Public opinion research tracker: Baseline survey

Report of findings

Prepared for the Canadian Radio-television and Telecommunications Commission (CRTC)

Supplier: Ipsos Limited Partnership

Contract Number: CW2291885

Contract Value: $114,713.98 (including HST)

Award Date: 2023-02-27

Delivery Date: October 23, 2023

Registration Number: POR 131-22

For more information on this report, please contact ROP-POR@crtc.gc.ca

Ce rapport est aussi disponible en français

This public opinion research report presents the results of an online survey conducted by Ipsos Limited Partnership on behalf of the Canadian Radio-television and Telecommunications Commission (CRTC). The research study was conducted with 2,561 Canadians between June 8 to August 4, 2023.

Cette publication est aussi disponible en français sous le titre : Suivi de recherche sur l'opinion publique : Sondage de référence

This publication may be reproduced for non-commercial purposes only. Prior written permission must be obtained from the CRTC. For more information on this report, please contact CRTC at: ROPPOR@crtc.gc.ca or at:

Canadian Radio-television and Telecommunications Commission (CRTC)

1 Promenade du Portage

Gatineau, Quebec J8X 4B1

The Canadian Radio-television and Telecommunications Commission (CRTC)

Ottawa, Ontario

Canada

K1A ON2

Tel: 819-997-0313

Toll-free: 1-877-249-2782 (in Canada only)

Catalogue Number: BC92-129/2024E-PDF

International Standard Book Number (ISBN): 978-0-660-68992-0

© His Majesty the King in Right of Canada, 2023 © His Majesty the King in Right of Canada, as represented by the Canadian Radio-television and Telecommunications Commission, 2023.

Executive Summary

Introduction

Ipsos was commissioned by the Canadian Radio-television and Telecommunications Commission (CRTC) to conduct a baseline wave of public opinion research on Canadians views with respect to their broadcasting, online and telecommunications services.

Background

The CRTC regulates the communications industry in the public interest in a time of significant socio-cultural, economic and technological change and is looking to increase its capacity to measure and track Canadian public opinion. The importance of this grows when considering that the CRTC is implanting new legislation (Online Stream Act) and policy directions (Telecom and Broadcasting) that will require the CRTC to develop new regulatory approaches that consider the views of all Canadians to ensure the system includes and reflects fully the diversity of Canada. In light of these developments, the public opinion research is intended to support the CRTC's efforts to gather the views of all Canadians.

In 2021, the CRTC commissioned Ipsos to develop strategic options for Public Opinion Research. After considering the recommendations and resulting strategy that was presented in September 2022, the CRTC decided to implement a pilot project of the POR strategy and conduct a baseline wave of research. Moving forward, the study will evolve into a bi-annual tracking study.

Research Objectives

The primary objective of the POR is to gain a better understanding of the views of Canadians with respect to their broadcasting, online and telecommunications services and other matters of strategic importance for the CRTC. An essential component of the POR is to ensure the inclusion and representation of all Canadians. Specific focus is placed on ensuring sufficient participation from Anglophones, Francophones, Indigenous Peoples, Official Minority Language Communities (OLMC), Racialized Canadians, TSLGBTQ+ and those living in the North.

In developing the questionnaire, Ipsos worked with CRTC staff to synthesize and incorporate input from all relevant sectors. This included conducting a series of meetings with staff in the Broadcasting, Telecommunications, Compliance and Enforcement (C&E), and Consumer, Research and Communications (CRC) units.

The questionnaire included a core section of key tracking measures and sections to address more topical information needs that would be custom to each wave of research or rotated in future waves.

The baseline POR survey addressed the following areas:

- Consumers' satisfaction with their telecommunications and/or broadcasting services;

- Primary source(s) of media content and satisfaction with the quality of content;

- Broader attitudes, including affordability, quality of service, satisfaction, importance of local media, trust in media and cybersecurity;

- Classification questions to ensure the inclusion of diverse groups regarding Indigenous peoples, ethnicity, people born in or outside Canada, language spoken, sexual orientation, gender identity, household income, and persons with a disability;

- Ad-hoc issues- perceptions of international roaming.

Methodology

The POR was conducted through a quantitative survey executed through a mixed methodology approach including online and telephone interviews among a national sample of 2,561 Canadians aged 18 years and older (1,561 online, 1,000 telephone). Fieldwork was conducted from June 8 to August 4, 2023. Average survey length was 18 minutes (15 minutes online, 22 minutes by telephone).

Quotas and weighting were employed by gender, age and region to reflect the composition of the Canadian general population based on the latest Census. Results were accurate to within + 2.2 percentage points of what the results would have been had every Canadian been polled.

Minimum sample sizes (of at least 100) were achieved among key audiences including Anglophones (n=1842), Francophones (n-529), Indigenous peoples (n=121), Official Minority Language Communities (n=142), racialized Canadians (n=323), and 2SLGBTQI+ (n=214). Oversamples of TSLGBTQ+ Canadians and those residing in the North were required and notably, fieldwork in the North proved more challenging than anticipated and the target of n=100 could not be achieved in the fieldwork period (n=82 was achieved).

Notes to Readers

- All results in the report are expressed as a percentage, unless otherwise noted.

- Throughout the report, percentages may not always add to 100 due to rounding.

- When reporting sub-group variations, only differences that are significant at the 95% confidence level, indicative of a pattern and pertaining to a sub-group sample size of more than n=30 are discussed.

- For open-ended measures, results have been coded into thematic category and expressed as individual codes that align most closely to respondents answers and broader themes (NETs) for comparison purposes.

Expenditure

The contract value for the POR survey was $114,713.98 (including HST)

Key Findings

Virtually all adult Canadians report they currently receive one or more telecommunications, broadcast, or audio or video streaming services for personal use, and a strong majority of those who receive each type of service are satisfied with their provider.

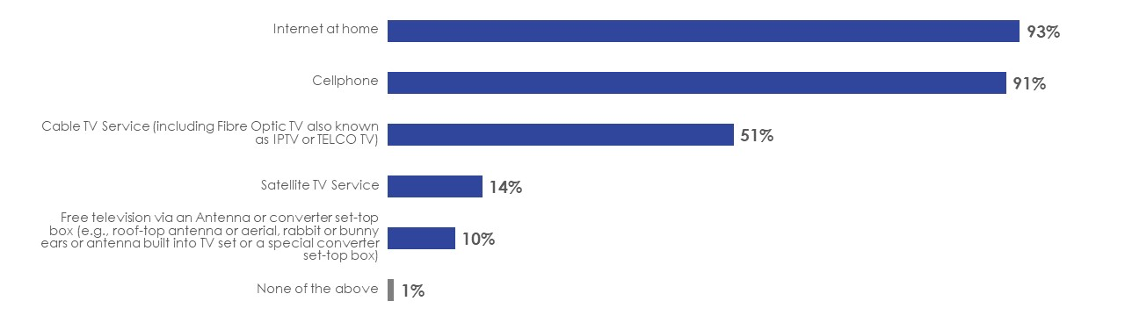

- More than ninety percent report they have internet service at home (93%) or cellphone service (91%), three-quarters subscribe or have access to at least one video streaming service (74%) and roughly half at least one audio streaming service (52%) or cable TV service (51%). Relatively few in comparison have satellite TV service (14%) or use free television services (10%).

- Satisfaction is highest for audio streaming services (73%), followed by two-thirds for internet (65%), video streaming (64%), or cellphone service (64%), and six in ten for cable TV (61%) or satellite TV service (59%).

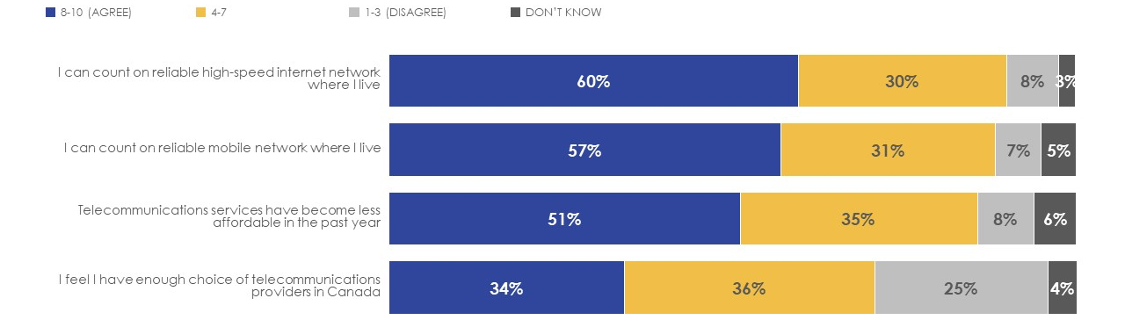

- Reliability is the most common factor driving satisfaction with internet service in particular, and to a lesser extent cellphone and cable TV service, and is mentioned more often as a positive reason than as a negative. Broader impressions of reliability are reasonably strong and the majority of Canadians feel that they count on reliable high-speed internet (60%) and mobile networks (57%) where they live.

- Affordability, while mentioned less often as a reason for satisfaction with the service in general, is cited more often among cellphone or cable TV customers as a reason for lower satisfaction. Most Canadians feel that telecommunications (51%), television (49%), and streaming video services (47%) have become less affordable in the past year, and only one-third that agree they have enough choice of telecommunications providers (34%).

- Quality and variety of content is by far the biggest reason for satisfaction with audio and video streaming services. Notably, nearly half of French-speakers (47%) feel that the content on these types of platforms should be regulated like traditional broadcasting compared to three in ten English-speakers (29%).

The majority of Canadians (66%) are confident in their ability to pay for the telecommunications, broadcast or streaming services they receive in the immediate future, however roughly one-quarter (27%) report they have had to make changes to their services recently to improve affordability.

- Two in ten (19%) made changes to make their services more affordable in the past month, while one in ten planned on cancelling their service but were convinced to stay with a better price (10%), cancelled and switched providers (9%) or cancelled entirely their services (8%).

- Those who made changes to improve affordability are most likely to have adjusted the services they receive or changed providers for their cellphone service, followed by home internet or video steaming services.

Canadians' use of international calling or text products or services is limited and relatively few have a strong understanding of the rate plans or options available. Affordability is the primary factor driving usage, however impressions of the reasonableness of the rates or cost of purchase are relatively weak.

- A sizeable minority of Canadians (34% to 44%) report they have never used each type of international calling or text product or service. Canadians are most likely to report having used international roaming through a flat-rate-per-day option before (31%), followed by domestic SIM/eSIM (25%), international roaming through a pay-per-text/call/MB option (24%) and international SIM/eSIM (21%). Few report using any product or service on a frequent basis with the largest proportion having used each once or twice a year (7% to 14%).

- The most common reason for using the product or service they did is because it was the most cost-effective option (45%), followed by the one they were most familiar with (39%), and the easiest, most convenient option to set up (26%).

- Nearly four in ten who used a domestic SIM/eSIM found the cost reasonable (36%), followed by international SIM/eSIM (32%), international roaming through a flat-rate-per-day option (21%) and international roaming through a pay-per-text/call/MB option (19%).

- Around one in ten (14%) of all Canadians agree that the rates they pay to use their cellphone while travelling outside of the country are reasonable and one third (32%) of those with a cellphone for personal use feel they have a good understanding of the rate plans/ options for using their cellphone outside of the country.

When asked about their primary sources for 'news and information' and 'entertainment', the vast majority of Canadians rely on video content for 'entertainment' and to a lesser extent for 'news and information', half use audio sources for either, while online media and print and are more common for 'news and information'. Nearly two-thirds (62%) are satisfied with the quality of the 'entertainment' content and just over half (54%) for 'news and information'.

- The most common sources of media content for 'news and information' are regular television (46%), followed by online media (36%), AM/FM radio (34%), online social media (25%) and print media (20%). For 'entertainment', the primary sources are online video streaming (45%) and regular television (43%), followed by online social media (34%).

- Satisfaction with 'entertainment' is highest for audio podcasts (70%) and generally consistent for all other sources (ranging from 61% to 65%), while satisfaction with 'news and info' is more varied and is highest for TV (60%) and print (59%), and lower for online social media (48%), social networking sites (51%), and online music streaming (50%).

Attitudes towards Canadian content specifically are generally positive but soft. While most feel it is at least somewhat important to have access to Canadian-made programming and that they rely on Canadian news media to understand the world, Canadian's impressions of the quality, variety and depth of content as well as trust in media are relatively weak and most do not feel reflected in the types of programming available or that it is relevant to their lives.

- Roughly four in ten agree that it is important for them to have access to Canadian-made television programs (41%) and music (38%), and are satisfied with the quality and variety of Canadian music available today (39% each). Closer to one-third are satisfied with the quality (35%) and variety (34%) of Canadian television programs, agree that the types of news, music, and television programming are relevant to their lives (36%) or that they see themselves reflected in the programming available (32%).

- Nearly half rely on Canadian news media to help them understand what's going on in the world (45%), and that news programming covers a diverse range of topics and issues (41%). Fewer agree that they trust the information provided by news media in Canada (36%), that the types of news programming offers a variety of perspectives (36%), and that they are satisfied the quality of information and analysis offered by Canadian news media (37%).

Differences by Demographics

Age cohort: Older Canadians (in particular 65 or older) are more likely to report they receive cellphone and cable TV service and to a lesser extent home internet than younger Canadians. They are more likely than younger Canadians to feel confident in their ability to pay for all their services in the immediate future and are less likely to have had to make changes in past month to improve affordability.

Older Canadians are more likely than younger Canadians to rely on regular television as their primary source of 'news and information' and 'entertainment' and AM/FM radio or print media sources for 'news and information'. They are more likely to be satisfied with the 'news and information' content they receive, to rely on and trust Canadians news media, and to be satisfied with the variety of opinions, quality, and depth of coverage. They are also more likely to feel it is important for them to have access to Canadian-made TV programs and music and to agree that the content of online streaming platforms should be regulated like traditional broadcasting.

Older Canadians are more likely than younger Canadians to report that they often receive unsolicited phone calls or emails trying to trick them into sharing personal information or clicking a malicious link and to feel that the amount has increased in the past year.

Younger Canadians are more likely than older Canadians to rely on online social media, online video streaming services, audio podcasts, and social networking sites for 'news and information' or 'entertainment' content, as well as online music streaming services for 'entertainment' content.

Region of residence: Residents of Quebec are more likely than those from other regions to rely on regular television as their primary source of 'news and information' and to be satisfied with both the 'entertainment' and 'news and information' content they receive. They are more likely to agree it is important for them to have access to Canadian-made TV programs and music, to be satisfied with the quality and variety of Canadian television programs and music available today, and to see themselves reflected in the programming available. They are also more likely to rely on Canadian news media and to be satisfied with the variety of opinions, quality, and depth of coverage.

They are also more likely to agree that they can count on reliable high-speed internet and mobile networks where they live and that they have enough choice of telecommunications providers.

Official Language: Differences by official language are virtually identical to those observed among residents of Quebec compared to those from other regions. French-speakers are more likely to report that their primary source of 'news and information' or 'entertainment' content is regular television, while English-speakers are more likely to rely on online video streaming services, online music streaming services, audio podcasts and social networking sites for both types of content. French-speakers are also more likely than English-speakers to be satisfied with both the 'entertainment' and 'news and information' content they receive.

They are more likely to agree it is important for them to have access to Canadian-made TV programs and music, to be satisfied with the quality and variety of Canadian television programs and music available today, and to see themselves reflected in the programming available, and that content available through online video or streaming platforms should be regulated similar to traditional broadcasting. They are also more likely to rely on Canadian news media, trust the information provided by news media in Canada to be accurate and impartial, and to be satisfied with the variety of opinions, quality, and depth of coverage.

French-speakers are also more likely than English-speakers to agree that they can count on reliable high-speed internet and mobile networks where they live and that they have enough choice of telecommunications providers.

English-speakers are more likely than French-speakers to agree that they or someone they know has experienced a scam attempt in the past month.

Household income: Lower income households (in particular with annual incomes of $40k or less) are less likely than higher income households to report they currently have cellphone or internet service. They are less likely to feel confident in their ability to pay for the services they have and are more likely to have had to make changes recently to improve affordability or to have cancelled a service entirely.

Higher income households are more likely than lower income households to rely on online video streaming services as their primary source of 'entertainment' content. They are also more likely to agree that they often receive unsolicited emails trying to trick them into clicking malicious links, and that they or someone they know have experienced a scam attempt.

Indigenous status: Those who identify as Indigenous are less likely than those who do not identify as Indigenous to report they receive internet or cable TV service and are more likely to report they currently have satellite TV service. They are less likely to feel confident in their ability to pay for the services they have and are more likely to have had to make changes recently to improve affordability, switched to a different provider or to have cancelled a service entirely. They are also less likely to agree that they can count on reliable high-speed internet or mobile networks where they live, and that they have enough choice of telecommunications providers.

Ethnicity: Racialized Canadians are more likely than those who are not racialized to report they currently receive cellphone service and less likely to report they receive internet or cable TV service. They are more likely to have had to make changes to their services recently to improve affordability, switched to a different provider, were convinced to stay with a better price or to have cancelled a service entirely. They are also less likely to agree that they can count on reliable high-speed internet where they live.

Racialized Canadians are more likely than those who are not racialized to rely on online video streaming services and online social media as their primary sources of 'news and information' and 'entertainment' content and are also more likely to rely on online music streaming services for 'entertainment'.

Political Neutrality Statement

I hereby certify as Senior Officer of Ipsos that the deliverables fully comply with the Government of Canada political neutrality requirements outlined in the Communications Policy of the Government of Canada and Procedures for Planning and Contracting Public Opinion Research. Specifically, the deliverables do not include information on electoral voting intentions, political party preferences, standings with the electorate or ratings of the performance of a political party or its leaders.

Mike Colledge

President

Ipsos Public Affairs

Detailed Findings

Satisfaction with service(s) overall

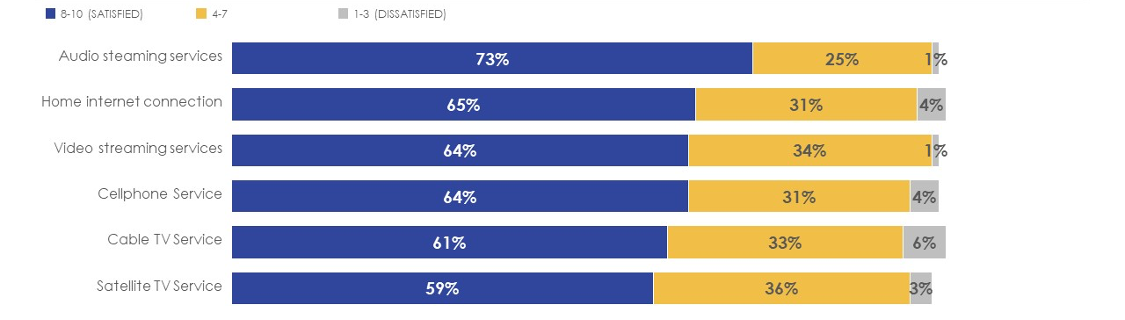

Among those who report they currently have each type of service, nearly three-quarters (73%) are satisfied with the audio streaming service they receive, followed by roughly two-thirds for their home internet (65%), video streaming (64%), and cellphone service (64%). Six in ten are satisfied with their cable TV (61%) or satellite TV service (59%).

- Canadians 65 or older and residents of Quebec are more likely to be satisfied with nearly all the services they receive than younger Canadians and those from other regions respectively.

Figure 1: Satisfaction with providers by service

Base: Those who have cable TV, satellite TV, internet, cellphone, video streaming and/ or audio streaming services (n=2529)

Q8. Overall, how satisfied are you with the [SERVICE] you receive from [PROVIDER]?

This horizontal bar chart shows responses to a question about satisfaction with providers by each type of service. Respondents were asked to provide ratings on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as satisfied, 4 to 7 as neither satisfied nor dissatisfied and 1 to 3 as dissatisfied. A total of 2529 who have cable TV, satellite TV, internet, cellphone, video streaming and/ or audio streaming services answered this question as follows:

- Audio streaming services: 73% satisfied, 25% neither satisfied nor dissatisfied , 1% dissatisfied.

- Home internet connection: 65% satisfied, 31% neither satisfied nor dissatisfied , 4% dissatisfied.

- Video streaming services: 64% satisfied, 34% neither satisfied nor dissatisfied , 1% dissatisfied.

- Cellphone Service: 64% satisfied, 31% neither satisfied nor dissatisfied , 4% dissatisfied.

- Cable TV Service: 61% satisfied, 33% neither satisfied nor dissatisfied , 6% dissatisfied.

- Satellite TV Service: 59% satisfied, 36% neither satisfied nor dissatisfied , 3% dissatisfied.

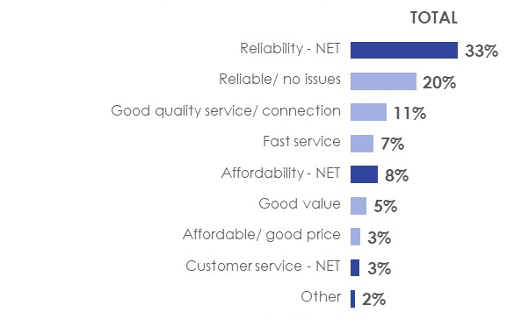

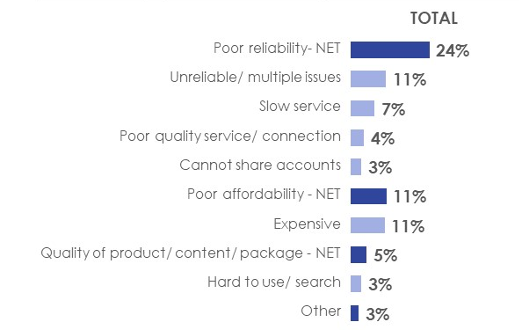

When asked to explain their satisfaction with the internet service they receive, nearly four in ten provide a positive reason (39%) while slightly fewer provide a negative reason (36%). The most common positive comments relate to reliability (33%), and specifically not having issues (20%), a good connection (11%) and fast service (7%), followed by mentions of affordability (8%). The most common negative comments include poor reliability (24%), and specifically having multiple issues (11%), and slow service (7%), while one in ten (11%) mention poor affordability.

Figure 2: Positive reason(s) for satisfaction with service by internet provider

Base: Those who have internet services (n=2390)

Q9. You provided a rating of [RATING] out of 10 for the [SERVICE] you receive from [PROVIDER]. Why do you say that? Please be as detailed in your response as possible.

This horizontal bar chart shows the positive reasons for satisfaction with the internet service received. Respondents were asked to explain the reasons for the satisfaction rating provided for their internet service provider. A total of 2390 internet service customers answered as follows:

- Reliability (NET): 33%.

- Reliable/ no issues: 20%.

- Good quality service/ connection: 11%.

- Fast service: 7%.

- Affordability (NET): 8%.

- Good value: 5%.

- Affordable/ good price: 3%.

- Customer service (NET): 3%.

- Other: 2%.

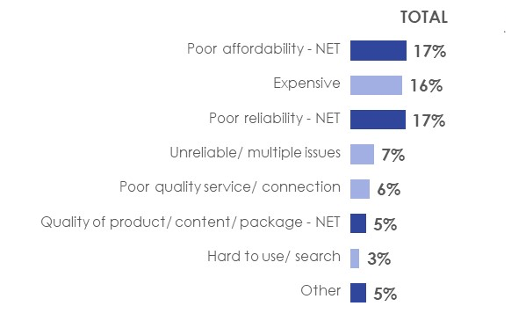

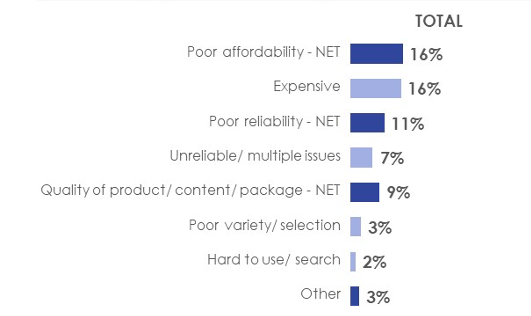

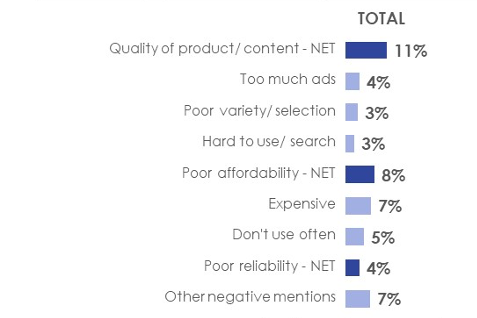

Figure 3: Negative reason(s) for satisfaction with service by internet provider

Base: Those who have internet services (n=2390)

Q9. You provided a rating of [RATING] out of 10 for the [SERVICE] you receive from [PROVIDER]. Why do you say that? Please be as detailed in your response as possible.

This horizontal bar chart shows the negative reasons for satisfaction with the internet service received. Respondents were asked to explain the reasons for the satisfaction rating provided for their internet service provider. A total of 2390 internet service customers answered as follows:

- Poor reliability (NET): 24%.

- Unreliable/ multiple issues: 11%.

- Slow service: 7%.

- Poor quality service/ connection: 4%.

- Cannot share accounts: 3%

- Poor affordability (NET): 11%.

- Expensive: 11%.

- Quality of product/ content/ package (NET): 5%.

- Hard to use/ search: 3%.

- Other: 3%.

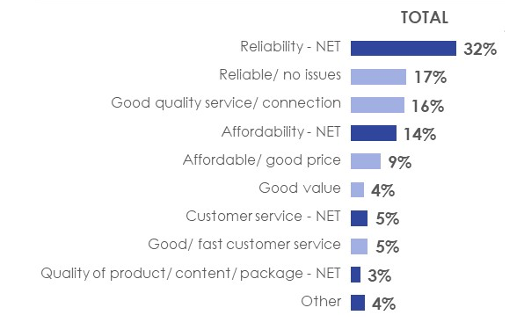

When asked to explain their satisfaction with the cellphone service they receive, nearly half provide a positive reason (47%) and four in ten a negative reason (38%). The most common positive comments relate to reliability (32%), and specifically not having issues (17%) or good connection (16%), followed by affordability (14%). The most common negative comments include poor affordability (17%) and poor reliability (17%).

Figure 4: Positive reason(s) for satisfaction with service by cellphone provider

Base: Those who have cellphone services (n=2318)

Q9. You provided a rating of [RATING] out of 10 for the [SERVICE] you receive from [PROVIDER]. Why do you say that? Please be as detailed in your response as possible.

This horizontal bar chart shows the positive reasons for satisfaction with the cellphone service received. Respondents were asked to explain the reasons for the satisfaction rating provided for their cellphone service provider. A total of 2318 cellphone service customers answered as follows:

- Reliability (NET): 32%.

- Reliable/ no issues: 17%.

- Good quality service/ connection: 16%.

- Affordability (NET): 14%.

- Affordable/ good price: 9%.

- Good value: 4%.

- Customer service (NET): 5%.

- Good/ fast customer service: 5%.

- Quality of product/ content/ package (NET): 3%.

- Other: 4%.

Figure 5: Negative reason(s) for satisfaction with service by cellphone provider

Base: Those who have cellphone services (n=2318)

Q9. You provided a rating of [RATING] out of 10 for the [SERVICE] you receive from [PROVIDER]. Why do you say that? Please be as detailed in your response as possible.

This horizontal bar chart shows the negative reasons for satisfaction with the cellphone service received. Respondents were asked to explain the reasons for the satisfaction rating provided for their cellphone service provider. A total of 2318 cellphone service customers answered as follows:

- Poor affordability (NET): 17%.

- Expensive: 16%.

- Poor reliability (NET): 17%.

- Unreliable/ multiple issues: 7%.

- Poor quality service/ connection: 6%.

- Quality of product/ content/ package (NET): 5%.

- Hard to use/ search: 3%.

- Other: 5%.

When asked to explain their satisfaction with the cable TV service they receive, nearly four in ten (39%) provide a positive reason while slightly fewer provide a negative reason (37%). The most common positive comments relate to reliability (23%), and specifically having no issues (13%) and good quality connection (10%), followed by quality of the content (8%) and affordability (7%). The most common negative comments include poor affordability (14%), poor quality of the content/packages (13%) and poor reliability (12%).

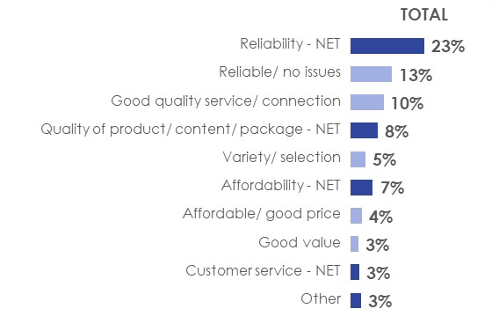

Figure 6: Positive reason(s) for satisfaction with service by cable TV provider

Base: Those who have cable TV services (n=1324)

Q9. You provided a rating of [RATING] out of 10 for the [SERVICE] you receive from [PROVIDER]. Why do you say that? Please be as detailed in your response as possible.

This horizontal bar chart shows the positive reasons for satisfaction with the cable TV service received. Respondents were asked to explain the reasons for the satisfaction rating provided for their cable TV service provider. A total of 1324 cable TV service customers answered as follows:

- Reliability (NET): 23%.

- Reliable/ no issues: 13%.

- Good quality service/ connection: 10%.

- Quality of product/ content/ package (NET): 8%.

- Variety/ selection: 5%.

- Affordability (NET): 7%.

- Affordable/ good price: 4%.

- Good value: 3%.

- Customer service (NET): 3%.

- Other: 3%.

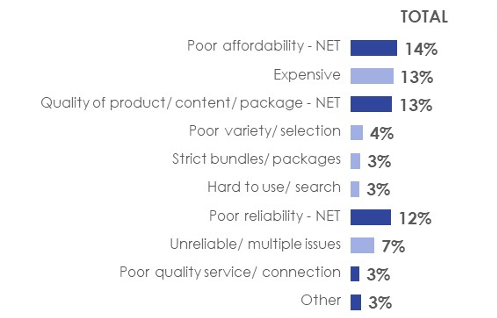

Figure 7: Negative reason(s) for satisfaction with service by cable TV provider

Base: Those who have cable TV services (n=1324)

Q9. You provided a rating of [RATING] out of 10 for the [SERVICE] you receive from [PROVIDER]. Why do you say that? Please be as detailed in your response as possible.

This horizontal bar chart shows the negative reasons for satisfaction with the cable TV service received. Respondents were asked to explain the reasons for the satisfaction rating provided for their cable TV service provider. A total of 1324 cable TV service customers answered as follows:

- Poor affordability (NET): 14%.

- Expensive: 13%.

- Quality of product/ content/ package (NET): 13%.

- Poor variety/ selection: 4%.

- Strict bundles/ packages: 3%.

- Hard to use/ search: 3%.

- Poor reliability (NET): 12%.

- Unreliable/ multiple issues: 7%.

- Poor quality service/ connection: 3%.

- Other: 3%.

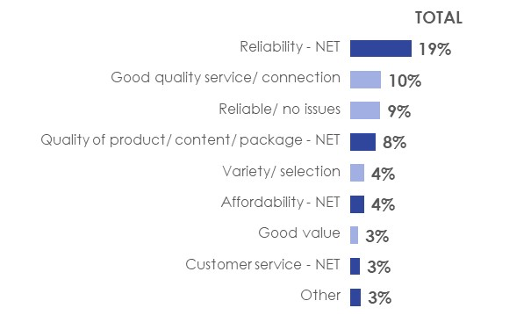

When asked to explain their satisfaction with the satellite TV service they receive, roughly one-third provide either a positive (35%) or negative reason (34%). The most common positive comments relate to reliability (19%), and specifically good quality connection (10%) and no issues (9%), followed by the quality of product/ content or package (8%). The most common negative comments include poor affordability (16%), followed by poor reliability (11%) and quality of content /packages (9%).

Figure 8: Positive reason(s) for satisfaction with service by satellite TV provider

Base: Those who have satellite TV services (n=345)

Q9. You provided a rating of [RATING] out of 10 for the [SERVICE] you receive from [PROVIDER]. Why do you say that? Please be as detailed in your response as possible.

This horizontal bar chart shows the positive reasons for satisfaction with the satellite TV service received. Respondents were asked to explain the reasons for the satisfaction rating provided for their satellite TV service provider. A total of 345 satellite TV service customers answered as follows:

- Reliability (NET): 19%.

- Good quality service/ connection: 10%.

- Reliable/ no issues: 9%.

- Quality of product/ content/ package (NET): 8%.

- Variety/ selection: 4%.

- Affordability (NET): 4%.

- Good value: 3%.

- Customer service (NET): 3%.

- Other: 3%.

Figure 9: Negative reason(s) for satisfaction with service by satellite TV provider

Base: Those who have satellite TV services (n=345)

Q9. You provided a rating of [RATING] out of 10 for the [SERVICE] you receive from [PROVIDER]. Why do you say that? Please be as detailed in your response as possible.

This horizontal bar chart shows the negative reasons for satisfaction with the satellite TV service received. Respondents were asked to explain the reasons for the satisfaction rating provided for their satellite TV service provider. A total of 345 satellite TV service customers answered as follows:

- Poor affordability (NET): 16%.

- Expensive: 16%.

- Poor reliability (NET): 11%.

- Unreliable/ multiple issues: 7%.

- Quality of product/ content/ package (NET): 9%.

- Poor variety/ selection: 3%.

- Hard to use/ search: 2%.

- Other: 3%.

When asked to explain their satisfaction with the video streaming service(s) they receive, more than six in ten provide a positive reason (62%) while nearly half provide a negative reason (48%). The most common positive comments relate to quality of product/ content (42%), including variety (26%) and good content (18%), followed by reliability (21%) and affordability (14%). The most common negative comments include quality of the content (32%), and specifically poor variety (19%), followed by poor affordability (15%) and poor reliability (11%).

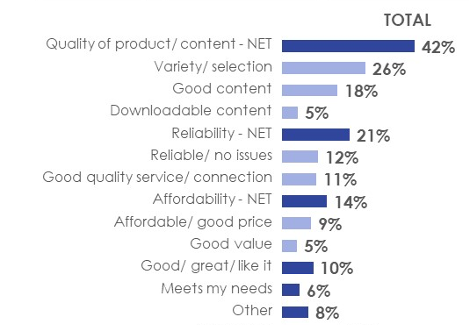

Figure 10: Positive reason(s) for satisfaction with service by video streaming services provider

Base: Those who have video Streaming services (n=1875)

Q9. You provided a rating of [RATING] out of 10 for the [SERVICE] you receive from [PROVIDER]. Why do you say that? Please be as detailed in your response as possible.

This horizontal bar chart shows the positive reasons for satisfaction with the video streaming service received. Respondents were asked to explain the reasons for the satisfaction rating provided for their video streaming service provider. A total of 1875 video streaming service customers answered as follows:

- Quality of product/ content/ package (NET): 42%.

- Variety/ selection: 26%.

- Good content: 18%.

- Downloadable content: 5%.

- Reliability (NET): 21%.

- Reliable/ no issues: 12%.

- Good quality service/ connection: 11%.

- Affordability (NET): 14%.

- Affordable/ good price: 9%.

- Good value: 5%.

- Good/ great/ like it: 10%.

- Meets my needs: 6%.

- Other: 8%.

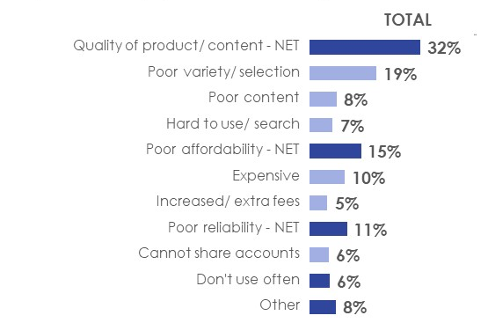

Figure 11: Negative reason(s) for satisfaction with service by video streaming services provider

Base: Those who have video Streaming services (n=1875)

Q9. You provided a rating of [RATING] out of 10 for the [SERVICE] you receive from [PROVIDER]. Why do you say that? Please be as detailed in your response as possible.

This horizontal bar chart shows the negative reasons for satisfaction with the video streaming service received. Respondents were asked to explain the reasons for the satisfaction rating provided for their video streaming service provider. A total of 1875 video streaming service customers answered as follows:

- Quality of product/ content (NET): 32%.

- Poor variety/ selection: 19%.

- Poor content: 8%.

- Hard to use/ search: 7%.

- Poor affordability (NET): 15%.

- Expensive: 10%.

- Increased/ extra fees: 5%.

- Poor reliability (NET): 11%.

- Cannot share accounts: 6%.

- Don't use often: 6%.

- Other: 8%.

When asked to explain their satisfaction with the audio streaming service(s) they receive, six in ten provide a positive reason (61%) while nearly three in ten provide a negative reason (28%). The most common positive comments relate to quality of content (38%), and specifically variety (23%), followed by reliability (19%) and affordability (11%). The most common negative comments include poor quality of the content (11%) and poor affordability (8%).

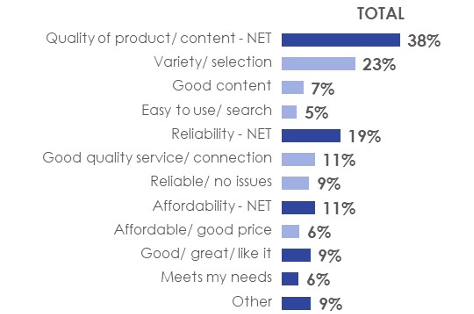

Figure 12: Positive reason(s) for satisfaction with service by audio streaming services provider

Base: Those who have Audio Streaming services (n=1313)

Q9. You provided a rating of [RATING] out of 10 for the [SERVICE] you receive from [PROVIDER]. Why do you say that? Please be as detailed in your response as possible.

This horizontal bar chart shows the positive reasons for satisfaction with the audio streaming service received. Respondents were asked to explain the reasons for the satisfaction rating provided for their audio streaming service provider. A total of 1313 audio streaming service customers answered as follows:

- Quality of product/ content (NET): 38%.

- Variety/ selection: 23%.

- Good content: 7%.

- Easy to use/ search: 5%.

- Reliability (NET): 19%.

- Good quality service/ connection: 11%.

- Reliable/ no issues: 9%.

- Affordability (NET): 11%.

- Affordable/ good price: 6%.

- Good/ great/ like it: 9%.

- Meets my needs: 6%.

- Other: 9%.

Figure 13: Negative reason(s) for satisfaction with service by audio streaming services provider

Base: Those who have Audio Streaming services (n=1313)

Q9. You provided a rating of [RATING] out of 10 for the [SERVICE] you receive from [PROVIDER]. Why do you say that? Please be as detailed in your response as possible.

This horizontal bar chart shows the negative reasons for satisfaction with the audio streaming service received. Respondents were asked to explain the reasons for the satisfaction rating provided for their audio streaming service provider. A total of 1313 audio streaming service customers answered as follows:

- Quality of product/ content (NET): 11%.

- Too much ads: 4%.

- Poor variety/ selection: 3%.

- Hard to use/ search: 3%.

- Poor affordability (NET): 8%.

- Expensive: 7%.

- Don't use often: 5%.

- Poor reliability (NET): 4%.

- Other: 7%.

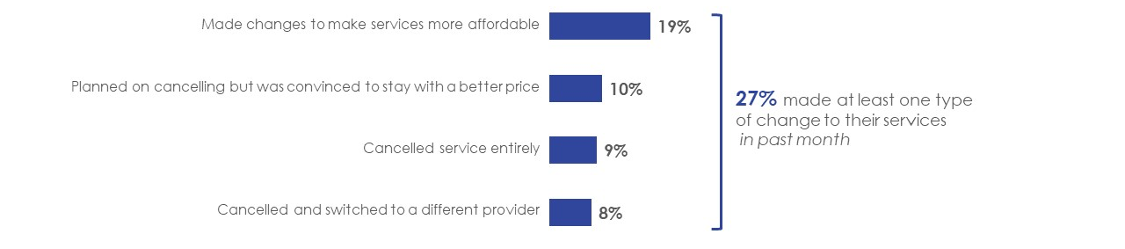

Changes to Services in Past Month

Among those who receive telecommunications, TV, audio and/or video subscription services, roughly one-quarter (27%) made some type of change to their services to improve the affordability in the past month. Nearly two in ten (19%) made changes in the past month to make their services more affordable, while one in ten planned on cancelling their service but were convinced to stay with a better price (10%), cancelled and switched providers (9%) or cancelled entirely their services (8%).

- Younger Canadians (in particular those under 35) are more likely than older Canadians to have made changes to their services to make them more affordable, planned on cancelling but were convinced to stay with a better price, cancelled service entirely or cancelled and switched to a different provider.

- Households with income of less than $40,000 are more likely to have made changes to make their services more affordable (25%) or were convinced to stay with a better price (15%) than higher income households.

- Those who identify as Indigenous and racialized Canadians are more likely than those who are not Indigenous or racialized to have made changes to their services to make them more affordable (27% and 22% respectively) or cancelled and switched to a different provider (11% and 12%). Racialized Canadians are also more likely than those who are not racialized to have been convinced to stay with a better price (16%).

Figure 14: Changes made to services to make them more affordable (in past month)

Base: Those who have cable TV, satellite TV, internet, cellphone, video streaming and/ or audio streaming services (n=2529)

Q10. Thinking about the last month, have you or anyone in your household made changes to any of your telecommunications, television, audio and/or video subscription services (e.g., changed package) in order to make them more affordable, planned on cancelling but was convinced to stay with a better price or cancelled any services (and/or switched to a different provider) because you could no longer afford them?

This horizontal bar chart shows the type of changes made to telecommunications, television, audio and/or video subscription services in the past month to make them more affordable. Those who have cable TV, satellite TV, internet, cellphone, video streaming and/ or audio streaming services were asked this question. A total of 2529 answered as follows:

- Made changes to make services more affordable: 19%.

- Planned on cancelling but was convinced to stay with a better price: 10%.

- Cancelled service entirely: 9%.

- Cancelled and switch to a different provider: 8%.

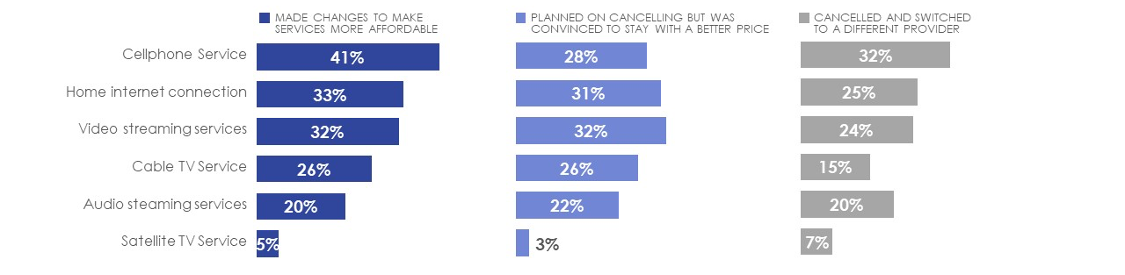

Among the 19% who made changes to make services more affordable, four in ten made changes to their cellphone service (41%), followed by home internet (33%) or video streaming services (32%), cable TV service (26%), audio streaming services (20%), and satellite TV service (5%).

Among the 10% who were convinced to stay with a better price, just over three in ten mention this was for video streaming services (32%) or home internet (31%), followed by cellphone (28%), cable TV (26%), audio steaming services (22%), and satellite TV service (3%).

Among the 8% who cancelled and switched to a different provider, one-third report this was for their cellphone service (32%), followed by home internet (25%), video streaming services (24%), audio streaming services (20%), cable TV (15%), and satellite TV service (7%).

- Younger Canadians are more likely to have made changes to their cellphone, video streaming or audio streaming services than older Canadians, while those 45 or older (in particular over 55) are more likely to have made changes to their cable TV service than those under 45 years old.

Figure 15: Changes made by type of service(s)

Base: Those who made changes (n=474); planned on cancelling but convinced to stay (n=255); cancelled and switched (n=196)

Q11. Which of these services did you, or someone in your household, ['make changes to'/'plan on cancelling but were convinced to stay with a better price instead'/'cancel and switch to a different provider'] in the last month?

This horizontal bar chart shows the type of changes made by each service in the past month to make them more affordable. Sample size varies by type of change, 474 made changes; 255 planned on cancelling but convinced to stay and 196 cancelled and switched.

- Made changes to make services more affordable: 41% Cellphone service, 33% Home internet connection, 32% Video streaming services, 26% Cable TV service, 20% Audio streaming services, 5% Satellite TV service

- Planned on cancelling but was convinced to stay with a better price: 28% Cellphone service, 31% Home internet connection, 32% Video streaming services, 25% Cable TV service, 22% Audio streaming services, 3% Satellite TV service

- Cancelled and switched to a different provider: 32% Cellphone service, 25% Home internet connection, 24% Video streaming services, 24% Cable TV service, 20% Audio streaming services, 7% Satellite TV service

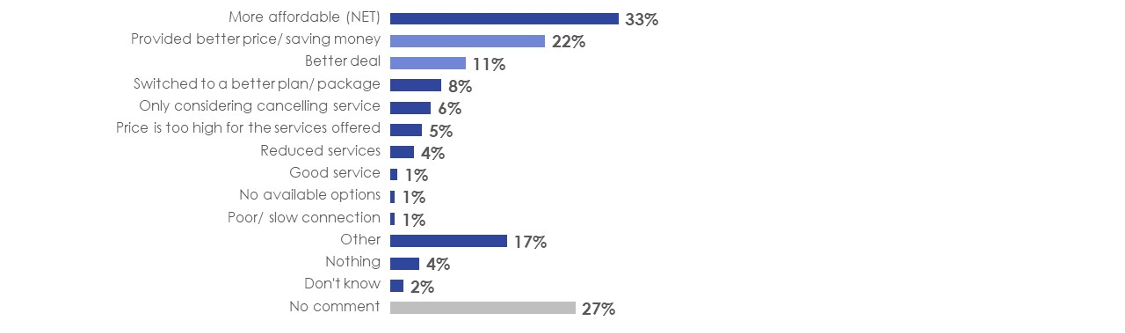

Among those who planned on cancelling but were convinced to stay with a better price, the main reasons why are because they were able to make their services more affordable (33%), and specifically provided a better price (22%) and received a better deal (11%), followed by switched to better plans or packages (8%).

Figure 16: Reason(s) why for those who planned on cancelling but were convinced to stay with a better price

Base: Those who planned on cancelling but were convinced to stay with a better price (n=255)

Q13. You indicated you had planned on cancelling a service but were convinced to stay with a better price. Please provide more detail on your experience and why you ended up adjusting your services instead of cancelling.

This horizontal bar chart shows the reasons why those who planned on cancelling their services but were convinced to stay with a better price ended up adjusting them instead of cancelling. A total of 255 customers who planned on cancelling their service but were convinced to stay with a better price gave the following reasons:

- More affordable (NET): 33%.

- Provided better price/ saving money: 22%.

- Better deal: 11%.

- Switched to a better plan/ package: 8%.

- Only considering cancelling service: 6%.

- Price is too high for the services offered: 5%.

- Reduced services: 4%.

- Good service: 1%.

- No available options: 1%.

- Poor/ slow connection: 1%.

- Other: 17%.

- Nothing: 4%.

- Don't know: 2%.

- No comment: 27%.

One in ten (9%) Canadians report having cancelled their cable TV service in the past month, 5% home internet, cellphone or satellite TV service, 4% video streaming services and 2% audio streaming services.

- Older Canadians (in particular those 55 or older) are less likely to have cancelled any of the services they receive in the past month than younger Canadians.

- Households with income less than $40k are more likely than higher income households to have cancelled their home internet service (9%) than higher income households.

- Racialized Canadians are more likely than those who are not racialized to have cancelled their cable TV (12%), home internet (8%), cable TV (8%) or satellite TV service (7%), while those who identify as Indigenous are more likely to have cancelled their home internet service (9%) than those who do not.

Figure 17: Cancellation of service entirely

Base: All respondents (n=2561)

Q12. And, which of these services did you, or someone in your household, cancel entirely?

This horizontal bar chart shows the services that were cancelled entirely. A total of 2561 respondents were asked which services they or someone in their household cancelled entirely:

- Cable TV service: 9%.

- Home internet connection: 5%.

- Cellphone service: 5%.

- Satellite TV service: 5%.

- Video streaming service: 4%.

- Audio streaming service: 2%.

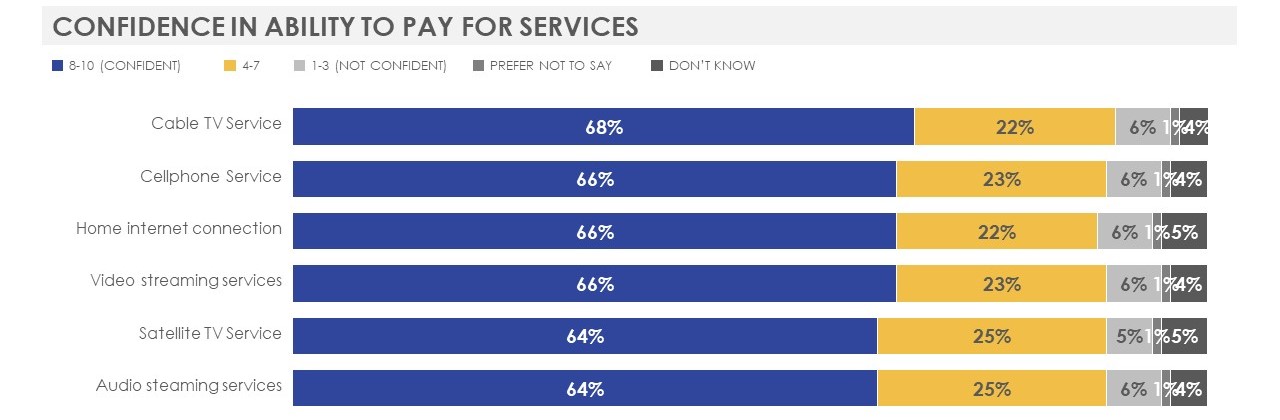

Confidence in ability to pay for services

Two-thirds (66%) of Canadians are confident that they will be able to pay for their telecommunications, television, audio and/or video subscription services without making any changes in the next three months. Roughly one-quarter (23%) express more moderate confidence, while 7% are not confident in their ability to pay for their services without making adjustments.

- Canadians 65 or older (70%), men (69%), and residents of Quebec (71%) are more likely to feel confident in their ability to pay for their services, while those who identify as Indigenous (52%), persons with a disability (54%), those with lower household income (in particular less than $40,000, 55%), residents of Atlantic Canada (58%), those who identify as TSLGBTQ+ (59%), and women (63%) are less likely.

Figure 18: Confidence in ability to pay for service(s)

Base: Those who have cable TV, satellite TV, internet, cellphone, video streaming and/ or audio streaming services (n=2529)

Q14. How confident or not are you that you and your household will be able to pay for your telecommunications, television, audio and/or video subscription services without making any changes in the next three months?

This horizontal bar chart shows responses to a question about the confidence customers have in the ability to pay for their services in the next three months. Respondents were asked to provide ratings on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as confident, 4 to 7 as neither confident nor not confident and 1 to 3 as not confident. A total of 2529 respondents answered as follows:

- 66% confident, 23% neither confident nor not confident, 7% not confident, 1% prefer not to say and 4% don't know.

Among those who report they currently have each service, confidence in ability to pay for their services without making any changes in the next three month is consistent by type of service. Roughly two-thirds of those who receive cable TV service are confident in their ability to pay (68%), followed closely by those who have cellphone, internet service or video streaming services (66% each), and those who have satellite TV or audio streaming services (64%).

Figure 19: Confidence in ability to pay by type of service

Base: Those who have Cellphone, Home Internet, Cable TV, Satellite TV, audio or video streaming services (n=varies)

Q14. How confident or not are you that you and your household will be able to pay for your telecommunications, television, audio and/or video subscription services without making any changes in the next three months?

This horizontal bar chart shows responses to a question about the confidence customers have in the ability to pay for their services in the next three months by each type of service. Respondents were asked to provide ratings on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as confident, 4 to 7 as neither confident nor not confident and 1 to 3 as not confident. Sample sizes vary.

- Cable TV service: 68% confident, 22% neither confident nor not confident l, 6% not confident, 1% prefer not to say and 4% don't know.

- Cellphone service: 66% confident, 23% neither confident nor not confident, 6% not confident, 1% prefer not to say and 4% don't know.

- Home internet connection: 66% confident, 22% neither confident nor not confident, 6% not confident, 1% prefer not to say and 5% don't know.

- Video streaming services: 66% confident, 23% neither confident nor not confident, 6% not confident, 1% prefer not to say and 4% don't know.

- Satellite TV service: 64% confident, 25% neither confident nor not confident, 5% not confident, 1% prefer not to say and 5% don't know.

- Audio streaming services: 64% confident, 25% neither confident nor not confident, 6% not confident, 1% prefer not to say and 4% don't know.

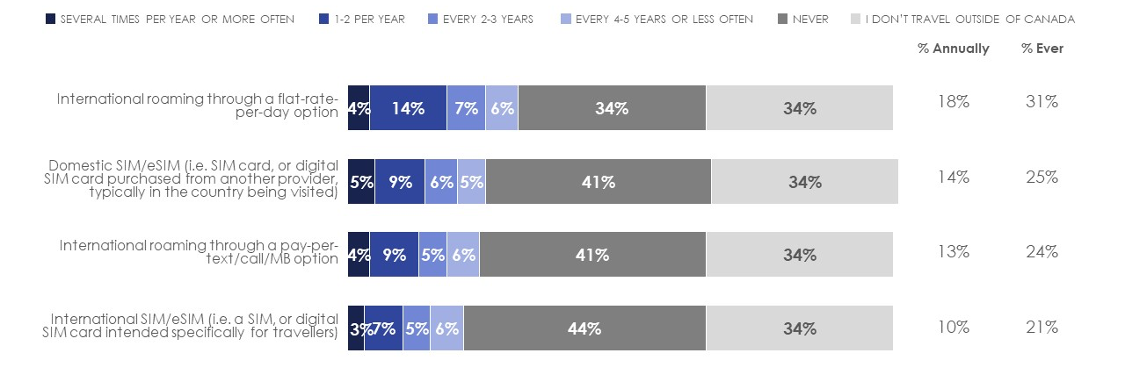

Usage and Attitudes towards international roaming

Usage and attitudes towards international roaming were assessed as an ad-hoc issue in the survey. Canadians' use of international calling and texting services are limited with between one-third to more than four in ten (34% to 44%) who have never used any of these products or services. Canadians who have a cellphone for personal use are most likely to report having used international roaming through a flat-rate-per-day option before (31%), followed by domestic SIM/eSIM (25%), international roaming through a pay-per-text/call/MB option (24%) and international SIM/eSIM (21%). Few report using any international calling or text product or service on a frequent basis with the largest proportion (7% to 14%) having used each once or twice a year.

Figure 20: Frequency of use of international calling or text product or service

Base: Those who have cellphone services (n=2318)

Q15. Thinking about when using your personal cellphone while travelling outside of Canada, how often do you use you each of the following types of products or services?

This horizontal bar chart shows responses to a question about the frequency of international roaming use. Respondents were asked how often they use different types of roaming products and services. A total of 2318 cellphone customers answered as follows.

- International roaming through a flat-rate-per-day option: 4% several times per year or more often, 14% once or twice per year, 7% every two to three years, 6% every four to five years or less often, 34% never and 34% don't travel outside of Canada.

- Domestic SIM/eSIM (i.e. SIM card or digital SIM card purchased from another provider, typically in the country being visited): 5% several times per year or more often, 9% once or twice per year, 6% every two to three years, 5% every four to five years or less often, 41% never and 34% don't travel outside of Canada.

- International roaming through a pay-per-text/call/MB option: 4% several times per year or more often, 9% once or twice per year, 5% every two to three years, 6% every four to five years or less often, 41% never and 34% don't travel outside of Canada.

- International SIM/eSIM (i.e. SIM card or digital SIM card intended specifically for travelers): 3% several times per year or more often, 7% once or twice per year, 5% every two to three years, 6% every four to five years or less often, 44% never and 34% don't travel outside of Canada.

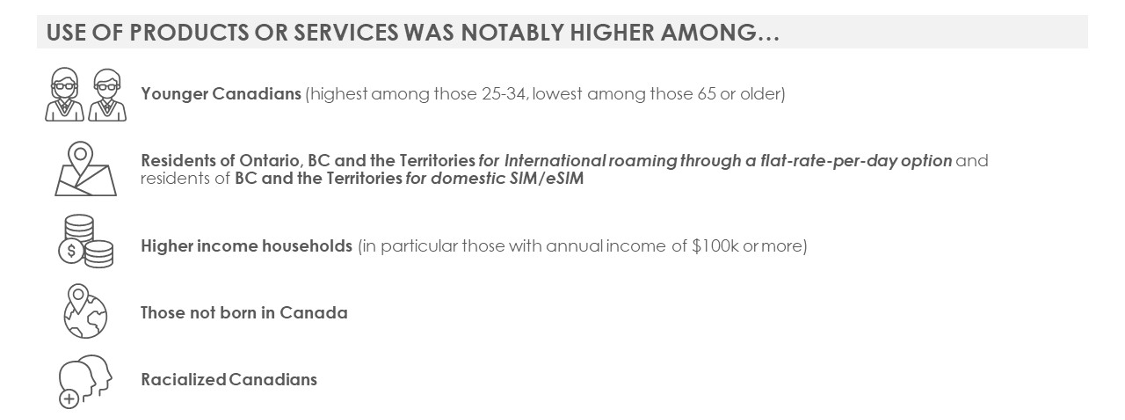

Figure 21: Profile of users of international calling or text product or service

This image shows a profile of users of international calling or text product or service and highlights notable differences in demographics. Use of international calling or text products was notably higher among younger Canadians (highest among those 25-34, lowest among those 65 or older), residents of Ontario, BC and the Territories for International roaming through a flat-rate-per-day option and residents of BC and the Territories for domestic SIM/eSIM, higher income households (in particular those with annual income of $100k or more), those not born in Canada, and racialized Canadians.

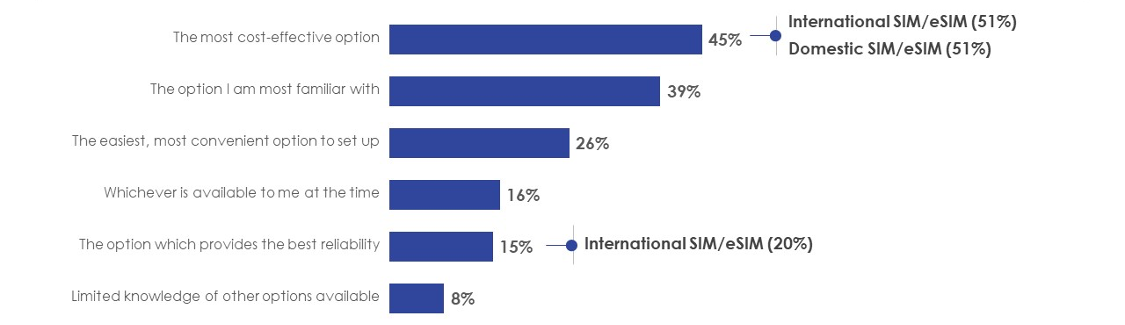

The most common reason for customers using the international calling or text product or service they did is because it was the most cost-effective option (45%), followed by the option they were most familiar with (39%) and the easiest, most convenient option to set up (26%).

- Those who reported having used an international or domestic SIM/eSIM before are more likely to say it was the most cost-effective option, while those who have used an international SIM/eSIM are also more likely to cite that it is the option which provided the best reliability.

- Younger Canadians and those in lower income households are more likely to say it is because it was the most cost-effective option than older Canadians and higher income households respectively.

Figure 22: Reason(s) for using international calling or text product or service

Base: Those who used personal cellphone while travelling outside of Canada (n=1073)

Q16. Generally speaking, what informs your decision about which type of international calling or text product or service to use when travelling outside of Canada? Please select all that apply.

This horizontal bar chart shows the reasons for using international calling or text products or services. Respondents were asked to explain what informs their decision on which type of international roaming product or service to use when travelling outside of Canada. Those who used personal cellphone while travelling outside of Canada. A total of 1073 users answered as follows:

- The most cost-effective option: 45%.

- The option I am more familiar with: 39%.

- The easiest, most convenient option to set up: 26%.

- Whichever is available to me at the time: 16%.

- The option which provides the best reliability: 15%.

- Limited knowledge of other options available: 8%.

Among those who have used each international calling or text product or service before, relatively few felt the rates and /or cost of purchase were reasonable and most had softer, more moderate impressions. Nearly four in ten who used a domestic SIM/eSIM found the cost reasonable (36%), followed by international SIM/eSIM (32%), international roaming through a flat-rate-per-day option (21%) and international roaming through a pay-per-text/call/MB option (19%).

- Older Canadians are more likely to say that the rates and /or cost of purchase were unreasonable.

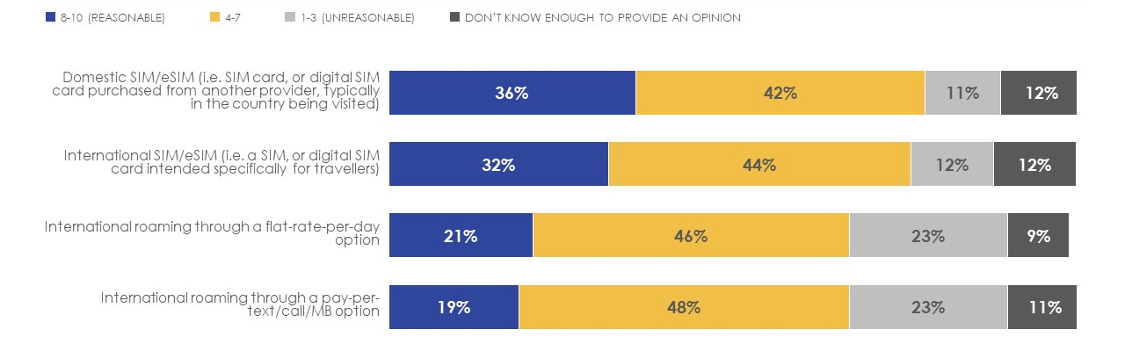

Figure 23: Reasonableness of rates and/ or cost of purchase

Base: Those who used for each product/ service while travelling outside of Canada (n=varies)

Q17. Based on your own experience, how reasonable do you feel the rates and/or cost of purchase are for each of the following products or services?

This horizontal bar chart shows responses to a question about the reasonableness of rates and/ or cost of purchase an international roaming products or services. Respondents were asked to provide ratings on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as reasonable, 4 to 7 as neither reasonable nor unreasonable and 1 to 3 as unreasonable. Sample sizes vary.

- Domestic SIM/eSIM (i.e. SIM card or digital SIM card purchased from another provider, typically in the country being visited): 36% reasonable, 42% neither reasonable nor unreasonable, 11% unreasonable, 12% don't know enough to provide an opinion.

- International SIM/eSIM (i.e. SIM card or digital SIM card intended specifically for travelers): 32% reasonable, 44% neither reasonable nor unreasonable, 12% unreasonable, 12% don't know enough to provide an opinion.

- International roaming through a flat-rate-per-day option: 21% reasonable, 46% neither reasonable nor unreasonable, 23% unreasonable, 9% don't know enough to provide an opinion.

- International roaming through a pay-per-text/call/MB option: 19% reasonable, 48% neither reasonable nor unreasonable, 23% unreasonable, 11% don't know enough to provide an opinion.

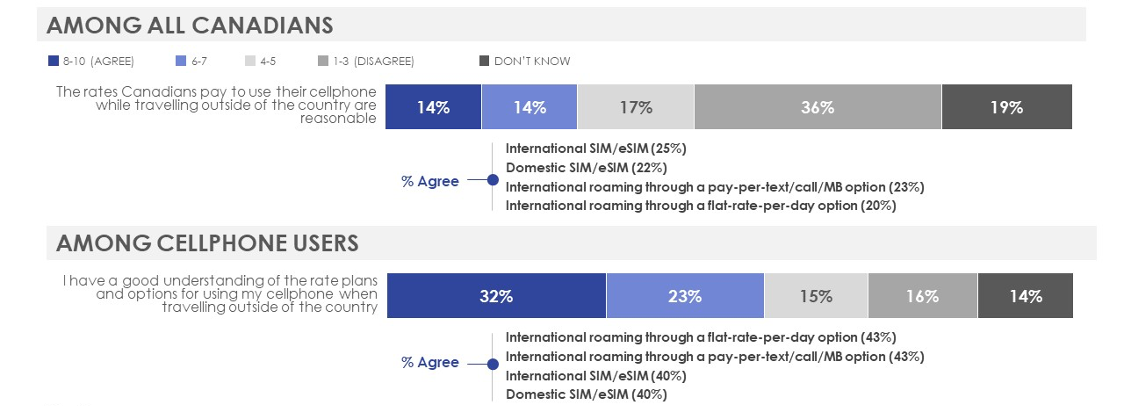

Around one in ten (14%) Canadians agreed that the rates they pay to use their cellphone while travelling outside of the country are reasonable and one third (32%) of those with a cellphone for personal use agree that they have a good understanding of the rate plans/ options for using their cellphone outside of the country. Those who reported having used an international calling or text product or service before are more likely to agree to either statements.

- Older Canadians are more likely than younger Canadians to disagree that the rates and /or cost of purchase are reasonable and that they have a good understanding of the rate plans/ options for using their cellphone outside of the country.

Figure 24: Attitudes towards international calling or text products and services

Base: varies by statement

Q20. Please indicate the extent to which you agree or disagree with each of the following statements.

This horizontal bar charts show responses to a question about the attitudes towards international calling or text products and services. Respondents were asked to state their level of agreement with two statements regarding international roaming on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as agree, 6 and 7 as somewhat agree, 4 and 5 as somewhat disagree and 1 to 3 as disagree. Sample sizes vary per statement.

- The rates Canadians pay to use their cellphone while travelling outside of the county are reasonable: 14% agree, 14% somewhat agree, 17% somewhat disagree, 36% disagree and 19% don't know.

- I have a good understanding of the rate plans and options for using my cellphone when travelling outside of the country: 32% agree, 23% somewhat agree, 15% somewhat disagree, 16% disagree and 14% don't know.

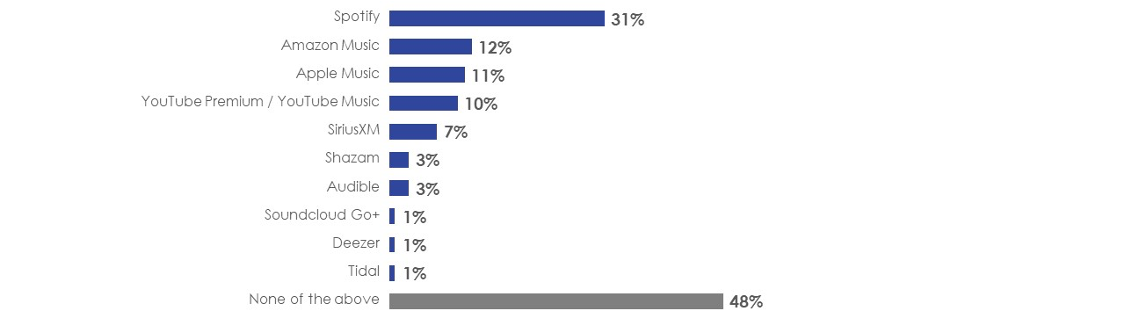

Primary source(s) and satisfaction with programming

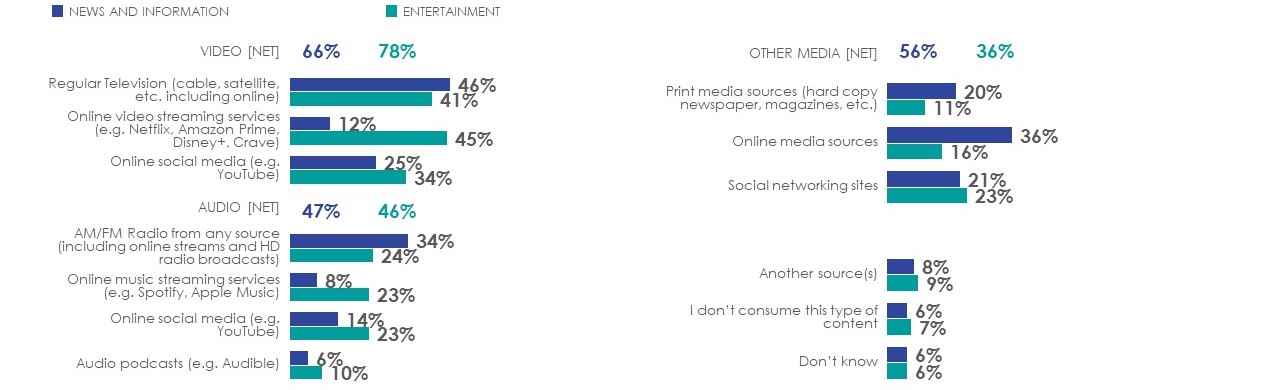

Canadians' primary sources of media content for both 'entertainment' and 'news and information' are video (78% and 66% respectively). Roughly half report their primary sources for either type of content are audio (47% and 46%) and nearly six in ten (56%) use other media sources for 'news and information' compared to roughly four in ten (36%) for 'entertainment' content.

The most common sources of media content for 'news and information' are regular television (46%), followed by online media (36%), AM/FM radio (34%) and online social media (25%). For 'entertainment', the primary sources are online video streaming (45%) and regular television (43%), followed by online social media (34%).

- Older Canadians (in particular those 55 or older) are more likely than younger Canadians to report that their primary sources of 'news and information' content are regular television, AM/FM radio or print media sources and that their primary source of 'entertainment' content is regular television.

- Younger Canadians are more likely than older Canadians to report that their primary sources of 'news and information' or 'entertainment' content are online social media, online video streaming services, audio podcasts, and social networking sites, as well as online music streaming services for 'entertainment' content.

- Residents of Quebec are more likely than those from other regions to report that their primary sources of 'news and information' content are regular television, while residents of BC are more likely to use online or print media sources.

- French-speakers are more likely than English-speakers to report that their primary source of 'news and information' or 'entertainment' content is regular television, while English-speakers are more likely to rely on online video streaming services, online music streaming services, audio podcasts and social networking sites for both types of content.

- Those who identify as Indigenous and racialized Canadians are more likely than those who are not to report that their primary sources of 'news and information' content are online video streaming services and online social media. Racialized Canadians are also more likely than those who are not racialized to report that their primary source of 'entertainment' content are online video streaming services, online social media and online music streaming services.

- Higher income households are more likely than lower income households to report that their primary source of 'entertainment' content are online video streaming services.

Figure 25: Primary source(s) for 'news and information' and 'entertainment' content

Base: All respondents (n=2561)

Q18. What are your primary source(s) of media content for 'news and information' and 'entertainment'? Please select the most common source(s) you use for each.

This horizontal bar chart shows the primary source(s) for 'news and information' and 'entertainment' content. Respondents were asked to indicate which types of media content are their primary sources for each of 'news and information' and 'entertainment'. A total of 2561 respondents answered as follows:

- Regular television (cable, satellite, etc. including online): 46% news and information and 41% entertainment.

- Online video streaming (e.g. Netflix, Amazon Prime, Disney+, Crave): 12% news and information and 45% entertainment.

- Online social media (e.g. YouTube): 25% news and information and 34% entertainment.

- AM/FM Radio from any source (including online streams and HD radio broadcasts): 34% news and information and 24% entertainment.

- Online music streaming services (e.g. Spotify, Apple Music): 8% news and information and 23% entertainment.

- Online social media (e.g. YouTube): 14% news and information and 23% entertainment.

- Audio podcasts (e.g. Audible): 6% news and information and 10% entertainment.

- Print media sources (hard copy newspaper, magazines, etc.): 20% news and information and 11% entertainment.

- Online media sources: 36% news and information and 16% entertainment.

- Social networking sites: 21% news and information and 23% entertainment.

- Another source(s): 8% news and information and 9% entertainment.

- I don't consume this type of content: 6% news and information and 7% entertainment.

- Don't know: 6% news and information and 6% entertainment.

Satisfaction with programming by type of content

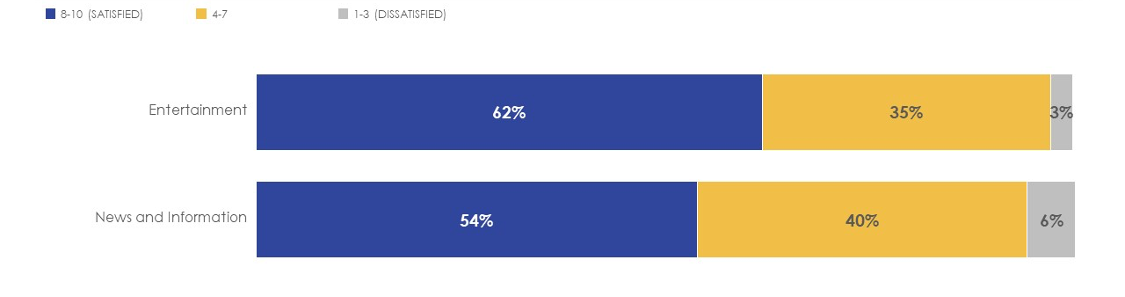

Among those who report they consume each type of programming, six in ten (62%) are satisfied with the 'entertainment' content they receive, while slightly more than half (54%) are satisfied with the 'news and information' content. Between one-third to four in ten express softer levels of satisfaction with either, while few are dissatisfied.

- Canadians 65 or older are more likely than younger Canadians to be satisfied with the 'news and information' content they receive (64%).

- Residents of Quebec are more likely than those from other regions to be satisfied with both the 'entertainment' (69%) and 'news and information' content they receive (64%).

- French-speakers are more likely than English-speakers to be satisfied with both the 'entertainment' (69% vs. 60%) and 'news and information' content they receive (66% vs. 50%).

Figure 26: Satisfaction with quality of content for 'news and information' and 'entertainment'

Base: Those who consume 'entertainment' (n=2239) and/or 'news and information' (n=2274) content

Q19. Overall, how satisfied are you with the quality of content you receive for…?

This horizontal bar chart shows responses to a question about satisfaction with the quality of content received for 'entertainment' and 'news and information'. Respondents were asked to provide ratings on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as satisfied, 4 to 7 as neither satisfied nor dissatisfied and 1 to 3 as dissatisfied. Sample size vary by type of content.

- Entertainment: 62% satisfied, 35% neither satisfied nor dissatisfied, 3% dissatisfied. A total of 2239 respondents answered this question.

- News and information: 54% satisfied, 40% neither satisfied nor dissatisfied, 6% dissatisfied. A total of 2274 respondents answered this question.

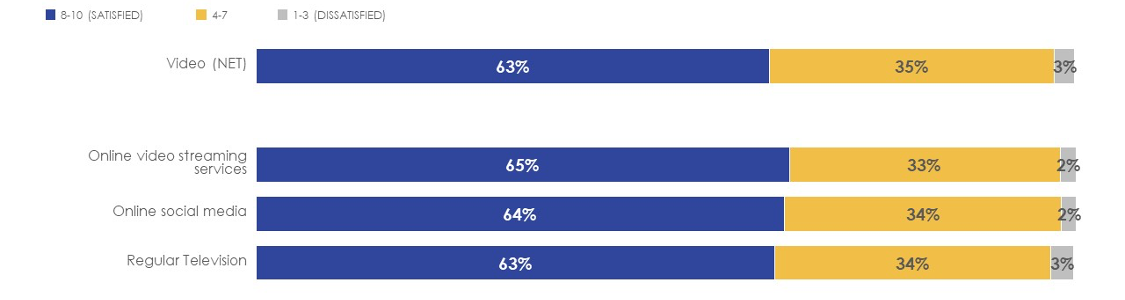

More than six in ten (63%) are satisfied with the quality of 'entertainment' content they receive from video sources, followed by six in ten (60%) for content from audio sources and other types of media sources (61%).

Satisfaction is consistent by the type of video content they receive and more than six in ten are satisfied with the content from online video streaming services (65%), online social media (64%) and regular television (63%).

Figure 27: Satisfaction with quality of content for 'entertainment' by video source(s)

Base: Those who consume 'entertainment' (n=2239) content, base varies by source

Q19. Overall, how satisfied are you with the quality of content you receive for…?

This horizontal bar chart shows responses to a question about satisfaction with quality of content for 'entertainment' by video source(s). Respondents were asked to provide ratings on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as satisfied, 4 to 7 as neither satisfied nor dissatisfied and 1 to 3 as dissatisfied. A total of 2239 respondents answered this question as follows:

- Video (NET): 63% satisfied, 35% neither satisfied nor dissatisfied, 3% dissatisfied.

- Online video streaming services: 65% satisfied, 33% neither satisfied nor dissatisfied, 2% dissatisfied.

- Online social media: 64% satisfied, 34% neither satisfied nor dissatisfied, 2% dissatisfied.

- Regular television: 63% satisfied, 34% neither satisfied nor dissatisfied, 3% dissatisfied.

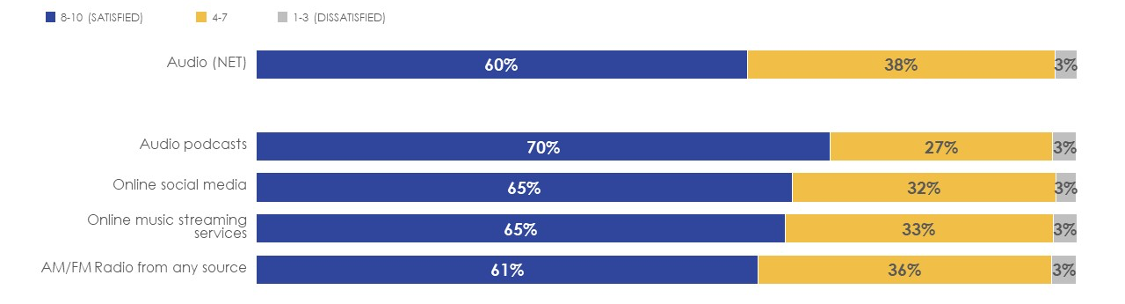

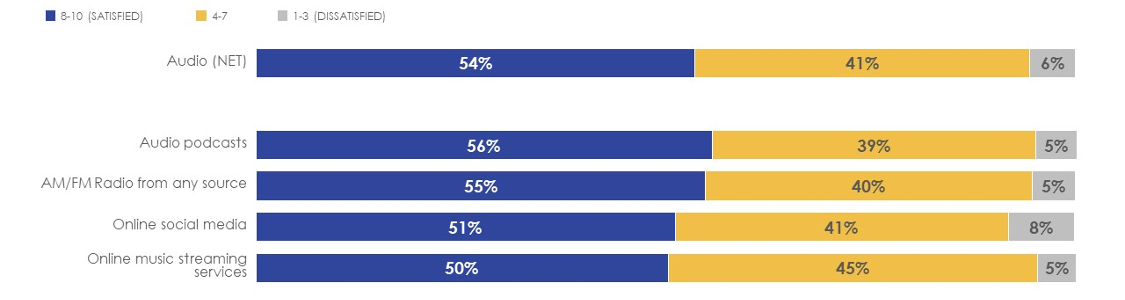

Seven in ten are satisfied with the content from audio podcasts (70%), followed by two-thirds for online social media and online music streaming (65% each), and six in ten for AM/FM radio (61%).

Figure 28: Satisfaction with quality of content for 'entertainment' by audio source(s)

Base: Those who consume 'entertainment' (n=2239) content, base varies by source

Q19. Overall, how satisfied are you with the quality of content you receive for…?

This horizontal bar chart shows responses to a question about satisfaction with quality of content for 'entertainment' by audio source(s). Respondents were asked to provide ratings on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as satisfied, 4 to 7 as neither satisfied nor dissatisfied and 1 to 3 as dissatisfied. A total of 2239 respondents answered this question as follows:

- Audio (NET): 60% satisfied, 38% neither satisfied nor dissatisfied, 3% dissatisfied.

- Audio podcasts: 70% satisfied, 27% neither satisfied nor dissatisfied, 3% dissatisfied.

- Online social media: 65% satisfied, 32% neither satisfied nor dissatisfied, 3% dissatisfied.

- Online music streaming services: 65% satisfied, 33% neither satisfied nor dissatisfied, 3% dissatisfied.

- AM/FM radio from any source: 61% satisfied, 36% neither satisfied nor dissatisfied, 3% dissatisfied.

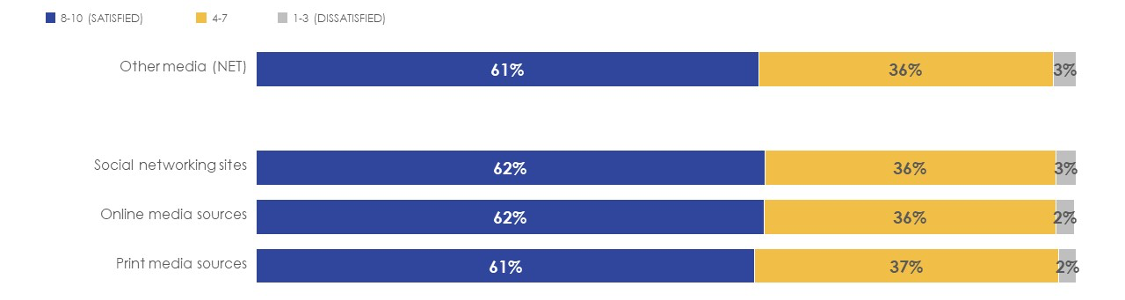

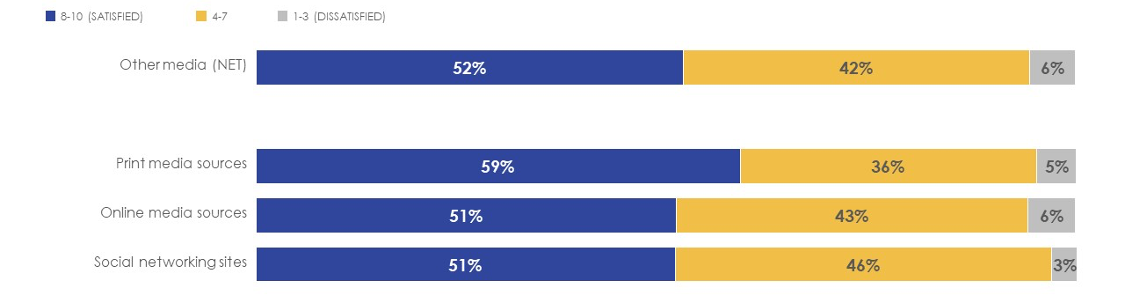

Satisfaction is consistent by the type of other media content and just over six in ten are satisfied with the content from social networking sites and online media (62% each) and print media (61%).

Figure 29: Satisfaction with quality of content for 'entertainment' by other media source(s)

Base: Those who consume 'entertainment' (n=2239) content, base varies by source

Q19. Overall, how satisfied are you with the quality of content you receive for…?

This horizontal bar chart shows responses to a question about satisfaction with quality of content for 'entertainment' by other media source(s). Respondents were asked to provide ratings on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as satisfied, 4 to 7 as neither satisfied nor dissatisfied and 1 to 3 as dissatisfied. A total of 2239 respondents answered this question as follows:

- Other media (NET): 61% satisfied, 36% neither satisfied nor dissatisfied, 3% dissatisfied.

- Social networking sites: 62% satisfied, 36% neither satisfied nor dissatisfied, 3% dissatisfied.

- Online media sources: 62% satisfied, 36% neither satisfied nor dissatisfied, 2% dissatisfied.

- Print media sources: 61% satisfied, 37% neither satisfied nor dissatisfied, 2% dissatisfied.

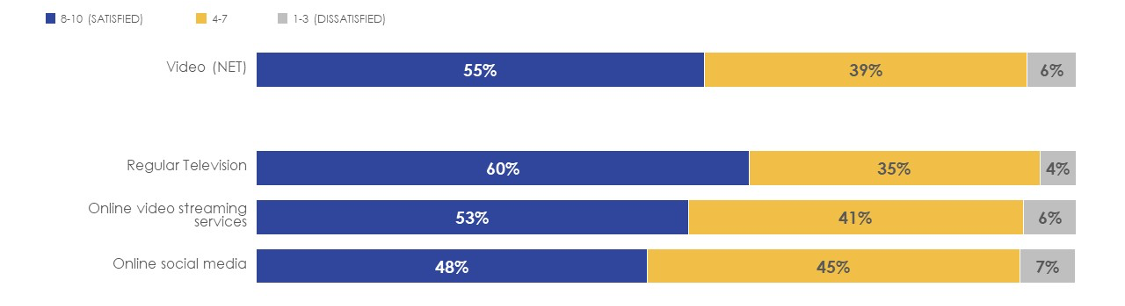

Just over half (55%) are satisfied with the quality of 'news and information' content they receive from video sources, audio sources (54%) or other types of media sources (52%).

Six in ten are satisfied with the video content from regular television (60%), followed by just over half for online video streaming (53%) and roughly half for online social media (48%).

Figure 30: Satisfaction with quality of content for 'news and information' by video source(s)

Base: Those who consume 'news and information' (n=2274) content

Q19. Overall, how satisfied are you with the quality of content you receive for…?

This horizontal bar chart shows responses to a question about satisfaction with quality of content for 'news and information' by video source(s). Respondents were asked to provide ratings on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as satisfied, 4 to 7 as neither satisfied nor dissatisfied and 1 to 3 as dissatisfied. A total of 2274 respondents answered this question as follows:

- Video (NET): 55% satisfied, 39% neither satisfied nor dissatisfied, 6% dissatisfied.

- Regular television: 60% satisfied, 35% neither satisfied nor dissatisfied, 4% dissatisfied.

- Online video streaming services: 53% satisfied, 41% neither satisfied nor dissatisfied, 6% dissatisfied.

- Online social media: 48% satisfied, 45% neither satisfied nor dissatisfied, 7% dissatisfied.

Nearly six in ten are satisfied with the content from audio podcasts (56%) and AM/FM radio (55%), followed by closer to half for online social media (51%) and online music streaming services (50%).

Figure 31: Satisfaction with quality of content for 'news and information' by audio source(s)

Base: Those who consume 'news and information' (n=2274) content, base varies by source

Q19. Overall, how satisfied are you with the quality of content you receive for…?

This horizontal bar chart shows responses to a question about satisfaction with quality of content for 'news and information' by audio source(s). Respondents were asked to provide ratings on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as satisfied, 4 to 7 as neither satisfied nor dissatisfied and 1 to 3 as dissatisfied. A total of 2274 users answered this question as follows:

- Audio (NET): 54% satisfied, 41% neither satisfied nor dissatisfied, 6% dissatisfied.

- Audio podcasts: 56% satisfied, 39% neither satisfied nor dissatisfied, 5% dissatisfied.

- AM/FM radio from any source: 55% satisfied, 40% neither satisfied nor dissatisfied, 5% dissatisfied.

- Online social media: 51% satisfied, 41% neither satisfied nor dissatisfied, 8% dissatisfied.

- Online music streaming services: 50% satisfied, 45% neither satisfied nor dissatisfied, 5% dissatisfied.

Six in ten are satisfied with the content from print media (59%), followed by roughly half for online media sources and social network sites (51% each).

Figure 32: Satisfaction with quality of content for 'news and information' by other media source(s)

Base: Those who consume 'news and information' (n=2274) content, base varies by source

Q19. Overall, how satisfied are you with the quality of content you receive for…?

This horizontal bar chart shows responses to a question about satisfaction with quality of content for 'news and information' by other media source(s). Respondents were asked to provide ratings on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as satisfied, 4 to 7 as neither satisfied nor dissatisfied and 1 to 3 as dissatisfied. A total of 2274 respondents answered this question as follows:

- Other media (NET): 52% satisfied, 42% neither satisfied nor dissatisfied, 6% dissatisfied.

- Print media sources: 59% satisfied, 36% neither satisfied nor dissatisfied, 5% dissatisfied.

- Online media sources: 51% satisfied, 43% neither satisfied nor dissatisfied, 6% dissatisfied.

- Social networking sites: 51% satisfied, 46% neither satisfied nor dissatisfied, 3% dissatisfied.

Broader Attitudes

Attitudes towards broadcasting

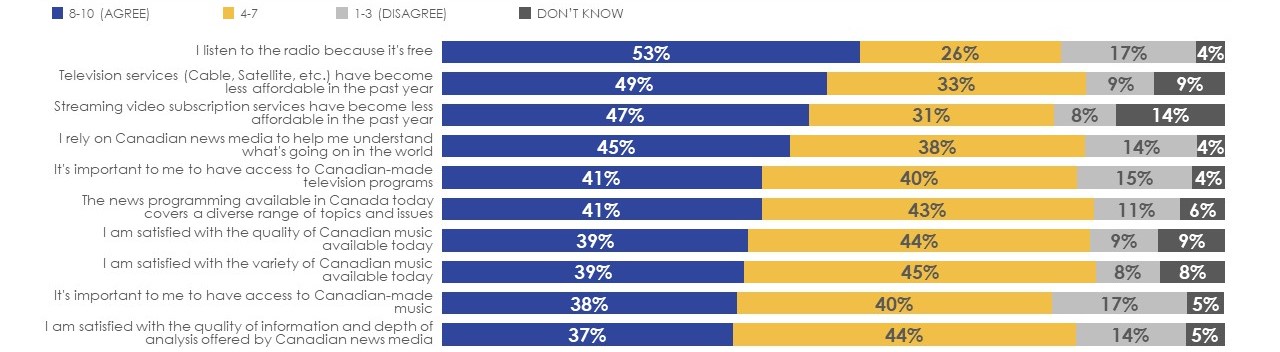

At just over half (53%), the majority of Canadians agree that they listen to radio because it is free.

Around four in ten agree that they rely on Canadian news media to help them understand what's going on in the world (45%), and that it's important for them to have access to Canadian-made television programs (41%) and music (38%). Nearly four in ten agree that they trust the information provided by news media in Canada (36%), that the types of news programming offers a variety of perspectives (36%) and that the types of news, music, and television programming is relevant to their life (36%).

Roughly four in ten are satisfied with the quality and variety of Canadian music available today (39% each), the quality of information and analysis offered by Canadian news media (37%) and that news programming covers a diverse range of topics and issues (41%). One-third agree they are satisfied with the quality (35%) and variety (34%) of Canadian television programs, and that they see themselves reflected in the programming available (32%).

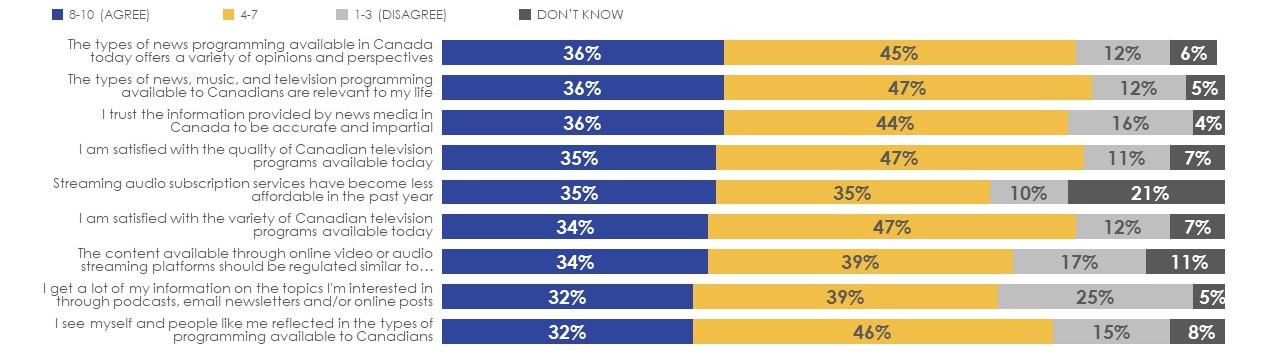

Roughly half of Canadians agree that television (49%) and streaming video services (47%) have become less affordable in the past year. One-third agree that the content of streaming platforms should be regulated like traditional broadcasting (34%).

- Canadians 65 and older are more likely than those under 65 to agree that the types of news programming available in Canada offer a variety of opinions and perspectives, that they trust the information provided by news media in Canada to be accurate and impartial, that they rely on Canadian news media to understand what's going on, that it is important to have access to Canadian-made TV programs and music, that programming covers diverse topics and issues, that they are satisfied with the quality and depth of analysis of Canadian news media, and that the content of streaming platforms should be regulated like traditional broadcasting.

- Canadians 45 and older are more likely than those under 45 to agree that TV services have become less affordable in the past year, while those 34-45 are more likely to agree that streaming video services have become less affordable.

- Canadians 45-54 years old are more likely to listen to the radio because it's free than other age groups.

- Residents of Quebec are more likely than those from other regions to agree that they rely on Canadian news media to understand what's going on, that the types of news programming available in Canada offers a variety of opinions and perspectives, that it's important to have access to Canadian-made TV programs and music, that they are satisfied with the quality and variety of Canadian televisions programs and music available today, and the quality and depth of analysis of Canadian news media, and that they see themselves reflected in the programming available.

- French-speakers are more likely than English-speakers to agree that they rely on Canadian news media to understand what's going on, that the types of news programming available in Canada offers a variety of opinions and perspectives, and that they trust the information provided by news media in Canada to be accurate and impartial. They are also more likely to agree that it's important to have access to Canadian-made TV programs and music, that they are satisfied with the quality and variety of Canadian televisions programs and music available today, and the quality and depth of analysis of Canadian news media, that they see themselves reflected in the programming available, and that content available through online video or streaming platforms should be regulated similar to traditional broadcasting.

- Persons with a disability are more likely than those who do not have a disability to agree that television services have become less affordable in the past year, that they rely on Canadian news media to understand what's going on, and that the types of news programming available in Canada offers a variety of opinions and perspectives.

Figure 33: Attitudes towards broadcasting (1/2)

Base: All respondents (n=2561)

Q20. Please indicate the extent to which you agree or disagree with each of the following statements.

This horizontal bar chart shows responses to a question about attitudes towards broadcasting. Respondents were asked to provide their level of agreement with a series of statements regarding broadcasting on a 10-pt scale and results were grouped by those who provided a rating of 8 to 10 as agree, 4 to 7 as neither agree nor disagree and 1 to 3 as disagree. A total of 2561 consumers answered as follows:

- I listen to the radio because it's free: 53% agree, 26% neither agree nor disagree, 17% disagree and 4% don't know.

- Television services (Cable, Satellite, etc.) have become less affordable in the past year: 49% agree, 33% neither agree nor disagree, 9% disagree and 9% don't know.

- Streaming video subscription services have become less affordable in the past year: 47% agree, 31% neither agree nor disagree, 8% disagree and 14% don't know.

- I rely on Canadian news media to help me understand what's going on in the world: 45% agree, 38% neither agree nor disagree, 14% disagree and 4% don't know.

- It's important to me to have access to Canadian-made television programs: 41% agree, 40% neither agree nor disagree, 15% disagree and 4% don't know.

- The news programming available in Canada today covers a diverse range of topics and issues: 41% agree, 43% neither agree nor disagree, 11% disagree and 6% don't know.

- I am satisfied with the quality of Canadian music available today: 39% agree, 44% neither agree nor disagree, 9% disagree and 9% don't know.

- I am satisfied with the variety of Canadian music available today: 39% agree, 45% neither agree nor disagree, 8% disagree and 8% don't know.