Prepared for the Canada Revenue Agency

Supplier Name: Environics Research

Contract Number: CW2245627

Contract Value: $71,048.75 (including HST)

Award Date: 2022-10-21

Delivery Date: 2023-03-03

Registration Number: POR 065-22

For more information on this report, please contact Canada Revenue Agency at: cra-arc.media@cra-arc.gc.ca

Ce rapport est aussi disponible en Français.

Qualitative Research on Scientific Research and Experimental Development (SR&ED) Client Portal

Final report

Prepared for Canada Revenue Agency

Supplier name: Environics Research

March 2023

The Canada Revenue Agency (CRA) commissioned Environics Research to conduct qualitative research with small to medium sized Canadian businesses focusing on their behaviours, motivations and experiences with SR&ED claims to inform future initiatives in the digital space, including the SR&ED Client Portal.

Cette publication est aussi disponible en français sous le titre : Recherche qualitative sur le portail clients du Programme de la recherche scientifique et du développement expérimental

This publication may be reproduced for non-commercial purposes only. Prior written permission must be obtained from the Canada Revenue Agency.

For more information on this report, please contact the Canada Revenue Agency at: cra-arc.media@cra-arc.gc.ca

101 Colonel By Drive

Ottawa, Ontario K1A 0K2

Canada

Catalogue Number: Rv4-169/1-2023E-PDF

International Standard Book Number (ISBN): 978-0-660-47948-4

Related publications (registration number: POR 065-22)

Catalogue Number: Rv4-169/1-2023F-PDF (Final Report, French)

International Standard Book Number (ISBN): 978-0-660-47950-7

© His Majesty the King in Right of Canada, as represented by the Minister of the Canada Revenue Agency, 2023.

The Scientific Research and Experimental Development Program (SR&ED) is the largest Government of Canada program supporting research and development in Canada, providing more than $3 billion in tax credits to over 16,000 businesses annually.

The Canada Revenue Agency (CRA) aims to create digital services that are user-friendly, accessible, and efficient for SR&ED claimants in obtaining information and support to claim the credits to which they are entitled, as well as meeting their compliance obligations. The program required direct insight into the needs, motivations, and behaviours of SR&ED claimants, including what they need to fill their SR&ED claims on their own without the assistance of professional claim preparers.

Thus, the objectives of this qualitative research were to explore:

Environics conducted individual interviews with 35 small or medium-sized businesses (less than 100 employees) across Canada, representing one of three key audiences:

For simplicity, this report uses the term "claimants" to refer to all interview participants, including both potential and existing claimants.

The CRA initiated the recruitment, reaching out to a list of organizations (by email and phone) and providing them with a link to a screening survey hosted by Environics. Claimants who completed the screening survey, met the eligibility criteria and provided their contact information were contacted by Environics to schedule an interview. Interviews were held with a company representative who (a) is directly involved in claim preparation, either from a technical or financial perspective, or (b) has some SR&ED decision-making responsibilities within their organization.

Interviews were conducted virtually (by Zoom, Teams or Google Meet) or by telephone, depending on participant preference, between January 12 and February 24, 2023. They ranged between 30-60 minutes in length depending on participants' responses. Thirty-three (33) interviews were completed in English and two (2) in French.

Since the CRA's initial email outreach included a large proportion of new or potential claimants who had participated in CRA webinars or other information opportunities, the interviews subsequently skewed to this group of claimants. The phone outreach focused on addressing the recruitment gaps. The following table summarizes the final distribution of the interviews:

Summary of completed interviews

| Region | SEGMENT A New or potential claimants |

SEGMENT B Experienced claimants who have not used a claim preparer (consistently or ever) |

SEGMENT C Experienced claimants who consistently use a claim preparer |

|---|---|---|---|

| West | 9 | 3 | 1 |

| Ontario | 12 | 5 | 1 |

| Quebec | 2 | 0 | 0 |

| Atlantic | 2 | 0 | 0 |

| Total | 25 | 8 | 2 |

More information about the study methodology is included in Appendix A.

Statement of limitations: Qualitative research provides insight into the range of opinions held within a population, rather than the weights of the opinions held, as measured in a quantitative study. The results of qualitative research should be viewed as indicative rather than projectable to the population.

The SR&ED claimants who participated in the interviews are highly motivated to submit SR&ED claims. Although they represent many different types of companies, the common thread was their reliance on the SR&ED claim to support their continued business operation and growth – especially since there are limited funding opportunities for innovation in Canada.

The research confirms that the claim process is, broadly speaking, meeting claimants' expectations. In some cases, the claim process even exceeds expectations, when the CRA is seen to go the extra mile by giving personalized direction through its First Time Claimant Advisory Service (FTCAS) and, for experienced claimants, when the process is consistently dependable year-over-year.

However, claimants continue to see room for improvement in addressing the pain points in their claim preparation journey:

The CRA has created tools and services like the Pre-Claim Consultation Service (PCC) and the Self-Assessment and Learning Tool (SALT) to address some of these known pain points. The limited take-up of these tools among interview participants suggests the goal should now be to promote the tools and services more widely and make them easy to find.

The CRA is also developing a SR&ED workspace to help claimants compile the financial and technical information needed to complete the T661 claim form. Initial impressions are that the workspace is a step in the right direction, but its value will largely hinge on the tips and information accessed through the question mark icon.

A key finding of this research is that many pain points are more prominent for first-time claimants; as claimants develop experience over multiple filings, they develop confidence in their ability to manage the process. This is the driver behind the CRA's First Time Claimant Advisory Service (FTCAS). However, because FTCAS takes place once a claim is filed and not beforehand, it does not fully alleviate the information gap for first-time claimants. Thus, the CRA should continue to develop pre-claim tools and services with first-time claimants in mind.

The research also reveals that the decision about how to prepare a claim is not limited to in-house versus professional claim preparation. Some businesses use a mixed model, where they are responsible for one aspect of the claim (either the technical or the financial) and their claim preparer is responsible for the other, or they use a third party (typically their general accountant) to advise on or review a claim prepared in-house. The main decision-making factors include cost; time and capacity constraints; the size of the claim and degree of risk; and confidence in their knowledge (versus that of a third-party).

Ultimately, claimants acknowledge and understand the need for a careful, detailed claim process to ensure the investment tax credits go to the right businesses and the program achieves its mandate to support innovation in Canada. At the same time, they would like to see greater transparency about the information the CRA is looking for, to remove the guesswork. That is why claimants place such value on the FTCAS: because they learn exactly what the CRA is looking for and are given the chance to discuss how that applies to their specific case. The more the CRA can provide directly pertinent information to a claimants' situation, and make that information easy to locate, the more confident claimants will be in their ability to submit a compliant claim.

The cost of this research was $71,048.75 (HST included).

I hereby certify as a senior officer of Environics that the deliverables fully comply with the Government of Canada political neutrality requirements outlined in the Communications Policy of the Government of Canada, and Procedures for Planning and Contracting Public Opinion Research. Specifically, the deliverables do not include information on electoral voting intentions, political party preferences, standings with the electorate, or ratings of the performance of a political party or its leaders.

Sarah Roberton

Vice President, Corporate and Public Affairs

Environics Research Group

sarah.roberton@environics.ca

613-793-2229

The Scientific Research and Experimental Development Program (SR&ED) is the largest Government of Canada program supporting research and development in Canada, providing more than $3 billion in tax credits to over 16,000 businesses annually.

The Canada Revenue Agency (CRA) identified the current SR&ED web content as a barrier for claimants, causing concerns about missed opportunities to claim tax incentives, an excess of non-compliant claims, and overreliance on professional claim preparers. Approximately 78% of claims are filed by professional SR&ED claim preparers, with around 8% of the SR&ED credits claimed going to preparers' fees.

Reflecting the direction provided by the Minister of National Revenue Mandate Letters and the CRA Corporate Business Plan, the CRA has begun taking steps towards building a more user-centric digital presence. This included a "design jam" with external stakeholders to identify pain points and potential solutions (2019) and a new Self-Assessment and Learning Tool (SALT) to help users quickly and confidently assess their eligibility for SR&ED tax credits (June 2022). Ongoing initiatives include the development of an SR&ED Client Portal (launching 2023/24) and a Web Content Optimization Project (launched late 2022).

The CRA is looking to better understand the behaviours, motivations and experiences of businesses around SR&ED claims, to inform the design and development of digital services, including the SR&ED Client Portal and future initiatives in the digital space.

The CRA aims to create digital services that are user-friendly, accessible, and efficient for SR&ED claimants in obtaining information and support to claim the credits to which they are entitled, as well as meeting their compliance obligations. The program required direct insight into the needs, motivations, and behaviours of SR&ED claimants to support filing their SR&ED claims on their own, where this supports their business model. The research objectives were to explore:

There are multiple ways in which claimants have heard about SR&ED:

For all, the top motivator for claiming SR&ED is the financial benefit to their organization, allowing them to continue to operate and, ideally, to grow. Experienced claimants are also motivated by program consistency and their ability to depend upon the claim to support their R&D year-over-year.

"It's really attractive for an early-stage startup to recoup costs." (Segment A)

"That is mission critical money for a young company, for that next year. We spend it and if we get it back quickly, then we can meet payroll for a couple of months." (Segment C)

I'm a big, big fan…It's simple enough and fast enough and doesn't change much year to year. That's the strength of it. If I can put it in our budget and be confident we'll get it, then it's very helpful." (Segment C)

Overall, there is a sense that, over time, the SR&ED claim process has undergone minor adjustments rather than substantial changes. The main changes of note are:

A few noted changes to program policy (e.g., allowable expenses) that subsequently impacted their claim.

More fundamentally, there are varying views about the CRA's overall approach to the SR&ED program and how that is reflected in the claims process. Among individuals with multiple claims over multiple years (Segments B and C, as well as Segment A who have previous SR&ED experience), some say the CRA used to work more closely with claimants, providing guidance and allowing changes to the claim, but that feeling of partnership no longer exists. Others say the opposite: that the CRA is trying to work with businesses more so now than in the past. The latter viewpoint is due at least in part to the value claimants see in the First Time Claimant Advisory Service (FTCAS), discussed in greater detail later in this report.

"There has been some improvement. [Compared to previous audit experience at other firms], more recently it has been more of a consultation, the CRA says let's walk through the claim and give you our feedback. It's very useful in understanding how SR&ED is defined. Earlier there were surprises about elements of the claim being challenged that seemed to be arbitrary." (Segment A)

"The process has gotten worse. The main problem is inconsistency in interpretation. The time it will take you to support a claim depends on the client…sometimes coming across as more of a compliance program rather than a benefits program, with less focus on helping people qualify…The program has gone through periods where it seems like they've been trying to reject more claims and other periods where it seems to want to help businesses…From talking to CRA advisors, you used to get clear answers, now it's not like that. Overall, it's a good program but it goes through ebbs and flows." (Segment B)

The interviews suggest two factors influencing claimant perspectives:

Experience level. The research design was based on firm experience: new claimants (fewer than four claims) versus existing claimants (4 or more claims). However, the interviews revealed the experience is often held by the individual, not the firm; that is, although the (current) firm is considered a "new claimant", the individual themselves brought SR&ED experience from previous companies to their current firm. This is particularly true for entrepreneurs who have been involved in multiple start-ups. Thus, the new claimant target group (Segment A) as defined in this research somewhat conflates SR&ED experience, since it encompasses multi-year claimants across multiple firms in addition to firms that have not (yet) submitted a claim and first-time claimants.

Industry. Industry was not systematically collected as a data point in this research but was often provided or discussed in the interview as part of the business context. Based on the discussions, we hypothesize that new pure technology firms (e.g., app creators) may find SR&ED claims more challenging than do other industry types (e.g., manufacturing, health sciences) with a more traditional or established R&D model. The challenge for technology firms can stem from: (a) the need to understand and establish eligibility (i.e., the existence of research and development activities), and/or (b) setting up a documentation process, which may be less of standard operating procedure for these types of firms.

"The creative process is more fluid. When you're innovative you don't always track every single thing – we don't know what's going to work out and what isn't. The CRA wants very structured records which doesn't match up with the innovation process." (Segment A)

This potential connection is important as the world of work shifts towards technology solutions. However, since this information was not systematically collected, further research or analysis of the SR&ED database is needed to confirm this hypothesis.

The CRA has found that approximately 78% of claims are filed by professional SR&ED claim preparers, with around 8% of the SR&ED credits claimed going to preparers' fees. This research probed the reasons for using a professional claim preparer versus preparing a claim in-house, and the perceived advantages and disadvantages to each approach.

A key finding is that the choice between in-house versus professional claim preparation is not dichotomous. There is a range of experiences, including third-party use for only part of the claim (either the technical or financial piece) while preparing the other part in-house, or using a third party only for advice or review of a claim prepared in-house.

Reasons for (advantages to) in-house preparation. Reasons given for preparing claims in-house include:

"When I looked at what to do and saw people online getting reduced amounts or their claims audited, I realized it was going to be harder than I thought. A friend said they outsourced [their claim] and regretted it because of how much they paid. I called around to find out how much [third parties] are charging and was told 20-30% of what I get back. The cheapest was $5,000. A couple were super shady…but we were concerned if we get audited, we need to prove [our claim]." (Segment A)

"We get bombarded by people that want to help us. After talking to them, we realized we still have to do all the work and then pay them at the end of it!" (Segment A)

"A third party did approach the company. I felt they were making conclusions [about what qualifies] they didn't have information to make a conclusion about. [The third party] didn't make sure the company was aware the documentation needs to come from them and that consultants don't do all the work. When I gave them that feedback, the company agreed maybe [the third party] were not the people to trust such an important thing to." (Segment A)

Reasons for (advantages to) third party preparation. Reasons given for choosing a third party to prepare SR&ED claims include:

"You don't want to make mistakes, especially with the CRA." (Segment A)

"Our SR&ED claim is in the thousands of dollars. It is very important to know when that money is going to come in. We pay more for that confidence." (Segment C)

"They have experience with the requirements and schedules. They know what the government wants in the write up. The process is too involved when you don't have the capacity and resources on your own." (Segment C)

Other factors. It is important to note the decision between in-house versus third party claim preparation is not only related to external factors (e.g., cost, time constraints). Especially because many of the firms are small and entrepreneurial, individual styles and mindsets also have a role to play, such as comfort with risk or degree of self-reliance (i.e., wanting to learn for themselves). Another factor is claimants' existing perceptions of the CRA and tax filing, or of government programs and processes in general: some are of the mindset that tax transactions are always tricky and best handled by experts, while others believe government processes can be navigated by anyone who wants to. Both risk perceptions and belief in the ability to navigate government processes can be mitigated by experience with the system.

"I wouldn't file my own taxes and [SR&ED claim] is an amendment to that. It's best to get a third party." (Segment A)

"[The claim process] is intimidating but [CRA] makes it doable and straightforward with the guide." (Segment A)

"My advice to newbies is don't worry about the mistakes, just submit it. If something is not allowable, they just won't accept it. But learn how to do it first without egregious errors, otherwise you are pushing it." (Segment B)

"Get your head around what SR&ED means in terms of eligible activities. Run through the self-assessment tool, if you'd get back a reasonable amount of money, have a meeting, try it and see." (Segment C)

Switching behaviours. There is some evidence of switching from a third party initially to in-house preparation in subsequent filing years. Among the interview participants, there was no-one who had switched in the other direction, from initially preparing a claim themselves to using a professional claim preparer. (A representative quantitative survey would be necessary to confirm the true distribution of behaviours).

The reasons given for moving their claim preparation in-house includes:

"When we first started asking questions and heard our activities might be SR&ED-eligible, that piqued our interest. It felt like we didn't easily find information on the Canadian government site. Consultants try to be your guide, they say it's very difficult and don't do it on your own, you need a consultant, so you just believe that because there is no other information easily available. We ended up signing a contract with a third-party consultant. Even my accountant didn't want to touch SR&ED with a ten-foot pole. But having gone through it now, if someone asked me about SR&ED, I would say don't hire someone." (Segment A)

The largest group (roughly half) of claimants say the SR&ED claim process met (but did not exceed) their expectations. They attribute their evaluation to the fact that the program works as intended, and the amount of preparation is reasonably commensurate for the claim received, while acknowledging room for improvement.

The remaining claimants lean towards the view that the claim process exceeded their expectations. The most common reason is their participation in FTCAS, where they had the opportunity to learn about the program and felt they had someone from the CRA in their corner. This kind of individualized support is clearly important to claimants.

A few claimants say the claim process fell short of their expectations, because of problems they encountered getting their claim processed, including audits and inconsistencies in how the program rules are applied.

Met expectations:

"SR&ED is now a significant help but it just meets expectations. It's not like its required for our success but it hasn't let us down. We haven't been denied yet but sometimes it seems like it's a bit mysterious in terms of how it works and how things are evaluated by the CRA." (Segment B)

"It met expectations, provided what it said it would and it promotes R&D for smaller organizations. There is no way to exceed expectations, it's very black and white...It's right to have a proper and fair process - it doesn't need to be easier." (Segment C)

"It met expectations. To exceed, they need to reach out and help us with this year's 2022 submission." (Segment A)

"It's fine. It's a bit detailed but the CRA has to protect taxpayer dollars and so on. It meets expectations. It's typical. There are criteria to meet but it's a lot of work." (Segment A)

"It met my expectations. I knew what to expect from previous experiences. The [FTCAS] exceeded expectations, with three people from the CRA who say we care about your company and want to help you succeed. But to exceed expectations [overall], something should have drastically changed in 17 years. It's still a form with three questions." (Segment A)

Exceeds expectations:

"It exceeded expectations. It's dependable, consistent, well-defined, doesn't change much year to year, doesn't get slashed, and is not dependent on maintaining a relationship with a government contact." (Segment C)

"Exceeded expectations. After the investment and how smooth it was and quick, we submitted our tax return early, got an assessment within a couple of weeks, two days later we got the cheque. We have lots of experience with the CRA in other matters and that is not characteristic of them." (Segment A)

"It met expectations, it was a lot of work, but it was worth it…Actually let's change that to exceeded expectations because the financial and technical reviewers were helpful and we felt well supported." (Segment A)

"I'm leaning towards [saying] exceeded. I was not expecting the first-time claimant interview, we were actually contacted by a CRA representative and they scheduled an interview." (Segment A)

Fell short of expectations:

"It fell short, there was way too much follow-up, we wasted so much time and money chasing them." (Segment A)

"It fell short of expectations because of the audit processes we have been through…We do our best to be a straight up, honest company, we are not trying to scam the system. We understand checks and balances have to be in place… [But this is an] area to improve: if the CRA has a robust process in place, a company has [previously] been audited and continues to practice that way, we should be a known entity and the CRA should not waste our time." (Segment B).

A key objective of the research was to understand the challenges that claimants face in preparing their claim. This can inform the design of information and tools to alleviate those barriers. Interview participants were asked to describe the steps they take to prepare their claim and any "pain points" they encounter along the way. The following summarizes the key pain points identified. Notably, many of these challenges are more prominent for first-time (and newer) claimants. Experience, including participating in the FTCAS, seems to help claimants overcome these challenges.

Information gathering (first-time claimants). A first-time claimant becomes aware of the SR&ED program and then needs to inform themselves about what the claim involves. Those willing to invest the time to educate themselves do not rely solely on CRA resources but cast the net widely, seeking online expertise such as blogs, forums and videos. There is an opportunity here for the CRA to produce a greater range of content to expand its share-of-voice. Other claimants may limit themselves to the basics and rely on their general accountants or SR&ED experts to know the program details.

"Information gathering was first: doing the research on the Government of Canada website, pulling out the T661 and necessary schedules, guides and writeup. It seems intimidating at first because it's more of an accounting-based document which isn't my specialty. There is jargon, I was unsure of amounts and what's included or not – it was a learning curve for the first time." (Segment A)

"The first big phase was learning. Scouring online resources, I watched YouTube videos, read forums, checked the CRA SR&ED website. My nighttime reading was SR&ED. This phase took the most time." (Segment A)

Is the project qualified for SR&ED? A central decision point is whether a firm has a viable SR&ED claim. Identifying whether a project does or does not qualify continues to be a pain point for some claimants, particularly less experienced ones. Both the Pre-Claim Consultation Service (PCC) and Self-Assessment and Learning Tool (SALT) were designed by the CRA to address this barrier. However, the interviews suggest there is limited uptake of these tools, which would hinder their ability to address the problem (see next section for more details). Moreover, there are also concerns about a lack of consistency and transparency in how the eligibility rules are applied by the CRA, which goes beyond what can be addressed by an online tool.

"The first step is review the data and write up the project. That's the most important part of SR&ED: to make sure it is eligible. What are the technical advancements you achieved, what was the objective. Once that's done, the accountant takes it from there." (Segment A)

"SR&ED is supposed to be an enabler of SMEs. But the audit takes a different tone, you have to prove you are eligible under the technical rules. This frustrates a lot of claimants and there is no transparency about how auditors arrive at their decision…But at that point, you've already spent the money and time to prepare the claim. So it's not really an enabler, in some respects it becomes an impediment." (Segment A)

Pulling together the evidence (documentation). The CRA has also previously identified documentation as a pain point for SR&ED claimants, and the interviews further confirm that. It is evident that more experienced firms (Segments B and C) have developed a process that works for them, while first-time claimants – who are more likely to be new firms – find themselves having to go back and locate the necessary evidence post-hoc. The challenge appears to be less about document storage, and more about (a) identifying early on what is acceptable evidence and (b) developing a process to systematically gather that evidence on an on-going basis.

"Gathering the data and evidence is a challenge. It's so day-to-day that the consultant can't help with it. We end up combing through a lot of scattered sources like project management software, chats, deactivated accounts when people leave, etc. [Documentation] is definitely an obstacle since we do it quite a bit later." (Segment A)

"Now I'm keeping track of time and work done. Is that sufficient? I don't know if the process I'm creating is correct. Am I spending the time effectively in terms of creating a process? [It would be helpful] if the CRA can provide multiple examples of different ways people can keep track of documentation in terms of what they are looking for." (Segment A)

"I'm planning how to separate employees who are doing SR&ED versus non-SR&ED work. How am I going to manage timesheets and percent of time allocated to various projects? It's tough in start-ups, it's dynamic. One day you are working on one thing, another day on something else." (Segment A)

"In-house we do up a scenario: based on the science, could we build a project? What's our initial budget and how far are we going to get with that amount? Then we start putting our notes in place [about project progress]…It takes couple of months to see a trend and document that trend. Then all the invoices come in the door for materials, etc. We give that a project number." (Segment B)

"We have a timesheet system that includes R&D projects. Staff report their time on a semi-monthly basis on those projects, so we don't get to the end of the year and have to re-engineer the time allocated." (Segment B)

A couple claimants offered the perspective that claiming the SR&ED credit can compel firms to invest in developing appropriate processes. It may be worthwhile to frame documentation as a benefit to the claim process rather than a drawback, to help more claimants embrace this shift in thinking.

"The planning [for SR&ED] is a big benefit of it. There are some unknowns with R&D. [SR&ED] helps with tracking what tasks you're doing. The added accountability and tracking leads to internal benefits [to the firm]." (Segment A)

"Having a project plan [from] the beginning turned out to be good for other reasons. Satisfying the SR&ED documentation requirement is providing other benefits in terms of making people's time efficient and helping make decisions on whether to keep on investing time." (Segment A)

Since the storage of documentation was not identified as a pain point, most participants could not envision themselves using a free, secure space provided by the CRA to upload and store documentation prior to filing a claim. This was viewed as an extra, unnecessary step and one that might carry privacy concerns with respect to their corporate financial information or their intellectual property.

"We use Google workspace so all the files and invoices are kept up to date. They're all in the right folders, it's easy for someone new [other than me] to come in. We already have the system so it's part of the day to day, it's not an extra effort to gather the info since they set things up knowing about [SR&ED]." (Segment A)

"Privacy [aspect] scares me - if you have our initial transcripts, our intellectual property, what assurances does the CRA have to protect that information?" (Segment A)

Filling in the forms (including writing the project description). The next barrier that claimants may face is filling in the claim forms, in particular the project description. The main question appears to be the amount of technical detail required (i.e., how high level should it be? How much detail is too much?)

"[The next phase] is putting it all online then figuring out the tax software (Intuit). The first tax software I used wouldn't let me submit SR&ED so I had to find another one. [Then] the writing phase - understanding the language, what to speak about - also took a really long amount of time." (Segment A)

"A pain point is the three-box description, because the description is very vague, I don't even know what they are looking for, I don't know what the expectation is. Is it exam-style where I should use the full word limit or optics-wise is that not good and I should use the full length?" (Segment A)

"This is the pain point. Writing a report that summarizes in very few words what took you a year to do is tough. It's not about providing information technology services to help. This is a language thing. [The CRA needs to provide] some sort of coaching – maybe a sanctioned 3rd party system that doesn't take a 15% flat fee…Someone who reviews the claim and gives a second opinion on the text. If something is glaringly wrong, I want to know up front." (Segment A)

Tracking the claim status. Once the claim has been submitted, claimants have the impression that it goes into a vacuum. They do not appear to have a way to know that status of their claim, which leads to uncertainty about the timing of when the return will be issued. It was noted that companies that lend against SR&ED returns are evidence that the nature of the timing is important for claimants.

"Actually submitting [the claim] was difficult. I needed to submit it a couple of times. When I called, the CRA couldn't confirm my submission. It took a whole month to show it was received." (Segment A)

"[Pain point is] not having visibility on when the claim is going to get paid out. By not being able to file halfway through year, it's very choppy when you get the money back. It's hard to do cash flow planning. Some years, the money comes pretty quick; some years, it takes a little longer." (Segment B)

Review/audit (for experienced claimants). Some claimants had experience with a claim review. In general, they understood the need for reviews and were able to successfully navigate the review process. Criticism falls into three categories: the length of the audit delayed receipt of their return; the frequency of the reviews for a single firm was excessive given that no problems were identified with their claims; and concerns about inconsistency in reviewers' interpretation and application of the CRA's own rules.

"I wish [the review] had been faster. It took three months…The review [itself] was fine. We did it over zoom. We gave them a lot of info ahead of time and they didn't have to poke around too much. But it took a lot of time to get the money. The approval person was a bottleneck. It took more than 12 months from when we originally submitted the claim, when it is typically 90 days otherwise." (Segment B)

"We have been audited several times. It's never been an issue, it's gone smoothly. One time we were audited two times in three years. An audit is time consuming and annoying because it delays the claim. The audits were too frequent considering [the CRA never identified] any issues." (Segment B)

Interview participants were asked which CRA tools, resource or services they used to prepare their claims. The most widely mentioned tool was the CRA website. Some participants recalled attending either a virtual or an in-person seminar in the early days when they were new to the process. First-time claimants also spend time searching for other online sources that fill in missing information gaps. Few participants voluntarily recalled a call with CRA personnel or accessing guides/PDFs online.

"I've used all online resources on the website. There's some really lengthy guides and examples of claims. I found them pretty helpful. I also had a call from someone that gave me an introduction and I called them a few times to ask questions." (Segment A)

Other claimants reported limited familiarity with or use of CRA resources.

"I'm not aware of any [CRA resources]. I know general information on definitions of what is allowable. I'm trying to stay on top of that but the CRA could improve on communicating any updates or improvements to us." (Segment B)

"Last time I checked the website was a few years ago. It's different from what I recall from before." (Segment B)

"We looked through everything on the website but there are no services offered by the CRA to help us prepare the claim." (Segment A)

Those who use third-party claim preparers express less interest in accessing CRA resources. They feel their claim preparers are sufficiently knowledgeable and trust them to handle the details.

"I went to a couple webinars before filing the first time but I didn't find them very useful. Too nitty gritty and technical. It was like information overload. I found my consultant a lot more helpful." (Segment A)

"I haven't felt the need. My accountant and consultant are enough." (Segment C)

Claimants were also asked specifically about four current CRA resources. Claimant impressions of these resources are discussed below, in order from highest perceived value to lowest perceived value:

First Time Claimant Advisory Service (FTCAS). Of the four tools probed in the interview, there was greatest awareness of the FTCAS. Participants seemed aware that the CRA determines whether claimants receive this service or not.

"Yes, I used this because they said it was mandatory. I believe the CRA decides whether you need this or not." (Segment A)

Those who received FTCAS felt the main value comes from sitting down with someone who is knowledgeable about the process to learn how it works. Participants also value the opportunity to get questions specific to their claim answered.

"It was very informative. At first I thought it was an audit but then I realized it's meant to teach you about the entire SR&ED process." (Segment A)

"Incredibly beneficial. It helped me understand what will or won't count. Learning how they want things written was helpful too." (Segment A)

"Yes, I found it helpful because it happened early on." (Segment A)

However, some participants felt that this service could be improved by holding it earlier in the process (before they submit their claim). Some participants would also like to receive follow-up materials or to be able to record or save the presentation for reference.

"I think it's a good way to deal with new claimants but it's not used properly" (Segment B)

"It was good but they didn't want you to record or share the presentation. It gives the information business owners need but the struggle is with timing – I don't want to sit through hours of a presentation." (Segment A)

"The answers about documentation were still vague and there were no presentation slides so I had to take notes." (Segment A)

"I was expecting some follow-up materials but I never received them. It would have been helpful if they delivered what they promised." (Segment A)

Self-Assessment and Learning Tool (SALT). Some participants have heard of and used SALT. Notably, they often appear to hear about during the FTCAS or to have found it on the website after submitting their claim. Claimants who have not used SALT tended to express interest in trying it, but reserved judgment about whether they feel it would improve the claim process for them.

"I've played around with it, but never used it before. I just wanted to get familiar with it, maybe I'll use it next time." (Segment B)

"I saw it on the website. Seems like it's useful. It confirmed what I already knew and that the program hasn't changed that much." (Segment A)

"I'm aware of it but I haven't really used it because of my consultant." (Segment A)

"Sounds like a great tool for a first-timer." (Segment C)

Pre-Claim Consultation Service (PCC). There was less awareness of the PCC than for the FTCAS, and fewer participants have used the PCC. Those who have used it signed up via email. The main perceived benefits are the opportunity to have a conversation with the CRA about a new project, to get clarity on a project for which they haven't filed a claim previously, and to better understand what are considered eligible expenses.

"I learned about it this year but it's not of use because we've rolled over our research from the previous year. If we were to start a new project, we would use it." (Segment B)

"Yes, I've used PCC. It was a fairly detailed and thorough discussion. It gave us an idea of whether we qualify and reaffirmed the project. It prevented us wasting time because if we didn't qualify, we could have spent a lot of hours on this." (Segment A)

"I did use that the first time. It was helpful to get you going." (Segment C)

There were a couple participants who used the PCC service but did not find it beneficial due to the CRA advisor handling their consultation.

"Yes, I used it once but didn't find it helpful. I didn't really get a clear answer because the advisor couldn't make a decision. It didn't save time." (Segment B)

"I have heard of it and used it last year. Their response did not feel good, I felt I was interrupting their time more than anything else." (Segment A)

Webinars and outreach activities. Interview participants reported limited use of CRA webinars or other outreach activities (e.g., industry communities of practice, industry specific engagements, in-person meetings). They were more likely to reference online resources provided by third-party claim preparers or information sessions offered by start-up incubators. A couple of individuals had signed up for a CRA webinar but were unable to attend due to conflicting priorities, and would like the opportunity to watch a video recording.

"The incubators provide SR&ED webinars but I haven't seen much from the CRA." (Segment A)

"I get regular communications from the CRA but nothing about these types of outreach activities." (Segment A)

"I used to go to them a couple times a year for 10-12 years. Used to be useful when it was joint industry and the CRA. Would be helpful to have industry-specific CRA interpretation seminars…" (Segment B)

"It would be great if they recorded it so we could watch it later, a lot of the times we are working during the seminar." (Segment B)

In general, claimants felt the CRA could do a better job promoting their resources and services. Claimants, especially those who file their claims in-house, find the SR&ED process to be time-consuming and want to minimize the time they spend locating resources that work for them. Third-party services and resources are currently helping claimants fill that gap. Focusing on accessible ways for claimants to get their questions answered, as well as the timing of services like the FTCAS or PCC will also be important in helping new/potential claimants feel comfortable in tackling the claims process themselves.

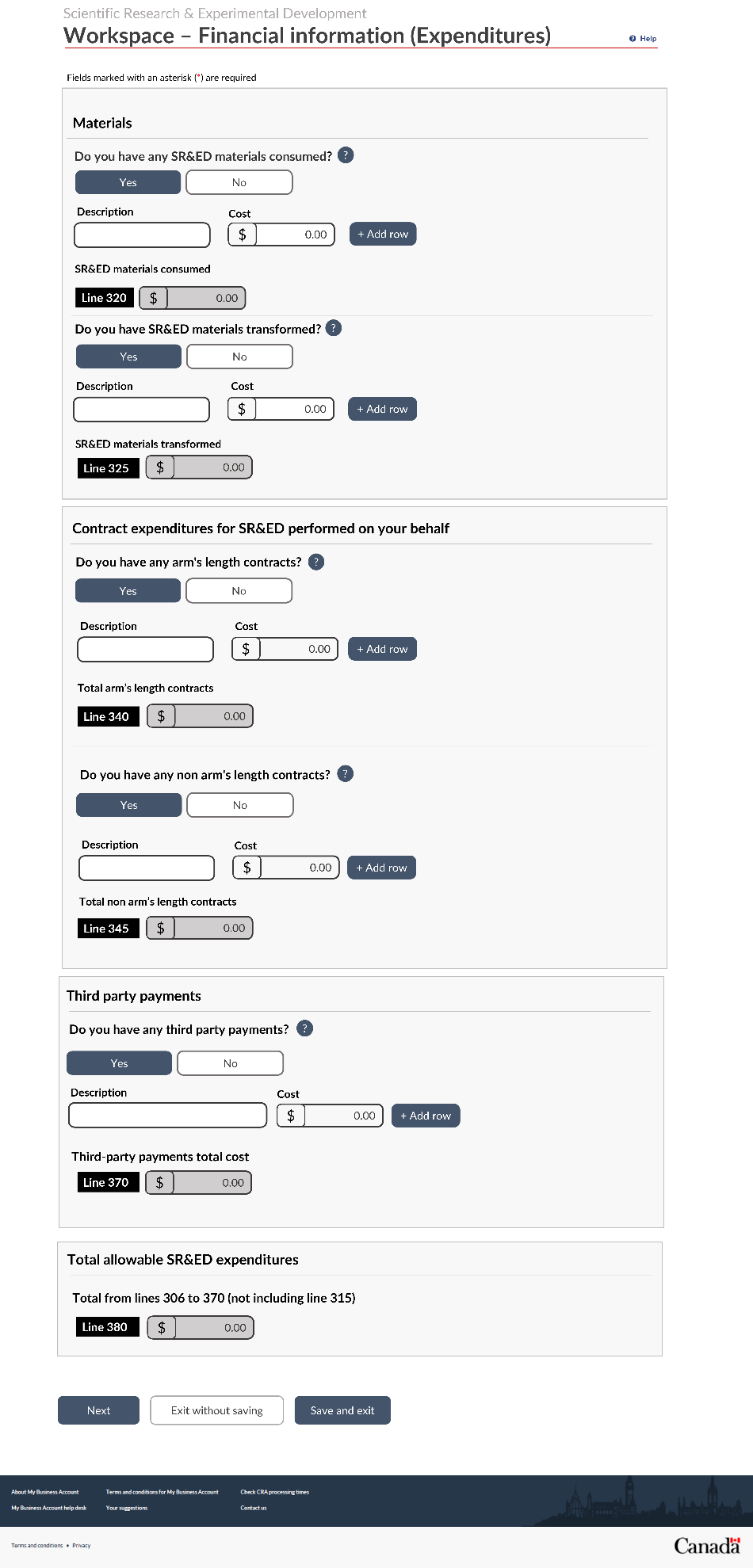

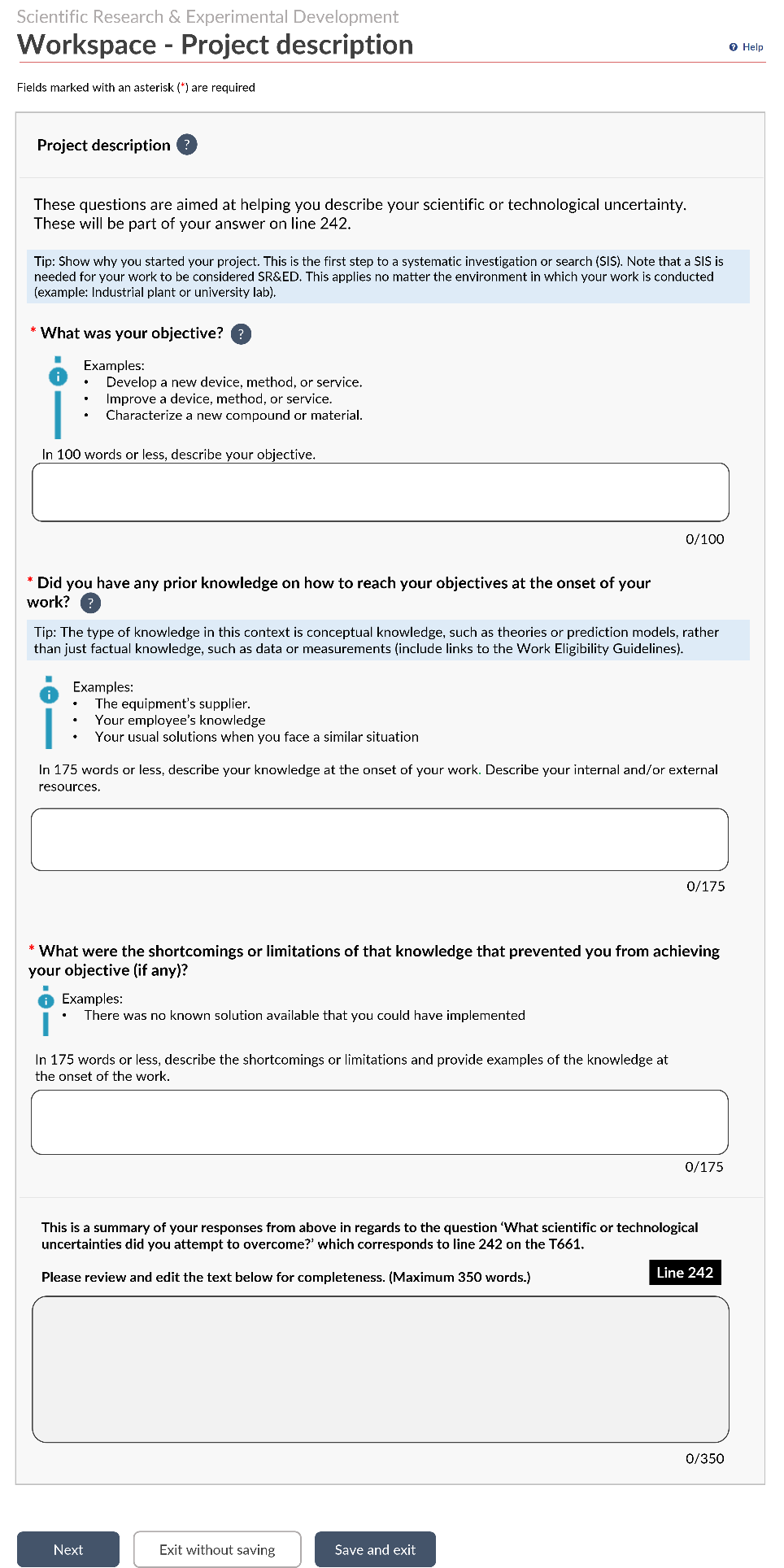

Future Tool (SR&ED Workspace)

Participants were shown screenshots of the SR&ED Workspace, a tool currently being developed by the CRA (see screenshots in Appendix D).

Overall, this tool was well-received across the claimant groups. The initial impression is that it has the potential to address some pain points. The main value hinges on the tips, examples and prompts, particularly those that will appear upon clicking the question mark icon. Participants believe the tool will be especially useful if the tips are relevant and in plain language. The ability to save and edit their work is considered a nice feature, and participants who file themselves generally saw themselves using this tool. Those who use a third-party claim preparer often said that, even though they might not use the tool themselves, they imagine it could be helpful for accountants and other claim preparers.

"It seems useful because it's simplified and breaks it down. [The tool] might make it faster to do the write up yourself. It's potentially helpful for the numbers too because the boxes make it seem easy enough to get inputs from the accountant." (Segment A)

One perceived drawback is that the workspace does not automatically populate the T661 form, so would ultimately require them to fill in the information twice (once in the workspace and once in the T661). Other additions or improvements to the workspace that claimants would like include built-in logic to catch discrepancies or alert claimants to errors; and access for multiple users to collaborate in the same workspace (with changes visible to everyone).

"This would be useful if it feeds into the form. I don't want to fill out the info twice." (Segment A)

The interviews wrapped up with questions about what information, tools or resources claimants want to assist them in filing an SR&ED claim and how to build claimants' confidence in their ability to file claims themselves without third-party assistance. Responses aligned closely with their identified pain points.

Information gathering. There is a need for further efforts at building claimants' awareness of the tools the CRA already offers, such as the PCC and SALT. This likely requires the CRA to build its' profile as the first and most trusted source of SR&ED information. The CRA's approach should consider how claimants currently do their research: searching online sources (Google) for evidence of SR&ED expertise in the form of blog and Q&A content and answers to specific questions – content which claimants are currently finding via external SR&ED consultants.

"It would have been good to know [before now] that there was a pre review consultation." (Segment A)

‘There needs to be more active communication from the CRA...The website could be reconfigured for better awareness of resources." (Segment A)

"[The CRA should offer] training programs for accountants that don't necessarily have a ton of corporate clients but are doing taxes for small businesses – they need to step up their game. Empowering those accountants would empower those businesses and be less of a barrier to SR&ED." (Segment A)

Fulfilling information requirements. As discussed earlier, the main pain point continues to be ensuring the claim contains the relevant information the CRA is looking for. The two ways in which claimants believe this can be alleviated are (a) being transparent about exactly what qualifies or doesn't qualify for SR&ED, or (b) providing very concrete examples so they can learn from how others have completed their claim forms.

"Just having a concise 1-3 pages to understand the process the CRA goes through in their review. The finance side is the easier one. We have receipts, time tracking of people we are claiming for and their salaries. All the accounting information can be provided for backup. What is nebulous is the scientific audit…and how they go about qualifying or disqualifying the claim or parts of the project." (Segment B)

"Elaborating more on what's SR&ED-able and not in terms of hours, salaries, type of project. Concrete examples and use cases." (Segment A)

"I need to tap into what other people have done." (Segment A)

Alternately, claimants would like to access personalized advice, input or mentoring directly from the CRA (e.g., the ability to sit down with a CRA advisor, to reach someone who will answer questions).

"If there was a free group session or a paid one-on-one meeting that is quick and specific to my needs, I would choose the latter. Time is my resource. I don't really want to do [the claim] myself but I also don't want to give 25% of my claim to a pricey consultant." (Segment A)

"I was not familiar with the proxy method, the little box you check…that made a difference of $13,000 for us. And once you submit, you can't go back and change your claim. I'd love to have had that session before making that claim." (Segment A)

Tracking the claim status. Claimants reiterated interest in knowing their claim status, both in terms of where it is in the process and when they will receive claim, to avoid the sense of sending their claim "into the void".

"I didn't see anything online to state where in the process the claim is at, or to expect a response by a certain date." (Segment A)

"Need more visibility on where claim is at. The CRA is a big black box. We submit it and then we get the final result. There is no understanding what is happening in between. It would be nice to have. If they are processing the claim in a reasonable time period, then it's less concerning." (Segment B)

"The CRA is focusing their efforts on the wrong part. We don't need tools to make the process better, we need people to be available to us and to trust that the process will happen when it's supposed to. Filing the claim is fine, the problem is everything after. The size of our claim versus the fee we pay for a tax consultant – it's a big claim and it's a reasonable amount of money for a third-party. [The CRA] should just be able to process these claims and pay us within a reasonable timeframe." (Segment A)

Policy changes. Although the focus of this research was on the claims process, some recommendations were raised around changes to program policy. The main one is to prioritize financial support (i.e., assign a larger proportion of the available funding pool) for small companies/start-ups or for companies outside major urban centres, who do not face an even playing field when competing for investment.

Environics conducted individual interviews with a total of 35 small or medium-sized businesses (less than 100 employees) across Canada, representing one of three key audiences:

Recruitment and scheduling. Due to privacy limitations, the CRA could not directly provide Environics with a list of SR&ED claimants. For that reason, the CRA initiated the recruitment, reaching out to organizations (707 by email, plus an additional 54 emails to associations asking them to share the message with their members, and 386 by phone) and providing them with a link to a screening survey hosted by Environics. A total of 205 individuals went to the survey link, of whom 49 completed the screening survey, met the eligibility criteria and provided their email address for subsequent contact by Environics. A total of 35 interviews were successfully scheduled and conducted in the time available for the research.

The initial research design called for 20 completed interviews per claimant Segment, for a total of 60 interviews. However, the CRA's initial email outreach included a large proportion of new or potential claimants who had participated in CRA webinars or other information opportunities. Thus, the Segment A quota was surpassed. The CRA's phone outreach focused on addressing the recruitment gaps, but ultimately the number of Segment B and Segment C claimants who completed the online screener was insufficient to reach 20 interviews each. We do not believe this has compromised the outcome of the research, since many of the research topics covered are especially relevant to new and potential claimants.

The following table summarizes the final distribution of the interviews:

Summary of completed interviews

| Region | SEGMENT A New or potential claimants |

SEGMENT B Experienced claimants who have not used a claim preparer (consistently or ever) |

SEGMENT C Experienced claimants who consistently use a claim preparer |

|---|---|---|---|

| West | 9 | 3 | 1 |

| Ontario | 12 | 5 | 1 |

| Québec | 2 | 0 | 0 |

| Atlantic | 2 | 0 | 0 |

| Total | 25 | 8 | 2 |

Interviews. Interviews were held with a company representative who (a) is directly involved in claim preparation, either from a technical or financial perspective, or (b) has some SR&ED decision-making responsibilities within their organization.

Interviews were conducted virtually (by Zoom, Teams or Google Meet) or by telephone, depending on participant preference, between January 12 and February 24, 2023. They ranged between 30-60 minutes in length depending on participants' responses. Thirty-three (33) interviews were completed in English and two (2) in French. Each participant was provided a $150 cash incentive as a thank you for their time.

All interviews were recorded for use in subsequent analysis by the research team. During the recruitment process and at the start of their interview, participants provided consent to such recording and were assured of their anonymity in subsequent reporting.

December 9, 2022

Environics Research

SR&ED Services qualitative research 2022

Canada Revenue Agency

PN11653

Recruitment for SME interviews – ONLINE VERSION

LANDING PAGE FROM SURVEY RECRUITMENT LINK

Welcome and thank you for your interest in this research about the Canada Revenue Agency's Scientific Research and Experimental Development (SR&ED) Program.

[Drop-down] Please select your preferred language / Veuillez choisir la langue dans laquelle vous souhaitez répondre au sondage

01 – English

02 – Français

[NEXT PAGE] Environics Research is conducting this research project on behalf of the Canada Revenue Agency (CRA). We are looking for representatives of Canadian companies (with fewer than 100 employees) that have submitted or are planning to submit an SR&ED claim, or that do research and development that may qualify for SR&ED, to participate in a one-on-one interview with a senior Environics researcher. The interview will be conducted over Zoom and will last up to one hour, depending on your responses. Participants who qualify and take part in the research will receive a cash gift of $150 for taking the time to share their thoughts and opinions.

This is not an attempt to sell or market anything. Your participation in the research is completely voluntary, confidential and your decision to take part or not will not affect any dealings you may have with the CRA.

If you are interested in participating in an interview, please click continue and fill out our short survey. Those who qualify for participation will be contacted by Environics with more information and scheduling.

CONTINUE

Privacy Details:

Your participation in this research is completely voluntary. The interview will be recorded. The recording will be used only to assist in preparing the report and will be destroyed once the report is completed. All information collected, used and/or disclosed will be used for the purposes of this study only and administered as per the requirements of the Privacy Act.

Environics upholds the highest standards of Personal Information Protection and Electronic Documents Act and adheres to privacy standards set out by the Canadian Research Insights Council (CRIC), as well as ESOMAR, the global association for the data and insights industry. Environics Research has a privacy policy which can be consulted at https://environicsresearch.com/privacy-policy/

If you have any questions about the study, please contact Environics: annika.jagmohan@environics.ca

This study has been registered with the Canadian Research Insights Council's Research Verification Service so that you may validate its authenticity. If you would like to enquire about the details of this research, you can visit CRIC's website https://www.canadianresearchinsightscouncil.ca/rvs/home/?lang=en. If you choose to verify the authenticity of this research you can reference project code 20221213-EN284

[NEXT PAGE] The following questions will help us determine who qualifies for participation. Environics will contact those who qualify with more information.

01 – 1 employee

02 – 2-4 employees

03 – 5-19 employees

04 – 20-49 employees

05 – 50-99 employees

06 – 100 or more employees THANK AND TERMINATE (Thank you very much for your interest, but we are looking for small and medium sized businesses with fewer than 100 employees)

01 – British Columbia WEST

02 – Alberta WEST

03 – Saskatchewan WEST

04 – Manitoba WEST

05 – Ontario ONTARIO

06 – Quebec QUEBEC

07 – Nova Scotia ATLANTIC

08 – New Brunswick ATLANTIC

09 – Prince Edward Island ATLANTIC

10 – Newfoundland and Labrador ATLANTIC

11 – Yukon WEST

12 – Northwest Territories WEST

13 – Nunavut WEST

01 - Yes

02 - No SKIP TO Q7

01 – Between 1 to 3 claims TARGET A - SKIP TO Q6

02 – 4 or more claims ASK Q5

01 – All claims prepared in-house TARGET B

02 – All claims prepared by an external firm TARGET C

03 – Originally prepared claims in-house and then switched to using an external firm TARGET C

04 – Originally used an external firm to prepare claims and then switched to preparing them in-house TARGET B

01 – You are directly involved in the claim preparation, either from a technical or financial perspective

02 – You have some SR&ED decision-making responsibilities in your organization

03 – Both

04 – Neither THANK AND TERMINATE (Thank you very much for your interest, but we are looking for an individual who has direct involvement or some decision-making responsibilities related to SR&ED)

NOW SKIP TARGET A, B, C TO Q9

01 - Yes

02 – No THANK AND TERMINATE (Thank you very much for your interest, but we are looking for companies who do R&D and who may be eligible for SR&ED)

03 – I'm not sure THANK AND TERMINATE (Thank you very much for your interest, but we are looking for companies who do R&D and who may be eligible for SR&ED)

01 - be directly involved in the claim preparation or submission, either from a technical or financial perspective

02 - be involved in decisions whether to submit a SR&ED claim

03 – Both

04 – Neither THANK AND TERMINATE (Thank you very much for your interest, but we are looking for an individual who would be directly involved in any SR&ED claims)

IF Q7=YES AND Q8=01-03, RESPONDENT ALSO QUALIFIES AS TARGET A. CONTINUE TO Q9.

01 – President/CEO/Owner

02 – CFO/Comptroller

03 – Accountant

04 – Payroll Manager/Officer

05 – Manager

06 – Bookkeeper

07 – Financial Officer

08 – Chief Technology Officer

09 – VP Research & Development

10 – Chief Engineer

11 – Lead Researcher

12 – Other (Specify) _________________________________________

01 – You were contacted directly by CRA, by email

02 – You were contacted directly by CRA, by phone

03 – You were contacted by an industry organization

04 – Saw the information about the research project on the CRA/SR&ED website

98 – Other. Please specify:_______________________________________

01 – English

02 – French

01 – Pacific Standard Time

02 – Mountain Standard Time

03 – Central Standard Time

04 – Eastern Standard Time

05 – Atlantic Time Zone

06 – Newfoundland Standard Time

01 – Morning (between 8 am – 12 noon)

02 – Afternoon (between 12 noon and 4 pm)

03 – Evening (after 4 pm and before 9 pm)

[NEXT PAGE] Thank you for filling out this survey. So that we can reach you to set up an interview, please provide us with your contact information below.

[checkbox] By registering, you grant Environics Research permission to contact you for the sole purposes of this study.

[checkbox] I understand that filling out this form does not guarantee me an interview, and I will be contacted by Environics to confirm my spot.

First Name:

Last Name:

Organization:

Email Address:

Phone Number:

SUBMIT

Thank You Page Copy:

Thank you for your time and interest in this study, we are currently reviewing your submission. Our recruitment specialist will be in touch shortly with more information.

Le 9 décembre 2022

Nous vous souhaitons la bienvenue et vous remercions de votre intérêt envers cette étude portant sur le Programme de la recherche scientifique et du développement expérimental (RS&DE) de l'Agence du revenu du Canada.

[Drop-down] Please select your preferred language/Veuillez choisir la langue dans laquelle vous souhaitez répondre au sondage :

01 – Anglais

02 – Français

[NEXT PAGE] Environics Research mène ce projet de recherche pour le compte de l'Agence du revenu du Canada (ARC). Nous cherchons des représentants d'entreprises canadiennes (comptant moins de 100 employés) qui ont présenté ou prévoient de présenter une demande de RS&DE ou dont les activités de recherche et de développement pourraient être admissibles à la RS&DE afin de réaliser une entrevue individuelle avec un(e) chercheur(se) principal(e) d'Environics Research. L'entrevue se déroulera par Zoom et durera tout au plus une heure, selon les réponses que vous donnerez. Les participants admissibles qui prendront part à la recherche recevront un cadeau en argent de 150 $ en guise de remerciement pour avoir partagé leur opinion avec nous et nous avoir consacré de leur temps.

Il ne s'agit pas d'une tentative pour vous vendre ou pour promouvoir quoi que ce soit. Votre participation est entièrement volontaire et confidentielle, et votre décision de participer ou non ne nuira d'aucune façon aux interactions que vous pourriez avoir avec l'ARC.

Si vous souhaitez participer à une entrevue, veuillez cliquer sur continuer et remplir notre court sondage. Environics Research communiquera avec les personnes admissibles à l'entrevue pour leur transmettre plus de renseignements et planifier l'entrevue en question.

CONTINUER

Confidentialité

Votre participation à cette étude est entièrement volontaire. L'entretien sera enregistré. L'enregistrement sera utilisé exclusivement pour préparer le rapport et sera détruit lorsque la rédaction du rapport sera terminée. Tous les renseignements recueillis, utilisés et/ou divulgués le seront à des fins de recherche uniquement en plus d'être administrés conformément aux exigences de la Loi sur la protection des renseignements personnels.

Environics respecte les normes les plus élevées de la Loi sur la protection des renseignements personnels et les documents électroniques (LPRPDE) et se conforme aux normes établies par le Conseil de recherche et d'intelligence marketing canadien (CRIC) ainsi qu'au code de conduite d'ESOMAR, une association internationale de chercheurs et d'utilisateurs de recherches du secteur des études de marché. Vous pouvez consulter la politique sur la vie privée d'Environics Research à l'adresse https://environics.ca/about-us/politique-de-confidentialite/.

Pour toute question à propos de cette étude, veuillez communiquer avec Environics à l'adresse .

La présente étude a été enregistrée auprès du Service de vérification des recherches du CRIC afin que vous puissiez valider son authenticité. Si vous souhaitez connaître les détails de l'étude, vous pouvez visiter le site Web du CRIC au https://www.canadianresearchinsightscouncil.ca/rvs/home/?lang=fr. Si vous choisissez de vérifier l'authenticité de cette recherche, vous pouvez faire mention du code de projet 20221213-EN284.

[NEXT PAGE] Les questions qui suivent nous aideront à déterminer votre admissibilité. Environics Research communiquera avec les personnes admissibles à l'entrevue pour leur transmettre plus de renseignements.

01 – 1 employé

02 – 2 à 4 employés

03 – 5 à 19 employés

04 – 20 à 49 employés

05 – 50 à 99 employés

06 – 100 employés ou plus THANK AND TERMINATE (Nous vous remercions de votre intérêt, mais nous recherchons des petites et moyennes entreprises qui comptent moins de 100 employés)

01 – Colombie-Britannique WEST

02 – Alberta WEST

03 – Saskatchewan WEST

04 – Manitoba WEST

05 – Ontario ONTARIO

06 – Québec

QUEBEC07 – Nouvelle-Écosse

ATLANTIC08 – Nouveau-Brunswick

ATLANTIC09 – Île-du-Prince-Édouard

ATLANTIC10 – Terre-Neuve-et-Labrador

ATLANTIC11 – Yukon WEST

12 – Territoires du Nord-Ouest

WEST13 – Nunavut WEST

01 – Oui

02 – Non SKIP TO Q7

01 – Entre 1 et 3 demandes TARGET A - SKIP TO Q6

02 – 4 demandes ou plus ASK Q5

01 – Toutes les demandes ont été préparées à l'interne TARGET B

02 – Toutes les demandes ont été préparées par une firme extérieure TARGET C

03 – Les demandes étaient au départ préparées à l'interne, puis nous avons opté pour une firme extérieure TARGET C

04 – Les demandes étaient au départ préparées par une firme extérieure, puis nous avons opté pour les préparer à l'interne TARGET B

01 – Vous participez directement à la préparation de la demande, que ce soit du point de vue technique ou financier

02 – Vous avez quelques responsabilités décisionnelles en matière de RS&DE au sein de votre entreprise

03 – Les deux

04 – Ni l'un ni l'autre THANK AND TERMINATE (Nous vous remercions de votre intérêt, mais nous recherchons une personne qui participe directement à la préparation des demandes de RS&DE ou qui a quelques responsabilités décisionnelles à cet égard)

NOW SKIP TARGET A, B, C TO Q9

01 – Oui

02 – Non THANK AND TERMINATE (Nous vous remercions de votre intérêt, mais nous recherchons des entreprises qui font de la R&D et qui pourraient être admissibles à la RS&DE)

03 – Je ne suis pas certain(e) THANK AND TERMINATE (Nous vous remercions de votre intérêt, mais nous recherchons des entreprises qui font de la R&D et qui pourraient être admissibles à la RS&DE RS&DE)

01 – directement au processus de préparation ou de présentation de la demande, que ce soit du point de vue technique ou financier

02 – au processus décisionnel visant à déterminer si vous présenterez ou non une demande de RS&DE

03 – Les deux

04 – Ni l'un ni l'autre THANK AND TERMINATE (Nous vous remercions de votre intérêt, mais nous recherchons une personne qui participerait directement au processus visant à présenter une demande de RS&DE)

IF Q7=YES AND Q8=01-03, RESPONDENT ALSO QUALIFIES AS TARGET A. CONTINUE TO Q9.

01 – Président(e)/président(e)-directeur(trice) général(e)/propriétaire

02 – Directeur(trice) financier(ère)/contrôleur(se) des services financiers

03 – Comptable

04 – Responsable/agent(e) de la paye

05 – Gestionnaire

06 – Commis comptable

07 – Agent(e) financier(ère)

08 – Directeur(trice) des technologies

09 – Vice-président(e) de la recherche et du développement

10 – Ingénieur(e) principal(e)

11 – Chercheur(se) principal(e)

12 – Autre (Précisez) _________________________________________

01 – Vous avez été contacté(e) directement par l'ARC par courriel

01 – Vous avez été contacté(e) directement par l'ARC par téléphone

03 – Vous avez été contacté(e) par une organisation de votre secteur d'activités

04 – Vous avez vu l'information au sujet du projet de recherche sur le site web de l'ARC/RS&DE

98 – Autre. Veuillez préciser : _______________________________________

01 – Anglais

02 – Français

01 – Heure normale du Pacifique

02 – Heure normale des Rocheuses

03 – Heure normale du Centre

04 – Heure normale de l'Est

05 – Heure de l'Atlantique

06 – Heure normale de Terre-Neuve

01 – En matinée (de 8 h à 12 h)

02 – En après-midi (de 12 h à 16 h)

03 – En soirée (après 16 h jusqu'à avant 21 h)

[NEXT PAGE] Nous vous remercions d'avoir pris le temps de répondre à ce sondage. Veuillez indiquer vos coordonnées ci-dessous pour que nous puissions vous joindre pour planifier une entrevue.

[checkbox] En vous inscrivant, vous autorisez Environics Research à communiquer avec vous aux fins de la présente étude uniquement.

[checkbox] Je comprends que le fait de remplir le présent formulaire ne garantit pas que je passerai l'entrevue, et qu'Environics Research communiquera avec moi pour confirmer ma participation.

Prénom :

Nom :

Organisation :

Courriel :

Téléphone :

SOUMETTRE

Page de remerciement

Nous vous remercions de votre temps et de votre intérêt envers cette étude. Nous examinons actuellement votre candidature. Notre spécialiste en recrutement communiquera sous peu avec vous pour vous transmettre plus de renseignements.

Environics Research

December 22, 2022

Canada Revenue Agency

SR&ED Interviews with SMEs

Discussion guide – FINAL

Name:

Organization:

Date: _______________

Interviewer:

Interview number:

Introduction

Hello, my name is ______________ from Environics Research. Thanks for joining me today.

As you know, we are conducting interviews on behalf of the Canada Revenue Agency about the Scientific Research and Experimental Development investment tax credit, also called SR&ED. We would like you to share your thoughts and experiences.

The interview will take approximately 45-60 minutes to complete, depending on your responses.

Your responses will not be linked to your name or organization (your identity and the identity of your organization will remain confidential). The session is being recorded. The recording is for my use only to help in preparing the report on this research, and will not be provided to the CRA.

Do you have any questions before we begin?

Warm-up/motivations for filing (5 minutes)

How and when did you (first) decide to apply? Why did you decide to apply? (motivations)

Behaviour (10 minutes)

IF MOST RECENT CLAIM DONE BY 3e PARTY:

What makes someone use a preparer or not?

Probe: What information sources (if any) did you use to make your decision?

Probe: Are you generally satisfied or dissatisfied with your provider? Why do you say that?

What makes someone change their filing behaviour? (switching behaviours)

If previously did it in-house (i.e., switched), probe: When did you prepare a claim in-house? Why? Why did you switch to third party?

If always used party (i.e., never switched), did you ever consider doing it in-house? Why did you decide against it?

Ask all: would you consider doing it in-house (again) in the future?

IF MOST RECENT CLAIM DONE IN-HOUSE:

What makes someone use a preparer or not?

Probe: What information sources (if any) did you use to make your decision?

What makes someone change their filing behaviour? (switching)

If previously used party (i.e., switched), probe: When did you use a third party? Why? Why did you switch to preparing the claim in-house?

If always did it in-house (i.e., never switched), did you ever consider using a third party? Why did you decide against it?

Ask all: Would you consider using a third party (again) in the future?

Customer journey (15-20 minutes)

AT EACH STEP, ASK:

What feelings do you associate with this step of the process?

What problems, if any, did you encounter this step?

Were you able to solve/overcome those problems? If so, how? If not, why not?

Did you change anything about how you did this compared to previous years?

STEPS TO PROBE (IF NOT VOLUNTEERED):

ONCE DOCUMENTATION IS MENTIONED DURING THE "JOURNEY", CONTINUE WITH Q12 LINE OF QUESTIONING BEFORE RETURNING TO REST OF JOURNEY STEPS:

Resources (15 minutes)

Yes – Have you used it? Was this service useful to you? Would you recommend it?

No – Does this service sound like it might be of interest to you? What would your expectations be?

| - | If not mentioned at Q14, have you heard of it? How? | If heard of it, have you used it? Why or why not? | If used, what liked and disliked? |

|---|---|---|---|

|

- | - | - |

|

- | - | - |

Lessons learned (5 minutes)

TARGET B/C: What advice would you give to businesses who are new to SR&ED and are looking to submit their first claim?

Next steps/reaction to potential tools (5 minutes)

Show screen shot 1: This tool will help you to answer the questions in your project description, by breaking those questions down, and providing tips and help as you fill them out. (give time to read)

Show screen shot 2: The tool would also help you fill in the expenditure portion of the information. (give time to read)

On both screens, you can input the information, save it and then come back later and make changes or updates as required. Once you are happy with your project description and expenditures, you can print or save the results so you can complete a T661 and submit your claim with your tax return.

Would a tool like this be useful to you/would you use this tool? Why or why not?

Wrap-up

Anything else that CRA should know? Any questions I should have asked you but didn't?

NON CLASSIFIÉ

Environics Research

22 décembre 2022

Agence du revenu du Canada

Entrevues réalisées auprès des PME sur le Programme de la recherche scientifique et du développement expérimental (RS&DE)

Guide de discussion – FINAL

Nom :

Organisation :

Date : _______________

Intervieweur(se) :

Numéro d'entrevue :

Introduction

Bonjour, je me nomme ____________________ et je vous appelle de la part d'Environics Research. Je vous remercie d'avoir accepté de vous joindre à moi aujourd'hui.

Comme vous le savez, nous réalisons des entrevues pour le compte de l'Agence du revenu du Canada (ARC) au sujet du crédit d'impôt à l'investissement pour la recherche scientifique et le développement expérimental, ou RS&DE. Nous aimerions vous inviter à nous faire part de vos points de vue et de vos expériences au sujet de ce programme.

L'entrevue devrait durer de 45 à 60 minutes environ, selon vos réponses.

Soyez assuré(e) que les réponses que vous donnerez ne permettront pas de vous identifier ou d'identifier votre organisation (votre identité et celle de votre organisation demeureront confidentielles). L'entrevue sera enregistrée pour mon usage exclusif afin de m'aider à préparer le rapport portant sur cette étude, et l'enregistrement ne sera pas remis à l'ARC.

Avez-vous des questions à me poser avant que nous commencions?

Mise en train/raisons à l'origine de la présentation d'une demande (5 minutes)

Qu'est-ce qui vous a amené(e) à présenter une (première) demande et à quand cela remonte-t-il? Pourquoi avez-vous décidé de présenter une demande? (raisons)

Attitude (10 minutes)

SI LA DERNIÈRE DEMANDE A ÉTÉ REMPLIE PAR UNE FIRME EXTÉRIEURE :

Pour quelles raisons choisit-on ou non de faire remplir une demande par une firme extérieure?

Intervention : Quelles sources d'information (s'il y a lieu) avez-vous utilisées pour prendre votre décision?

Intervention : Dans l'ensemble, êtes-vous satisfait(e) ou insatisfait(e) des services rendus par la firme extérieure? Pourquoi dites-vous cela?

Qu'est-ce qui incite quelqu'un à procéder autrement pour remplir une demande? (changement d'attitude)

Si une demande a déjà été remplie à l'interne (c.-à-d. changement d'attitude), intervention : À quand cela remonte-t-il? Pourquoi? Pourquoi avez-vous décidé d'opter plutôt pour une firme extérieure?

Si la tâche a toujours été confiée à une firme extérieure (c.-à-d. aucun changement d'attitude), intervention : Avez-vous déjà envisagé de réaliser cette tâche à l'interne? Qu'est-ce qui vous a dissuadé(e) de le faire?

Poser la question suivante à tous les répondants : Envisageriez-vous de remplir (de nouveau) une demande à l'interne à l'avenir?

SI LA DERNIÈRE DEMANDE A ÉTÉ REMPLIE À L'INTERNE :

Pour quelles raisons choisit-on ou non de faire remplir une demande par une firme extérieure?

Intervention : Quelles sources d'information (s'il y a lieu) avez-vous utilisées pour prendre votre décision?

Qu'est-ce qui incite quelqu'un à procéder autrement pour présenter une demande? (changement d'attitude)

Si une firme extérieure a déjà rempli une demande (c.-à-d. changement d'attitude), intervention : Quand avez-vous fait appel à une firme extérieure? Pourquoi? Pourquoi avez-vous décidé de remplir vos demandes à l'interne?

Si les demandes ont toujours été remplies à l'interne (c.-à-d. aucun changement d'attitude), intervention : Avez-vous déjà envisagé de faire appel à une firme extérieure? Qu'est-ce qui vous a dissuadé(e) de le faire?

Poser la question suivante à tous les répondants : Envisageriez-vous de confier (de nouveau) la tâche à une firme extérieure à l'avenir?

Processus du client/de la cliente (15-20 minutes)

À CHACUNE DES ÉTAPES, POSER LES QUESTIONS SUIVANTES :

Quelles émotions associez-vous à cette étape du processus?

À quels problèmes avez-vous été confronté(e), s'il y a lieu, à cette étape?

Avez-vous été en mesure de résoudre/surmonter ces problèmes? Si oui, de quelle manière? Si non, pourquoi pas?

Avez-vous modifié quoi que ce soit dans le processus que vous avez suivi comparativement aux années antérieures?

ÉTAPES À PROPOSER (SI ELLES NE VIENNENT PAS D'ELLES-MÊMES) :

DÈS QU'IL EST FAIT MENTION DE LA DOCUMENTATION DURANT LE « PROCESSUS », POURSUIVRE L'ENTREVUE AVEC LES QUESTIONS ÉNONCÉES À LA Q12, PUIS REPRENDRE À L'ÉTAPE DU PROCESSUS OÙ VOUS ÉTIEZ RENDU(E) :

Ressources (15 minutes)

Oui – Y avez-vous eu recours? Ce service vous a-t-il été utile? Le recommanderiez-vous?

Non – Ce service vous semble-t-il intéressant? Quelles seraient vos attentes?

| - | Si cet outil n'a pas été mentionné à la Q14 : En avez-vous déjà entendu parler? De quelle façon? | Si le(la) répondant(e) en a entendu parler : L'avez-vous utilisé? Pourquoi ou pourquoi pas? | Si le(la) répondant(e) l'a utilisé : Qu'avez-vous aimé ou pas aimé de cet outil? |

|---|---|---|---|

|

- | - | - |

|

- | - | - |

Leçons apprises (5 minutes)

CIBLE B/C : Quel conseil donneriez-vous aux entreprises qui n'ont aucune expérience avec le crédit d'impôt pour la RS&DE et qui envisagent de présenter leur première demande?

Prochaines étapes/réaction aux outils potentiels (5 minutes)