is pleased to present this report to the CRA summarizing the results of the quantitative and qualitative research conducted to help the CRA better understand the issue of tax schemes.

Tax schemes and plans aim to deceive taxpayers by promising to reduce the taxes they owe and are often positioned to appear as legitimate financial products or business opportunities. They are directly advertised to Canadians through direct mail and social media and seem “too good to be true”. Promoters (individuals or corporations) who sell these schemes seek to break or bend the Canadian tax laws, deliberately making false claims to assist their clients in tax cheating, all while obtaining a financial benefit for themselves and their clients. Research was needed to help the CRA address the issue of tax schemes, develop strategies to combat tax avoidance and investigate the effectiveness of current promoter compliance measures, tools, and initiatives. More specifically, this study investigated taxpayers’ awareness and expectations of the Promoter Compliance Program. The CRA believes its ability to communicate about this program and its results in the detection and correction of promoter non-compliance will have an impact on future compliance.

The specific objectives of the research were to assess:

Feedback from the research will help the CRA develop relevant and meaningful communication material with the goal of increasing awareness of tax schemes in general and to enhance the CRA’s Promoter Compliance Program. This study will also help to determine the effectiveness of other compliance tools, measures and initiatives, including Dedicated Promoter Auditors, Tax Alerts and public education ad campaigns.

To meet these objectives, Earnscliffe conducted a two-part research program.

The first phase was quantitative and involved an online survey of 1,005 Canadians aged 18 years or older. The survey was conducted online by our sub-contractor, Léger, using their proprietary panel. The research was conducted from February 4-10, 2019 and the survey took respondents an average of 13 minutes to complete. The data was weighted by age, gender and region.

The second phase involved a wave of qualitative research which included a series of six focus groups with two segments of the Canadian population: those with a household income of less than $150,000 and those with a householde income of $150,000 or more. The sessions were conducted in: Toronto (February 26); Montreal (February 27); and, Vancouver (February 28). The groups in Montreal were conducted in French. Please refer to the Recruitment Screener in the Appendix of this report for all relevant screening and qualifications criteria.

In each city, the group with individuals with a household income of less than $150,000 began at 5:30 pm and the group with individuals with a household income of $150,000 or more began at 7:00 pm. The sessions were approximately 1.5 hours in length. Focus group participants were given an honorarium of $120 as a token of appreciation for their time.

It is important to note that qualitative research is a form of scientific, social, policy and public opinion research. Focus group research is not designed to help a group reach a consensus or to make decisions, but rather to elicit the full range of ideas, attitudes, experiences and opinions of a selected sample of participants on a defined topic. Because of the small numbers involved the participants cannot be expected to be thoroughly representative in a statistical sense of the larger population from which they are drawn and findings cannot reliably be generalized beyond their number.

The following presents the combined results for both the quantitative and qualitative phases of research. For purposes of reporting, the qualitative findings are woven throughout where these findings shed light on the quantitative results. The qualitative findings are presented in italicized font.

The vast majority of respondents (91%) say they have relied upon the advice of at least one source to minimize the amount of federal tax they pay. In fact, 80% have relied on more than one source. Respondents are most likely to have relied upon a member of their family or a friend for advice, education or help when it comes to ensuring they pay no more federal tax than necessary. Just under two-thirds (63%) have done so. Among those who have relied on family and friends, over half (62%) would do so again, 30% might or might not and 6% would not rely on their family and friends again. Among the 32% who have not relied on family and friends, half would consider doing so.

Respondents 55 years of age and older are less likely to have relied on family and friends (50% have). Respondents who have a university level education (67%), are a student (71%) or employed (70%) are more likely to have relied on family and friends.

The CRA follows as the second most common source of information to help respondents ensure they pay no more federal tax than necessary – 57% have relied on the CRA. Among those who have, 65% would do so again, 30% might or might not, and 5% would not. Among the 35% who have not relied on the CRA for advice, over two-thirds (68%) would consider getting information from the Agency. Older respondents are more likely to have relied on the CRA – 61% of those 35-54 and 60% of those 55+ have done so, compared to 47% of those 18-34.

A similar proportion have used accountants or accounting firms (48%), their own financial institution or bank (49%) and a person/firm focused on tax preparation or reduction (49%) for advice and education when ensuring they pay no more federal tax than they have to. Over half of those who have used these services would do so again. Of note, respondents with a household income of less than $60,000 per year are less likely to rely on outside help like accounting firms (40%).

Under half of respondents have used a financial planner (40%), but over half (60%) of those who have would do so again. Among the 52% of respondents who have not used a financial planner, almost two-thirds (65%) would consider doing so in the future. Financial planners are a more common source of information among those 55 and older (48%) and those with incomes between $60,000 and $99,999 (47%) and $100,000 and $199,999 (51%).

Just over a third (38%) have relied on media, and under half of that group would definitely do so again (39%). Those who have not used information from the news media are less keen to trust it as a source – two-thirds (67%) would not consider relying on the news media for tax advice.

| Sources of Information about Taxes | ||

| Have relied upon | Have not relied upon | |

| A member of your family/personal friends | 63% | 32% |

| The CRA | 57% | 35% |

| Your financial institution or bank | 49% | 44% |

| A person/firm focused on tax preparation/reduction | 49% | 44% |

| An accountant/accounting firm | 48% | 46% |

| A financial planner | 40% | 52% |

| The news media | 38% | 53% |

Q5. The first questions are about the kinds of individuals or organizations that people sometimes rely upon for advice, education or help when it comes to ensuring they pay no more federal tax than they have to. For each of the following, please indicate whether you have relied upon them or not in the past and whether you might consider or not. Base: n=1005.

| Likelihood of Relying on Sources Previously Used | |||

| Have relied upon, would again | Have relied upon, might or might not again | Have relied upon, would not again | |

| A member of your family/personal friends (n=629) | 62% | 30% | 6% |

| The CRA (n=573) | 65% | 30% | 5% |

| An accountant/accounting firm (n=480) | 65% | 29% | 6% |

| Your financial institution or bank (n=497) | 61% | 31% | 8% |

| A person/firm focused on tax preparation/reduction (n=497) | 57% | 31% | 12% |

| A financial planner (n=407) | 60% | 33% | 8% |

| The news media (n=377) | 39% | 50% | 11% |

Q5. The first questions are about the kinds of individuals or organizations that people sometimes rely upon for advice, education or help when it comes to ensuring they pay no more federal tax than they have to. For each of the following, please indicate whether you have relied upon them or not in the past and whether you might consider or not.

| Likelihood of Relying on Sources Not Previously Used | ||

| Have not relied upon, would not consider | Have not relied upon, might consider | |

| A member of your family/personal friends (n=322) | 50% | 50% |

| The CRA (n=350) | 32% | 68% |

| An accountant/accounting firm (n=458) | 35% | 65% |

| Your financial institution or bank (n=442) | 36% | 64% |

| A person/firm focused on tax preparation/reduction (n=440) | 36% | 64% |

| A financial planner (n=517) | 35% | 65% |

| The news media (n=534) | 67% | 33% |

Q5. The first questions are about the kinds of individuals or organizations that people sometimes rely upon for advice, education or help when it comes to ensuring they pay no more federal tax than they have to. For each of the following, please indicate whether you have relied upon them or not in the past and whether you might consider or not.

Over half (56%) of respondents have paid someone to help them prepare or reduce their federal taxes. Those in the 35-54 age category are more likely (63%) to have done so, along with Quebeckers (61%). Individuals with incomes between $60,000-$99,999 are more likely to have paid someone to help them with their taxes (61%) compared to those with incomes under $60,000 (53%). Those who have attended college (64%), are self-employed (70%) and employed (60%) are also more likely to have hired someone to help them with their taxes. Over half (58%) of respondents born in Canada have hired help, while fewer of those born outside of Canada have done so (49%). Slightly more respondents who are concerned about paying more tax than necessary (59%) have hired someone compared to those who are not concerned (51%). Similarly, a greater percentage of those who are interested in financial products or businesses that could help them reduce their taxes (60%) have hired someone, compared to 48% of those who are not interested.

Paid for Help Preparing Taxes

Q6. Have you ever paid someone to help you prepare or reduce your federal taxes? Base: n=1005

Qualitative Insights: Current Behaviours Related to Taxes

In terms of tax preparation, those in the higher income groups, particularly in Toronto and Montreal, tended to rely more heavily on professionals to prepare their income tax returns. The reasons they provided for doing so included: a sense that their taxes were too complicated; that they valued the reassurance that comes with having professionals take responsibility; and, the experience of a professional to do whatever they can (legally) to minimize the amount of federal taxes owed.

Those in the lower income groups, as well as those with higher incomes in Vancouver, tended to prepare their own income tax returns. Generally, most seemed to be more aware of what they can and cannot claim on their taxes, although, quite a few mentioned that they have their income tax returns vetted by a professional or an experienced friend or family member; mainly to confirm they prepared their return correctly.

Almost two-thirds (63%) say they are very or somewhat knowledgeable about determining the federal taxes they owe. Those most likely to say they are knowledgeable include:

Just under half (49%) claim to be very or somewhat knowledgeable about minimizing the federal taxes they owe. The demographic groups who say they are more knowledgeable about minimizing their taxes owed closely resembles those who said the same about determining their taxes, and include:

In addition, it is worth noting that more respondents born in Canada (50%) feel knowledgeable about the ways in which they can reduce their taxes compared to those born outside of Canada (42%).

Determining and Minimizing Taxes Owed

| Very knowledgeable | Somewhat knowledgeable | Not very knowledgeable | Not at all knowledgeable | DK/NR | |

| Minimizing taxes owed | 11% | 37% | 35% | 13% | 3% |

| Determining taxes owed | 17% | 46% | 25% | 9% | 3% |

Q7. How knowledgeable would you say you are about determining the federal taxes you owe? Base n=1005

Q8. How knowledgeable would you say you are about how to minimize the amount of federal taxes you owe? Base n=1005

Qualitative Insights: Determining and Minimizing Taxes Owed

Most participants felt that they were generally knowledgeable about determining the amount of federal taxes they owed and how to minimize the amount of federal taxes they owed.

Advice that participants had received to this effect included: Registered Retirement Savings Plan (RRSPs) and Tax-Free Savings Accounts (TFSAs) tax credits; federal tuition credit; charitable donations tax credit; and, public transit deductions, although many had heard through the media that this particular deduction was no longer available. Some of those in the higher income groups had also been advised about dividend income and capital gains.

Not surprisingly, in the case of those in the higher income groups, much of their knowledge was gained from their accountant or financial advisor. Those who said they prepare their taxes themselves using online tax filing software said that they had learned a lot based on the intuitive prompts initiated by the software. Others spoke of having received helpful advice (and annual reminders) from advisors and staff at their financial institutions.

Over two-thirds (68%) of respondents are concerned about paying more in federal taxes than necessary. Approximately one quarter (27%) say they are very concerned. Concern about this topic is highest among:

Concern about Paying More Tax than Necessary

Q9. How concerned are you about whether you are paying more in federal taxes than you absolutely have to? Base: n=1005.

Few respondents (14%) clearly recall hearing anything about financial products or business opportunities where the main benefit would be to reduce the amount of federal tax they would have to pay. Under a quarter (22%) say they vaguely recall hearing something about this topic, while over half (57%) do not recall hearing anything. Of note, recall is highest in Quebec, where 20% clearly and 27% vaguely recall having heard something about tax reduction opportunities. New Canadians are less likely to recall hearing something about tax reduction opportunities (31% vaguely or clearly recall) compared to those born in Canada (38%).

Recent Experience with Tax Schemes - Recall

Q10. In the past few months, have you seen, read or heard anything about financial products you could buy or business opportunities in which you could invest, where the main benefit would be to reduce the amount of federal tax you would have to pay, possibly even resulting in a tax refund? Base: n=1005.

Qualitative Insights: Awareness and Familiarity with Tax Schemes

Focus group participants’ awareness of and familiarity with tax schemes were very low. In fact, the term, ‘tax schemes’, was unknown to most.

Connotations of the term were both positive and negative but seemed to be dependent on language spoken and where a participant had lived before.

The majority of English-speaking participants, born in Canada, tended to view the term negative in its connotation and associated the term with words like: “fraud”, “tax evasion”, “scam”, “illegal”, etc. However, some English-speaking participants commented that in some other parts of the world, the word ‘scheme’ can be interpreted positively, as in “plan”, “strategy”, or “tactic”.

This interpretation was much more in line with that of French-speaking participants who associated the term, ‘stratagème fiscal’, with “optimization”, “maximization”, and, “planning”.

As a result, for the purposes of our qualitative discussions, ‘tax schemes’ were referred to as “stratagèmes fiscaux abusifs” in French; although, the characterization of ‘abusive’ tax schemes was not required in English given their (negative) interpretation of the term.

From a communications perspective, this will be important to bear in mind when communicating about tax schemes in either language and to new Canadians who may not interpret the term as intended.

Among those who did hear something about financial products or business opportunities to help them reduce their taxes, just under half (45%) were given the opportunity to purchase them. Of that 45%, half (51%) bought the product.

Recent Experience with Tax Schemes – Offer to Participate

Q11. [IF CLEARLY OR VAGUELY RECALL] Were you offered the chance to buy one of these products or invest in one of these business opportunities? Base: n=365.

Recent Experience with Tax Schemes – Purchased a Product/Invested

Q12. [IF OFFERED THE CHANCE TO BUY] Did you buy one of these products or invest in one of these business opportunities? Base: n=163.

Almost two-thirds (63%) of respondents would be interested in hearing more about tax reduction opportunities. Those who are most interested include:

Interest in Financial Products/Businesses to Reduce Taxes

Q13. If offered, how interested would you be in hearing about financial products you could buy or business opportunities in which you could invest, where the main benefit would be to reduce the amount of federal tax you would have to pay, possibly even resulting in a tax refund? Base: n=1005.

Over a third (37%) would be skeptical of offers to buy a financial product to reduce their taxes, while another 43% would be unsure whether to believe the offer. Few (14%) feel such an offer would be legitimate. Those more likely to say they would be skeptical of such an offer include:

Legitimacy of Offers to Reduce Taxes

Q14. If a professional you did not know told you there is a financial product you could buy or a business opportunity in which you could invest, that could reduce the amount of federal tax you would have to pay, possibly even resulting in a tax refund, how would you feel about that offer? Base: n=1005.

Qualitative Insights: Reactions to a Tax Scheme Example

As part of the focus group discussions, participants were presented with an example of a tax scheme. Participants were shown two slides in PowerPoint (depicted below) and the moderator read the following description:

Are you interested in an amazing business opportunity with a company in full development that meets the needs of small businesses through an innovative product?

How about an investment without a liquidity problem and impressive tax benefits?

You can be part of this amazing venture through the purchase of a Franchise.

What does your franchise sell? High tech affordable business software to make everyday tasks simpler. Every small business across the country will be signing up!

We take care of everything! You purchase the right to sell to small businesses in a specific region, but we do all the work! We operate the franchise and send you the paperwork you require at tax time. You receive tax benefits due to accelerated depreciation related to the software which also provides a cash flow through the tax advantage. What could be easier?

Most were very skeptical that they would take advantage of an offer like this. Participants indicated that they were generally skeptical of anything that looks too good to be true and that much of this opportunity seemed to fit that description. They pointed to language used to describe the business opportunity (i.e., “guaranteed”, “we do all the work”, and “the numbers speak for themselves”) and the financials as red flags.

Worth noting, some in the higher income groups who had an understanding of capital depreciation were more open to being convinced of the proposition, while maintaining some skepticism.

Large majorities agree that it’s important for everyone to pay their fair share of taxes (84%) and that it is legitimate for people to do everything they can to reduce the amount of taxes they owe (77%). Most respondents hold both views concurrently - 83% of those who agree it is important everyone pays their fair share of taxes also agree people should be allowed to do whatever is possible within the confines of the law to reduce their taxes. Respondents who were born in Canada are more likely to strongly agree that it is legitimate for people to do what they can to minimize their taxes (41%) compared to those who were not born here (32%). Older respondents (55+) are similarly more likely to view this as a legitimate practice (46% strongly agree) compared to 18-34 year olds (32%).

There is confidence in the CRA to catch people trying to get away with illegal tax schemes and widespread belief that the penalties if one is found to be participating in an illegal tax scheme are severe. One third strongly agree, while another 37% somewhat agree, that the CRA is very good at noticing when someone is trying to get away with an illegal tax scheme. Of note, Quebeckers are particularly confident in the CRA (83%). The plurality of respondents (44%) expect that the penalties for trying to get away with an illegal tax scheme are severe, and a third (34%) somewhat agree.

Qualitative Insights: Identification of Tax Scheme Promoters and Participants

Discussions in the focus groups suggested that participants were torn as to whether the CRA could easily identify those trying to take advantage of an abusive tax scheme on their taxes or those responsible for promoting abusive tax schemes. Certainly, the majority felt the CRA could more easily identify the former than the latter.

With respect to identifying those trying to take advantage of an abusive tax scheme, many participants assumed that the CRA has technology that can detect unusual patterns on personal income tax returns (i.e. an individual submitting a tax return that was not consistent with their previous returns). Once detected (on an individual return), participants thought the CRA could use that information to detect others trying to take advantage of the same tax scheme.

Conversely, most felt that it would be more challenging for the CRA to identify those responsible for promoting abusive tax schemes. Participants had the sense that tax scheme promoters were highly sophisticated, and typically, offshore. Most felt that these promoters had all the latest technology at their disposal to conceal their identities.

Qualitative Insights: Repercussions Associated with Tax Schemes

As part of the focus group discussions, we explored participants’ views of the repercussions associated with tax schemes.

Interestingly, participants’ views were quite homogenous. The majority of particpants were comfortable with the consequences – tax repayment plus interest, penalties, court fines, and jail time – facing those who knowingly choose to participate in or promote a tax scheme. However, there was a clear sense that those who choose to participate in a tax scheme should be treated on a case by case basis and that the severity of repercussions should be dependent on their prior knowledge/understanding of their crime. For example, most had the sense that tax scheme promoters tend to target those unfamiliar with the Canadian tax system (i.e., new Canadians); and, felt that someone who unknowingly participated in a tax scheme should not necessarily be penalized to the full extent of the law (i.e., no jail time).

With respect to tax scheme promoters, the majority of participants felt strongly that they should be penalized to the full extent of the law. Participants also felt that tax scheme promoters’ names (organizations’ names) should be broadcast publicly as a means of alerting/warning Canadians.

Most respondents like to keep their taxes as simple as possible (80%) and almost two-thirds (63%) expect the ways to minimize their taxes are probably complicated. A slightly higher proportion of those who like to keep their taxes simple think the ways to minimize their taxes could be complicated (68%). More women (84%) than men (77%) like to keep their taxes simple, as well as those 55 and older (85%) compared to those 18-34 (77%).

Three-quarters of respondents (76%) are always willing to hear about the ways they can minimize the federal taxes they pay. A similarly large proportion (70%) admit there are probably ways to reduce their taxes that they are unaware of. More+ respondents aged 18-34 agree with this statement (75%) than those 55 or older (66%). Those who are self-employed are less likely to agree that they are unaware of ways to reduce their taxes (61%), particularly compared with those who have a job, but are not self-employed (74%).

Opinion is more divided when it comes to determining whether a product or business opportunity to help reduce federal taxes is too good to be true. While the plurality (46%) agree the offer may be too good to be true, 36% neither agree nor disagree, and 12% disagree. Of note, respondents who were not born in Canada are slightly more skeptical. Over half (52%) agree that such an offer seems too good to be true, compared to 45% of those born here.

Respondents are also split over their confidence in knowing what they are and are not allowed to do to reduce the amount of federal tax that they owe. The plurality (42%) agree that they are confident, but 23% disagree, and 29% neither agree nor disagree. Older respondents (55 and over) are more confident in their ability (48%) than those aged 18-34 (33%). Those with a household income under $60,000 are also less confident (37%). Men report a higher level of confidence (46%) than women (38%).

| Attitudinal Statements About Tax Schemes | ||||||

| Strongly agree | Agree | Neither | Disagree | Strongly disagree | Don’t know/Prefer not to say | |

| It’s important that everyone pays their fair share of federal taxes | 49% | 35% | 9% | 2% | 2% | 3% |

| I expect the penalties are pretty severe for anyone who gets caught trying to get away with an illegal tax scheme in Canada | 44% | 34% | 9% | 5% | 3% | 5% |

| It’s perfectly acceptable for someone to do everything they can to legally reduce the amount of federal taxes they owe | 39% | 38% | 14% | 3% | 3% | 4% |

| I like to keep my tax planning and tax returns as simple and uncomplicated as possible | 37% | 43% | 12% | 3% | 1% | 3% |

| I expect that the Canada Revenue Agency is very good at noticing when someone is trying to get away with an illegal tax scheme | 33% | 37% | 16% | 7% | 3% | 5% |

| I’m always willing to hear about ways I can reduce the amount of federal taxes I pay | 26% | 50% | 17% | 2% | 2% | 4% |

| I expect that there probably are ways to reduce my federal taxes that I’m not aware of | 21% | 49% | 18% | 6% | 2% | 4% |

| I expect some of the legal ways to minimize the federal taxes I pay could be pretty complicated | 18% | 45% | 21% | 7% | 1% | 7% |

| The idea that there is a financial product or a business opportunity that could reduce the amount of federal tax I would have to pay is too good to be true | 13% | 33% | 36% | 10% | 2% | 6% |

| I’m confident I know what I’m allowed and not allowed to do to reduce the amount of federal tax I pay | 10% | 32% | 29% | 18% | 5% | 6% |

Q15. Please indicate how strongly you agree or disagree with each of the following statements. Base: n=1005.

Few (13%) are very confident they could tell the difference between an illegal tax scheme and a legal offer to help them reduce their taxes, though the plurality are somewhat confident (45%). One quarter (26%) are not very confident, and 9% are not confident at all. Those who express higher levels of confidence include:

Confidence in Ability to Recognize Illegal Tax Schemes

Q16. How confident would you say you are that you could tell the difference between the offer of an illegal tax scheme and the offer to help you reduce the federal taxes you owe or pay that the law allows? Base: n=1005.

About one in six (16%) believe they have been invited to participate in an illegal tax scheme at some point. Over three-quarters (77%) do not believe they have ever been invited to participate in a tax scheme. Respondents aged 18-34 are more likely to think they have been invited to participate in an illegal tax scheme (22%) compared to those 55+ (10%), along with those who are employed (21%) compared to those who are not (10%) and those whose household income is between $60,000 and $99,999 (22%), compared to those with a household income under $60,000 (14%).

Invited to Participate in an Illegal Tax Scheme

Q17. To the best of your knowledge, have you ever been invited to participate in an illegal tax scheme – either by mail, email, telephone, in-person or online? Base: n=1005.

Three-quarters claim they have not been given advice on how to avoid being part of an illegal tax scheme. One in five believe they definitely have or think they may have received such information. Respondents aged 18-34 are slightly more likely (28%) to claim that they have received advice, along with Albertans (30%).

Received Advice About Avoiding Illegal Tax Schemes

Q18. Have you ever been given advice on how to avoid being part of an illegal tax scheme – either by mail, email, telephone, in-person or online? Base: n=1005.

Among those who recall having received advice about avoiding illegal tax schemes, the Government of Canada, including the CRA, and news media are the top sources (36%). Financial institutions (25%) and financial planners or advisers follow (22%). Accounting firms are the least common source of information (13%). Those who have attended university (30%) and men (28%) are more likely to have received advice from a financial planner.

Avoiding Illegal Tax Schemes – Sources of Information

Q19. [IF RECEIVED ADVICE ABOUT AVOIDING TAX SCHEMES] Have you received advice on how to avoid being part of an illegal tax scheme from the following? Base: n=196.

The quantitative portion of this research tested respondents’ reaction to three different videos:

Video A: How to Recognize a Tax Scheme Promoter

Video B: What is a Tax Scheme?

Video C: What do Tax Schemes Offer?

Reaction to each of the videos was similar, but positive. The majority hold favourable opinions of both videos A (59%) and B (61%), while just over two-thirds (67%) view video C in a favourable light. Those who are interested in products or business opportunities that could help them reduce their taxes have a more favourable opinion of the videos than those who are not interested:

Video Testing: Initial Impressions

| Very favourable | Somewhat favourable | Neutral | Somewhat unfavourable | Very unfavourable | DK/NR | |

| Video C: What do Tax Schemes Offer? | 33% | 34% | 20% | 6% | 5% | 2% |

| Video B: What is a Tax Scheme? | 28% | 33% | 22% | 7% | 7% | 3% |

| Video A: How to Recognize a Tax Scheme Promoter | 27% | 32% | 23% | 9% | 7% | 2% |

Q20, Q24, Q28. Overall, what is your impression of this video? Base: n=1005.

Overall, the vast majority of respondents found the messages in the videos easy to understand. That said, there is a gap between French and English speakers – more English speakers found the videos very easy to understand, compared to French speakers:

Video Testing: Ease of Understanding the Messages

| Very easy | Somewhat easy | Not easy | DK/NR | |

| Video C: What do Tax Schemes Offer? | 66% | 27% | 5% | 2% |

| Video B: What is a Tax Scheme? | 63% | 30% | 5% | 2% |

| Video A: How to Recognize a Tax Scheme Promoter | 66% | 28% | 4% | 2% |

Q21, 25, 29. How easy was it to understand the messages presented in this video? Base: n=1005.

Large majorities found the videos very or somewhat helpful. Again, French respondents did not find the messages in the video as helpful as English respondents. For example, 43% of English speakers found the messages in video B very helpful, compared to 32% of French speakers. Those who are interested in opportunities to reduce their taxes and those who have paid someone to prepare or reduce their taxes found the messages more helpful. For example, 44% of those who are interested in opportunities to reduce their taxes found the messages in video A very helpful, compared to 33% of those who are not interested. Almost half (49%) of those who have paid someone to help them prepare their taxes found the messages in video C very helpful, compared to 38% of those who have not paid someone to help them.

Video Testing: Helpfulness of Messages

| Very helpful | Somewhat helpful | Not very helpful | Not at all helpful | DK/NR | |

| Video C: What do Tax Schemes Offer? | 44% | 42% | 8% | 3% | 3% |

| Video B: What is a Tax Scheme? | 41% | 44% | 10% | 3% | 3% |

| Video A: How to Recognize a Tax Scheme Promoter | 42% | 41% | 11% | 3% | 4% |

Q22, 26, 30. How helpful are the messages presented in this video? Base: n=1005.

For each of the videos, over one quarter would definitely notice them in their social media feeds, while just under half might notice them. Of note, those 55 and older say they are more likely to notice any of the videos – 34% say they would definitely notice video A and video B, and 35% would notice video C.

Likelihood of Noticing Video in Social Media Feed

| Definitely | Possibly | Not very likely | Not at all likely | DK/NR | |

| Video C: What do Tax Schemes Offer? | 29% | 48% | 13% | 8% | 3% |

| Video B: What is a Tax Scheme? | 30% | 47% | 13% | 7% | 3% |

| Video A: How to Recognize a Tax Scheme Promoter | 28% | 46% | 14% | 8% | 3% |

Q23, 27, 31. How likely would you be to notice this if you came across a link to it as an online ad or in your social media feed? Base: n=1005.

Qualitative Insights: Reactions to the CRA’s Video Messages

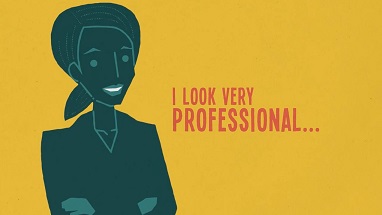

One of the three videos tested in the quantitative phase was tested in the qualitative phase, Video A: How to recognize a tax scheme promoter.

Overall reactions were quite favourable, with the exception of those in the higher income group in Toronto. Participants described the video as simple, direct, credible and effective at communicating the main messages: to be aware of tax schemes; to get a second opinion; and, for more information about tax schemes, to go to the Government of Canada’s, the CRA’s website, specifically. Participants appreciated the simplicity of the ad and felt the animation approach was attention-grabbing and modern.

Those in the higher income group in Toronto felt the animation approach and the message were too soft; not hard-hitting enough.

Focus group participants were also shown another video, Video D: Criminal Investigations Program – Promoters of Tax Evasion Schemes.

Reactions to this video were mixed but leaned negative. Most found the message contradictory and unclear. Participants questioned to whom the ad was directed – was it directed at Canadians to encourage whistle blower behaviour or was it directed at tax scheme promoters to advise them of the legal ramifications? The most troubling aspect of the video, for participants, however, seemed to be tied to the production value. There was a sense that the approach was a little “corny”, “outdated” and “melodramatic” which caused most to question its credibility and whether they would notice this ad online or in their social media feeds.

Worth noting, however, those in the higher income group in Toronto appreciated the more serious tone. Indeed, many came away with an understanding of the seriousness of the issue and the fact that it is a bigger issue than they thought.

After having watched these videos, over half (61%) claim to be more confident in their ability to recognize illegal tax schemes, including among those who were previously not confident in their ability to do so (60%). Respondents aged 18-34 are more likely to report feeling more confident (66%). Respondents aged 55 or older are more likely than respondents in younger age categories to say that the videos have not changed their confidence level (38% vs. 25% of those 18-34). French speakers are less likely than English speakers to feel more confident – 54% report that they are somewhat more or much more confident, compared to 62% of English speakers.

Change in Confidence to Detect Illegal Tax Schemes

| Much more confident | Somewhat more confident | No change | Less confident | DK/NR | |

| Previously not confident | 18% | 42% | 30% | 8% | 3% |

| Previously confident | 25% | 36% | 35% | 3% | 2% |

| Total | 22% | 39% | 32% | 5% | 3% |

Q32. After having watched these three videos, how much more or less confident are you that you know when to be suspicious of an offer to help you reduce your federal taxes? Base: n=1005.

The CRA is widely viewed as credible when it is communicating about illegal tax schemes. Over half say the Agency is very credible (53%) while a third say it is somewhat credible. The proportion who view the CRA as very credible is slightly lower among respondents aged 18-34 (48%) and Quebeckers (43%).

Q33. How would you rate the credibility of the Canada Revenue Agency when they communicate about illegal tax schemes? Base: n=1005.

Almost all respondents feel it is appropriate for the CRA to educate Canadians about illegal tax schemes. In fact, almost three-quarters (73%) feel education from the CRA is very appropriate. Any demographic variations in this view are a matter of degree, not direction. Slightly fewer men (67%), Quebeckers (63%) and French speakers (60%) view the CRA’s education as very appropriate, but in each case the vast majority feel it is at least somewhat appropriate.

CRA Education About Illegal Tax Schemes

Q34. How appropriate is it for the Canada Revenue Agency to educate Canadians about illegal tax schemes? Base: n=1005.

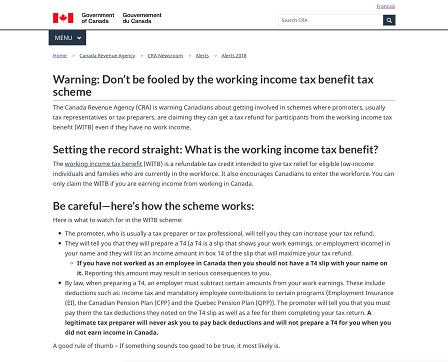

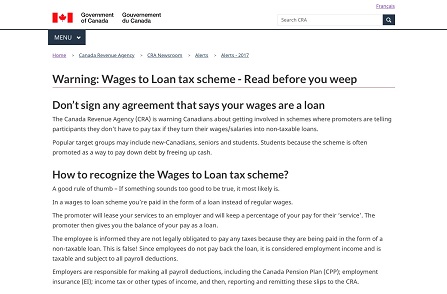

Qualitative Insights: CRA Tax Alerts

As part of the discussion groups, participants were asked to review the content of two different alerts that are available on the CRA’s website. The following are screen shots of part of the content; the alerts can be accessed through the hyperlinked titles provided below, and can also be found amongst others at the alerts website of Canada.ca https://www.canada.ca/en/revenue-agency/news/newsroom/alerts.html

Alert: Income Tax Benefit Tax Scheme

Alert: Income Tax Benefit Tax Scheme

Reactions to the alerts were overwhelmingly positive. Participants felt that the information was clear, easy to understand, well presented and credible. Most really appreciated the examples of tax schemes and felt it was appropriate and important for the CRA to alert Canadians.

Some questioned how they would receive these alerts. If only available on the website, many worried they would not see them. As a result, there were suggestions that the CRA’s homepage should feature alerts prominently but that it may also be good to email them or release them to the media (as is done for food recalls). Some also suggested including the alerts with the tax forms (mentioned as available in the post office) and as part of the online tax filing software/process; notes users have to read before preparing their income taxes.

Qualitative Insights: Preferred Modes of Communication

In terms of preferred modes of communication, participants provided a variety of suggestions.

Those in the lower income groups seemed to prefer traditional forms of communication such as television, radio, and public transportation, as well as, social media (i.e., Instagram, Facebook and YouTube).

Those in the higher income groups seemed to prefer more direct contact such as mail and email as they felt it was more official because the CRA could use identifiable information that they would see as legitimate.

There was a sense that connecting with new Canadians needs to be deliberate and targeted. Some participants reinforced the need for communications in the target population’s language. They suggested reaching out to local community centres, including post offices, libraries and community groups as a more effective way to reach new Canadians

The CRA commissioned this research to address the issue of tax schemes, develop strategies to combat tax avoidance, investigate the effectiveness of current promoter compliance measures, tools, and initiatives and determine how best to communicate with Canadians about these topics. The research suggests that awareness of and familiarity with tax schemes is low and that the CRA is well positioned to educate the population about tax schemes and how to recognize them.

The study demonstrates that paying federal taxes is widely accepted as a responsibility shared by all, but the results also clearly indicate that most are concerned about paying more than is absolutely necessary. Most agree it is important that everyone pays their fair share of taxes, but also view taking any legal steps to minimize the taxes they owe as legitimate.

Although well over half of respondents describe themselves as knowledgeable about how to prepare their own taxes, about half feel they are either not very or not at all knowledgeable about how to minimize the amount of federal taxes they pay. As a result, it is not suprising to see that the majority of respondents indicate they would be interested in hearing about opportunities to reduce the amount they owe. Taken together, it means a fairly large segment of respondents are receptive to information on reducing their federal taxes.

Though they are open to learning more about tax reduction opportunities, most respondents are skeptical or unsure of offers that seem “too good to be true”. Upon studying the examples of tax schemes presented in the focus group, most felt that terms such as, “guaranteed”, “we do all the work”, and “the numbers speak for themselves” and the financials were red flags. That said, few feel very confident in their ability to recognize a tax scheme and awareness of the term itself is low. In fact, Francophone participants did not feel the term necessarily has a negative connotation.

While respondents themselves may not feel confident they can identify an illegitimate scheme when they see one, there is certainly confidence that the CRA identifies such schemes. Further, the findings suggest there is an important role for the CRA to play in educating Canadians about tax schemes and that the language the Agency uses may need to be adjusted in order to communicate clearly with some audiences.

Respondents and focus group participants appreciated the video messages although some approaches were felt to be more effective than others. For the most part, the messages were clear and the information useful. More respondents reported feeling very confident in their ability to recognize a tax scheme after seeing the videos. Participants in the groups also responded favourably to the CRA Tax Alerts but might not see them if they are only posted to the CRA’s website. They suggested wider distribution to the media, organizations involved in tax preparation and tax software tools. Unlike the videos about tax schemes and the CRA Tax Alerts, the video about the Criminal Investigations Program received mostly negative feedback – participants in the focus groups had difficulty identifying the target audience and found the low production quality undermined the information being presented. Overall, the communications tools were met with generally positive feedback, but some could be further refined to ensure they both reach the intended audience and communicate the intended messages clearly.

Over half of the respondents in this study already rely on the CRA for advice about their taxes and most view the Agency as both a credible and appropriate source of information about tax schemes. However, the CRA should also note that an even greater proportion rely on family and friends for tax advice, and that those with higher incomes are more likely to pay someone, whether a financial advisor or accountant, to help them prepare or minimize their taxes. Consequently, the CRA should consider what information Canadians receive from these sources in its communication strategy around tax schemes.

Survey Methodology

Earnscliffe Strategy Group’s overall approach for this study was to conduct an online survey of Canadians aged 18 years or older using Léger’s online proprietary panel. A detailed discussion of the approach used to complete this research is presented below.

Questionnaire Design

The questionnaire for this study was designed by Earnscliffe in consultation with the CRA and provided for fielding to Léger. The survey was offered to respondents in both English and French and completed based on their preferences.

Sample Design and Selection

The sampling plan for the study was designed by Earnscliffe in collaboration with the CRA. The sample was drawn by Leger based on Earnscliffe’s instructions from their proprietary online panel.

Data Collection

The online survey was conducted in English and French from February 4-10, 2019. The survey was undertaken by Leger.

Targets/Weighting

The sample was targeted to the region, age and gender quotas.

The final data were weighted based on 2016 Census information. Weighting was applied based on region, age and gender statistics to help ensure that the final dataset was in proportion to the Canadian population aged 18 and older.

Quality Controls

Leger conducted a soft-launch pre-test of the survey, and Earnscliffe reviewed the data to ensure that all skip patterns were working and that all respondents were completing the survey in an appropriate amount of time.

Results

FINAL DISPOSITIONS

A total of 1,557 individuals entered the online survey, of which 1,005 qualified as eligible and completed the survey.

| Disposition | Count |

| Total Entered Survey | 1557 |

| Completed | 1005 |

| Not Qualified/Screen out/over quota | 449 |

| Suspend/Drop-off | 103 |

NON RESPONSE

Respondents for the online survey were selected from among those who have volunteered to participate in online surveys by joining an online opt-in panel. The notion of non response is more complex than for random probability studies that begin with a sample universe that can, at least theoretically, include the entire population being studied. In such cases, non response can occur at a number of points before being invited to participate in this particular survey, let alone in deciding to answer any particular question within the survey.

That being said, in order to provide some indication of whether the final sample is unduly influenced by a detectable non response bias, we provide the tables below comparing the unweighted and weighted distributions of each sample’s demographic characteristics.

All weighting was determined based upon the most recent Census data available from Statistics Canada. The variables used for the weighting of each sample were age and gender within each region.

SAMPLE PROFILE: UNWEIGHTED VERSUS WEIGHTED DISTRIBUTIONS

| Online | ||

| Region | Unweighted Sample | Weighted Sample |

| Atlantic | 67 | 68 |

| Quebec | 234 | 235 |

| Ontario | 386 | 388 |

| Manitoba/Saskatchewan | 65 | 66 |

| Alberta | 114 | 114 |

| British Columbia | 139 | 134 |

| Online | ||

| Age | Unweighted Sample | Weighted Sample |

| 18-34 | 277 | 289 |

| 35-54 | 343 | 346 |

| 55+ | 385 | 370 |

| Online | ||

| Gender | Unweighted Sample | Weighted Sample |

| Male | 491 | 494 |

| Female | 514 | 511 |

| Online | ||

| Education | Unweighted Sample | Weighted Sample |

| Some high school/High school diploma | 258 | 258 |

| Apprenticeship/Trade cert/College/CEGEP | 310 | 308 |

| Some/Graduated university (Bachelor’s level) | 325 | 326 |

| Post graduate degree above bachelor’s level | 103 | 103 |

| Prefer not to answer | 9 | 9 |

| Online | ||

| Employment Status | Unweighted Sample | Weighted Sample |

| Working full-time, that is, 35 or more hours per week | 367 | 373 |

| Working part-time, that is, less than 35 hours per week | 87 | 87 |

| Self-employed | 71 | 72 |

| Unemployed, but looking for work | 38 | 39 |

| A student attending school full-time | 95 | 97 |

| Retired | 251 | 241 |

| Not in the workforce (full-time homemaker, unemployed, not looking for work, unable to work) | 84 | 84 |

| Don’t know/Prefer not to answer | 12 | 12 |

| Online | ||

| Income | Unweighted Sample | Weighted Sample |

| Under $40,000 | 251 | 251 |

| $40,000-$60,000 | 148 | 149 |

| $60,000-$80,000 | 125 | 125 |

| $80,000-$100,000 | 135 | 134 |

| $100,000-$150,000 | 141 | 141 |

| $150,000+ | 84 | 85 |

| Prefer not to answer | 121 | 120 |

MARGIN OF ERROR

Respondents for the online survey were selected from among those who have volunteered to participate/registered to participate in online surveys. The data have been weighted to reflect the demographic composition of the Canadian population aged 18 and older. Because the sample is based on those who initially self-selected for participation in the panel, no estimates of sampling error can be calculated. The treatment here of the non-probability sample is aligned with the Standards for the Conduct of Government of Canada Public Opinion Research for online surveys.

SURVEY DURATION

The mean length of survey was 13 minutes.

Thank you for agreeing to take part in this survey. We anticipate that the survey will take approximately 10 minutes to complete.

[NEXT]

Background information

This research is being conducted by Earnscliffe Strategy Group, a Canadian public opinion research firm on behalf of the Canada Revenue Agency, a department of the Government of Canada.

The purpose of this online survey is to better understand Canadians’ opinions and behaviours relating to personal finances.

How does the online survey work?

What about your personal information?

If you have any questions about the survey, you may contact Earnscliffe at research@earnscliffe.ca.

Your help is greatly appreciated, and we look forward to receiving your feedback. [CONTINUE TO Q1]

1. Do you or does someone in your household or immediate family work for any of the following? [SELECT ALL THAT APPLY.] IF Q1=9 CONTINUE, OTHERWISE THANK AND TERMINATE.

2. What gender do you identify with?

3. In what year were you born?

[INSERT YEAR]

4. In which province or territory do you live?

5. The first questions are about the kinds of individuals or organizations that people sometimes rely upon for advice, education or help when it comes to ensuring they pay no more federal tax than they have to. For each of the following, please indicate whether you have relied upon them or not in the past and whether you might consider or not. [RANDOMIZE]

6. Have you ever paid someone to help you prepare or reduce your federal taxes?

7. How knowledgeable would you say you are about determining the federal taxes you owe?

8. And how knowledgeable would you say you are about how to minimize the amount of federal taxes you owe?

9. How concerned are you about whether you are paying more in federal taxes than you absolutely have to?

10. In the past few months, have you seen, read or heard anything about financial products you could buy or business opportunities in which you could invest, where the main benefit would be to reduce the amount of federal tax you would have to pay, possibly even resulting in a tax refund?

11. [IF Q16=2 or 3] Were you offered the chance to buy one of these products or invest in one of these business opportunities?

12. [IF Q17=2] Did you buy one of these products or invest in one of these business opportunities?

13. If offered, how interested would you be in hearing about financial products you could buy or business opportunities in which you could invest, where the main benefit would be to reduce the amount of federal tax you would have to pay, possibly even resulting in a tax refund?

14. If a professional you did not know told you there is a financial product you could buy or a business opportunity in which you could invest, that could reduce the amount of federal tax you would have to pay, possibly even resulting in a tax refund, how would you feel about that offer?

15. Please indicate how strongly you agree or disagree with each of the following statements. [RANDOMIZE]

16. How confident would you say you are that you could tell the difference between the offer of an illegal tax scheme and the offer to help you reduce the federal taxes you owe or pay that the law allows?

17. To the best of your knowledge, have you ever been invited to participate in an illegal tax scheme – either by mail, email, telephone, in-person or online?

18. And have you ever been given advice on how to avoid being part of an illegal tax scheme – either by mail, email, telephone, in-person or online?

19. [IF Q33=2 or 3] Have you received advice on how to avoid being part of an illegal tax scheme from the following? [SELECT ALL THAT APPLY]

The next few questions are to gather your impressions of messages that the Canada Revenue Agency (CRA) has shared to help Canadians avoid being part of an illegal tax scheme.

You’re going to be shown three different videos. In each case, you will be asked your overall favourability as well as questions about how easy it is to understand the message and how helpful the information is for knowing when to be suspicious of an offer to reduce your federal taxes. [RANDOMIZE ORDER OF TESTING EACH SPOT]

Click NEXT to continue to the first video.

VIDEO A: How to recognize a tax scheme promoter

https://www.youtube.com/watch?v=ZKLaN-5I1uQ&index=4&list=PLWsWrJHQSliuyqKlM--nKyCtJUwmO8CXI

20. Overall, what is your impression of this video?

21. How easy was it to understand the messages presented in this video?

22. How helpful are the messages presented in this video?

23. How likely would you be to notice this if you came across a link to it as an online ad or in your social media feed?

VIDEO B: What is a tax scheme?

https://www.youtube.com/watch?v=InkTg01Xwik&list=PLWsWrJHQSliuyqKlM--nKyCtJUwmO8CXI&index=1

24. Overall, what is your impression of this video?

25. How easy was it to understand the messages presented in this video?

26. How helpful are the messages presented in this video?

27. How likely would you be to notice this if you came across a link to it as an online ad or in your social media feed?

VIDEO C: What do tax schemes offer?

https://www.youtube.com/watch?v=LEM_I8qk2lk&list=PLWsWrJHQSliuyqKlM--nKyCtJUwmO8CXI&index=2

28. Overall, what is your impression of this video?

29. How easy was it to understand the messages presented in this video?

30. How helpful are the messages presented in this video?

31. How likely would you be to notice this if you came across a link to it as an online ad or in your social media feed?

32. After having watched these three videos, how much more or less confident are you that you know when to be suspicious of an offer to help you reduce your federal taxes?

33. How would you rate the credibility of the Canada Revenue Agency when they communicate about illegal tax schemes?

34. How appropriate is it for the Canada Revenue Agency to educate Canadians about illegal tax schemes?

The last few questions are strictly for statistical purposes. All of your answers are completely confidential.

35. What is the language you speak most often at home?

36. What is the highest level of schooling that you have completed?

37. What is your current employment status?

38. What are the first three digits of your postal code?

39. Which of the following categories best describes your total household income for 2018? That is, the total income of all persons in your household combined, before taxes?

40. Were you…?

41. [IF Q40=2] For how many years have you lived in Canada?

This concludes the survey. Thank you for your participation!

Looking for information about tax schemes and how to avoid them? Visit https://www.canada.ca/en/revenue-agency/campaigns/tax-schemes.html.

INTRODUCTION 10 min

Moderator introduces herself and her role: role of moderator is to ask questions, make sure everyone has a chance to express themselves, keep track of the time, be objective/no special interest.

Moderator will go around the table and ask participants to introduce themselves.

WARM-UP: GENERAL CONTEXT 10 min

Tonight, we are going to be discussing income taxes.

AWARENESS OF TAX SCHEMES 10 min

These products or business opportunities are sometimes referred to as “tax schemes”.

IMPRESSIONS OF TAX SCHEMES 20 min

I’d like to show you an example of a tax scheme. It could go something like this:

[SHOW SLIDE 1] Are you interested in an amazing business opportunity with a company in full development that meets the needs of small businesses through an innovative product?

How about an investment without a liquidity problem and impressive tax benefits?

You can be a part of this amazing venture through the purchase of a Franchise.

What does your franchise sell? High tech yet affordable business software to make everyday tasks simpler. Every small business across the country will be signing up!

We take care of everything! You purchase the right to sell to small businesses in a specific Region but we do all the work! We operate the franchise and send you the paperwork you require at tax time. You receive tax benefits due to accelerated depreciation related to the software which also provides a cash flow through the tax advantage. What could be easier?

[SHOW SLIDE 2] The numbers speak for themselves! You can purchase however many franchises you need to meet your needs!

REACTIONS TO VIDEO MESSAGES 15 min

Now, we will be reviewing video messages that were developed by the Canada Revenue Agency. We have two different concepts to show you. We will look at each one-by-one.

[MODERATOR TO PLAY EACH VIDEO TWICE. ORDER OF VIDEOS WILL BE SHOWN IN RANDOMIZED ORDER. MODERATOR TO LEAD A DISCUSSION ABOUT EACH VIDEO BASED ON THE FOLLOWING PROMPTS.]

REPERCUSSIONS OF ABUSIVE TAX SCHEMES 10 min

REACTIONS TO TAX ALERTS 10 min

I would like to take a few minutes to review a couple of tax alerts that the CRA has produced to educate Canadians about abusive tax schemes.

[MODERATOR TO SHOW EACH TAX ALERT ON SCREEN ONE AT A TIME.]

COMMUNICATIONS NEEDS 5 min

CONCLUSION

MODERATOR TO CHECK IN THE BACK ROOM AND PROBE ON ANY ADDITIONAL AREAS OF INTEREST.

Focus group summary

Group 1 NON-AFFLUENT

Group 2 AFFLUENT

| TORONTO Tuesday, February 26, 2019 | |

| Group 1: Non-affluent | 5:30pm |

| Group 2: Affluent | 7:00pm |

| MONTREAL Wednesday, February 27, 20198 | |

| Group 1: Non-affluent | 5:30pm |

| Group 2: Affluent | 7:00pm |

| VANCOUVER Thursday, February 28, 2019 | |

| Group 1: Non-affluent | 5:30pm |

| Group 2: Affluent | 7:00pm |

| Respondent’s name: Respondent’s phone number: (home) Respondent’s phone number: (work) Respondent’s fax number: Respondent’s email: Sample source: panel random client referral |

Interviewer: Date: Validated: Quality Central: On list: On quotas: |

Hello/Bonjour, my name is _______________ and I’m calling on behalf of the Earnscliffe Strategy Group, a national public opinion research firm.

Would you prefer that I continue in English or French? Préférez-vous continuer en français ou en anglais? [IF FRENCH, CONTINUE IN FRENCH OR ARRANGE A CALL BACK WITH FRENCH INTERVIEWER: Nous vous rappellerons pour mener cette entrevue de recherche en français. Merci. Au revoir].

We are organizing a series of discussion groups on behalf of the Canada Revenue Agency. The Canada Revenue Agency is interested in understanding Canadians’ awareness of and attitudes towards tax schemes. We are looking for people who would be willing to participate in a discussion group that will last up to an hour and a half. These people must be 18 years of age or older. Up to 8 participants will be taking part and, as a token of our appreciation for their time, they will receive an honorarium. May I continue?

Participation is voluntary. We are interested in hearing your opinions; no attempt will be made to sell you anything or change your point of view. The format is a ‘round table’ discussion led by a research professional. All information collected, used and/or disclosed will be used for research purposes only and the research is entirely confidential. But before we invite you to attend, we need to ask you a few questions to ensure that we get a good mix and variety of people. May I ask you a few questions; this should only take 5 minutes?

READ TO ALL: “This call may be monitored or audio taped for quality control and evaluation purposes.

ADDITIONAL CLARIFICATION IF NEEDED:

S1. Do you or any member of your household currently work for or have you or has any member of your household ever worked for…IF “YES” TO ANY OF THE ABOVE, THANK AND TERMINATE

S2. DO NOT ASK – NOTE GENDER. ENSURE GOOD MIX OF GENDER.

S3. Could you please tell me which of the following age categories you fall into? Are you...ENSURE GOOD MIX OF AGE

S4. What is your current employment status? ENSURE GOOD MIX OF EMPLOYMENT STATUS

S5. Which of the following categories best describes your total household income? That is, the total income of all persons in your household combined, before taxes? [READ LIST] IF 1 TO 6, CONTINUE FOR GROUP 1. IF 7 TO 10, CONTINUE FOR GROUP 2.

GROUP 1 [NON-AFFLUENT]: HOUSEHOLD INCOME IS LESS THAN $150,000

GROUP 2 [AFFLUENT]: HOUSEHOLD INCOME IS $150,000 OR MORE

S6. Were you:

S7. [IF BORN OUTSIDE CANADA] For how many years have you lived in Canada?

S8. What is the last level of education that you have completed? ENSURE GOOD MIX OF EDUCATION

S9. To make sure that we speak to a diversity of people, could you tell me what is your ethnic background? DO NOT READ. ENSURE GOOD MIX OF ETHNICITY

S10. Have you participated in a discussion or focus group before? A discussion group brings together a few people in order to know their opinion about a given subject. (MAX 1/3 PER GROUP, ASK S11, S12, S13)

S11. When was the last time you attended a discussion or focus group? DO NOT READ

S12. How many of these sessions have you attended in the last five years? DO NOT READ

S13. And what was/were the main topic(s) of discussion in those groups?

IF RELATED TO CRA OR TAXES/TAXES, TERMINATE.

INVITATION

S14. Participants in discussion groups are asked to voice their opinions and thoughts. How comfortable are you in voicing your opinions in front of others? Are you… (READ LIST)

S15. Sometimes participants are asked to read text and/or review images during the discussion. Is there any reason why you could not participate?

S16. Based on your responses, it looks like you have the profile we are looking for. I would like to invite you to participate in a small group discussion, called a focus group, we are conducting at [TIME], on [DATE].

As you may know, focus groups are used to gather information on a particular subject matter; in this case, the motivators and barriers with filing taxes. The discussion will consist of 8 to 10 people and will be very informal. It will last up to two hours, refreshments will be served and you will receive $100.00 as a thank you for your time. Would you be willing to attend?

PRIVACY QUESTIONS

Now I have a few questions that relate to privacy, your personal information and the research process. We will need your consent on a few issues that enable us to conduct our research. As I run through these questions, please feel free to ask me any questions you would like clarified.

P1) First, we will be providing the hosting facility and session moderator with a list of respondents’ names and profiles (screener responses) so that they can sign you into the group. This information will not be shared with the Government of Canada department organizing this research. Do we have your permission to do this? I assure you it will be kept strictly confidential.

We need to provide the facility hosting the session and the moderator with the names and background of the people attending the focus group because only the individuals invited are allowed in the session and the facility and moderator must have this information for verification purposes. Please be assured that this information will be kept strictly confidential. GO TO P1A

P1a) Now that I’ve explained this, do I have your permission to provide your name and profile to the facility?

P2) An audio and/or video tape of the group session will be produced for research purposes. The tapes will be used only by the research professional to assist in preparing a report on the research findings and will be destroyed once the report is completed.

Do you agree to be audio and/or video taped for research purposes only?

It is necessary for the research process for us to audio/video tape the session as the researcher needs this material to complete the report.

P2a) Now that I’ve explained this, do I have your permission for audio/video taping?

P3) Employees from the CRA and/or the Government of Canada may be onsite to observe the groups in-person from behind a one-way mirror.

Do you agree to be observed by Government of Canada employees?

P3a) It is standard qualitative procedure to invite clients, in this case, Government of Canada employees, to observe the groups in person. They will be seated in a separate room and observe from behind a one-way mirror. They will be there simply to hear your opinions first hand although they may take their own notes and confer with the moderator on occasion to discuss whether there are any additional questions to ask the group.

Do you agree to be observed by Government of Canada employees?

Invitation:

Wonderful, you qualify to participate in one of our discussion sessions. As I mentioned earlier, the group discussion will take place the evening of [Day, Month, Date] @ [Time] for up to two hours.

Do you have a pen handy so that I can give you the address where the group will be held? It will be held at:

| TORONTO Tuesday, February 26, 2019 | Honorarium: $120 5:30 pm 7:00 pm |

| MONTREAL Wednesday, February 27, 2019 | Honorarium: $120 5:30 pm 7:00 pm |

| VANCOUVER Thursday, February 28, 2019 | Honorarium: $120 5:30 pm 7:00 pm |

We ask that you arrive fifteen minutes early to be sure you find parking, locate the facility and have time to check-in with the hosts. The hosts may be checking respondents’ identification prior to the group, so please be sure to bring some personal identification with you (for example, a driver’s license). If you require glasses for reading make sure you bring them with you as well. And, please, don’t forget to bring your smartphone as you will not be able to participate without one.

As we are only inviting a small number of people, your participation is very important to us. If for some reason you are unable to attend, please call us so that we may get someone to replace you. You can reach us at [INSERT PHONE NUMBER] at our office. Please ask for [NAME]. Someone will call you in the days leading up to the discussion to remind you.

So that we can call you to remind you about the discussion group or contact you should there be any changes, can you please confirm your name and contact information for me?

First name

Last Name

email

Daytime phone number

Evening phone number

If the respondent refuses to give his/her first or last name or phone number please assure them that this information will be kept strictly confidential in accordance with the privacy law and that it is used strictly to contact them to confirm their attendance and to inform them of any changes to the discussion group. If they still refuse THANK & TERMINATE.