Final Report

Prepared for the Financial Consumer Agency of Canada

Supplier Name: Phoenix SPI

Contract Number: 5R000-182334-001-CY

Contract Value: $202,640.58 (including HST)

Award Date: 2019-01-25

Delivery Date: 2019-07-12

Registration Number: POR 114-18

For more information on this report, please contact the Financial Consumer Agency of Canada at: info@fcac-acfc.gc.ca

Ce rapport est aussi disponible en français.

This public opinion research report presents the results of a telephone survey of 3,007 Canadians that was conducted between February 8 and March 10, 2019. Surveys averaged 15 minutes to complete.

This publication may be reproduced for non-commercial purposes only. Prior written permission must be obtained from FCAC. For more information on this report, please contact FCAC at:

Financial Consumer Agency of Canada

427 Laurier Ave. West,

Ottawa ON

K1R 1B9

Catalogue Number:

FC5-62/2019E-PDF

International Standard Book Number (ISBN):

978-0-660-31828-8

Related publications (registration number: POR 114-18):

Catalogue Number FC5-62/2019F-PDF (Final Report, French)

ISBN 978-0-660-31829-5

© Her Majesty the Queen in Right of Canada, as represented by the Minister of Finance Canada, 2019.

Figure 1: Banking Responsibility

Figure 2: Banking Proxies

Figure 3: Trusted Contact

Figure 4: Most Common Method of Banking

Figure 5: Most Common Method of Banking [all age segments]

Figure 6: Frequency of Banking

Figure 7: Banking Products [seniors]

Figure 8: Issues Using Banking Products

Figure 9: Banking Products with Issues [seniors]

Figure 10: Preferred Method of Receiving Banking Information

Figure 11: Preferred Method of Receiving Banking Information [all age segments]

Figure 12: Clarity of Information Received from Bank.

Figure 13: Frequency of Receiving Difficult to Understand Information [seniors]

Figure 14: Perceptions of Bank Employees

Figure 15: Perceptions of Bank Employees [all age segments]

Figure 16: Perceptions of Bank Employees' Skills & Knowledge

Figure 17: Perceptions of Bank Employees' Skills & Knowledge [all age segments]

Figure 18: Financial Abuse, Fraud, or Scams [all age segments]

Figure 19: Frequency of Online Banking

Figure 20: Issues with Online Banking

Figure 21: Health Issues

Figure 22: Bank Closures

The Financial Consumer Agency of Canada (FCAC) is a federal government agency that protects and educates consumers about financial products and services. In the fall of 2018, the Minister of Finance tasked FCAC with creating a code of conduct to guide banks in their delivery of services to Canada’s seniors.

FCAC commissioned Phoenix Strategic Perspectives (Phoenix SPI) to conduct a 15-minute telephone survey of Canadians aged 18 and older. A total of 3,007 interviews were completed via dual-frame (landline and cell phone) random digit dialling: 2,254 interviews were completed with Canadians aged 55 and older,[1] and 753 interviews were completed with Canadians under 55 years of age. The fieldwork was conducted from February 8 to March 10, 2019. The sample of 2,254 Canadians aged 55 and older can be considered accurate to within ±2.1% at the 95% confidence level. The sample of 753 Canadians under the age of 55 can be considered accurate to within ±3.6% at the 95% confidence level. The margin of error for the overall sample of 3,007 Canadians aged 18 and older is ±1.8% at the 95% confidence level.

The purpose of this research was to assess the banking experiences of seniors as well as to identify challenges and potential solutions.

The following are key findings from the survey:

Communication and Disclosure

Relationship with Banks

Fraud and Financial Abuse

Technology and Accessibility

The contract value was $202,640.58 (including HST).

I hereby certify as a Senior Officer of Phoenix Strategic Perspectives that the deliverables fully comply with the Government of Canada political neutrality requirements outlined in the Policy on Communications and Federal Identity of the Government of Canada and Procedures for Planning and Contracting Public Opinion Research. Specifically, the deliverables do not contain any reference to electoral voting intentions, political party preferences, standings with the electorate, or ratings of the performance of a political party or its leader.

![]()

Alethea Woods

President

Phoenix SPI

The Financial Consumer Agency of Canada (FCAC) commissioned Phoenix Strategic Perspectives Inc. (Phoenix SPI) to conduct public opinion research (POR) on the use of banking products and services by Canadians.

FCAC is a federal government agency that protects and educates consumers about financial products and services. In November 2018, it was announced that FCAC was going to engage with banks and seniors’ groups to create a code of conduct to guide banks on how they can best deliver their services to meet the needs of Canada’s seniors.

FCAC commissioned POR and inform the development the code of conduct. While much research has been done on the issues older Canadians face with financial services, important gaps remain. The purpose of this research was to assess the banking experiences of seniors as well as to identify challenges and potential solutions.

A nationally representative telephone survey of Canadians aged 18 or older was used for this research. All respondents were required to hold an account with a bank at the time of the interview. A total of 3,007 interviews were completed via dual-frame (landline and cell phone) random digit dialling—specifically, 2,254 interviews were completed with Canadians aged 55 and older, and 753 interviews were completed with Canadians under 55 years of age. The fieldwork was conducted February 8 to March 10, 2019.

The sample of Canadians aged 55 and older included an oversample of Canadians aged 75 and older.[2] Canadians under 55 were sampled in proportion to the population. The sample of 2,254 Canadians aged 55 and older can be considered accurate to within ±2.1% at the 95% confidence level. The sample of 753 Canadians under the age of 55 can be considered accurate to within ±3.6% at the 95% confidence level. The overall sample of 3,007 Canadians aged 18 and older can be considered accurate to within ±1.8% at the 95% confidence level.

Survey data have been weighted by region, age and gender to ensure results that are representative of the Canadian population. Population figures from Statistics Canada (2016 Census) were used to construct the weights for the survey. The results of this research can be considered representative of the populations of Canadians aged 55 and older, Canadians under the age of 55, and the general population of Canadians aged 18 and older.

More information on the methodology can be found in the Appendix of this report: Technical Specifications of Research.

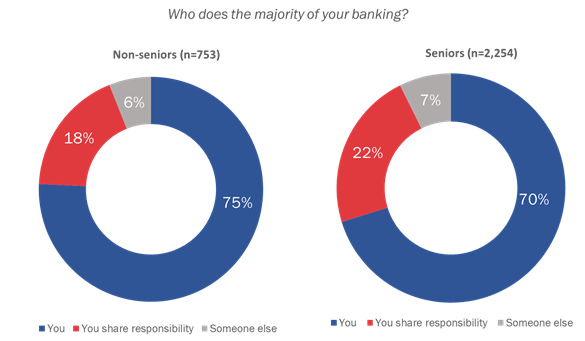

The majority of respondents are responsible for their own banking

Most seniors in Canada (70%) are responsible for conducting the majority of their banking. Seniors were less likely than non-seniors (75%) to be solely responsible for their banking and were more likely to share this responsibility equally with someone else, such as a family member or friend (22% versus 18%, respectively). Relatively few seniors (7%) have delegated all of their banking responsibility (Figure 1).

Figure 1: Banking Responsibility

Intro1. To start, who does the majority of your banking?

Base: all respondents [Refusal=<1%]

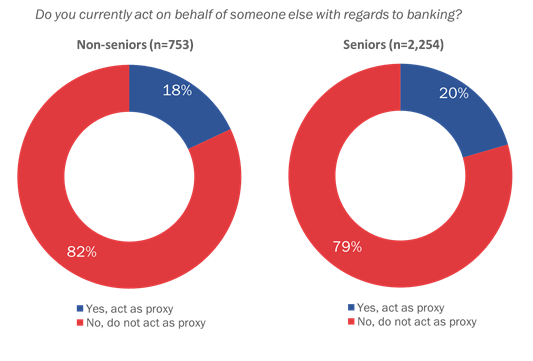

One in five Canadian seniors acts as a proxy with regards to banking

One in five Canadian seniors acts on behalf of someone else with regards to banking (Figure 2). Seniors were no more likely than non-seniors to indicate they act on behalf of someone else. However, Canadians aged 45 to 54 were more likely than most other age groups to indicate they act on behalf of someone else (28% compared to a low of 11% of 18 to 24 year olds and high of 20% of 65 to 74 year olds).

Figure 2: Banking Proxies

Intro2. Do you currently act on behalf of someone else with regards to banking?

Base: all respondents [DK/Refusal=<1%]

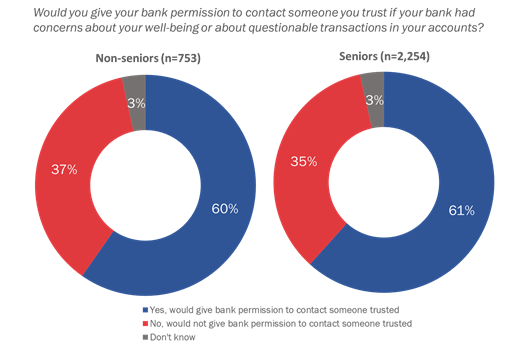

Six in 10 Canadian seniors would give their bank permission to contact someone they trust if their bank had concerns about their well-being

If presented with the opportunity, six in 10 seniors (61%) would give their bank permission to contact someone they trust if the bank had concerns about their well-being or about questionable transactions in their accounts. Just over one-third (35%) would not give their bank permission to contact someone they trust, and 3% were unsure. Non-seniors were just as likely as seniors to indicate they would give their bank permission to contact someone they trust (Figure 3).

Figure 3: Trusted Contact

GE1. If given the opportunity, would you give your bank permission to contact someone you trust if your bank had concerns about your well-being or about questionable transactions in your accounts?

Base: all respondents [Refusal=<1%]

Most seniors generally feel positively about dealing with their bank

The vast majority of seniors (91%) generally feel positively about dealing with their bank.[3] In contrast, fewer non-seniors (83%) expressed positive feelings about dealing with their bank.

Among seniors, positive feelings were most often based on good customer service (18%) or aspects of customer service, such as having a good experience with the bank and being a long-term client (14%), receiving personal and attentive service (10%), receiving friendly and courteous service (9%), being treated with respect (7%), and receiving service from helpful (7%) and knowledgeable (3%) bank employees.

Other reasons for satisfaction or positive feelings included simply having no issues or problems with the bank (21%), having one’s needs met (8%), receiving fast service in branch (7%), and having trust and confidence in the bank and its employees (7%).

Feelings of discontent were relatively limited and expressed through references to poor customer service (7%), dissatisfaction with fees (3%), and financial products that do not meet one’s needs (1%).

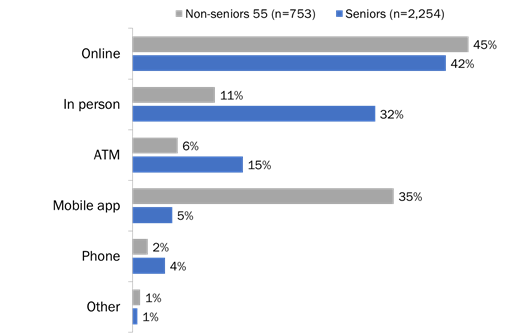

Seniors are more likely to bank in person

Over the past 12 months, the majority of seniors most commonly did their banking online or using their bank’s website (42%), or in person at a branch (32%). Fewer seniors most commonly banked using an ATM (15%), via a mobile app (5%), or by phone (4%).

Compared to non-seniors, seniors were more likely to have banked most commonly over the past 12 months in person (11% and 32%, respectively) or using an ATM (6% and 15%, respectively) and were far less likely to have most commonly banked via a mobile app (5% and 35%, respectively; Figure 4).

Figure 4: Most Common Method of Banking

Q1. Over the past 12 months, what is the most common way you did your banking?

Base: all respondents; [DK/Refusal=<1%]

Over the past 12 months, Canadians aged 75 and older were more likely than any other age group to have most commonly banked in person at a branch (54%) and were less likely to have most commonly banked online (23%; Figure 5).

Figure 5: Most Common Method of Banking [all age segments]

![Figure 5: Most Common Method of Banking [all age segments]](images/fig_05-eng.png)

Q1. Over the past 12 months, what is the most common way you did your banking?

Base: all respondents; [DK/Refusal=<1%]

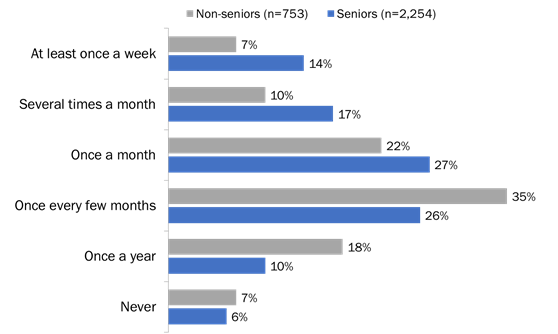

Seniors bank by speaking with an employee at a branch more frequently than do non-seniors

Over the past 12 months, 58% of seniors have conducted their banking by speaking with an employee at a branch at least once a month (i.e., at least once a week, several times a month or once a month) as compared to 39% of non-seniors (Figure 6).

Canadians 75 and older were the most likely to bank in person relatively frequently: at least once a week (16%) or several times a month (22%).

Figure 6: Frequency of Banking

Q2. Over the past 12 months, how often did you do your banking in person?

Base: all respondents; [DK/Refusal=<1%]

Seniors use a variety of banking products and services

Almost all seniors have a chequing or savings account (97%) and the majority (87%) have a credit card. Nearly-two thirds (64%) have a registered account, such as a Registered Retirement Savings Plan (RRSP), Registered Retirement Income Fund (RRIF), or a Tax-Free Savings Account (TFSA), and 54% have a personal line of credit or other loan. Fewer seniors have other savings (such as a GIC (29%), a mortgage (26%), or a home equity line of credit (24%). Very few (2% or less) identified having other banking products, such as a reverse mortgage (2%; Figure 7).

In comparing the banking products used by seniors and non-seniors, seniors are more likely to have a personal line of credit or other type of loan (54% and 49%, respectively), a home equity line of credit (24% and 17%, respectively), an RRSP, RRIF, or TFSA (64% and 56%, respectively) and other savings, such as a GIC (29% and 16%, respectively).

Figure 7: Banking Products [seniors]

![Figure 7: Banking Products [seniors]](images/fig_07-eng.png)

Q3. Which of the following banking products and services do you have? [multiple responses accepted]

Base: n=2,254; those 55 plus [DK/Refusal=1%] [Multiple responses accepted]

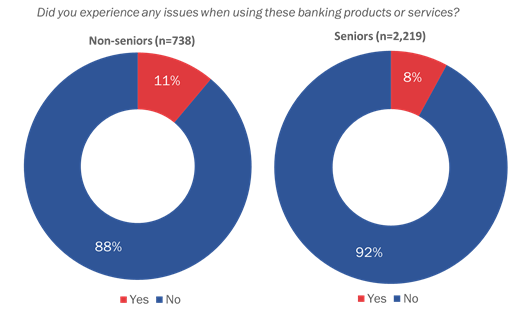

Few seniors and non-seniors report experiencing issues with banking products and services

Over the past 12 months, nearly one in 10 (8%) Canadians aged 55 and older have experienced an issue when using a banking product or service (Figure 8). [4] In general, non-seniors were more likely than seniors to have had experienced such an issue (11% versus 8%, respectively). However, seniors and non-seniors did not differ in the products and services with which they experienced issues.

Figure 8: Issues Using Banking Products

CD_4. Over the past 12 months, did you experience any issues when using these banking products or services?

Base: all respondents who use banking products [DK=<1%]

Seniors who have experienced issues when using their banking products and services most commonly experienced an issue with a chequing or savings account (44%), or credit card (21%). A smaller proportion of seniors have experienced issues with a registered account (8%), a personal line of credit or other loan (6%), other savings (5%), a mortgage (3%), or a home equity line of credit (1%; Figure 9). Among these seniors, the most frequently cited issues were a mistake on the bank’s part (24%), an issue related to security or fraud (20%), being overcharged fees (13%), or not receiving the expected interest rate (9%).

Fewer than 5% of seniors identified other issues. Other issues identified most often related to information, such as taking too long to get information or service, receiving unclear or incorrect information, receiving conflicting information or advice, not receiving requested information, services, or forms, and not knowing where to obtain information. A small proportion also identified problems with online banking and taking too long to process an application or receive a decision.

Just over one in 10 seniors who experienced an issue with a banking product or service could not recall with which product or service they experienced an issue.

Figure 9: Banking Products with Issues [seniors]

![Figure 9: Banking Products with Issues [seniors]](images/fig_09-eng.png)

Q4a. With what product or service did you experience an issue?

Base: n=170; those 55 plus who experienced issues with banking products

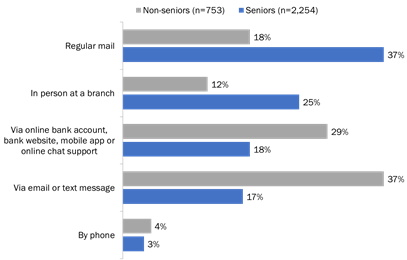

Seniors prefer more traditional methods of receiving information about their banking products or services

The majority of Canadian seniors prefer to receive information about their banking products and services through more traditional methods, such as by mail (37%) or in person at a branch (25%). A little over one-third prefer to receive this information electronically, for example, via online or through a mobile app (18%), or via email or text message (17%). A small proportion prefer to receive this information by phone (3%; Figure 10).

Figure 10: Preferred Method of Receiving Banking Information

Q5. How do you prefer to receive information about your banking products and services?

Base: all respondents [DK/Refusal=1%]

In general, older Canadians prefer traditional methods of communication, while younger Canadians prefer electronic communication (Figure 11). Correspondingly, Canadians aged 75 and older were more likely than any other age group to prefer to receive information about their banking products and services in person at a branch (35%). When looking at the different age groups of seniors, these seniors were also more likely than Canadians under the age of 65 to prefer mail (40%) and less likely to prefer to receive information electronically via online or through a mobile app (10%), or through email or text message (8%).

Figure 11: Preferred Method of Receiving Banking Information [all age segments]

![Figure 11: Preferred Method of Receiving Banking Information [all age segments]](images/fig_11-eng.png)

CD_5. How do you prefer to receive information about your banking products and services?

Base: all respondents [DK/Refusal=1%]

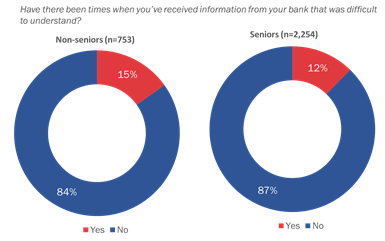

Some Canadians have received information from their bank that was difficult to understand

Over the past 12 months, a little over one in 10 (12%) seniors said there were times when the information they received from their bank was difficult to understand. Seniors were no more likely to report this than were individuals in any other age group (Figure 12).

Figure 12: Clarity of Information Received from Bank.

CD_6. Over the past 12 months, have there been times when you’ve received information from your bank that was difficult to understand?

Base: all respondents [DK=1%]

Among seniors who have received information that was difficult to understand, almost half (45%) specified this occurred rarely, 35% specified this occurred sometimes, 11% specified often and 8% specified nearly always. Canadians aged 65 or older are more likely to report they rarely receive information from their bank that is difficult to understand than are Canadians aged 55 to 64 (34% versus 55% and 53% of Canadians aged 55 to 64, 65 to 74, and 75 years and older, respectively).

Figure 13: Frequency of Receiving Difficult to Understand Information [seniors]

![Figure 13: Frequency of Receiving Difficult to Understand Information [seniors]](images/fig_13-eng.png)

CD_6a. How often would you say this tended to happen?

Base: n=262; those 55 plus who received difficult information [DK/Refusal=1%]

Seniors who had received information from their bank that was difficult to understand (n=262) suggested communications might be enhanced through better explanations of terminology (25%), better in-person or over the phone explanations (18%), more detailed information (13%) and using simpler language (13%). Seniors also suggested the organization of the content might be improved (8%), and relevant information could be explained more clearly and concisely (7%).

Fewer seniors (less than 5%) suggested banks might provide a written copy of information, make pages less cluttered, use larger text/font, use visual aids such as pictures, charts or graphs, and use videos.

Nearly one-quarter (23%) of seniors who received information they found difficult to understand did not provide a suggestion.

In general, seniors and non-seniors report a positive relationship with their bank

Seniors and non-seniors used a five-point Likert scale (1=strongly disagree; 5=strongly agree) to rate their level of agreement or disagreement with the following five statements about their interactions with bank employees[5]:

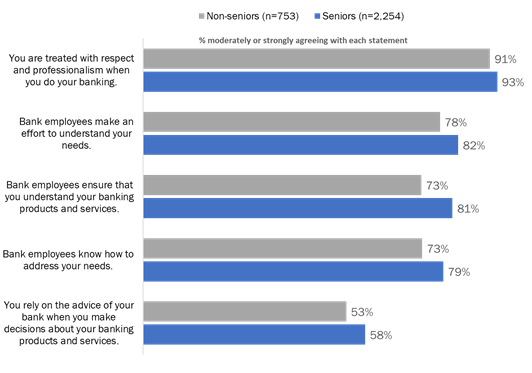

More than nine in 10 seniors and non-seniors agreed they are treated with respect and professionalism when they do their banking (93% and 91%, respectively). In addition, smaller majorities of seniors and non-seniors agreed that bank employees try to understand their needs (82% and 78%, respectively), ensure they understand their banking products and services (81% and 73%, respectively), and know how to address their needs (79% and 73%, respectively). A little over half of seniors and non-seniors rely on the advice of their bank when making decisions about their banking products and services (58% and 53%, respectively).[6] With the one exception—being treated with respect and professionalism—seniors were more likely to offer positive assessments of their bank and bank employees compared to non-seniors (Figure 14).

Figure 14: Perceptions of Bank Employees

TR. Thinking about the interactions you’ve had during the past 12 months, please tell me how much you agree or disagree with the following statements….

Base: all respondents who use banking products [DK/Refusal=1% or less]

In general, seniors who bank in person report the most positive relationships with their banks.

Seniors who most commonly bank in person were more likely than seniors who most commonly bank using other methods to provide positive assessments of bank employees and their bank. Specifically:

In addition, seniors who most commonly banked using a mobile app were less likely to strongly agree that bank employees make an effort to understand their needs (40% versus 52% of those who bank via ATM, 52% who bank online, and 59% who bank via telephone).

Seniors who most commonly banked via an ATM were more likely than those who banked online to agree (generally and strongly) that bank employees ensure they understand their banking products and services (81% versus 76%, respectively), to strongly agree that they rely on the advice of their bank when making decisions about banking products and services (31% versus 25%), and to agree that they are treated with respect and professional when they do their banking (24% versus 17%, respectively).

In general, seniors aged 75 and older were more likely than younger Canadians to provide positive assessments of bank employees and their bank (Figure 15). Specifically:

Figure 15: Perceptions of Bank Employees [all age segments]

![Figure 15: Perceptions of Bank Employees [all age segments]](images/fig_15-eng.png)

TR1-5. Thinking about the interactions you’ve had during the past 12 months, please tell me how much you agree or disagree with the following statements….

Base: all respondents who use banking products [DK/Refusal=1% or less]

Seniors were more likely than non-seniors to agree bank that employees have the knowledge and skills to help identify signs of financial abuse, fraud, or scams

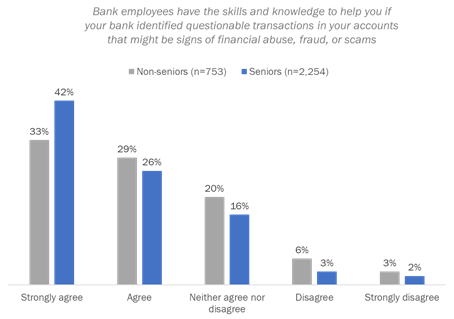

Seniors (68%) were more likely than non-seniors (62%) to agree that bank employees have the knowledge and skills to help them if their bank identified questionable transactions in their accounts that might be signs of financial abuse, fraud, or scams (Figure 16).

Figure 16: Perceptions of Bank Employees' Skills & Knowledge

FR1. Thinking about the interactions you’ve had during the past 12 months, please tell me how much you agree or disagree with he following statements….

Base: all respondents who use banking products [DK/Refusal=4%]

Seniors were more likely than non-seniors to strongly agree that bank employees have the skills and knowledge to help them if their bank identified questionable transactions in their accounts (Figure 17).

Figure 17: Perceptions of Bank Employees' Skills & Knowledge [all age segments]

![Figure 17: Perceptions of Bank Employees' Skills & Knowledge [all age segments]](images/fig_17-eng.png)

FR1. Thinking about the interactions you’ve had during the past 12 months, please tell me how much you agree or disagree with he following statements….

Base: all respondents who use banking products [DK/Refusal=4%]

Seniors were less likely to report they have been provided information about how to protect themselves from financial abuse, fraud, or scams

Four in 10 seniors have not received information from their bank about how to protect themselves from financial abuse, fraud, or scams (Figure 18). Further, half of Canadians aged 75 and older (51%) reported they have not received information from their bank about protecting themselves from financial abuse, fraud or scams. In contrast, almost one-third of non-seniors reported not having received this information from their bank.

Figure 18: Financial Abuse, Fraud, or Scams [all age segments]

![Figure 18: Financial Abuse, Fraud, or Scams [all age segments]](images/fig_18-eng.png)

FR2. Has your bank ever provided you with information about protecting yourself from financial abuse, fraud, or scams?

Base: all respondents who use banking products [Refusal=<1%]

Seniors who received information about protecting themselves from their bank were more likely to report banking online (63%) than banking by phone (44%), in person (51%), or via an ATM (55%). Among non-seniors, there were no statistically significant differences in terms of the channels used to bank and receive information about protecting themselves from financial abuse, fraud or scams.

Suggestions to help protect seniors from financial abuse/fraud

Canadian seniors suggested banks could help protect their clients from financial abuse, fraud and scams by providing consumer alerts (16%), contacting customers if questionable transactions are identified (11%), providing customer education on financial abuse, fraud and scams (9%), providing more information and updates (8%), having better online security/technology (7%) and better detecting fraud through technology (7%).[7]

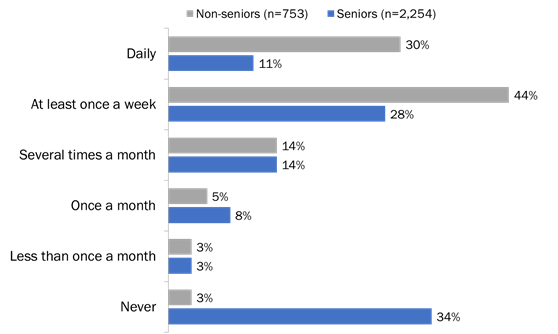

Seniors bank online less frequently than non-seniors

Seniors bank online less frequently than non-seniors, with 39% of seniors using online banking at least once a week compared to 74% of non-seniors (Figure 19). Further, 34% of seniors indicated they never bank online compared to only 3% of non-seniors. The likelihood of never banking online increases with age, from 1% of Canadians under 45 years of age to 8% of those 45 to 54, 22% of those 55 to 64, 33% of those 65 to 74, and 57% of seniors aged 75 and older.

Figure 19: Frequency of Online Banking

TE1. How often do you use online banking?

Base: all respondents [DK/Refusal=1%]

Seniors who do not bank online identified safety and security concerns (32%) as their primary barrier. Safety and security concerns were followed by a preference for banking in person or by phone (20%) and not using the internet (20%). Other barriers include not having a computer (12%), finding online banking to be too difficult or complex (11%), and a lack of trust in online banking (10%). Reasons identified less frequently include lacking reliable internet access at home (6%), not being shown how to bank online (6%), no need or interest (4%), and their banking is done by someone else (2%).

Those 55 to 64 and 65 to 74 years of age were more likely to point to safety or security concerns as the reason they do not bank online (39% and 37%, respectively, versus 23% of seniors aged 75 and older).

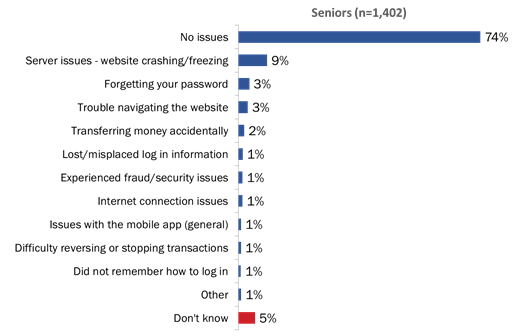

The majority of seniors who bank online do not encounter issues

Of seniors who have used online banking over the past 12 months, nearly three-quarters (74%) have not experienced issues. Non-seniors (58%) were more likely to experience issues than were seniors. Issues experienced by seniors are presented in Figure 20.

Figure 20: Issues with Online Banking

TE3. Over the past 12 months, what issues, if any, did you encounter when using online banking?

Base: n=1,402; those 55 plus who use banking products and bank online [Refusal=<1%] [Multiple responses accepted]

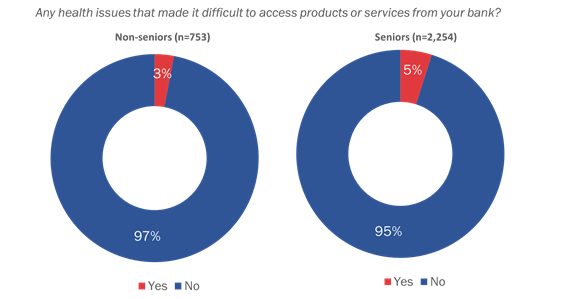

Older seniors are more likely to experience health issues that make it difficult to access banking products or services than are any other age group

The vast majority (95%) of seniors reported that, over the past 12 months, they did not have health issues that made it difficult to access products or services from their bank (Figure 21). The likelihood of having these health issues was highest among seniors aged 75 and older (8%) (although caution should be exercised in interpreting this finding given small sample size).

Figure 21: Health Issues

TE4. Over the past 12 months, have you had any health issues that made it difficult to access products or services from your bank?

Base: all respondents; those who use banking products [DK/Refusal=<1%]

Of those who experienced health issues that made it difficult for them to access products or services from their bank, over half (53% of seniors and 52% of non-seniors) indicated these issues were related to mobility and just under one in five identified these issues as a chronic illness or injury (18% of seniors and 17% of non-seniors). Other issues identified less frequently (4% or less) include problems with vision, difficulty remembering, a diagnosed mental health condition, and difficulty hearing.

Various factors make it difficult to access bank services

Seniors and non-seniors were asked to indicate if the following barriers have made it difficult to access services at their bank over the past 12 months:

Similar proportions of seniors and non-seniors face barriers in accessing banking products and services. Among seniors, one in five (20%) pointed to a lack of employees to assist them as a factor that made it difficult for them to access services at their bank. Approximately one in 10 or fewer experienced other barriers. For example, 13% could not make it to their bank during normal business hours, 12% lived far from a bank branch, 7% were unable to access a bank branch via public or personal transport, 4% were not presented information in their language of choice, and 4% were not treated with respect.

Non-seniors were more likely than seniors to report difficulty making it to their bank branch during their normal business hours (31% and 13%, respectively). In addition, Canadians between the ages of 55 and 64 were more likely then those aged 65 years and older to report this as a barrier (16% and 11%, respectively).

A very small number of respondents (less than 1%) identified factors other than those that were asked about. These include issues with physical access to a bank branch, issues with customer service or support, issues with bank policies or practices, and issues with phone access.

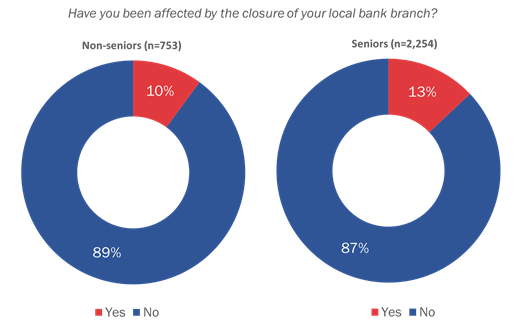

Seniors are more likely than non-seniors to have been affected by the closure of a bank branch within the past five years

Seniors are more likely than non-seniors to have been affected by the closure of a bank branch within the past five years (13% and 10%, respectively; Figure 22).

Figure 22: Bank Closures

TE5. Over the past 5 years, have you been affected by the closure of your local bank branch?

Base: all respondents [DK=<1%]

Of seniors who have been affected by a branch closure, close to half were affected ‘a lot’ either because there are few or no bank branches nearby (39%), or because they experienced issues with the location of the new branch (7%). In addition, just over one-third were affected ‘a little’ either because they had to change where they did their banking (28%), or because of general inconvenience (6%). A further 16% were affected ‘not much’ because the new location was still easy to get to and 10% were affected ‘not at all’ because they do most of their banking online.

Suggestions for improving bank products and services

When asked what banks could do to improve how they provide their products and services, 37% of seniors were satisfied and had no suggestions to offer. An additional 19% did not know how banks could improve their products and services.

Suggestions among seniors included improving policies and practices in general (10%), lowering fees (8%), incorporating more personal and flexible customer service (7%), and providing more information in plain language (6%). Other suggestions (5% or less) included hiring more employees and staff, better interest rates, better training for employees, ending the practice of closing branches, spending more time with clients, more advertising, longer hours, improving online or mobile banking, providing information in other languages, opening more branches, locations or kiosks, and improving products in general.

The Survey on Banking of Canadians yielded several important findings concerning the banking experiences of Canada’s seniors.

The following specifications applied to this survey:

| Total | Landline | Cell | |

|---|---|---|---|

| Total Numbers Attempted | 184,468 | 74,964 | 109,504 |

| Out-of-scope - Invalid | 96,566 | 26,714 | 69,852 |

| Unresolved (U) | 55,228 | 27,413 | 27,815 |

| No answer/Answering machine | 55,228 | 27,413 | 27,815 |

| In-scope - Non-responding (IS) | 26,448 | 16,593 | 9,855 |

| Language barrier | 903 | 561 | 342 |

| Incapable of completing (ill/deceased) | 636 | 461 | 175 |

| Callback (Respondent not available) | 3,462 | 1,577 | 1,885 |

| Refusal | 20,975 | 13,662 | 7,313 |

| Termination | 472 | 332 | 140 |

| In-scope - Responding units (R) | 6,226 | 4,244 | 1,982 |

| Completed Interview | 3,007 | 1,807 | 1,200 |

| Quota Full | 2,627 | 2,171 | 456 |

| NQ - Under 18 (QB) | 103 | 0 | 103 |

| NQ - Industry (QE) | 251 | 99 | 152 |

| NQ - Age (QG) | 83 | 66 | 17 |

| NQ - Refused to provide Province/Territory (QH) | 5 | 2 | 3 |

| NQ - No Bank Account (QI) | 150 | 99 | 51 |

| Response Rate | 7.62 | 9.64 | 5.26 |

Survey on Banking of Canadians

Section 1: Introduction

Good morning/afternoon/evening, my name is [Interviewer's name]. I’m calling on behalf of Phoenix SPI, a public opinion research company. We are conducting a survey for the Government of Canada on issues of interest to Canadians. Would you prefer to continue in English or French? / Préférez-vous continuer en anglais ou en français?

Please be assured that we are not selling or soliciting anything. The survey takes about 15 minutes and is voluntary. Your responses will be kept entirely confidential and anonymous.

[LANDLINE SAMPLE]

[CELL SAMPLE]

[EVERYONE]

THANK/DISCONTINUE MESSAGE: “Thank you for your willingness to take part in this survey, but you do not meet the eligibility requirements of this study.”

THANK/DISCONTINUE MESSAGE: “Thank you for your willingness to take part in this survey, but you do not meet the eligibility requirements of this study.”

THANK/DISCONTINUE MESSAGE: “Thank you for your willingness to take part in this survey, but you do not meet the eligibility requirements of this study.”

THANK/DISCONTINUE MESSAGE: “Thank you for your willingness to take part in this survey, but you do not meet the eligibility requirements of this study.”

The questions in this survey deal with banking, but please be assured that you will not be asked to provide any information about your personal finances. The Government of Canada would like to find out what Canadians think about their banks. IF A RESPONDENT QUESTIONS THE LEGITIMACY OF THE SURVEY, PROVIDE THE FOLLOWING INFORMATION:

Can contact the Financial Consumer Agency of Canada Consumer Services Centre from Monday to Friday 8:30am to 5:00pm eastern time:

For service in English: 1-866-461-3222

For service in French: 1-866-461-2232

[NOTE TO INTERVIEWER: READ IF RESPONDENT HOLDS AN ACCOUNT WITH MORE THAN ONE BANK AND SEEKS CLARIFICATION ABOUT WHICH BANK THE SURVEY QUESTIONS REFER TO: IF YOU BANK WITH MORE THAN ONE FINANCIAL INSTITUTION, PLEASE FOCUS ON THE ONE THAT YOU USE MOST OFTEN]

INTR_1: To start, who does the majority of your banking? [READ LIST]

INTR_2: Do you currently act on behalf of someone else with regards to banking? This could be formally through a Power of Attorney or informally by helping a family member with his or her banking, such as paying bills or managing accounts. If asked by the respondent, paying bills refers to managing one’s bill payments.

Section 2: Communication and Disclosure

CD_R1: The first few questions ask about your banking experience and how you prefer to get information on banking products and services.

CD_1 Over the past 12 months, what is the most common way you did your banking? [READ LIST]

CD_2 Over the past 12 months, how often did you do your banking at a branch by speaking with a bank employee? Would you say… [READ LIST]

CD_3 Which of the following banking products and services do you currently have? [READ LIST. ACCEPT MULTIPLE RESPONSES] INTERVIEWER: IF NEEDED, REMIND THE RESPONDENT THAT YOU ARE NOT ASKING FOR ANY ACCOUNT SPECIFIC INFORMATION – JUST WHETHER OR NOT THEY HAVE ONE OF THESE PRODUCTS.

[INTERVIEWER: THE FOLLOWING ADDITIONAL REGISTERED ACCOUNTS MAY BE ACCEPTED]:

CD_4 Over the past 12 months, did you experience any issues when using these banking products or services?

CD_4A [CD_4=1] With what product or service did you experience an issue? IF RESPONDENT VOLUNTEERS THAT ISSUES WERE EXPERIENCED WITH MORE THAN ONE PRODUCT/SERVICE SAY: If you experienced issues with more than one product or service, please tell me which product or service you experienced the biggest issue with. [READ LIST; LIST TO BE POPULATED WITH ITEMS MENTIONED AT CD_3]

CD_4B Over the past 12 months, what issues did you encounter with [INSERT PRODUCT/SERVICE FROM CD_4A]? [DO NOT READ LIST; ACCEPT MULTIPLE RESPONSES]

CD_5 How do you prefer to receive information about your banking products and services? [READ LIST]

CD_R2: Could you please tell me if the following statements describe your experience getting information on banking products and services from your bank. If something does not apply to you, please just say so.

CD_6 Over the past 12 months, have there been times when you’ve received information from your bank that was difficult to understand?

CD_6A [IF CD_6=1] How often would you say this tended to happen? [READ LIST]

CD_6B [Ask if CD_6 = 1] What could your bank do to provide you with information that is easier to understand? [DO NOT READ LIST. ACCEPT MULTIPLE RESPONSES]

Section 3: Relationship with Banks

TR_R1: We would now like to ask you about your interactions with bank employees - including in-person, by phone or online. Thinking about the interactions you’ve had during the past 12 months, please tell me how much you agree or disagree with the following statements, using a 5-point scale where ‘1’ means strongly disagree, ‘5’ means strongly agree, and ‘3’ means neither agree nor disagree. If something does not apply to you, please just say so.

[ROTATE STATEMENTS; REPEAT SCALE INSTRUCTIONS AS NEEDED]

TR_1 Bank employees make an effort to understand your needs.

TR_2 Bank employees know how to address your needs.

TR_3 Bank employees ensure that you understand your banking products and services.

TR_4 You rely on the advice of your bank when you make decisions about your banking products and services.

TR_5 You are treated with respect and professionalism when you do your banking.

[RESPONSE OPTIONS; INTERVIEWER: IF A RESPONDENT GIVES THE LABEL – AGREE/STRONGLY AGREE, ETC. ACCEPT AND DO NOT CONFIRM SCALE NUMBER]

Section 4: Fraud and Financial Abuse

FR_R1: The next few questions ask about scams, fraud and financial abuse - including times when a bank account has been used without permission or someone felt pressure to share their money or property.

FR_R2: Please tell me how much you agree or disagree with the following statement. To do so, please use a 5-point scale where ‘1’ means strongly disagree, ‘5’ means strongly agree, and ‘3’ means neither agree nor disagree. [INTERVIEWER: ACCEPT ANSWER IF RESPONDENT PROVIDES RESPONSE AS STATEMENT]

FR_1 Bank employees have the skills and knowledge to help you if your bank identified questionable transactions in your accounts that might be signs of financial abuse, fraud, or scams.

FR_2 Has your bank ever provided you with information about protecting yourself from financial abuse, fraud, or scams?

FR_3 What do you think your bank could do to help protect you from financial abuse, fraud or scams? [MARK ALL THAT APPLY. DO NOT READ]

Section 5: Technology and Accessibility

TE_R1: Next, we would like to ask you about your experiences with online banking.

TE_1 How often do you use online banking? This includes banking on your computer, tablet, or other mobile device. [READ LIST]

TE_2A [If TE_1=5, 6] What are the main reasons you do not frequently bank online? [DO NOT READ LIST; ACCEPT MULTIPLE RESPONSES]

TE_2B [If TE_1= 7] What are the main reasons you do not bank online? [DO NOT READ LIST; ACCEPT MULTIPLE RESPONSES]

TE_3 [If TE_1=1,2,3,4,5,6] Over the past 12 months, what issues, if any, did you encounter when using online banking? [DO NOT READ; ACCEPT MULTIPLE RESPONSES]

TE_R2 We would now like to ask you about your experience accessing banking products and services.

TE_4 Over the past 12 months, have you had any health issues that made it difficult to access products or services from your bank?

TE_4A [Ask if TE_4A =1] Over the past 12 months, what health issues made it difficult for you to access products or services from your bank? [DO NOT READ; ACCEPT MULTIPLE RESPONSES]

TE_5 Over the past 12 months, did any of the following make it difficult to access services at your bank? [READ LIST; RANDOMIZE]

[RESPONSE OPTIONS; DO NOT READ]

TE_5 Over the past 5 years, have you been affected by the closure of your local bank branch? [DO NOT READ]

TE_5A [If TE_5=1] How did this branch closure or relocation affect your ability to conduct your regular banking activities? [DO NOT READ; ACCEPT MULTIPLE RESPONSES]

Section 6: General

GE_R We would now like to ask you a few general questions about your banking products and services.

GE_1 If given the opportunity, would you give your bank permission to contact someone you trust if your bank had concerns about your well-being or about questionable transactions in your accounts? [DO NOT READ; INTERVIEWER: IF ASKED BY RESPONDENT, WELL-BEING REFERS TO MENTAL HEALTH, PHYSICAL HEALTH, AND SAFETY FROM FINANCIAL FRAUD]

GE_2 In general, how do you feel about dealing with your bank?

[TEXT FIELD]

GE_2A Please briefly describe why you feel this way.

[TEXT FIELD]

GE_3 What do you think banks could do to improve how they provide their products and services? [DO NOT READ LIST; ACCEPT MULTIPLE RESPONSES]

Section 7: Demographic and Socio-Economic Questions

DM_R1 The last few questions are for classification purposes only

DM_1 [RECORD BY OBSERVATION] If unsure of respondent’s gender, please confirm.

DM_2 What is your current marital status? [DO NOT READ]

DM_3 Were you born in Canada? [DO NOT READ]

DM_3A [If DM_3=2] In what year did you first immigrate or move to Canada?

DM_4 Do you identify as an Aboriginal person, that is, First Nations (North American Indian), Métis or Inuk (Inuit)? [DO NOT READ] INTERVIEWER: IF THE RESPONDENT ANSWERS ESKIMO, CODE YES.

DM_5 What is the highest level of formal education that you have completed? [READ LIST; STOP WHEN A RESPONSE IS SELECTED]

DM_6 Which of the following categories best describes your current employment status? Are you…[READ LIST; STOP WHEN A RESPONSE IS SELECTED]

DM_7 Which of the following categories best describes your total household income for 2018? That is, the total income of all persons in your household combined, before taxes. Please be assured that your response to this, and all, questions in the survey is confidential [READ LIST; STOP WHEN A RESPONSE IS SELECTED]

DM_8 Overall, who in your household is primarily responsible for making sure that the regular ongoing bills and other financial commitments are met? [DO NOT READ UNLESS HELPFUL]

DM_9 Would you please provide your postal code? [TEXT FIELD: ENTER POSTAL CODE]

DM_9A [IF NO] Would you be comfortable providing the first 3 digits of your postal code? [TEXT FIELD: ENTER FSA]

That concludes the survey. Thank you very much for your thoughtful feedback. It is much appreciated. This survey was conducted on behalf of the Financial Consumer Agency of Canada.

[1] In Canada, the term “seniors” is generally ambiguous, with some definitions identifying seniors as individuals aged 55 and older, while others define seniors as those aged 65 and older. For the purposes of this research, seniors are defined as Canadians aged 55 and older in order to identify the unique banking experiences and challenges of older Canadians and to ensure the code of conduct remains relevant for older Canadians in the future.

[2] Sampling in proportion to the population would have yielded the following number of completed interviews by age group: 55-64 (n=1,100), 65-74 (n=700), and 75+ (n=450). Instead, interviews were completed as follows: 55-64 (n=850), 65-74 (n=701), and 75+ (n=703). An oversample of Canadians aged 75 and older was required to ensure an adequate sample size for statistical comparisons.

[3] Seniors most commonly expressed these feelings with words such as ‘very good’, ‘good’, and ‘fine’.

[4] If respondents volunteered that they experienced an issue with more than one product or service, they were asked to identify which product they experienced the biggest issue.

[5] Interactions with bank employees includes both in-person, phone, and online interactions.

[6] Among seniors, agreement with each of these statements was more likely to be strong than moderate—strong agreement ranged from a low of 31% for replying on advice from their bank to a high of 74% for being treated with respect and professionalism. In the case of non-seniors, strong agreement with these statements ranged from a low of 25% for relying on advice from their bank (the only statement for which agreement was more likely to be moderate than strong) to a high of 68% for being treated with respect and professionalism.

[7] Four in 10 (40%) seniors did not offer any suggestions of what their bank could do to help protect them from financial abuse, fraud or scams and almost one in 10 (9%) indicated there was nothing their bank could do.

[8] The response rate formula is as follows: [R=R/(U+IS+R)]. This means that the response rate is calculated as the number of responding units [R] divided by the number of unresolved [U] numbers plus in-scope [IS] non-responding households and individuals plus responding units [R].