INTRODUCTION

The

Financial Consumer Agency of Canada (FCAC) is an agency of the Government of

Canada that ensures federally regulated financial entities comply with consumer

protection measures, promotes financial education, and raises consumers’

awareness of their rights and responsibilities. It was established in 2001 by

the federal government to strengthen oversight of consumer issues and expand

consumer education in the financial sector. FCAC provides information and

resources to consumers, merchants, and the industry and is focused on

strengthening financial literacy in Canada.

The

Bank of Canada is the nation's central bank. Its principal role is to promote

the economic and financial welfare of Canada. This is done primarily through

conducting monetary policy to keep inflation low and stable. Another important

core function is to promote safe, sound and efficient financial systems in

Canada and internationally. The Bank also designs, issues and distributes

Canada’s bank notes and acts as the “fiscal agent” for the Government of

Canada, managing its public debt program and foreign exchange reserves.

Mortgage

loans with terms longer than 5 years (longer-term mortgages) are available to

Canadian consumers. However, take-up rates are very low compared to mortgages

with term lengths of 5 years or less (shorter-term mortgages). Just 2% of all

mortgages issued in 2018 were fixed-rate loans with a term longer than five

years. Given that interest rates have been at historically low levels for an

extended period of time, borrowers may be exposed to financial risks should

interest rates rise. For example, some borrowers could be at risk of experiencing

additional financial stresses due to the rising cost of servicing a mortgage at

a higher interest rate (interest rate risk). Other borrowers may be at risk of not

being able to obtain a new mortgage to finance the remaining principal at the time

of renewal (rollover risk). This current research seeks to understand the level

of consumer awareness about available mortgage options as well as to understand

the factors associated with consumer mortgage choices.

Ipsos was

commissioned by the Financial Consumer Agency of Canada (FCAC) in collaboration

with the Bank of Canada (BoC) to conduct research to provide a baseline on

Canadian consumers level of awareness and interest in longer-term mortgages.

The research also sought to explore consumers rationale, behavioural biases

and other factors that motivate decisions to obtain, or not, a longer-term

mortgage.

The

research was conducted in two phases. Phase 1 involved qualitative research designed

to help initiate the study and discover the depth and breadth of awareness,

misconceptions and opportunities related to mortgage decision-making. The

results of Phase 1 are provided under separate cover. Building upon the

learning gained from the qualitative phase, Phase 2 involved a quantitative

survey to validate and further refine the learnings from the qualitative study.

The quantitative

study leveraged previous research to help build an understanding of factors

that may impact borrowers decision to choose longer-term mortgages. Results

from an omnibus survey conducted by the Privy Council Office in September 2018

suggest that demand side factors may in part explain the lack of take-up of

such mortgages. For example, more than half of the Canadian adult population

may not know that longer-term mortgages are available. This lack of awareness

is greatest among Canadians with lower levels of education and those with lower

levels of income.

The

research conducted in September 2018 found that motivating factors to taking up

a longer-term mortgage include:

Additionally,

the research found there are factors that may lead borrowers to avoid choosing

longer-term mortgages, such as:

-

unwillingness to

commit for a longer term (e.g., employment insecurity, possible need to move

houses in a few years, possible changes in family situation, etc.);

-

perception that

interest rates are significantly higher for longer-term mortgages.

Very

few participants mentioned prepayment penalties as their motivating factors for

taking up or avoiding longer-term mortgage. None of the participants mentioned

that the penalty calculation using the interest rate differential (IRD) is not

applicable after 5 years.

The

relatively short survey produced interesting and important first-round results,

although certain questions that are relevant from a policy perspective remain

unanswered. For example, are consumers aware of their prepayment right and associated

costs on various products? Does consumer attitude towards longer-term mortgages

vary with their financial well-being (e.g., indebtedness)? How much will the

relative price of a longer-term mortgage need to decline to generate a greater

interest?

The

current research set out to address these questions.

The

quantitative phase was conducted via an online survey. The survey was conducted

in English and French between June 18 and June 30, 2019. Respondents to the

survey were drawn from Ipsos panel sample sources making it a non-probability

sample. Online panels are considered non-probability samples because

respondents have been pre-recruited to participate in research, and therefore,

respondents are not randomly selected from the broad universe of Canadian

population. Due to the non-probabilistic nature of the research, a known

sampling limitation is that the results cannot be extrapolated to the rest of

the Canadian population. However, online panel surveys like the one conducted,

are commonly used in the public opinion and market research industry and

provide useful insights on the preferences of the Canadian population as the samples

are designed to be representative of the population, regionally,

demographically and socio-economically. Moreover, the large sample size on

which the current survey is based (greater than n=2,500 per sample) ensures the

insights are highly reliable. For these reasons, consumers and respondents

are used interchangeably when discussing results throughout the report.

The survey

was conducted with two separate samples. Sample 1, which is referred to as the

target

audience

, included those Canadians who currently own a home with a mortgage,

or those likely to purchase a home with a mortgage in the next 5 years. This

group has a greater propensity to have previous experience making borrowing

decisions, or to do so in the future, than the general population.

Sample 2 represents

the

general population

, which will naturally include some overlap with

the type of individuals represented in Sample 1: a sub-set of homeowners with a

mortgage or those likely to purchase a home in the future. However, the two

samples were mutually exclusive; no respondent falls into both samples.

A total of

n=5036 Canadians age 18 and older were surveyed -- split roughly 50% between

the target audience (n=2511) and 50% general population (n=2525).

The target audience quotas were set by region (based

on the 10 provinces, those living in the territories were excluded) based on

the 2016 Census and were achieved, thus no weighting was applied.

Gender and age were not weighted because the sample was not intended to be representative

of the general population and demographic composition figures for this audience

are not available.

Figure

1

: Target Audience Sample Composition

|

|

Unweighted

Sample Size

|

Sample Proportions

|

|

Canada

|

2,511

|

100%

|

|

Region

|

|

|

|

British

Columbia

|

334

|

13%

|

|

Alberta

|

288

|

11%

|

|

Manitoba/Saskatchewan

|

171

|

7%

|

|

Ontario

|

941

|

38%

|

|

Quebec

|

604

|

24%

|

|

Atlantic

Canada

|

173

|

7%

|

|

Gender

|

|

|

|

Male

|

1156

|

46%

|

|

Female

|

1350

|

54%

|

|

Other/Prefer

not to say

|

5

|

<1%

|

|

Age

|

|

|

|

18-24

|

97

|

4%

|

|

25-34

|

607

|

24%

|

|

35-44

|

485

|

19%

|

|

45-54

|

430

|

17%

|

|

55-64

|

472

|

19%

|

|

65+

|

420

|

17%

|

The

general population data were weighted by region, age, gender and household

income to ensure that the survey samples composition reflects that of the

adult population according to 2016 Census data. Household income targets were

calculated at an individual level. The percentages represent the number of

individuals in Canada aged 18 or older, who are part of a household with the

respective household income. Additionally, the decision was made to offer

respondents a prefer to not say option when reporting household income. In

total 9% of the sample took this option. Given that household income was a

weighting variable, the target percentages were re-based to reflect the

allowance of this 9% to remain in the data the data was not imputed or

re-assigned to other income categories.

Figure

2

:

General Population Sample Composition

|

|

Unweighted

Sample Size

|

Sample Proportions

|

Weighted

Sample Size

|

Sample Proportions

|

|

Canada Canada

|

2,525

|

100%

|

2,525

|

100%

|

|

Region

|

|

|

|

|

|

British Columbia

|

336

|

13%

|

283

|

14%

|

|

Alberta

|

280

|

11%

|

343

|

11%

|

|

Prairies (SK/MB)

|

165

|

7%

|

165

|

7%

|

|

Ontario

|

968

|

38%

|

970

|

38%

|

|

Quebec

|

610

|

24%

|

593

|

24%

|

|

Atlantic Canada

|

166

|

7%

|

172

|

7%

|

|

Gender

|

|

|

|

|

|

Male

|

1,204

|

48%

|

1237

|

49%

|

|

Female

|

1,302

|

52%

|

1237

|

49%

|

|

Other/Prefer not

to say

|

19

|

<1%

|

50

|

1%

|

|

Age

|

|

|

|

|

|

18-24

|

179

|

7%

|

286

|

11%

|

|

25-34

|

482

|

19%

|

425

|

17%

|

|

35-44

|

446

|

18%

|

412

|

16%

|

|

45-54

|

416

|

17%

|

461

|

18%

|

|

55-64

|

492

|

19%

|

450

|

18%

|

|

65+

|

510

|

20%

|

492

|

20%

|

|

Net household income

|

|

|

|

|

|

<$20,000

|

227

|

9%

|

138

|

6%

|

|

$20,000 -<$40,000

|

392

|

16%

|

282

|

11%

|

|

$40,000-<$60,000

|

478

|

19%

|

332

|

13%

|

|

$60,000-<$80,000

|

380

|

15%

|

320

|

13%

|

|

$80,000-<$100,000

|

338

|

13%

|

276

|

11%

|

|

$100,000-<$150,000

|

346

|

14%

|

680

|

27%

|

|

$150,000+

|

138

|

5%

|

270

|

11%

|

|

Prefer not to say

|

226

|

9%

|

227

|

9%

|

Since both the target audience and

general population samples were based on those who initially self-selected for

participation in the panel, no formal margin of error has been calculated. However,

throughout the report,

descriptive statistics have been reported and tests of significance have been

conducted to establish the extent of the relationship among variables. The

survey instrument was an average of 14.2 minutes in length and the median

length was 10 minutes. It included a series of closed-ended and open-ended

questions and explored the following:

-

awareness of

mortgage terminology;

-

awareness and

knowledge of longer-term mortgages;

-

level of interest

in longer-term mortgages absent specific interest rate considerations;

-

likelihood of

considering a longer-term mortgage given specific interest rate scenarios;

-

attitudes towards

factors found to influence appetite in longer-term mortgages (based on the

findings of the Phase 1 qualitative and 2018 Privy Council Office omnibus

survey);

-

the

influence of providing additional information about mortgage options and

features that respondents may not have known before entering the survey on the

probability of considering a longer-term mortgage.

The survey also employed a conjoint

exercise designed to estimate the likelihood of a consumer choosing a longer-term

mortgage over a shorter-term mortgage with a fixed or variable interest rate. Conjoint

analysis is a statistical technique to determine what combination of a limited

number of attributes is most influential on respondents choice or decision

making. In this circumstance, the attributes under evaluation were variable

vs. fixed terms; the length of the term (e.g., 5 years vs. 10 years); and the

interest rate at which each option is offered. While all scenarios were

evaluated, the primary goal was to understand the attributes that are most

influential in choosing a 10-year fixed mortgage.

The exercise required respondents to assume

a scenario where they need to borrow $300,000 (initial principal amount) and

were asked to assume the following conditions:

-

The

loan needs to be paid off within 25 years. So, you need to re-negotiate a new

contract in 5 years (if you choose the 5-year variable or fixed rate mortgage),

or in 10 years (if you choose the 10-year fixed rate mortgage);

-

You

know that you qualify for any of the mortgages presented in the scenarios.

Each respondent was shown 4 screens,

each showing a different set of choices (4 choice sets in total per respondent).

Each choice set contained 3 options: a 5-year variable, 5-year fixed and 10-year

fixed terms with various interest rates. The respondent was required to choose

one of the options none and dont know options were not permitted. The design

of choice sets was built using interest rate levels ranging from 4.00% to 6.75%

with the following conditions:

-

The

5-year variable term was always offered at a 4.00% interest rate;

-

The

5-year fixed term interest rate could not be lower than variable rate (4.00%);

-

The

10-year fixed term interest rate was at least 0.25% higher than the 5-year

fixed term.

The

results of the conjoint analysis measure the percentage of respondents that

will choose the 10-year fixed interest rate option over a 5-year fixed interest

rate or 5-year variable interest rate option when offered at specific interest

rates. Although respondents answered only four scenarios, the scenarios were

designed and rotated such that the probability of choosing the 10-year interest

rate option can be modelled based on interest rate differentials covered in the

survey, as well as those not covered in the survey if they are within the

bounds of minimum and maximum interest rate levels.

In order to understand the potential impact

of providing respondents with more information about variable and fixed rate

options that could influence their decision-making on which option to choose, within

each sample group, target audience and general population, respondents were

randomly assigned into one of three sub-groups:

Group

1 respondents were provided with no additional information about each option

this was referred to as the

no disclosure

group or control group;

Group

2 respondents were provided with limited additional information this was

referred to as the

partial disclosure

group; and,

Group

3 respondents were provided with more information as the

full disclosure

group.

The partial and full disclosure information

provided to respondents is shown in the table below.

Figure

3

: Disclosure Information

|

|

5-year

variable

|

5-year

fixed rate

|

10-year

fixed rate

|

|

[Group 2 & Group 3] Can the interest

rate change during the term?

|

Yes - But you can

switch to a fixed rate at any time without paying a penalty

|

No

|

No

|

|

[Group 2 & Group 3] Will my payment

amount

change during the term?

|

No

|

No

|

No

|

|

[Group 2, Group 3] Can I know how much

will be left to pay on my house at the end of the term?

|

No - If the interest

rate goes up, a larger portion of your payment will go towards paying the

interest.

|

Yes

|

Yes

|

|

[Group 3] Can I break my mortgage

contract?

|

Yes with a

penalty fee

|

Yes with a

penalty fee

|

Yes with a

penalty fee

|

|

[Group 3] Approximate penalty fee if I

break the mortgage contract after 3 years (e.g. sell the home).

|

If interest rates go up by 1%

|

$3,600

|

$4,000

|

$4,400

|

|

If interest rates go down by 1%

|

$3,600

|

$6,000

|

$21,000

|

|

[Group 3] Approximate penalty if I break

the mortgage contract after 5 years.

Note:

The penalty

calculation changes after 5 years have passed.

|

n/a

|

n/a

|

$4,400

|

-

The

terms target audience and homeowners and likely homeowners are used

interchangeably throughout the report to denote the target audience.

-

All

results in the report are expressed as a percentage, unless otherwise noted.

-

Throughout

the report, percentages may not always add to 100% due to rounding or if

respondents were permitted to give more than one response.

-

Due

to rounding, some percentages in the report may not match those presented in

the tabulated data (available under separate cover).

-

When

reporting sub-group variations, only differences that are significant at the

95% confidence level, indicative of a pattern and pertaining to a sub-group

sample size of more than n=30 are discussed.

-

Throughout

the report arrows can be seen, which indicate statistically significant

differences between the target audience and the general population:

-

A green up arrow indicates a

significantly larger percentage within the designated population.

A green up arrow indicates a

significantly larger percentage within the designated population.

-

A red down arrow indicates a

significantly lower percentage within the designated population.

A red down arrow indicates a

significantly lower percentage within the designated population.

-

Appended

to the report is a copy of the questionnaire.

KEY FINDINGS

Many consumers do not have a good

understanding of mortgage-related terminology half of consumers are confused

about what mortgage term means providing incorrect or vague descriptions or

indicating they simply do not know (51% of the general population, 42% of the target

audience). The amortization period is even more commonly misunderstood with

most respondents offering a description that is incorrect. Correct

understanding of this terminology is higher among the target audience than the

general population, but still represents less than half of consumers. Only 26%

of the target audience and 18% of the general population sample provide correct

answers for both phrases.

Less than half of consumers (40% general

population, 37% target audience) claim to be aware that longer-term mortgages

are available in Canada. Only one-quarter believe fixed mortgage terms of 10

years are available in Canada. This is consistent across the target and general

populations.

However, as noted above, many consumers do

not have a correct understanding of mortgage terminology. Therefore, the true

level of awareness of longer-term mortgages in Canada is likely significantly

lower. The survey found that only 7% of the target audience and 6% of the

general population have a correct understanding of the relevant terminology (a

correct understanding of both mortgage term and amortization period) and indicate

that 10-year fixed terms are available in Canada. In total, only 10% of the target

audience and 7% among the general population have a correct understanding of

terminology of both term and amortization and believe any terms greater than 5

years are available in Canada. Notably, among consumers generally (including

those with incorrect or vague understanding of mortgage terminology), more

consumers believe that 10-year fixed mortgages are not available compared to those

who indicate being unsure or dont know. Consistent with previous research conducted

on the topic, awareness is lower among consumers with less education.

In many

cases, consumers misunderstanding of mortgage terms and the differences

between shorter and longer-term mortgages creates a barrier to their openness

to considering longer-term mortgages. For example, a large minority of

consumers (43% of the target audience and 40% of the general population)

believe that the longer the mortgage term the more expensive it is to break

the mortgage contract, This is correct if the respondent is thinking about the

cost of breaking a contract during the first 5 years, but not the later 5 years

which is an important feature of a 10-year fixed mortgage. Further, among both

the target and general population, almost three quarters (70% respectively)

stated they do not know whether the rules regarding penalty fees change after 5

years in longer-term mortgages, indicating a low knowledge base and a high

degree of uncertainty among Canadians on the features of longer-term mortgages.

This misinformation about the costs of breaking a longer-term mortgage and lack

of knowledge of how penalty fees work become even more relevant to the nearly

half of consumers (44% of the target audience and 42% of the general

population) who say they would be afraid of missing out on a potential

decrease in interest rates if [they] locked into a mortgage longer than 5 years.

It is possible that with a better understanding of the changes in mortgage

penalties after 5 years consumers would be more open to considering longer-term

mortgages. In fact, the survey found that those who are aware that the rules

around longer-term mortgage penalties change after 5 years are significantly

more likely to consider a longer-term mortgage.

The survey

found that consumers are more than twice as likely to say they would lean

toward a fixed interest mortgage than a variable interest mortgage (46% vs 19%

respectively among the target audience and 42% vs. 16% respectively among the

general population). Interestingly, these responses do not vary based upon

whether the respondents feel that their life stage makes them more suited to a

shorter or longer-term mortgage.

A

reasonably large percentage of consumers (29% of the target audience and 41% of

the general population) indicated that the next time they need to renew [their]

mortgage / if they were to purchase a home and finance it with a mortgage, a

mortgage term longer than 5 years would suit them. This is given their life

plans and circumstances and applies in the absence of being provided an

interest rate to consider. Even among those consumers who have a correct

understanding of mortgage terminology (mortgage term and amortization

period), as many as 16% of the target audience and 31% of the general

population say a mortgage term longer than 5 years would suit their life

plans. If we consider this question a proxy for preference, then there is a

reasonably large pool of consumers who (again absent an interest rate

comparison) would lean toward longer-term mortgages.

One in ten

consumers (11% target audience and 14% general population) indicate that they

would

almost certainly

consider a longer-term mortgage the next time

they need to renew their mortgage or when they buy a home. Likelihood is

significantly lower among homeowners with a mortgage (6%) compared to others

(21%). More consumers indicate being

likely

to consider (not

almost

certain

) a longer-term mortgage (15% among the target audience and 18%

among the general population).

There is a

correlation between life plans and an appetite in longer-term mortgages. Sixty

percent of the general population that indicates that a mortgage term of more

than 5 years is suited to their life plans (e.g., expected time to own the home,

etc.) are

almost certain

or

likely

to consider a longer-term mortgage

compared to only 12% of those who do not believe their life stage suits a term

longer than 5 years.

A

conjoint exercise was conducted to supplement consumers stated likelihood of

choosing a longer-term mortgage. The exercise asked consumers to make a choice

between 3 options: 5-year variable, 5-year fixed and 10-year fixed mortgage offered

at various interest rate levels. This exercise was intended to validate the

qualitative finding that consumers are primarily open to considering a

longer-term mortgage if the interest rate differential between the 5-year fixed

option and 10-year fixed option is 1% or less. The results are generally

consistent with this finding. However, the survey found a significant drop off

in probability to choose a 10-year fixed term at a lower interest rate

differential compared to a 5-year fixed: 0.75% or greater, rather than a 1.0%

differential. In the choice exercise, the probability of choosing the 10-year

fixed option dropped significantly when the differential interest rate was

0.75% higher than the 5-year fixed.

Share

of preference in choosing the 10-year fixed mortgage is highest in the

following scenario: 4.00% for 5-year variable, 4.00% for 5-year fixed and

4.25% for 10-year fixed 17% among non-mortgage holders and 9% among current

mortgage holders (it was consistently found in the choice exercise that

non-mortgage holders are more open to considering a 10-year fixed term than

mortgage holders). Share of preference falls to only 8% among non-mortgage

holders and 3% among mortgage holders in a steep interest rate scenario (4.00%

for 5-year variable, 5.50% for 5-year fixed and 6.50% for 10-year fixed).

In

addition to the size of interest rate differential between mortgage options,

the research found household income, financial stress

and risk aversion

influence consideration of a longer-term mortgage. Other secondary factors were

found to influence this choice as well. These include: the perception that

there is greater consistency of mortgage payments with fixed terms, interest

rate risk (feeling more comfortable having interest rate fixed for as long as

possible to avoid the risk of increasing), and the appeal of avoiding the

hassle of renewing.

A partial

least squares regression analysis of the probabilities of choosing a 10-year

fixed mortgage over a 5-year fixed or 5-year variable reveals that

both low income and

higher income individuals could choose the 10-year mortgage, but for different

reasons. More specifically:

-

Financially

stressed consumers who place more weight on minimizing the risk of interest

rates rising;

-

Higher

income consumers who are willing to tolerate the risk of losing out on a

potential financial benefit from choosing a shorter-term mortgage if interest

rates decline over time.

Financially

stressed

consumers tend to have lower household income and believe

there is greater consistency of

mortgage payments with fixed terms (compared to variable interest rate terms).

They also have greater concerns about interest rates rising (feeling more

comfortable having interest rate fixed for as long as possible to avoid the

risk of increasing), and the appeal of avoiding the hassle of renewing. C

onsumers under medium

and high financial stress skew younger, more strongly toward women than men,

and those who do not yet own a home yet would like to own one.

By virtue

of being concerned about the risk of rising interest rates, these consumers appear

to be most aligned with the benefit of longer-term mortgages such that

borrowers are less

frequently

exposed to the risk that the interest rate will increase significantly upon

renewal. However, there is no evidence that the motivations are this clean cut.

Being assured of the consistency of payments for budgeting purposes and

avoiding the hassle and stress of renewing are attitudes that are also found

among consumers that place greater importance on guaranteed interest rate

stability.

In contrast, higher

income consumers who are willing

to tolerate more risk

appear

to be less concerned about potentially making a wrong decision by locking

themselves into a 10-year fixed mortgage potential cost of this error

should interest rates go down is not something that they would pay attention to

now. These consumers may not care much if they can win some money if interest

rates decline. Their approach to a 10-year fixed mortgage might be

characterized as shoot-and-forget meaning they are making a choice because

they believe negative consequences will be small/not a cause of major concern.

Taking into consideration the relatively low mortgage amount being simulated in

the hypothetical exercise for some respondents (for example compared to housing

prices in Toronto and Vancouver), this perspective could be inflated.

Figure

4: Patterns of Factors Associated with Choice

of 10-Year Fixed Term

|

Lower

income, higher financial stress

|

Higher income, lower financial stress

|

|

Interest Rate Risk Avoidance

& Avoiding Hassle of

Renewing

|

Shoot

and Forget

|

|

Higher

risk aversion

|

Medium risk aversion

|

|

Lower

education level

|

Higher education level

|

|

Lower

household income

|

Higher household income

|

|

Higher

financial stress

|

Lower financial stress

|

|

Life

plan is suited to a term greater than 5 years

|

Life plan is suited to a term of 10 years

or longer

|

|

Less

likely to have a mortgage now (e.g. renters)

|

More likely to have a mortgage

|

|

Feel

more comfortable having interest rate fixed for as long as possible to avoid

the risk of increasing

|

Not afraid of missing out on a potential

decreased in interest rates if locked into a term longer than 5 years

|

|

Place

importance on consistency of mortgage payments over the term

|

No

strong opinion on the consistency of mortgage payments

|

|

Find

avoiding the hassle of having to renew their mortgage often appealing

|

Would

NOT feel anxious to be locked into a term longer than 5 years

|

The

research explored the extent to which providing additional information to

consumers influences their probability of choosing 10-year fixed terms (see

Figure 3). Among the target audience and general population, the survey found

no significant difference, regardless of what information was provided. This

suggests that consumers are more likely to default to their predisposed views

or understanding and/or place significant weight on the interest rate

differential, when making choices rather than consider information that may

positively or negatively influence their choice of a 10-year fixed term.

DETAILED FINDINGS

This

section details the level of awareness and knowledge of longer-term mortgages

among both the target audience and the general population.

In order

to assess the baseline knowledge of both the target audience and the general

population, survey respondents were asked to provide their understanding of the

phrases mortgage term and amortization period by answering open-ended

questions asking them what they believe these phrases mean.

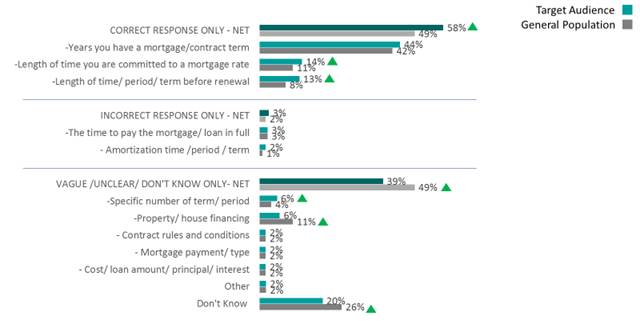

The responses

indicate that there is a significant lack of knowledge about mortgage terms

among both the general population and the target audience. Only half of the

general population (49%) provided a strictly correct description of the phrase

mortgage term. Correct answers included: years you have a mortgage/contract

term, the length of time you are committed to a mortgage rate, or the

length of time before renewal. The target audience was only slightly more

knowledgeable with 58% offering a strictly correct answer. Notably, very few

respondents offered strictly incorrect responses (3% of target audience and 2%

of general population) a much larger share of respondents (49% among the

general population and 40% among the target audience) either provided a mix of correct

and incorrect answers, chose do not know or most commonly, offered what would

be characterized as a vague response such as specific number/term or

property/house financing. Additionally, 20% of the target audience state

that they dont know what the phrase mortgage term means, demonstrating that

there is potential for discrepancies between the understanding of what a

mortgage term is, what respondents believe is available in Canada, and their

knowledge of what their own mortgage term is.

Figure 5: Understanding of the Phrase Mortgage Term

Q7. What does the phrase mortgage term mean?

Base: All respondents - Target audience (n=2511); General population

(n=2525)

Within

both the target and general populations, consumers with higher levels of

education (e.g., university degree) (high 50s 60 percentage) and higher household

income ($100,000 or greater) (mid 50s- 60% range) are more likely to have a

correct understanding of mortgage term. Amid the target audience, awareness is

higher among those with a fixed term mortgage (63%), lower financial stress

(64%), and among men compared to women (60% vs 56%).

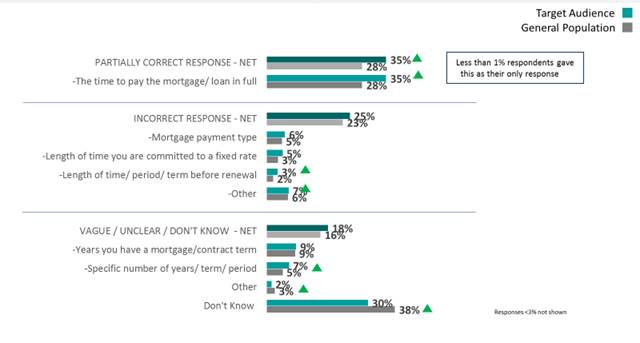

Understanding

of amortization among both the target audience and general population is considerably

weaker than the understanding of mortgage term. In fact, less than 1% of

respondents gave a strictly correct response by saying only that it means the

time to pay the mortgage in full. While approximately a third (35%) of the target

audience and 28% of the general population correctly defined

amortization

period

as the time to pay off a mortgage or loan in full, these

respondents also indicated something that would be characterized as incorrect

or vague. Thus, these individuals might be considered partially correct.

Nearly as

many respondents offered responses that would be characterized as strictly

incorrect. One quarter of the target audience (25%) and 23% of the general

population provided incorrect responses ranging from mortgage payment type (6%)

to the length of time you are committed to a fixed rate (5%), indicating

confusion between the meaning of mortgage term and amortization period. Importantly,

three in ten (30%) in the target audience and almost four in ten (38%) in the

general population do not know what the phrase amortization period means.

Figure

6

: Understanding of the Phrase Amortization

Period

Q11. What does the phrase amortization period mean?

Base: All respondents - Target audience (n=2511); General population

(n=2525)

The above

evidence indicates an important finding: that there is not a strong

understanding of what a mortgage term or an amortization period is among

Canadians. Indeed, there is some confusion between the two within both the target

audience and the general population. This is important context as uptake of a

longer-term mortgage may be predicated on a misunderstanding of mortgage term

and amortization period.

To

mitigate any bias or misunderstanding within the survey, the following

definitions were provided to respondents following their responses to these

unaided awareness questions:

The mortgage term is the length of time a mortgage contract will be in effect. This includes everything the mortgage contract outlines, including the interest rate.

The amortization period is the total length of time it takes to pay off a home in full.

Only four

in ten of the target audience indicate that mortgage terms of greater than 5

years are available in Canada (37%). However, as noted above, many consumers do

not have a correct understanding of mortgage terminology. Therefore, the true

level of awareness of longer-term mortgages in Canada is likely significantly

lower. The survey found that only 7% of the target audience and 6% of the

general population have a correct understanding of the relevant terminology (a

correct understanding of both mortgage term and amortization period) and

indicate that 10-year fixed terms are available in Canada. In total, only 10%

of target audience and 7% among the general population have a correct

understanding of terminology of both term and amortization and believe any

terms greater than 5 years are available in Canada.

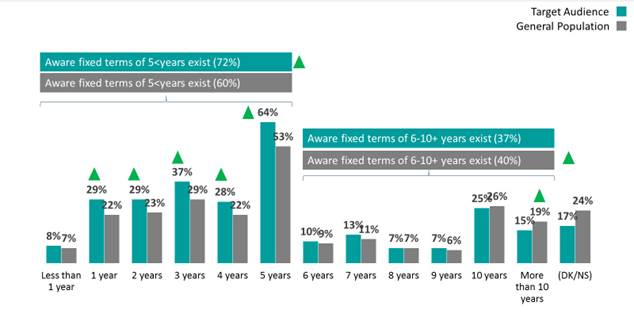

Canadians

are most familiar with 5-year mortgage terms. When asked to indicate the

various mortgage terms they believe are available in Canada, more than half

(64%) of the target audience answered that they are aware of a 5-year mortgage

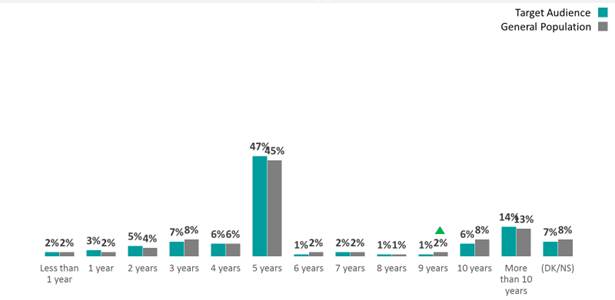

term. Mortgage terms less than 5 years had much lower recognition with a third

of respondents being aware of 4-year terms (28%), 3-year terms (37%), 2-year

terms (29%) and 1-year term (29%). Knowledge is even less strong for mortgage

terms more than 5 years. Only one in ten respondents are aware of a 6-year (10%),

7-year (13%), 8-year (7%), or 9-year (7%) mortgage. There is a greater

recognition of the 10-year mortgage (25%) and mortgage terms greater than 10

years (15%). However, awareness is still low with 75% indicating either a 10-year

mortgage term is not available (58%) or they dont know if it is available (17%).

General

population awareness of terms longer than 5 years is generally consistent with

the target audience (40% vs. 37%), while awareness of 5-year mortgage terms is

lower than the general population (53% vs. 64%). Between a quarter and a third

of the general population are aware of the 4-year (22%), 3-year (29%), 2-year

(23%) and 1-year (22%) mortgage terms. Awareness of the 10-year mortgage fixed

term is 26% among the general population and 19% claim to know mortgage terms

of longer than 10 years are available.

Figure

7

: Aware longer-term fixed mortgage terms are

available

Q8. As far as

you know which of following mortgage terms are available in Canada for

mortgages with a fixed interest rate?

Base: All respondents - Target audience (n=2511); General population

(n=2525)

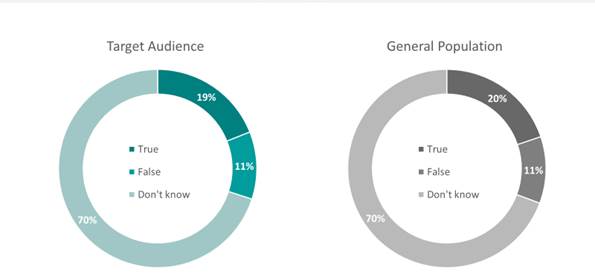

Knowledge of penalties for mortgage terms longer than 5 years is low, with only two in ten in the target audience and the general population respectively answering correctly that the rules regarding penalty fees change after 5 years. Among both the target and general population, 70% stated they do not know whether the rules regarding penalty fees change after 5 years in longer-term mortgages, indicating a low knowledge base and a high degree of uncertainty among Canadians on longer-term mortgages.

Figure

8

: Knowledge of Penalties on Longer-term

Mortgages

Q13. Please

answer True or False based on your knowledge. If you dont know select dont

know. Do not guess. For mortgage terms longer than 5 years, the rules regarding

penalty fees change after 5 years.

Base:

All respondents - Target audience (n=2511); General population (n=2525)

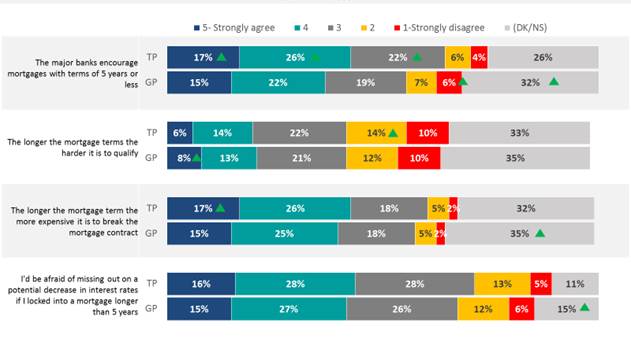

When asked

more directly about mortgage penalties, a large minority of consumers believe

that the longer the mortgage term the more expensive it is to break the

mortgage contract. A total of 43% of the target audience

agreed

with

this statement, with only 7%

disagreeing

. Within the general population,

39%

agreed

that longer mortgage terms are more expensive to break,

while, like the target audience, 7%

disagreed

. In both the target and

general population, a third of respondents stated that they did not know (32% target

audience, 35% general population). This becomes important to decision-making given

that the penalty to break a longer-term mortgage after 5 years is in fact often

consistent with breaking at a 5-year term.

A closer

examination of consumers understanding of mortgage terms provides further

confirmation that consumers know little about the details of longer-term

mortgages and many misunderstand several details. This could create a barrier

to their openness to considering longer-term mortgages.

Among the target

audience, almost half (44%)

agreed

that they would be afraid of missing

out on a potential decrease in interest rates if [they] locked into a mortgage

longer than 5 years, while 18%

disagreed

. Among the general population

41%

agreed

that they feared missing out on rate decreases, while, in the

target audience, 17%

disagreed

.

Figure

9

: Knowledge of Mortgage Terms

Q16. Based on your current understanding of mortgages, do you agree

or disagree with the following?

Base: All respondents - Target audience (n=2511); General population

(n=2525)

Nearly

half of the target audience (42%)

agrees

(rating of 4 or 5) that the

major banks encourage mortgages with terms of 5 years or less, while a quarter

(26%) state that they dont know. Similarly, 36% of the general population

agree

that the major banks encourage mortgages with terms of 5 years or less while

13%

disagree

and a third (32%) do not know.

Notably,

two in ten (21%) in the target audience

agree

that the longer the

mortgage terms the harder it is to qualify. While only slightly more

consumers, one-quarter of the target audience (24%),

disagrees

with this

statement, 33% are unsure. Similarly, two in ten (21%) in the general

population

agree

that longer mortgage terms are harder to qualify for,

while 22%

disagree

. As in the target audience, a third of respondents

are unsure.

There are notable

differences within the population pertaining to these knowledge related

measures. For example, homeowners with a mortgage are more likely to agree that

the major banks encourage mortgages with terms of 5 years or less (45% vs. 36%

in the general population and 30% among those likely to purchase a home in the next

5 years). Younger consumers (under age 45 in both the target and general

population) are more likely to agree that the longer the mortgage terms the

harder it is to qualify (26% vs 16% 45 years+). For both measures as well as

others, men are more likely to agree than women (47% vs 38% women on perception

of banks and 25% vs. 17% women on qualification).

This

section details common sources of mortgage information used by both the target

audience and the general population. Understanding where consumers look for

information will be useful when determining how best to reach consumers with

education about longer-term mortgages and related relevant information about

borrowing decisions.

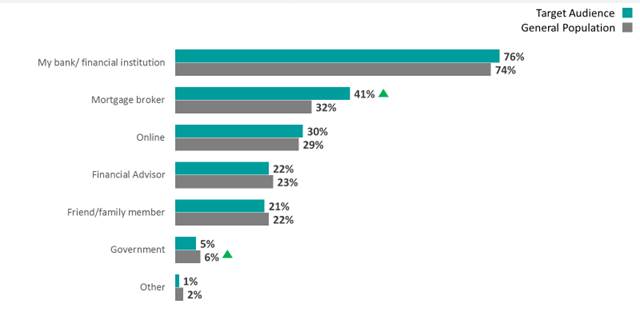

All

respondents were asked where they would obtain information about getting a new

mortgage or renewing an existing mortgage. More than three quarters of the target

audience (76%) say they would seek information from their bank or financial

institution. This was followed by just under half (41%) who say they would ask

a mortgage broker, and a third (30%) who would search online. Among the general

population, three quarters (74%) would look for information from their bank or

financial institution and a third would inquire with their mortgage broker

(32%) or online (29%).

Figure

10

: Obtaining Mortgage Information

Q1. If you

were looking to get a mortgage or renew an existing mortgage, where would you

get your information?

Base:

All respondents - Target audience (n=2511); General population (n=2525)

Those who said

that they would seek information online were asked where online they would look

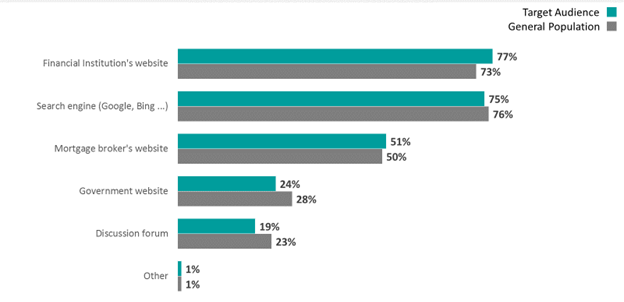

for information. Within the target audience more than three quarters (77%)

would look through their financial institutions website, while three quarters

of the target audience (75%) would look through a search engine like Google or

Bing. Approximately half (51%) would look at their mortgage brokers website.

Among the general population, approximately three quarters (76%) would utilize

a search engine while 73% prefer to go through their financial institutions

website. Consistent with the target audience, half of the general population

(50%) would get information from their mortgage brokers website.

Figure

11

: Obtaining Mortgage Information Online

Q2. Which websites would you go to? Base: Looking for mortgage info

online

Target audience (n=756); General population (n=713)

There are

notable differences within the population groups pertaining to the way consumers

seek out information. When asked how they would get information pertaining to

mortgages, members of the target audience aged 55+ are more likely to contact

their bank or financial institution (83% vs. 76% 45-54, 72% 35-44, 68% 18-34)

while younger target respondents (aged 18-34) are significantly more likely to

seek information from a financial advisor (33% vs. 23% 35-44, 18% 45-54, 15%

55+), friend or family member (34% vs. 22% 35-54, 19% 45-54, 11% 55+), or

through the government (9% vs. 5% 35-54, 2% 45-54, 2% 55+). Within the target

audience, men are significantly more likely to seek information online (33% vs.

28% women), while women are significantly more likely to consult a friend or

family member (23% vs. 19% men).

Within the

general population, Canadians aged 55+ are significantly more likely to consult

a bank or financial institution for information (85% vs. 75% 45-54, 70%

35-54, 63% 18-34). Younger

respondents (18-34) in the general population are more likely to seek

information from a friend or family member (37% vs. 25% 35-44, 17% 45-54, 11%

55+) while respondents under the age of 44 are significantly more likely to

consult a financial advisor (30% 18-34, 25% 35-44 vs. 19% 45-54, 18% 55+). Men

in the general population are more likely to look online for mortgage

information (33% vs. 24% women), while women are more likely to speak with a

financial advisor (26% vs. 20% men), or a friend or family member (24% vs. 19%

men).

This

section details the financial profile of respondents, including their current

mortgage type and term, their remaining loan and amortization, and the amount

of financial stress they are under. This information was captured in the

survey primarily for understanding the extent to which these attributes impact

mortgage term choices.

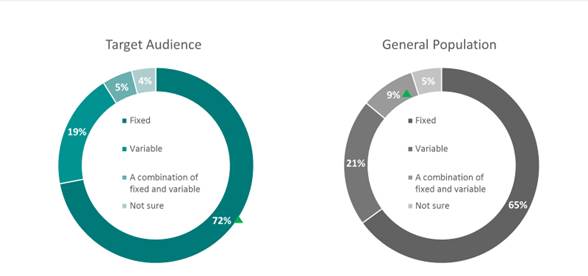

Among those who currently have mortgages in

the target audience, almost three quarters (72%) report having a fixed interest

rate mortgage while two in ten (19%) hold a variable interest rate mortgage. A

much smaller proportion (5%) holds a combination fixed and variable interest

rates. These proportions are similar among the general population of homeowners

as more than six in ten (65%) hold a fixed interest rate mortgage while two in

ten (21%) hold a variable interest rate mortgage. Approximately one in ten (9%)

respondents in the general population claim to hold a combination of fixed and

variable interest rate mortgage.

Figure

12

: Uptake of Fixed vs. Variable Interest

Rate Mortgages

Q3. Does your existing mortgage on your home have

a fixed interest rate or variable interest rate?

Base: Mortgage holders - Target

1 - Target audience (n=2088); General population (n=892)

Within the target audience, older

respondents (aged 55+) are significantly more likely to have a fixed interest

rate mortgage (76% vs. 71% 35-44, 68% 45-54, 68% 18-34) while younger

respondents (aged 18-34) are significantly more likely to have a combination of

fixed and variable (8% vs. 6% 45-54, 4% 35-44, 4% 55+). Respondents within the target

audience who live in the hot housing markets of Vancouver and Toronto are more

likely to have a variable interest rate mortgage (29% vs. 17% other locations).

Within the general population, older respondents (aged 55+) are significantly

more likely to have a fixed interest rate mortgage (74% vs.63% 45-54, 59%

35-54).

Among mortgage holders in the target

audience, half (47%) currently hold a 5-year mortgage. Just over one in ten

(14%) currently hold a mortgage term of more than 10 years while 22% of

homeowners in the target audience have 4 years or less on their current

mortgage. Among the general population, less than half (45%) hold a 5-year mortgage.

One in ten (13%) currently have a mortgage term of more than 10 years, while a

cumulative 21% have 4 years or less on their mortgage.

It is significant to note that the

respondents who answered they currently hold a mortgage term of more than 10

years (14%) is much higher than the data previously collected (outside of this

report) which indicates a number closer to 2%

. This discrepancy can be traced back to the lack of understanding of what amortization and mortgage term means. As noted, 43% of the target audience provided a vague or incorrect answer when asked to define the meaning of mortgage term, while half (51%) of the general population defined mortgage term incorrectly or with a vague response. Furthermore, when asked to define an amortization period, 25% of the target audience defined it incorrectly, with 35% of the target audience providing a definition that while partially correct, was clouded by responses that were vague, indicating the high degree of confusion of the difference between mortgage term and amortization period. Additionally, 20% of the target audience state that they dont know what the phrase mortgage term means, demonstrating that there is potential for discrepancies between the understanding of what a mortgage term is, what respondents believe is available in Canada, and their knowledge of what their own mortgage term is.

Figure

13

: Current Mortgage Term

Info screen before question: Most lenders offer

[mortgage] terms up to 10 years. Q9. What is the total mortgage term on your

current mortgage? By this we mean, the total length of your contract. Your

contract includes the interest rate and the details of the financing for your

home.

Base: Target audience (n=2088); General population

(n=892)

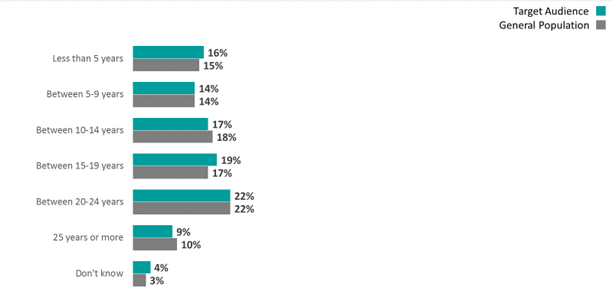

When asked about their remaining

amortization period, the target audience was most likely to say that it will

take between 15-19 years or between 20-24 years to pay off their home in full

(22% and 19% respectively). Nearly as many quote 10-14 years to pay off their

home (17%). The results are very similar among homeowners in the general

population.

Figure

14

: Remaining Amortization

Q12. What is the remaining amortization period on

your current mortgage? In other words, how many years will it take you to pay

off your home in full?

Base: Have a

mortgage - Target audience (n=2088); General population (n=892)

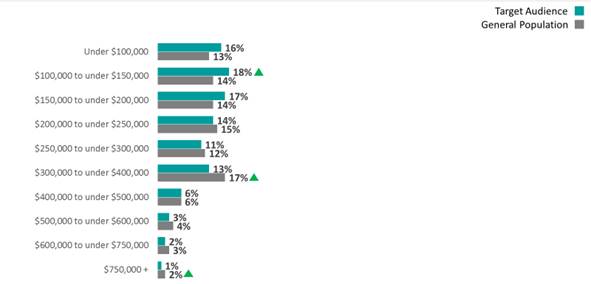

Within the

target audience, two in ten homeowners (18%) stated that their original

mortgage value was between $100,000 to under $150,000 or $150,000 to $200,000

(17%). A smaller portion (12%) had an original mortgage value of $400,000 or

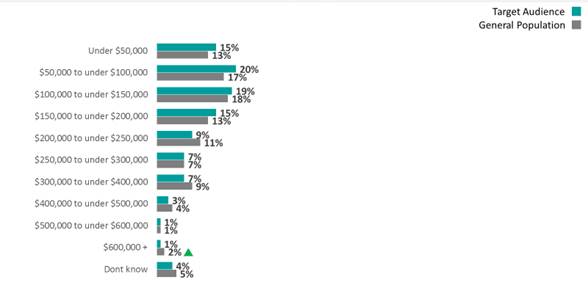

more. When asked what their remaining mortgage loan is, two in ten in the target

audience said there was $50,000 to under $100,000 remaining on their loan (20%)

or $100,000 to under $150,000 remaining on their loan (19%).

Figure

15

: Original Mortgage Value

D5. What was the original value of the mortgage loan on your

home? That is, when you first bought your current home, how much money

did you need to borrow?

Base: Have a mortgage - Target

audience (n=2088); General population (n=892)

Figure

16

: Remaining Mortgage

D6. And what is the approximate amount of money you have left on

your mortgage? Base: Have a mortgage - Target audience (n=2088); General population

(n=892)

In order

to better understand the financial stress that Canadians are under, and how

these stressors impact their mortgage decision-making, including their choice

of mortgage terms, a financial stress variable was created. The variable was

constructed as an aggregate of two variables: one that measures the extent to

which respondents are currently able to cover all their monthly household

expenses, and another measuring their ability to cover an unexpected expense

equal to a months income. The mean or average of the respondents rating

across the variables (dont know responses excluded) was then split into three

categories representing: low financial stress, medium financial stress, high

financial stress.

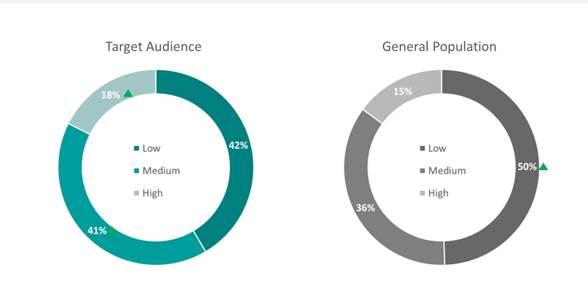

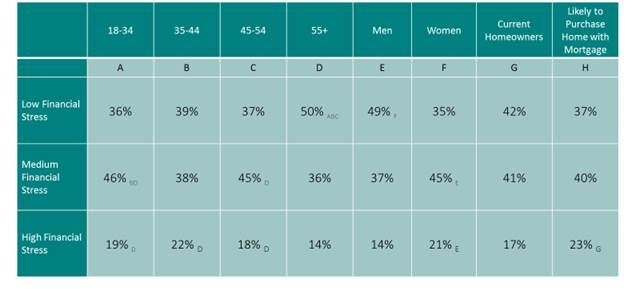

Within the

target audience, there is an even divide as 42% of respondents qualify as low

financial stress while 41% of respondents are medium financial stress. The

remaining 18% of respondents qualify as high financial stress. Contrastingly,

half (50%) of the general population falls under the low financial stress

heading, followed by 36% of the general population who are medium financial

stress. The remaining 15% of the general population are high financial

stress individuals.

Figure

17

: Financial Stress

Financial Stress Variable. Base: Those who

responded to D2 and D3 Target audience (n=2216), General population (n=2085).

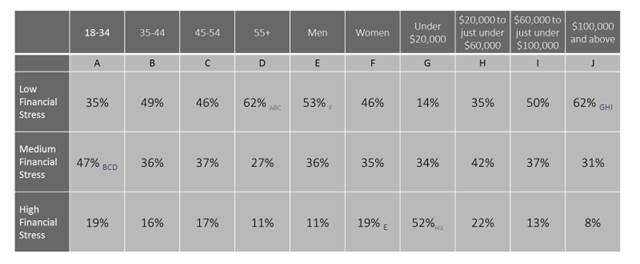

There are significant differences within

each group that correlate to their level of financial stress. Within the target

audience, homeowners and likely homeowners under age 45 are significantly more

likely to have medium and high financial stress, and women are more likely than

men to experience financial stress. Respondents who are

likely

to purchase a home with a mortgage (23% vs. 17% current homeowners with

mortgages) are significantly more likely to be under high financial stress.

Figure

18

: Financial Stress in the Target audience

by Demography

Financial Stress Variable.

Base:

Those who responded to D2 and D3 Target audience (n=2216)

Subscript letters reflect which sub-groups

the shown percentage is statistically significantly higher than.

Additionally, the type of mortgage

correlates to financial stress. Respondents in the target audience who have a

fixed or variable mortgage were significantly more likely to have low financial

stress than those who have a combination fixed/variable (42% fixed, 47%

variable vs. 31% combination). Furthermore, those in the target audience who

have a combination fixed/variable mortgage were more likely to have medium

financial stress (49% combination vs. 41% fixed, 38% variable).

The demographic trends among the general

population are the same as that noted for the target audience (younger, women,

those who want to buy a home). Household income is also a predictably strong

indication of financial stress with those making $100,000 and above more likely

to be low financial stress (62% vs. 50% $60,000 to <$100,000, 35% $20,000 to

<$60,000, 14% <$20,000) and those making less than $20,000 more likely to

be under high financial stress (52% vs 22% $20,000 to <$60,000, 13% $60,000

to <$100,000, 8% $100,000 and above).

Figure

19

: Financial Stress in the General

Population by Demography/Household Income

Financial Stress Variable Base

: Those

who responded to D2 and D3, General population (n=2085).

Subscript letters reflect which sub-groups

the shown percentage is statistically significantly higher than.

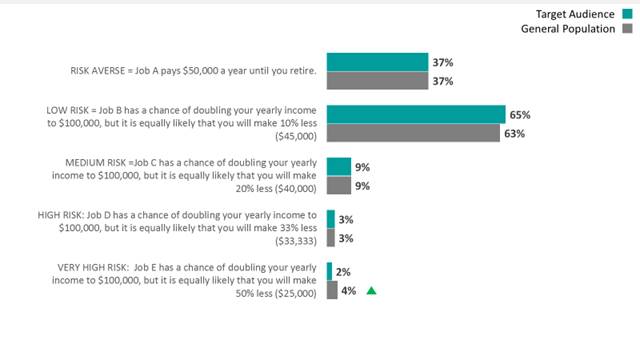

A survey

question was used to assess a respondents propensity to take risks

. This question asked the

respondent whether they would take the risk of losing a portion of their

income, if there was an equal chance of doubling their income. The question was

structured so that the probability of doubling your income or losing a portion

of your income remained constant, and the amount of income you could lose increased.

Therefore, respondents who were more willing to take the chance of losing a

greater portion of their income were deemed risk takers, while those who

selected a constant and fixed wage were deemed risk averse. Respondents were

asked to indicate all the options they would definitely consider

(multi-select).

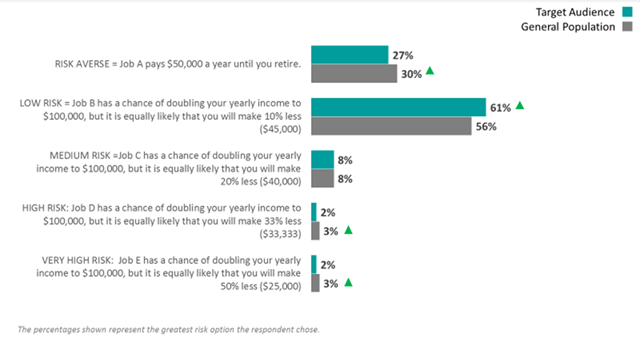

Among the target

audience, four in ten (37%) indicate that the risk averse job description would

definitely be a consideration, selecting that they would choose a constant wage

with no chance to increase their income, but also no risk of losing income. A majority

of homeowners and likely homeowners (65%) indicate they would definitely

consider the low risk job description, as they would take the chance to double

their income, while risking a small amount (10%) of their yearly income. Only

one in ten (13%) in the target audience displayed propensity to risk their

income (risking 20% or more) for the chance to double their income. Please

note: the totals will not add to 100% because respondents were able to indicate

if they would definitely consider more than one job description.

Results

were similar among the general population with four in ten (37%) being risk

averse and six in ten (63%) being low risk. The general population is

significantly more likely than the target audience to take large risks (the

chance to double their income, or lose 50% of their income), however, both

groups have a very small percentage of their population willing to take this

large risk (4% general population vs. 2% target audience).

Figure

20

: Estimate of Risk Aversion

Q18. Please suppose that you currently make $50,000 a year. Next

month you are re-locating and your company is offering 5 jobs to employees like

you. Your new salary will start on your first day and remain the same until you

retire. Please tell us which of these job(s) you will definitely consider.

Base: All respondents - Target audience (n=2511); General population

(n=2525)

In

reviewing the multi-select responses to this question, some potential

inconsistencies were observed (e.g. selecting Job B and D, but not A, C or E).

To manage any potential impact this may have on the use of the variable in

advanced analysis examining the impact of risk aversion on mortgage choice, a

new variable was created that recoded the variable from a multiple select to a

single select. The single selection applied reflects the greatest risk option

the respondent selected. Both the original multi-select and single select

versions were used in analysis. The result was that both versions performed

similarly.

Figure

21

: Risk Aversion (% representing riskiest

option chosen)

Q18. Please suppose that you currently make $50,000 a year. Next

month you are re-locating and your company is offering 5 jobs to employees like

you. Your new salary will start on your first day and remain the same until you

retire. Please tell us which of these job(s) you will definitely consider.

Respondents are allocated to their highest risk option selected. Base: All

respondents - Target audience (n=2511); General population (n=2525)

There are demographic differences

within the population pertaining to risk aversion as measured in the survey.

Perhaps not surprisingly, lower income consumers show more aversion to

risk-taking than those with higher incomes (52% of the general population with

household income under $20,000 demonstrate the lowest risk taking Job A among

their choices, 47% of those with household incomes between $20,000-<$60,000

vs. 33% or fewer among those with household incomes of $60,000 or higher). The

pattern is similar when looking at education levels lower educated consumers

lean toward strong risk aversion. While there is no significant difference

between men and women when it comes to highest level of risk (Jobs E), at each

of the lower risk levels, men demonstrate more openness to risk than women.

For example, 42% of women chose Job A among their choices vs. 32% of men).

There were some slight differences by age, but not a consistent pattern.

This

section investigates the attitudes and opinions Canadians have towards the

future of interest rates and comfort with factors related to longer-term

mortgages.

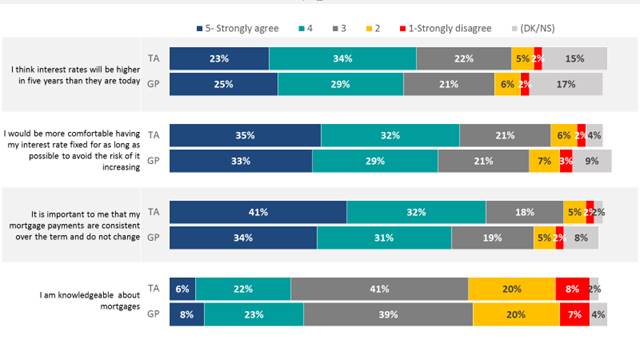

When asked

about the future of interest rates, more than half (57%) of the target audience

stated that they

agree

(responded 4, 5) that interest rates will be

higher in 5 years than they are today. More than two thirds (67%)

agree

that they would be more comfortable having a fixed interest rate for as long as

possible to avoid risks of increases. Among the general population agreement

was similarly strong with half (54%) stating they believe interest rates will

increase and 61% stating that they would prefer a longer fixed rate.

When

considering the consistency of mortgage payments three quarters of the target

audience (73%)

agree

that it was important [to them] that [their]

mortgage payments are consistent over the term and do not change. Two thirds

(66%) of the general population agreed with this same statement. Despite being

sure of their mortgage term preferences and predictions, only a quarter (28%)

of the target audience state that they are knowledgeable about mortgages, while

a third (30%) of the general audience agree that they are knowledgeable.

Figure

22

:

Attitudes

Toward

Factors Relevant to Longer-term Mortgages

Q16. Based on your current understanding of mortgages, do you agree

or disagree with the following?

Base: All respondents - Target

audience (n=2511); General population (n=2525)

There are

significant demographic differences that influence attitudes towards the future

of interest rates. Within the target audience, younger respondents (18-44) are

significantly more likely to

agree

that interest rates will be higher in

5 years (62% 35-44, 60% 18-34 vs. 52% 55+) while older respondents (55+) are

significantly more likely to

agree

they would feel more comfortable

having their interest rates fixed for as long as possible to avoid the risk of

it increasing (72% 55+ vs. 64% 35-44, 64% 45-54, 64% 18-34). Male homeowners or

likely homeowners are more likely to

agree

that interest rates will be

higher in 5 years (61% vs. 53% women), and that they are knowledgeable about

mortgages (36% vs. 21% women) while they are more likely to

disagree

that they would be more comfortable having a fixed interest rate for as long as

possible (10% vs. 8% women) and that it is important to them that their

mortgage payments are consistent over the term (9% vs. 6% women).

Among the

general population, older respondents (45+) are more likely to agree that they

would be comfortable having their interest rate fixed for as long as possible

(69% 55+, 64% 45-54 vs. 54% 35-44, 53% 18-34). Women in the general population

are significantly more likely to feel comfortable if their interest rate were

fixed for as long as possible (64% vs. 59% men), and to

agree

that it is

important that their mortgage payment stay consistent over time (68% vs. 63%

men) while they are more likely to

disagree

that they are knowledgeable

about mortgages (35% vs. 20% men).

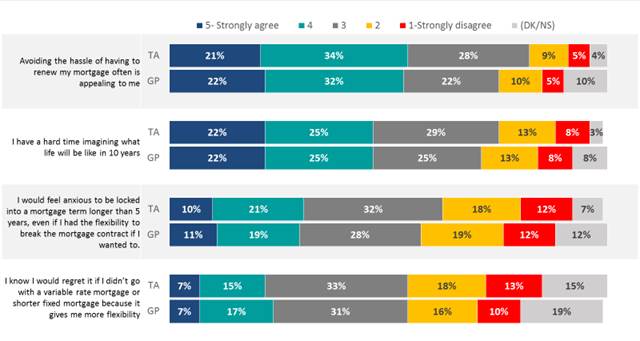

Looking

towards the future brought varying degrees of certainty for Canadians. Half of

the target audience (55%) and the general population (54%)

agree

that

avoiding the hassle of having to renew [their] mortgage often is appealing.

However, half of the target audience and the general population (47%

respectively)

agree

that they have a hard time imagining what life will

be like in 10 years. Consensus is much more divided on longer-term mortgages

as three in ten (31%) homeowners and likely homeowners

agree

that they

would feel anxious to be locked into a mortgage term longer than 5 years, even

with the flexibility to break the contract, while 30% disagree.

Figure

23

: Attitudes Toward Factors Relevant to

Longer-term Mortgages (continued)

Q16. Based on your current understanding of mortgages, do you agree

or disagree with the following?

Base: All respondents - Target audience (n=2511); General population

(n=2525)

Similarly,

30% of the general population agree that they would feel anxious being locked

into a longer-term mortgage, while 31%

disagree

. Further division is

indicated as 22% of the target audience

agrees

that they would regret it

if they didnt go with a variable rate mortgage or a shorter fixed mortgage, as

they give more flexibility, however a third of the target audience disagrees

with this same statement. Among the general population, a quarter (24%),

believe they would regret not choosing a variable rate or shorter fixed

mortgage, while a quarter (26%)

disagree

.

There are

demographic differences within the population pertaining to their attitudes and

opinions. Within the target audience, younger respondents (18-34) are more

likely to

agree

that they would feel anxious being locked into a

mortgage term longer than 5 years (36% vs. 29% 45-54, 28% 55+) and that they

would regret it if they didnt go with a variable mortgage, or a shorter fixed

mortgage, as those options provide flexibility (25% vs. 19% 45-54, 19% 55+). Older

respondents (aged 55+) are significantly more likely to state that avoiding the

hassle of having to renew a mortgage is appealing (58% vs. 53% 18-34, 51%

45-54). Financial stress is also a contributing factor, as those under high

financial stress are more likely to have difficulty imagining what life will be

like in 10 years (55% vs. 48% medium, 43% low).

Within the

general population, younger respondents (18-34) are similarly more likely to

agree

that they would feel anxious being locked into a mortgage term longer than 5

years (35%, 34% 35-54 vs. 25% 55+) and that they would regret it if they didnt

go with a variable mortgage, or a shorter fixed mortgage, as those options

provide flexibility (30% vs. 21% 45-54, 21% 55+). Similar to the target

audience, older respondents (aged 55+) highlighted their interest in avoiding

the hassle of frequently renewing their mortgage (58% vs. 51% 18-34, 49%

35-44).

This

section discusses consumers propensity to consider fixed rate mortgage terms

of 5 years or longer, and the motivations and barriers in such a choice.

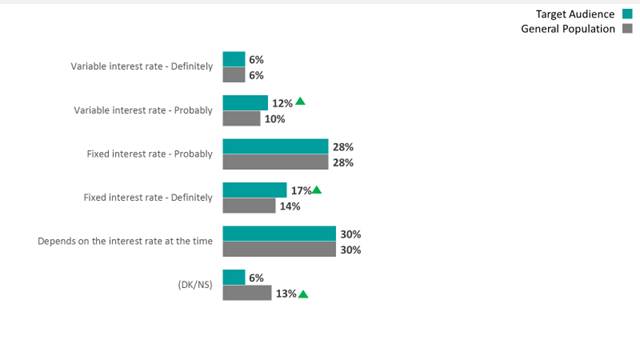

When asked

what type of mortgage they would lean towards when considering either renewing

or applying for a mortgage, almost half (46%) of the target audience would lean

towards a fixed rate mortgage, while 19% lean towards a variable. A further

third (30%) say that it would depend on the interest rate at the time.

Similarly, within the general population 42% lean towards a fixed interest rate

while 16% lean towards a variable interest rate. Notably, the general

population is significantly more likely (13% vs. 6% target audience) to say

that they dont know what type of mortgage they would lean towards.

Figure

24

: Preferences for Fixed or Variable

Mortgage

Q14. [The next time you need to renew your mortgage / If you were

to purchase a home with a mortgage loan] would you lean toward looking at

options for a mortgage with a variable interest rate or a fixed interest rate?

Base: All respondents - Target audience (n=2511); General population (n=2525)

Within the

target audience, a large minority (44%) of homeowners and likely homeowners

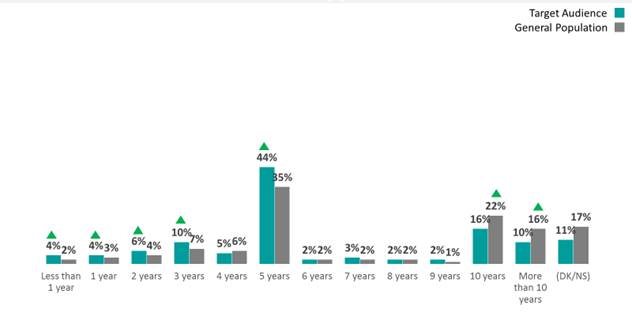

would prefer a 5-year mortgage. This is followed by 16% who would prefer a 10-year

mortgage term. Within the general population, a third (35%) of consumers would

prefer a 5-year mortgage term, while two in ten (22%) would prefer a 10-year

mortgage term. Interestingly, homeowners and likely homeowners are

significantly more likely to prefer terms of 5 years or less, while members of

the general population are significantly more likely to prefer mortgage terms

of 10 years or more.

Figure

25

: Life Stage Suitability

Q10. [The next time you need to renew your mortgage / If you were

to purchase a home and finance it with a mortgage] what mortgage terms would

ideally suit you best, given your life plans and circumstances? Please assume

the same interest rate would apply to any mortgage term.

Base: All respondents - Target audience (n=2511); General population

(n=2525)

Homeowners

with a mortgage were asked how likely they would be to consider a mortgage term

longer than 5 years the next time they need to renew their mortgage. Those who

do not own a home were asked about their consideration of a mortgage term

longer than 5 years if they were to purchase a home that they would finance with

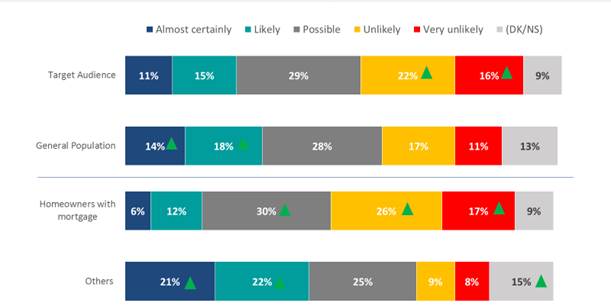

a mortgage. As shown in the chart below, only one in ten indicated that they

would

almost certainly

consider mortgage terms longer than 5 years (11%

among the target audience and 14% among the general population). Slightly more

say they would be

likely

to consider a longer-term mortgage (15% target

audience and 18% general population). Current homeowners with a mortgage

indicate much lower level of interest in longer-term mortgage (6% almost

certain, 12% likely) than others (21% almost certain, 22% likely).

Figure

26

: Stated Likelihood to Consider Longer-Term

Mortgages

Q15. [The next

time you need to renew your mortgage / If you were to purchase a home that you

finance with a mortgage] how likely are you to consider a mortgage term longer

than 5 years?

Base: All respondents - Target

audience (n=2511); General population (n=2525) Homeowners with a mortgage

(n=3093); Others (n=1943)

While the target

and general populations obtain their information about mortgages from similar

sources, homeowners and likely homeowners indicate slightly stronger knowledge

of longer-term mortgages, however, they are unsure of penalty fees associated

with these mortgages and are not strongly interested in them. Within the

general population, despite having slightly less knowledge of longer-term

mortgages and a low understanding of penalty fees, they indicate a stronger

interest in longer-term mortgages, indicating that the general population shows

more receptivity to the potential consideration of a longer-term mortgage. Notably,

these responses do not vary based upon whether the respondents feel that their

life stage makes them more suited to a shorter or longer-term mortgage.

A

conjoint exercise was conducted to supplement consumers stated likelihood in

the question above, by asking consumers to make choices from 3 options offered

at various interest rate levels. This exercise was intended to validate the

qualitative finding that consumers are primarily open to considering a

longer-term mortgage if the interest rate differential between the 5-year fixed

option and 10-year fixed option is 1% or less.

The data

shows that among non-mortgage holders the probability of choosing the 10-year

fixed option dropped significantly when the interest rate was 0.75% higher than

the interest rate offered with 5-year fixed option. When the differential was

0.5% the drop was within the threshold of the statistical error, but at 0.75% the

drop was outside the error margin.

The exercise was also designed to look at the share of

preference or probability of considering the 10-year fixed term option in four

specific interest rates scenarios flat, normal, steep, inverted.

The four scenarios were constructed

to mimic mortgage rate differentials that can be observed under different

economic conditions:

-

In the flat scenario, the mortgage interest rate changes by a small amount as the term

length increases;

-

In the normal

scenario, the mortgage interest rate increases steadily as the term length

increases;

-