Cette publication est aussi disponible en français sous le titre : Étude sur la satisfaction des clients du Service des délégués commerciaux du Canada 2022.

This publication may be reproduced for non-commercial purposes only. Prior written permission must be obtained from Global Affairs Canada. For more information on this report, please contact Public Opinion Research at POR-ROP@international.gc.ca

Catalogue Number:

FR5-160/2022E-PDF

International Standard Book Number (ISBN):

978-0-660-47889-0

Related publications (registration number: 039-22)

Table 3: Variation in Likelihood of Using Services Again

Table 4: Demographic Differences among the Tested Aspects of the TCS Service

Table 5: Demographic Differences in Priority Areas of Need

Table 6: Demographic Differences in Service Outcomes

Table 7: Contribution, Impact and Financial Outcomes of the TCS Services

Table 8: Demographic Differences in Obstacles

Table 9: Demographic Differences in Challenges Related to Export

Table 10: Response Rate Calculation

Table 11: Comparison of Sample with Population and 2019 Sample

List of Charts

Chart 1: Overall Satisfaction, Likelihood to Recommend and Likelihood of Future Use

Chart 2: Reasons for Dissatisfaction

Chart 3: Aspects of the Client Experience with the TCS

Chart 4: Priority Areas of Need among TCS Clients

Chart 5: Activities in Markets where TCS Provided Assistance

Chart 6: Service Outcomes of Interactions with the TCS

Chart 7: Obstacles to Conducting International Trade

Chart 8: Challenges Related to Export Activities

Chart 9: Export Activities to the U.S. and Other Markets

Chart 10: Top 10 National Markets by Total Value of Exports and Growth

Chart 11: Regions by Total Value and by Fastest Growing Export Markets

Chart 12: Initial Source of Awareness of the TCS

Chart 13: Nature and Length of Experience with International Trade

Chart 14: Years of International Business Experience

Chart 15: Current Engagement in International Trade

Summary

A. Background and Objectives

The Trade Commissioner Service (TCS) is a service offered by Global Affairs Canada (GAC) that provides expert advice and support to Canadian businesses on matters related to exploring and growing opportunities in foreign markets, improving access to foreign markets, attracting foreign investment, Canadian Direct Investment Abroad, and innovation. With offices across Canada and its presence in more than 160 cities worldwide, the TCS helps thousands of businesses each year. The Trade Commissioner Service also works with partner organizations such as provincial and municipal governments and industry associations that deliver programs and services to Canadian businesses.

The TCS commissioned Ekos Research Associates to conduct quantitative and qualitative research among its clients. The research was designed to gauge client satisfaction with the TCS and more clearly understand the types of services and information provide by the TCS that clients value.

B. Methodology

Two phases of research were conducted to deliver on the objectives: an initial quantitative phase in which a client satisfaction survey was sent to 2,978 TCS clients, followed by a qualitative phase that involved interviews with 41 key informant interviews survey respondents. The population of TCS clients includes all Canadian companies that sought the services of a Trade Commissioner in Canada or abroad between August 2020 and July 2022 to support their international business development.

Survey

The survey research involved a sample of n=2978 clients of the TCS who were identified through a contact list maintained by the TCS. The survey required an average of 15 minutes to complete and was conducted between November 24 and December 16, 2022. A response rate of 13% was obtained from the initial sample of 26,718. See Appendix A for details related to methodology, response rate calculation and potential for response bias. A margin of error is not applicable since a census of all members of the population was attempted.

Interviews

The qualitative research consisted of one-on-one interviews with 41 survey respondents between December 10, 2020 and February 1, 2023, with five completed in French. Each interview took between 30 and 45 minutes to complete. The questions included in the interview guide were primarily open-ended in nature in order to have the participants clarify key study issues in their own words and drawing on their experiences with the TCS.

It is important for readers to note that interview participants were purposely selected from the sample of respondents to over represent those indicating a lower level of satisfaction with the TCS in order to better understand the nature of dissatisfaction. It is therefore not intended to be a representative balance of the extent of satisfaction or dissatisfaction found in the population of TCS clients.

Please note that while the quantitative data provide a statistically representative means of reporting on the satisfaction and attitudes of clients, the qualitative interviews are a non-random exercise that focuses on discourse and anecdotal experiences which – by design – are not reflective of the entire population.

C. Key Findings

Key findings from the Survey Research

Consistent with past research in 2013 and 2019, the findings of this year's survey research show that a very high proportion of clients are happy with the service and information they have received. Specifically, the results find that:

at least four in five clients (81%) are satisfied with the service and advice provided by the TCS compared with 80% in 2019 and 83% in 2013

82% would definitely or probably recommend the TCS to a colleague compared with 83% in 2019 and 86% in 2013

85% would definitely or probably use the services of the TCS again compared with 85% in 2019 and 86% in 2013

Only 5% of respondents or fewer describe themselves as dissatisfied or say they are unlikely to recommend the TCS or use its services in the future. The primary reasons noted are insufficient value gained and quality of the service provided.

Aspects of the Client Experience

The core aspects of service that clients most often associate with the TCS are

consistent quality of service (78%)

receiving appropriate contacts (i.e., the right people to do business with) (78%)

useful intelligence on market conditions from the TCS (73%)

Positive views about the appropriateness of the contacts provided has increased significantly since 69% in 2019.

Two in three clients (69%) say the TCS provided them with intelligence that helped address problems, up from 62% in 2019.

Reasons for Contacting the TCS

About four in five clients say they need a great deal or at least some assistance with information on local companies or organizations (84%), market intelligence (82%), and referrals to international business opportunities or sales leads (79%). Other areas where most clients say they need assistance include:

recommendations on trade fairs or trade missions (74%)

help with understanding responsible business practices abroad (64%)

referrals to relevant programs and services available to their business (62%)

locating financing (is an area of need identified by 56%)

Half of clients or fewer say they need a great deal or some assistance with advice on planning a trip (52%), referrals to professional service providers (50%), support on intellectual property (IP) rights and dealings with local governments (50%), and referrals to technology or R&D-related partnerships (50%). Although most areas of need are in line with 2019 results, the proportion of clients needing assistance and information on locating financial assistance increased to 56% from 45% in 2019.

Client Outcomes

Other areas of TCS assistance frequently noted are related to exporting goods (35%) and services (28%), as well as with revenue-generating partnerships or joint ventures (27%), up from 22% in 2019.

Clients most often note that assistance provided by the TCS has given them access to market information they would not have otherwise had (63%) and enabled them to expand or explore markets (62%). Only slightly fewer (59%) say it provided them with contacts they would not have otherwise had and improved their knowledge of the competitive environment (56%). Respondents reported that marketing strategy (47%) and profile and credibility (46%) also improved with assistance from the TCS, along with the ability to overcome or avoid barriers to business opportunities (46%).

The most significant TCS contributions noted related to assistance with removing a trade barrier (53%), revenue-generating partnerships (46%) and foreign affiliate sales (43%). Each of these are up from 2019 levels, particularly removal of a barrier (44% in 2019). Significant contributions are also reported with regard to assistance with exporting of services (39%) and of goods (38%), along with the contribution made by assistance with attracting angel investors (36%), licensing of technology (36%), and investment abroad leading to revenue generation (35%). The TCS performance in all of these areas was judged to be much higher than in 2019.

Obstacles and Challenges Related to Export Activities

Significant obstacles to doing business in international markets that were noted by about half of clients are a lack of market contacts (57%), uncertainty of the regulatory environment in other countries (53%), lack of information about international business opportunities (52%), and a lack of access to financing (56%).

Administrative obstacles outside of Canada are a moderate to major challenge in relation to their organization's exporting activities, according to 53% of clients. Similar to 2019, about half of clients indicate that lack of financing or inadequate cash flow (51%) or financial risk (50%) is a challenge. Less than half cite logistical obstacles (45%), market knowledge issues (44%), or foreign border obstacles (43%); the latter two are reported as an obstacle by slightly fewer clients than in 2019. About one in three clients say that intellectual property issues in Canada (34%) or administrative obstacles in Canada (32%) are a challenge; both have also decreased marginally as a challenge from what clients reported in 2019. Among the challenges identified, Canadian border obstacles are a challenge for fewer (28%) clients.

Market Diversification

Two in three clients (65%) say they export goods and services to the United States and to other foreign markets. An additional one in six (16%) say they export goods and services to foreign markets other than the United States. Only 7% export exclusively to the United States.

As in 2019, two in three respondents (66%) identify the United States as first among their three largest export markets, followed by the United Kingdom and China at a distant 21% and 19%, respectively. France (11%), Germany (10%), Mexico (10%), India (9.5%), Japan (9%) and Australia (9%) are all top three markets for roughly one in ten clients.

On a regional basis, the United States is again reported as the largest export market for the greatest number of clients (67%), followed by Western Europe (44%) and East/Southeast Asia (36%). Latin America is the fourth largest region (26%). The United States is most often (53%) identified as the fastest-growing export market over the next three years followed by Western Europe (37%) and East/Southeast Asia (36%).

Key findings from the In-Depth Interview Research

Interactions with the TCS

Above all, TCS clients want support to identify contacts to conduct business internationally, including potential buyers or customers. A few said they look to the TCS for assistance in connecting with these contacts or providing an introduction, along with vetting potential contacts to ensure they are legitimate buyers. Some participants approached the TCS for market intelligence, information about the local business culture or barriers in conducting business in a market. A few participants sought information on regulations in a market. Finally, a few requested help identifying sources of funding and financial assistance.

Participants felt that help understanding the business culture in a target country was the most helpful element of their interaction with the TCS, along with the provision of contacts and the ability of the TCS to make connections and support introductions. Some said that the service was most helpful once they had an established relationship with a Trade Commissioner, or the Trade Commissioner offered strategic advice and follow-up.

Participants offered several areas for improvement, including improving consistency of assistance, responsiveness, and clarifying the priority areas (business size or sector) that the TCS supports. Related to responsiveness, only some said they would consider reaching out to the TCS in a crisis situation. Some felt that information the TCS provided was too general and not specific to their needs. Other gaps include a desire for more guidance to identify sources of funding, or more of the general information provided online.

Other Organizations

Most participants were aware of other organizations that offer comparable information or services as those offered by the TCS. Most often, other federal organizations such as EDC or BDC were mentioned, along with a few mentions of NRC, IRAP, or Statistics Canada. Participants were aware of private sector professionals such as lawyers, financial consultants, brokers, and banks. Provincial trade-focused organizations, federal government support from other markets, professional networks and associations were also mentioned.

Many have used the services or accessed information from at least one of these other organizations. A few noted that other private organizations are expensive; however, they provide more responsive or specialized information. What makes the TCS unique, according to participants, is the extensive presence of the TCS in other markets, market landscape understanding, and the weight of the federal government in making introductions.

Branding

The TCS conjures images of an ambassador or facilitator, and has the ability to make connections for Canadian businesses. For those who are satisfied with the TCS, descriptive words such as "knowledgeable", "insightful", "professional", or "trustworthy" come to mind.

The name of the Trade Commissioner Service itself was straightforward, according to some participants, or they felt that they were used to the name or the naming is unimportant. Particularly, "trade" implies the mandate of the organization, to facilitate trade, although a few said that "export" might be better or they are not in the business of "trade". The term "commissioner" was seen as bureaucratic or government-speak, although a few pointed out that the service is provided by a Trade Commissioner.

TCS Staff

Many participants, notably those who were satisfied with the TCS overall, considered the TCS staff to be professional, asking questions to develop knowledge of their business or sector. Some explained that although staff may be polite and willing to help, the processes themselves were slow or bureaucratic. A few participants noted a consistent turnover of "transient" staff.

Business Challenges During the COVID-19 Pandemic

Most notably, restrictions due to the COVID-19 pandemic resulted in business development challenges. Participants reported they were unable to travel to different markets to attend trade shows or meet with current or potential customers. Sales decreased for some due to changes in consumer behaviour, restrictions, or general uncertainty. Supply chain challenges were experienced by those with tangible products. Increased labour costs were a challenge, along with the ability to attract and retain labour.

Participants implemented various mitigation strategies throughout the pandemic, such as the transition to remote work environments. Others adapted their business model to enhance an online sales strategy, found other business ventures or products that would be profitable during the pandemic, or changed their purchasing model or suppliers.

Although a few businesses indicate they were unaffected by or increased revenue during the pandemic, only a few participants who said they experienced notable challenges indicate that they have fully recovered. Some anticipate continued challenges as they endeavour to recover, with a few small businesses stating they have taken on more debt and may not recover.

Anticipated Challenges

Many challenges are expected by participants over the next five years. Among them are an economic downturn, inflation, higher interest rates, and currency instability. Sourcing capital and financial support is an expected challenge for some, with a few continuing to experience cash flow difficulties due to the pandemic. Supply chain challenges are expected to persist, disrupting manufacturing, delivery delays, and increased cost. Labour shortages are expected to continue, along with the associated increased costs and loss of productivity. A few do not anticipate resuming business travel to the same level as before the pandemic due to increased costs, travel disruption, and lack of efficiency in meetings.

Use of the TCS in the Future

The TCS is considered an important resource for information and service to support international business activities; many inteview participants indicate they intend to continue to seek support from the TCS. Some described the need for more fulsome support to enter a new market, such as an overview of market intelligence, regulatory considerations, cultural knowledge, along with contacts and introductions. A few anticipate seeking support from specific services such as trade missions, funding, or help vetting identified organizations.

D. Note to Readers

Survey

Detailed findings are presented in the sections that follow. Overall survey results are presented in the main portion of the narrative and are typically supported by graphic or tabular presentation of results. Statistically and substantively significant differences between sub-groups of respondents are provided in tables or bulleted text below the main chart or table. If differences are not noted in the report, it can be assumed that they are either not statistically significant[1] in their variation from the overall result or that the difference was deemed to be substantively too small to be noteworthy. Results may not total 100% due to rounding. Similarly, some totals of percentages for two responses may not appear correct due to rounding. The programmed survey instrument can be found in Appendix B.

Interviews

As per section 10.2.3 of Public Services and Procurement Canada's Qualitative Research Standards, "Qualitative research is designed to reveal a rich range of opinions and interpretations rather than to measure what percentage of the target population holds a given opinion. These results must not be used to estimate the numeric proportion or number of individuals in the population who hold a particular opinion because they are not statistically projectable."[2] In order to avoid portraying these results as generalizable to the population, terms such as "a few," "some" and "most" are used to broadly indicate views rather than using specific percentages. To ensure a common understanding of the terms used in the analysis, the following guidelines were used in analyzing and reporting on participant results:

"A few participants" = at least two people but less than 25%;

"Some participants" = 25 to 49%;

"Many participants" = 50 to 75%; and,

"Most participants" = over 75%.

It should also be understood that the information provided by participants is subjective in nature and based on their own recollection, perceptions and information provided by Canadian business representatives. Appendix C provides the recruitment invitation, and Appendix D provides the interview guide.

E. Contract Value

The contract value for the POR project is $126,791.65 (including HST).

F. Political Neutrality Certification

I hereby certify as Senior Officer of Ekos Research Associates Inc. that the deliverables fully comply with the Government of Canada political neutrality requirements outlined in the Policy on Communications and Federal Identity and the Directive on the Management of Communications. Specifically, the deliverables do not include information on electoral voting intentions, political party preferences, standings with the electorate, or ratings of the performance of a political party or its leaders.

Signed by Susan Galley (Vice President)

Detailed Survey Findings

A. TCS Client Satisfaction

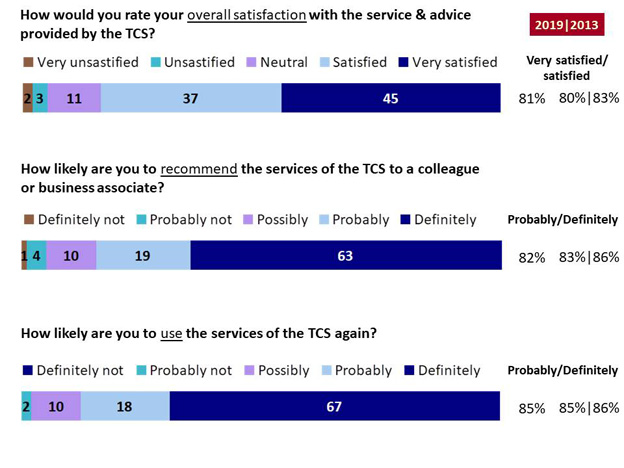

Four in five clients (81%) describe themselves as either very satisfied (45%) or satisfied (37%) with the service and advice provided by the TCS. Similarly, 82% say they would definitely (63%), or probably (19%) recommend the TCS to a colleague, and 85% would definitely (67%) or probably (18%) use the services of the TCS in the future. In each case, 5% or fewer clients describe themselves as dissatisfied or unlikely to recommend or use the services of the TCS in the future . These findings have remained stable since 2013.

Chart 1: Overall Satisfaction, Likelihood to Recommend and Likelihood of Future Use

Chart 1: Overall Satisfaction, Likelihood to Recommend and Likelihood of Future Use - Text Version

Chart 1: Overall Satisfaction, Likelihood to Recommend and Likelihood of Future Use

This stacked chart shows the percentage of results for responses to three questions across different categories. On the side, three columns show the percentage of results for the category ‘'very satisfied/satisfied ET probably/definitely" for 2022, 2019 and 2013.

Respondents were asked: "How would you rate your overall satisfaction with the service & advice provided by the TCS?"

The 2% who would probably not or definitely not use the services of the TCS in the future were most likely to say this was because of insufficient gain from previous interactions (63%) or they were not satisfied with the quality of the service provided (56%). Note: the small sample size of 86 client representatives for this question makes results imprecise.

Chart 2: Reasons for Dissatisfaction

Chart 2: Reasons for Dissatisfaction - Text Version

This chart of single bars shows the percentage of results for responses to seven statements.

Respondents were asked: "Which of the following best describes why you may be unlikely to use the services of the TCS in the future?"

Respondents selected:

Your organization did not gain sufficient value from previous interaction(s): 63%

You were not satisfied with the quality of service previously provided by the TCS: 56%

Your organization has developed to a point where the services provided by the TCS are no longer needed: 10%

You do not know how to get in touch with the right contact in the TCS: 7%

Your organization has not engaged in any new international business endeavors since its last interaction with the TCS: 3%

Other: 3%

Don't know: 2%

Base: All respondents (n=86)

QD4. Which of the following best describes why you may be unlikely to use the services of the TCS in the future?

Base: All respondents (n=86)

B. Factors Contributing to Client Satisfaction

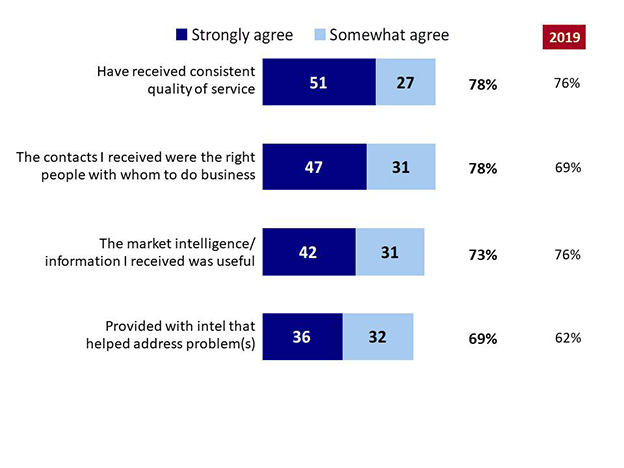

Clients were asked whether they agree or disagree with four statements about some aspects of the service provided by the TCS. Close to eight in ten agree that the TCS provided a consistent quality of service (78%) and that the TCS provided contacts to the right people with whom to do business (78%). Slightly fewer (73%) say they obtained useful intelligence on market conditions. Between 10% and 12% provided a neutral response (not shown in chart). Another 6% to 8% said they disagree with these statements. Results are similar to those found in 2019 with regard to consistency of quality and market information that is useful, although receiving the right contacts is rated more positively than in 2019 (69%).

Just over two in three (69%) clients say the TCS provided them with the information and advice that helped them address the problem(s), although 7% disagree and 16% provided a neutral response. Results are marginally more positive than those in 2019 (62%).

Chart 3: Aspects of the Client Experience with the TCS

Chart 3: Aspects of the Client Experience with the TCS - Text Version

This stacked chart shows the percentage of results for responses to four statements across two categories: strongly agree and somewhat agree. On the side, two columns show the percentage of results for the category "strongly/somewhat agree" for 2022 and 2019.

Respondents were asked: "Please indicate whether you agree or disagree with each of the following statements pertaining to the service you have received from the TCS."

B1A-D. Please indicate whether you agree or disagree with each of the following statements pertaining to the service you have received from the TCS.

Base: All respondents (n=2,978)

The following tables outline the significant differences in agreement among the major demographic subgroups. Partner organizations and large businesses (500 employees or more) are more likely than others to be positive about their experience. Clients in the Atlantic provinces are also more positive with regard to consistency of service and usefulness of the information.

Table 4: Demographic Differences among the Tested Aspects of the TCS Service

Table 4a: Consistent quality of service from all offices and agents (78%)

More likely than average

Less likely than average

Atlantic provinces (85%)

--

Table 4b: Contacts were the right people (78%)

More likely than average

Less likely than average

Partner institutions (84%)

Alberta (72%)

Large organizations (82%)

Planning to export (73%)

Service in 2022 (81%)

--

Education sector (82%)

Responsive sectors (71%)

Target market – East/South Asia (81%)

--

Base: All respondents (n=2965) / % strongly/somewhat agree

Table 4c: Market intelligence was useful (73%)

More likely than average

Less likely than average

Atlantic provinces (81%)

Problem solving (65%) Additional service (68%)

Partner institutions (80%)

Alberta (68%); Quebec (69%)

Large organizations (79%)

--

Education (81%) Cleantech (79%)

Responsive sectors (67%), Information & Communications Technology (67%)

Target market - South/East Asia (76%)

--

Exporting for 10+ years (76%)

--

Base: All respondents (n=2,978) / % strongly/somewhat agree

Table 4d: Information & advice helped address the problem (69%)

More likely than average

Less likely than average

Partner institutions (77%)

TCS service - Prepare for international markets (64%)

Large organizations (74%)

SMEs (67%), under 10 employees (66%)

Education (77%)

Arts & Cultural Industries (59%) Responsive sectors (63%)

Service in 2022 (72%)

--

Base: All respondents (n=2,978) / % strongly/somewhat agree

C. Need for Assistance

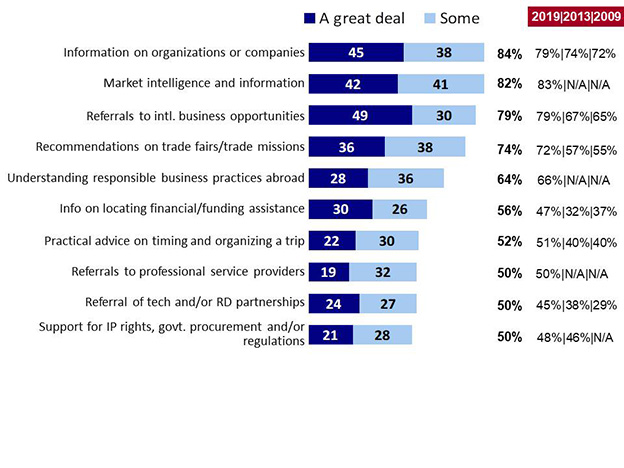

Clients were asked to describe the areas of assistance needed when developing business in markets outside of Canada. About four in five clients indicated their need for a great deal or at least some assistance with information on local companies or organizations of note (84%, an increase from prior surveys), market intelligence (82%, on par with 2019), and referrals to international business opportunities or sales leads (79%).

A second tier of priorities identified by at least six in ten clients as areas where they need a great deal or at least some assistance include recommendations on trade fairs or trade missions (74%) and help understanding responsible business practices abroad (64%). Satisfaction in both areas was similar to 2019 results.

In a third tier, just over half of clients say they need a great deal or some assistance with information on locating financial assistance (56%, an increase from 47% in 2019). Similar to 2019 results, about half report needing practical advice on planning a trip (52%), referrals to professional service providers (50%), referrals to technology or R&D-related partnerships (50%) or support on intellectual property (IP) rights and dealings with local governments (50%).

With the exception of support for intellectual property rights, government procurement and/or regulation, significantly greater proportions of clients said they need assistance than in 2013 or 2009. This pattern was also found in 2019. The only exception where the need for assistance did not vary over time is in obtaining support on IP rights and government regulations. In other area tested where the wording was comparable, clients are considerably more likely to say they need assistance compared to previous research in 2013, and 2009 where applicable.

Chart 4: Priority Areas of Need among TCS Clients

Chart 4: Priority Areas of Need among TCS Clients - Text Version

This stacked chart shows the percentage of results for responses to ten statements across two categories: a great deal and some. On the side, four columns show the percentage of results for the category "a great deal/some" for 2022, 2019, 2013 and 2009.

Respondents were asked: "How much assistance does your organization need in the following areas when developing business in markets outside of Canada?"

Respondents selected:

Information on organizations or companies:

Category "A great deal": 45%

Category "Some": 38%

Category "A great deal/some": 84%; 2019: 79%; 2013: 74%; 2009: 72%

Market intelligence and information:

Category "A great deal": 42%

Category "Some": 41%

Category "A great deal/some": 82%; 2019: 83%; 2013: N/A; 2009: N/A

Referrals to intl. business opportunities:

Category "A great deal": 49%

Category "Some": 30%

Category "A great deal/some": 79%; 2019: 79%; 2013: 67%; 2009: 65%

Recommendations on trade fairs/trade missions:

Category "A great deal": 36%

Category "Some": 38%

Category "A great deal/some": 74%; 2019: 72%; 2013: 57%; 2009: 55%

Understanding responsible business practices abroad:

Category "A great deal": 28%

Category "Some": 36%

Category "A great deal/some": 64%; 2019: 66%; 2013: N/A; 2009: N/A

Info on locating financial/funding assistance:

Category "A great deal": 30%

Category "Some": 26%

Category "A great deal/some": 56%; 2019: 47%; 2013: 32%; 2009: 37%

Practical advice on timing and organizing a trip:

Category "A great deal": 22%

Category "Some": 30%

Category "A great deal/some": 52%; 2019: 51%; 2013: 40%; 2009: 40%

Referrals to professional service providers:

Category "A great deal": 19%

Category "Some": 32%

Category "A great deal/some": 50%; 2019: 50%; 2013: N/A; 2009: N/A

Referral of tech and/or RD partnerships:

Category "A great deal": 24%

Category "Some": 27%

Category "A great deal/some": 50%; 2019: 45%; 2013: 38%; 2009: 29%

Support for IP rights, govt. procurement and/or regulations:

Category "A great deal": 21%

Category "Some": 28%

Category "A great deal/some": 50%; 2019: 48%; 2013: 46%; 2009: N/A

Base: All respondents (n=2,978)

QC1A-J. How much assistance does your organization need in the following areas when

developing business in markets outside of Canada?

Base: All respondents (n=2,978)

The tables below highlight the demographic subgroups significantly more or less likely to say they need a great deal or at least some assistance.

Table 5: Demographic Differences in Priority Areas of Need

Table 5a: Information about organizations or companies in foreign markets (84%)

More likely to need assistance

Less likely to need assistance

--

TCS service - Problem solving (72%)

Cleantech (88%)

Mining (73%)

Base: All respondents (n=2,978) / % some/a great deal

Table 5b: Market intelligence and information on local organizations (82%)

More likely to need assistance

Less likely to need assistance

Atlantic provinces (90%)

TCS service - Problem solving (73%)

Planning to export (88%)

--

Education (89%) Life Sciences (87%)

Mining (73%)

Base: All respondents (n=2,978) / % some/a great deal

Table 5c: Referrals to international business opportunities/sales leads (79%)

More likely to need assistance

Less likely to need assistance

SMEs (82%)

TCS service - Problem solving (64%)

Cleantech (86%) Agriculture and Processed Foods (84%) Information & Communications Technology (83%)

Mining (55%) Education 70%)

Planning to export (86%)

--

Visible minority owned (88%)

--

Base: All respondents (n=2,978) / % some/a great deal

Table 5d: Recommendations on trade fairs/ trade missions to attend (74%)

More likely to need assistance

Less likely to need assistance

Atlantic provinces (82%)

Large organizations (67%)

TCS service – Market potential assessment (78%)

TCS service - Problem solving (59%)

Visible minority owned (83%)

Conducting international business for over 10 years (70%)

Base: All respondents (n=2,978) / % some/a great deal

Table 5e: Understanding responsible business practices in foreign markets (64%)

More likely to need assistance

Less likely to need assistance

Atlantic provinces (74%)

Large organizations (59%)

Agriculture and processed foods (69%)

--

Visible minority owned (73%)

--

Planning to export (72%)

--

Base: All respondents (n=2,978) / % some/a great deal

Table 5f: Information or advice on locating financial/funding assistance (56%)

More likely to need assistance

Less likely to need assistance

SMEs (60%)

Conducting international business for over 10 years (45%)

Arts & cultural industries (79%) Cleantech (66%) Information & Communications Technology, Life Sciences (63%)

Education (30%)

Women owned (72%)

--

Visible minority owned (71%)

--

TCS service - Prep for international markets (64%)

--

Base: All respondents (n=2,978) / % some/a great deal

Table 5g: Practical advice on timing and organizing your business trip (52%)

More likely to need assistance

Less likely to need assistance

Atlantic provinces (64%)

Regularly conducting business in foreign markets (49%)

Partner organizations (62%)

--

Education (66%)

Mining (43%)

Women owned (57%)

--

Visible minority owned (68%)

--

Base: All respondents (n=2,978) / % some/a great deal

Table 5h: Referrals to legal professionals, human resource professionals, translators and other professional service providers (51%)

More likely to need assistance

Less likely to need assistance

Alberta (57%)

Partner organization (40%)

Government/NGO (40%) Education (44%)

Women owned (56%)

Conducting international business for over 10 years (44%)

Visible minority owned (60%)

--

Planning to export (61%)

--

Base: All respondents (n=2,978) / % some/a great deal

Table 5i: Support for the protection of intellectual property rights, government procurement and/or regulatory matters (50%)

More likely to need assistance

Less likely to need assistance

Planning to export (64%)

Large organizations (40%)

Cleantech, Information & Communications Technology (55%)

Education (34%)

Women owned (57%)

Conducting international business for over 10 years (43%)

Visible minority owned (57%)

--

Base: All respondents (n=2,978) / % some/a great deal

Table 5j: Referral of technology and/or RD partnership opportunities (50%)

More likely to need assistance

Less likely to need assistance

Alberta (57%)

TCS service - Problem solving (39%)

TCS service – market potential assessment (55%)

British Columbia (44%)

Life Sciences (67%) Cleantech (59%) Information & Communications Technology (58%)

Agriculture and Processed Foods (39%) Education (44%)

Visible minority owned (62%)

Conducting international business for over 10 years (44%)

Planning to export (65%)

Base: All respondents (n=2,978) / % some/a great deal

D. Client Outcomes

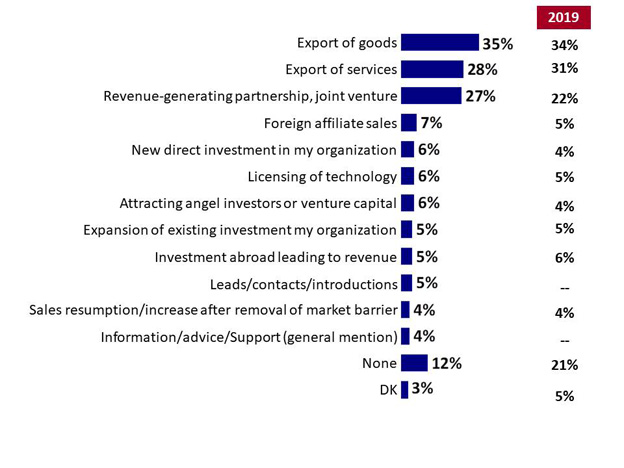

Clients most often report that the TCS provided assistance with exporting goods (35%) or services (28%) or in the development of a revenue-generating partnership or joint venture (27%). Beyond these three major types of activities, fewer than one in ten clients say they received other assistance from the TCS. Just over one in ten (12%) say they have not received assistance or do not know what these services are (3%).

Chart 5: Activities in Markets where the TCS Provided Assistance

Chart 5: Activities in Markets where the TCS Provided Assistance - Text Version

This chart of single bars shows the percentage of results for responses to fourteen statements. On the side, one column shows the percentage of results for 2019.

Respondents were asked: "Which of the following has your organization done in foreign markets where you received assistance from TCS?"

QE2. For which of the following activities in foreign markets has your organization received assistance from the TCS?

Base: All respondents (n=2,978)

Only items with 4% or more shown.

Assistance with exporting goods is more often reported by clients located in the Prairie provinces (47%), the Atlantic provinces (42%) and Quebec (41%), as well as among those requesting assistance with problem solving (43%). It is most prominent in the agriculture and processed foods (67%) and defence/aerospace sectors (50%).

Assistance with exporting services is more often needed among clients in Ontario (31%) and among organizations with five years or less conducting business internationally (35%), as well as in the information & communications technology sector (45%).

Assistance with finding partners/investors is more commonly needed among partner institutions (37%), in the education sector (45%), and among clients receiving market potential assessment information (32%).

Those reporting that they did not receive service are most often in the planning stages (17%), which is also more prevalent in the Prairie provinces (19%) and Alberta (17%). It is highest among those dissatisfied with the services of the TCS (39%).

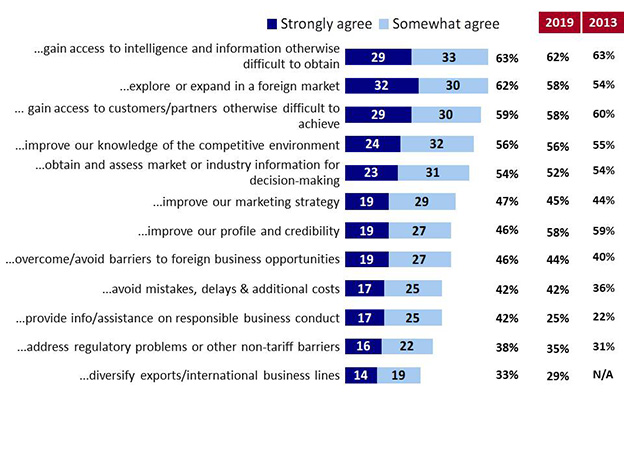

When asked whether the TCS assistance resulted in one of a number of outcomes, six in ten say that the TCS assistance enabled them to explore or expand in a foreign market (63%) and provided intelligence and information they could not have received elsewhere (62%). Slightly fewer say that the TCS assistance provided them with contacts they would not have otherwise found (59%), improved their knowledge about the competitive environment in a market (56%) or gave them market information that supported decision making (54%). Each of these results is on par with 2019 findings, although a slightly higher proportion (63%) note needing assistance with exploration or expansion into a foreign market compared with 58% in 2019.

Just under half of clients say that the TCS assistance enabled them to improve their marketing strategy (47%) or their organizations' profile and credibility (46%) or helped them to overcome a market barrier (46%). Note that in the next section of the report, results illustrate that clients who received assistance with the removal of market barriers were most likely to say that the TCS made a significant contribution.

Just over four in ten respondents say that the TCS assistance enabled them to avoid mistakes, delays or additional costs (42%), or assisted in areas related to corporate social responsibility (42%, up considerably from 25% in 2019.)[5] Slightly fewer clients say that the TCS helped them address regulatory challenges (38%), and one in three report that the TCS helped them diversify their exports or business lines (33%).

Chart 6: Service Outcomes of Interactions with the TCS

Chart 6: Service Outcomes of Interactions with the TCS - Text Version

This stacked chart shows the percentage of results for responses to twelve statements across two categories: strongly agree and somewhat agree. On the side, three columns show the percentage of results for the category "strongly/somewhat agree" for 2022, 2019, and 2013.

Respondents were asked: "Please indicate whether you agree or disagree with each of the following statements. The TCS helped my organization...?"

Respondents selected:

...gain access to intelligence and information otherwise difficult to obtain:

East/Southeast Asia (51%) and Africa and the Middle East (48%) as their top markets

Base: All respondents (n=2,978) / % somewhat agree/strongly agree

Table 6k: Improve ability to address regulatory problems or other non-tariff barriers (38%)

More likely agree

Receiving additional services (45%) or market potential assessment (42%)

Agriculture & Processed Foods (48%)

Partner institutions (44%)

East/Southeast Asia (45%) as their top market

Base: All respondents (n=2,978) / % somewhat agree/strongly agree

Table 6l: Gain confidence to diversify product lines exported or pursued (33%)

More likely agree

Agriculture & Processed Foods (38%)

East/Southeast Asia (41%) as their top market

Base: All respondents (n=2,978) / % somewhat agree/strongly agree

Between one in three and half of clients say the TCS made a considerable to essential contribution in each of the tested activities in markets where they requested assistance. In particular, close to half of clients say that the TCS made considerable or essential contributions by helping to remove market barriers (53%), helping to establish revenue-generating partnerships (46%) and helping with sales through foreign affiliates (43%). More than a third reported a sizable contribution with the export of goods and services (38% and 39%, respectively), attracting investors or venture capital, with information on licensing of technology (36% each), or with investment abroad (35%). Contributions were also reported with new direct investment (31%) and expansion of existing investment in the organization (30%).

Table 7: Contribution of the TCS Services

Activities Where Assistance was Provided

2022

2019

Sales resumption/increase after removal of market barrier (n=134)

Attracting angel investors or venture capital (n=163)

36%

30%

Licensing of technology (n=169)

36%

28%

Investment abroad leading to revenue (n=144)

35%

27%

New direct investment in my organization (n=186)

31%

29%

Expansion of existing investment in my organization (n=146)

30%

31%

Base sizes report the number of respondents saying the TCS provided assistance in each area.

Contribution reports the percentage rating the TCS contribution to each activity as important

or essential (4 or 5 on the scale provided).

Clients with five or fewer years of international business experience are more likely than others to report contributions as a result of the TCS assistance with investment abroad leading to revenue (30%) and attracting direct investment in their organization (28%).

Those in the Atlantic provinces were more likely to report a key contribution as a result of assistance with exporting services (25%) compared with other clients.

E. Obstacles to International Trade

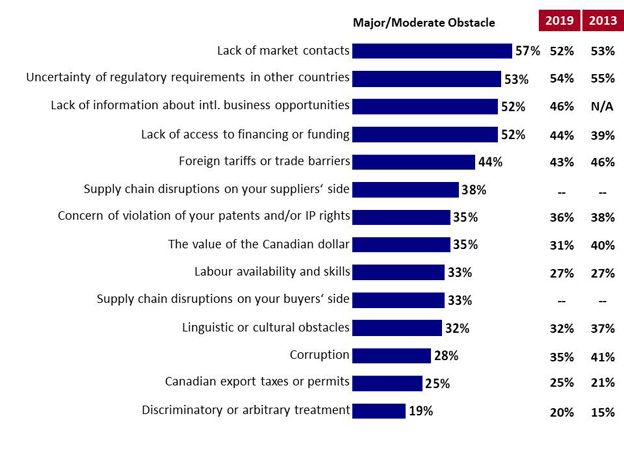

In terms of obstacles to activities in international markets, the most often noted obstacle is a lack of market contacts (57%), up slightly from 2019. Uncertainty about foreign regulatory requirements (53%), a lack of information about international business opportunities (52%) and a lack of access to financing (52%) were also cited by just over half of clients (the latter two activities were noted more often than in 2019, 46% and 44%, respectively). Foreign tariffs or trade barriers were mentioned as obstacles by 44% of clients, similar to previous results.

New to 2022, supply chain disruptions on the supplier side were mentioned by just under four in ten clients (38%). Concerns about violations of patents and intellectual property rights (35%, on par with 2019) and the value of the Canadian dollar (35%) continue to be a challenge for just over one in three. Similarly, one in three clients also noted challenges related to labour availability and skills (33%, listed more often than in 2019 or 2013), supply chain disruptions on the buyer side (33%, new in 2022) and linguistic or cultural obstacles (32%).

About one in four noted corruption (28%, noted less often than in 2019 or 2013) and Canadian export taxes or permits (25%) as major or moderate obstacles in international markets for their organization. This is followed by 19% pointing to discriminatory or arbitrary treatment as an obstacle.

Chart 7: Obstacles to Conducting International Trade

Chart 7: Obstacles to Conducting International Trade - Text Version

This chart of single bars shows the percentage of results for responses to fourteen statements across the category "major/moderate obstacle". On the side, two columns show the percentage of results for "major/moderate obstacle" for 2019 and 2013.

Respondents were asked: "How large of an obstacle are each of the following issues to your organization's activities in international markets?"

Respondents selected:

Lack of market contacts: 57%; 2019: 52%; 2013: 53%

Uncertainty of regulatory requirements in other countries: 53%; 2019: 54%; 2013: 55%

Lack of information about intl. business opportunities: 52%; 2019: 46%; 2013: N/A

Lack of access to financing or funding: 52%; 2019: 44%; 2013: 39%

Foreign tariffs or trade barriers: 44%; 2019: 43%; 2013: 46%

Supply chain disruptions on your suppliers‘ side: 38%; 2019: --; 2013: --

Concern of violation of your patents and/or IP rights: 35%; 2019: 36%; 2013: 38%

The value of the Canadian dollar: 35%; 2019: 31%; 2013: 40%

Labour availability and skills: 33%; 2019: 27%; 2013: 27%

Supply chain disruptions on your buyers‘ side: 33%; 2019: --; 2013: --

Linguistic or cultural obstacles: 32%; 2019: 32%; 2013: 37%

Corruption: 28%; 2019: 35%; 2013: 41%

Canadian export taxes or permits: 25%; 2019: 25%; 2013: 21%

Discriminatory or arbitrary treatment: 19%; 2019: 20%; 2013: 15%

Base: All respondents (n=2,978)

C2A-P. How large of an obstacle are each of the following issues to your organization's activities in international markets?

Base: All respondents (n=2,978)

The following tables show the relative importance of trade obstacles broken down by demographic group.

Table 8: Demographic Differences in Obstacles

Table 8a: Lack of market contacts such as potential buyers and partners technology sources, agents, etc. (57%)

More likely to be an obstacle

Less likely to be an obstacle

TCS service – Preparing for int'l markets (62%)

Large organizations (40%); partner organizations (41%)

Information & Communications Technology (69%) Life Sciences (65%)

Mining (42%) Government/NGOs (44%)

Women owned (67%)

TCS service – Problem solving (41%)

Visible minority owned (73%)

Over 10 years in int'l business (49%)

Plannning to export (71%)

--

Base: All respondents (n=2,978) / % moderate/major obstacle

Table 8b: Uncertainty of regulatory requirements in other countries (53%)

More likely to be an obstacle

Less likely to be an obstacle

Planning to export (58%)

--

SMEs (55%)

--

Agriculture & Processed Foods (67%) Life Sciences (62%)

Education (33%) Arts & Cultural Industries (34%)

Visible minority owned (60%)

Base: All respondents (n=2,978) / % moderate/major obstacle

Table 8c: Lack of information about international business opportunities (52%)

More likely to be an obstacle

Less likely to be an obstacle

Alberta (57%)

Large organizations (32%)

TCS service – Preparing for int'l markets (59%)

TCS service – Problem solving (36%)

Information & Communications Technology (62%)

Education (36%)

Women owned (65%)

Regular business in a foreign market (48%)

Visible minority owned (68%)

--

Base: All respondents (n=2,978) / % moderate/major obstacle

Table 8d: Lack of access to financing or funding (52%)

More likely to be an obstacle

Less likely to be an obstacle

Alberta (61%)

Regular business in a foreign market (46%)

Preparing for international markets (59%)

> 10 years in international business (40%)

Arts & Cultural Industries (73%) Life Sciences (65%) Cleantech (60%) Information & Communications Technology (59%)

Education (36%)

Women owned (69%)

Large organizations (33%)

Visible minority owned (70%)

--

Base: All respondents (n=2,978) / % moderate/major obstacle

Arts & Cultural Industries (10%) Information & Communications Technology (21%)

<6 years in int'l business (23%)

--

Exporting to Latin America & Caribbean (39%), Africa & Middle East (34%)

--

Base: All respondents (n=2,978) / % moderate/major obstacle

Table 8m: Canadian export taxes or permits (25%)

More likely to be an obstacle

Less likely to be an obstacle

Planning to export (31%)

Large organizations (21%)

Defence and Aerospace (43%) Agriculture & Processed Foods (36%)

Education (10%) Information & Communications Technology (18%)

Visible minority owned (30%)

Base: All respondents (n=2,978) / % moderate/major obstacle

Table 8n: Discriminatory or arbitrary treatment towards Canadian investors (19%)

More likely to be an obstacle

Less likely to be an obstacle

Alberta (25%)

--

Oil & Gas (30%)

Base: All respondents (n=2,978) / % moderate/major obstacle

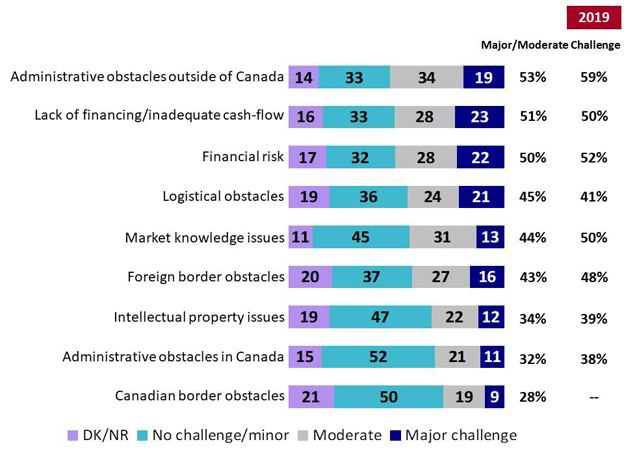

Just over half of the clients say that administrative obstacles outside of Canada (53%, a slight decrease from 59% in 2019) are a moderate to major challenge in relation to their organization's exporting activities. Similar to 2019, about half of clients indicate that lack of financing or inadequate cash flow (51%) or financial risk (50%) is a challenge. Fewer cite logistical obstacles (45%), market knowledge issues (44%, a decrease from 50% in 2019), or foreign border obstacles (43%, down from 48% in 2019). About one in three clients say that intellectual property issues (34%) or administrative obstacles in Canada (32%) are a challenge; fewer respondents identify these as challenges compared with 2019. Although 28% of clients say Canadian border obstacles are a challenge, half (50%) indicate it is no more than a minor challenge.

Chart 8: Challenges Related to Export Activities

Chart 8: Challenges Related to Export Activities - Text Version

This stacked chart shows the percentage of results for responses to nine statements across four categories: DK/NR, no challenge/minor, moderate, and major challenge. On the side, two columns show the percentage of results for the category ‘'major/moderate challenge'' for 2022 and 2019.

Respondents were asked: "How challenging do you consider each of the following issues to be, in relation to your organization's exporting activities? Please rate your view using the scale provided."

F3A-I. How challenging do you consider each of the following issues to be, in relation to your organization's exporting activities? Please rate your view using the scale provided.

Base: All respondents (n=2,978)

Table 9: Demographic Differences of Challenges Related to Export

Table 9a: Administrative obstacles outside of Canada (53%)

More likely to be a challenge

Less likely to be a challenge

Visible minority owned (60%)

Large organizations (46%)

Agriculture & Processed Foods (69%)

Education (42%) Information & Communications Technology (46%)

Base: All respondents (n=2,978) / % moderate/major challenge

Table 9b: Lack of financing/inadequate cash-flow (51%)

More likely to be a challenge

Less likely to be a challenge

TCS service – Preparing for int'l markets (61%)

Large organizations (27%)

Planning to export (71%)

Over 10 years in int'l business (39%)

Arts & Cultural Industries (71%) Life Sciences (65%) Cleantech (65%) Information & Communications Technology (62%)

Information & Communications Technology (20%) Cleantech (23%)

Base: All respondents (n=2,978) / % moderate/major challenge

F. Market Diversification

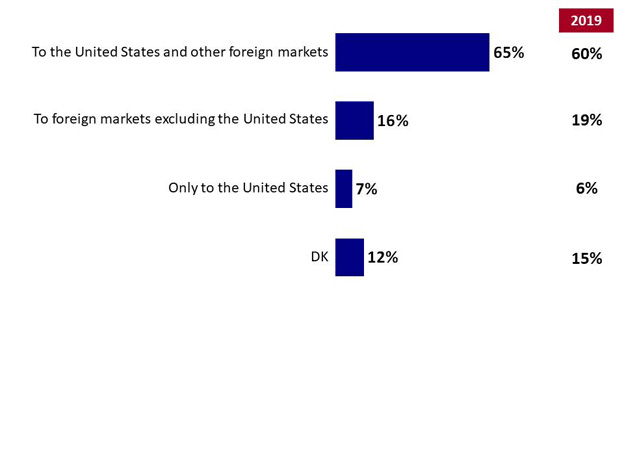

Two in three clients (65%) say they export goods and services to the United States and to other foreign markets, which is marginally higher than in 2019. An additional one in five (16%) say they export goods and services to foreign markets excluding the United States. Fewer than one in 10 (7%) say they export only to the United States, and just over one in 10 (12%) did not know how to answer the question.

Chart 9: Export Activities to the U.S. and Other Markets

Chart 9: Export Activities to the U.S. and Other Markets - Text Version

This chart of single bars shows the percentage of results for responses to four statements. On the side, one column shows the percentage of results for 2019.

Respondents were asked: "Does your organization export goods and services...?"

Respondents selected:

To the United States and other foreign markets: 65%; 2019: 60%

To foreign markets excluding the United States: 16%; 2019: 19%

Only to the United States: 7%; 2019: 6%

DK: 12%; 2019: 15%

Base: All respondents (n=2413)

QF1X. Where does your organization export goods and services?

Base: All respondents (n=2413)

Exporting only to the United States is most likely among those preparing for international markets (12%) and those who have been doing sporadic international business (12%). This is also more prevalent among organizations owned by women (11%), those with five or fewer years of experience with international business and TCS clients located in Alberta (11%).

Organizations exporting to countries outside of the United States are more often targeting Africa or the Middle East (30%), followed by Latin America and the Caribbean (26%) and South and/or East Asia (24%). This is also the case in the education (29%) and agriculture & processed foods (20%) sectors.

When asked to name their organization's three largest export markets, respondents most often identified the United States (66%), followed at a distance by the United Kingdom (21%) and China (19%) as a top market for their organization. France, Germany, Mexico, India and Japan are each noted by roughly one in ten clients as top three markets. Compared with results from 2019, the United States, the United Kingdom and China have risen significantly as key export destinations.

When asked to name the three markets for their organizations' exports which they expect to grow the fastest over the next three years, respondents again identified the United States (52%) as the top market followed by the United Kingdom (19%), China (17%) and India (12%). The United States is considerably more likely to be seen as the fastest-growing market in 2022 compared with 2019 results, as is the United Kingdom, while China is less often mentioned in 2022 compared to 2019.

Chart 10: Top 10 National Markets by Total Value of Exports and Growth

Chart 10: Top 10 National Markets by Total Value of Exports and Growth - Text Version

These two charts of single bars show the percentage of results for responses to eleven (left) and twelve (right) countries. On the side of each chart, one column shows the percentage of results for 2019.

Respondents were asked two questions: "[Left] TOP Markets by Total Value of Exports: What are the largest three markets for your organization in terms of the total value of exports?" AND [Right] TOP Fastest Growing Export Markets: Which three markets do you expect to be the fastest growing for your exports over the next three years?

Respondents selected: [Left]

United States: 66%; 2019: 60%

United Kingdom: 21%; 2019: 16%

China: 19%; 2019: 26%

France: 11%; 2019: 9%

Germany: 10%; 2019: 9%

Mexico: 10%; 2019: 10%

India: 9%; 2019: 9%

Australia: 9%; 2019: 10%

Japan: 9%; 2019: 9%

United Arab Emirates: 5%; 2019: --

Brazil: 5%; 2019: 5%

Respondents selected: [Right]

United States: 52%; 2019: 43%

United Kingdom: 19%; 2019: 13%

China: 17%; 2019: 26%

India: 12%; 2019: 13%

Germany: 10%; 2019: 9%

Mexico: 10%; 2019: 12%

Japan: 10%; 2019: 9%

France: 9%; 2019: 7%

Australia: 9%; 2019: 8%

Brazil: 8%; 2019: 8%

South Korea: 7%; 2019: --

United Arab Emirates: 6%; 2019: --

Base: Respondents who do international business outside of the U.S. (n=998)

Base: Respondents who do international business outside of the U.S. (n=2332)

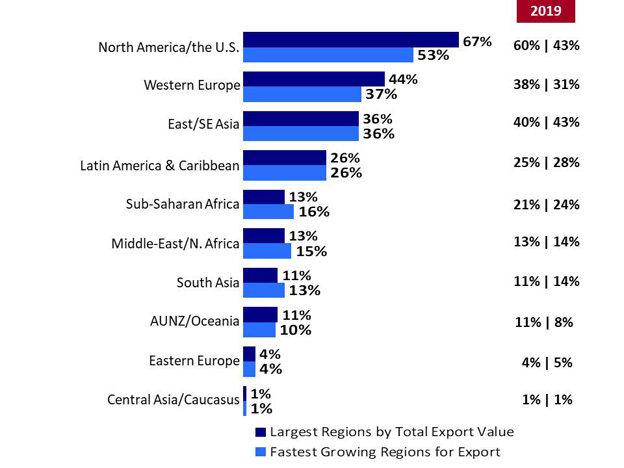

The following chart provides a regional summary of results for the largest current markets and those expected to grow the fastest in the next three years. Since Mexico has been included as part of Latin America for this survey, the result for North America is only for the United States.[9] As such, North America is considered by 67% as the largest region for current exports, up from 60% in 2019. North America is also expected to be the fastest-growing market over the next three years, according to 53% (also up from 2019). North America and Western Europe, with the oldest and best-established trading relationships with Canada, are the only regional markets where the proportion of respondents identifying these as the fastest-growing markets is lower than the proportion that identify them as top current markets. This pattern mirrors 2019 results, although the sub-Saharan region is less prominent among TCS clients in terms of size and extent to which it is perceived as a growing market compared with 2019.

Chart 11: Regions by Total Value and by Fastest Growing Export Markets

Chart 11: Regions by Total Value and by Fastest Growing Export Markets - Text Version

This chart of double bars shows the percentage of results for responses to ten countries across two categories "largest regions by total export value" and "fastest growing regions for export". On the side, two columns show the percentage of results for each category for 2019.

Respondents were asked two questions: "Largest Regions by Value of Exports: What are the largest three markets for your organization in terms of the total value of exports? (n=1951; currently exporting) AND Fastest Growing Regions for Exports: Which three markets do you expect to be the fastest growing for your exports over the next three years?"

Respondents selected:

North America/the U.S.:

Largest regions by total export value: 67%; 2019: 60%

Fastest growing regions for export: 53%; 2019: 43%

Western Europe:

Largest regions by total export value: 44%; 2019: 38%

Fastest growing regions for export: 37%; 2019: 31%

East/SE Asia:

Largest regions by total export value: 36%; 2019: 40%

Fastest growing regions for export: 36%; 2019: 43%

Latin America & Caribbean:

Largest regions by total export value: 26%; 2019: 25%

Fastest growing regions for export: 26%; 2019: 28%

Sub-Saharan Africa:

Largest regions by total export value: 13%; 2019: 21%

Fastest growing regions for export: 16%; 2019: 24%

Middle-East/N. Africa:

Largest regions by total export value: 13%; 2019: 13%

Fastest growing regions for export: 15%; 2019: 14%

South Asia:

Largest regions by total export value: 11%; 2019: 11%

Fastest growing regions for export: 13%; 2019: 14%

AUNZ/Oceania:

Largest regions by total export value: 11%; 2019: 11%

Fastest growing regions for export: 10%; 2019: 8%

Eastern Europe:

Largest regions by total export value: 4%; 2019: 4%

Fastest growing regions for export: 4%; 2019: 5%

Central Asia/Caucasus:

Largest regions by total export value: 1%; 2019: 1%

Fastest growing regions for export: 1%; 2019: 1%

Base: Respondents who do international business outside of the U.S. (n=1325; subset of those currently exporting)

QPF1. Largest Regions by Value of Exports: What are the largest three markets for your organization in terms of the total value of exports? (n=1951; currently exporting)

Fastest Growing Regions for Exports: Which three markets do you expect to be the fastest-growing for your exports over the next three years?

Base: Respondents who do international business outside of the U.S. (n=1325; subset of those currently exporting)

G. Learning About TCS Services

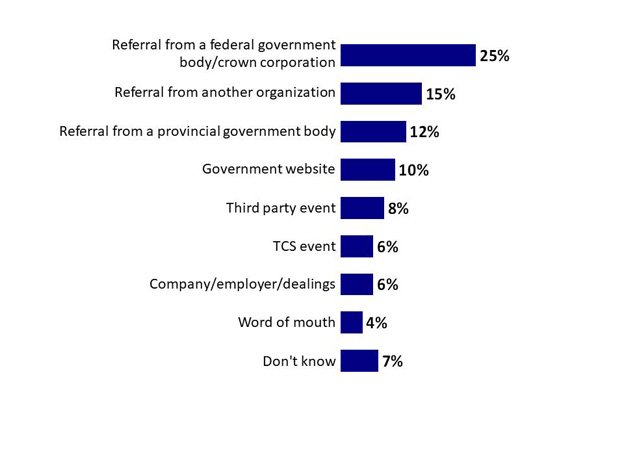

When asked how they initially learned about the TCS, respondents most often say they were referred by another federal government body or Crown corporation (25%), followed by referrals from a provincial government body (12%) or another organization (15%). Another 10% learned about the TCS on a government website, 8% attended a third-party event and 6% learned from an event organized by the TCS. A further 10% learned about the TCS through another company or employer or they have had dealings with the TCS in the past (6%) or through word of mouth (4%).

Chart 12: Initial Source of Awareness of the TCS

Chart 12: Initial Source of Awareness of the TCS - Text Version

This chart of single bars shows the percentage of results for responses to nine statements.

Respondents were asked: "How did you initially learn about the Trade Commissioner Service (or TCS)?"

Respondents selected:

Referral from a federal government body/crown corporation: 25%

Referral from another organization: 15%

Referral from a provincial government body: 12%

Government website: 10%

Third party event: 8%

TCS event: 6%

Company/employer/dealings: 6%

Word of mouth: 4%

Don't know: 7%

Base: All respondents (n=2,978)

Only items with 3% or more shown.

QA1. How did you initially learn about the Trade Commissioner Service (TCS)?

Base: All respondents (n=2,978)

Only items with 3% or more shown.

Referral from a provincial government body is more likely in the Atlantic provinces (23%) or Alberta, Manitoba or Saskatchewan (18%), as well as in the agriculture & processed foods sector (21%).

SMEs are more likely than larger organizations or partner institutions to have learned about the TCS through a referral by a provincial organization (13%) or another organization (15%).

Businesses owned by women are also more likely than other organizations to have received a referral from an organization outside of the federal government or a Crown corporation (18%).

H. Experience With and Activities in International Trade

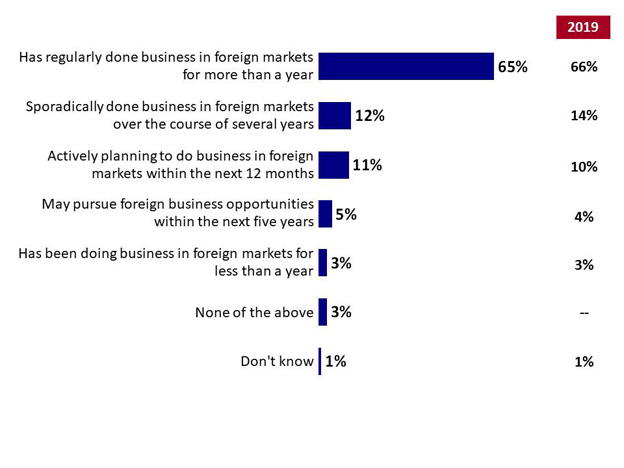

About two in three clients say their organization has done business abroad for over a year (65%). An additional 12% say they have only sporadically done business abroad. One in five respondents overall (19%) describe their organization as relatively inexperienced with international trade, saying either that they plan to do business abroad within a year (11%), that they are considering doing so within five years (5%), or that they have been doing business abroad for less than one year (3%). These results are similar to those in 2019.

Chart 13: Nature and Length of Experience with International Trade

Chart 13: Nature and Length of Experience with International Trade - Text Version

This chart of single bars shows the percentage of results for responses to seven statements. On the side, one column shows the percentage of results for 2019.

Respondents were asked: "Which of the following statements best describes your organization?"

Respondents selected:

Has regularly done business in foreign markets for more than a year: 65%; 2019: 66%

Sporadically done business in foreign markets over the course of several years: 12%; 2019: 14%

Actively planning to do business in foreign markets within the next 12 months: 11%; 2019: 10%

May pursue foreign business opportunities within the next five years: 5%; 2019: 4%

Has been doing business in foreign markets for less than a year: 3%; 2019: 3%

None of the above: 3%; 2019: --

Don't know: 1%; 2019: 1%

Base: All respondents (n=2,978)

QA2. Which of the following statements best describes your organization?

Base: All respondents (n=2,978)

Businesses owned by those self-identifying as Indigenous (26%), a visible minority (21%), or women (20%) are more likely than other organizations to be actively planning to do business in foreign markets within the next 12 months. This is also more often the case in the life sciences sector (21%) than in other sectors.

Those most likely to have done regular business in foreign markets are in the defence and aerospace (81%) and education sectors (75%).

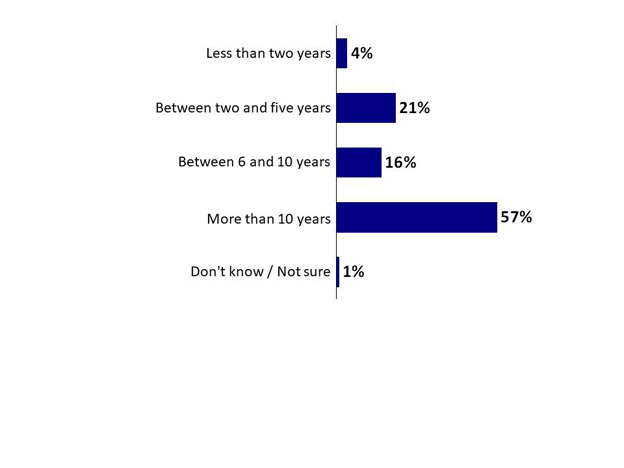

More than half of clients have done business internationally for more than 10 years (57%). Only 4% of those currently doing business internationally have less than two years of experience in this area.

Chart 14: Years of International Business Experience

Chart 14: Years of International Business Experience - Text Version

This chart of single bars shows the percentage of results for responses to five statements.

Respondents were asked: "How many years has your organization done business internationally?"

Respondents selected:

Less than two years: 4%

Between two and five years: 21%

Between 6 and 10 years: 16%

More than 10 years: 57%

Don't know/Not sure: 1%

Base: All respondents (n=2,315)

QA3. How many years has your organization done business internationally?

Base: All respondents (n=2315)

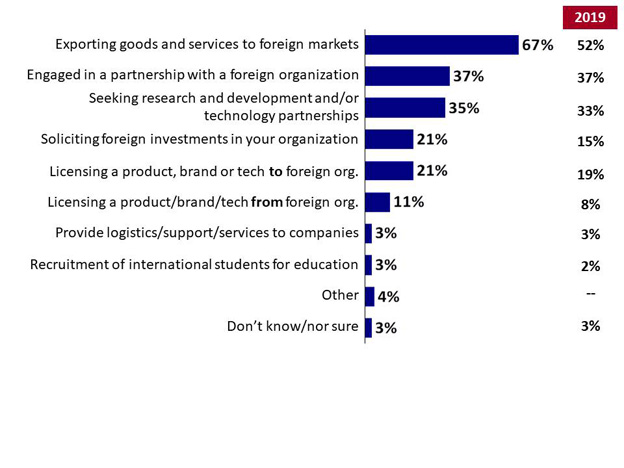

When asked what activities they are currently engaged in abroad, clients most often say they are exporting goods and services (67%) to foreign markets. Just over one in three say they are engaged in partnerships with foreign organizations (37%) or are seeking R&D or other technology partnerships (35%). About one in five (21%) are seeking project financing or venture capital, or licensing a product, brand or technology to a foreign organization, while 11% are licensing a product, brand or technology from a foreign organization.

Results are similar to those found in 2019 although there is a somewhat larger proportion currently soliciting foreign investment.

Chart 15: Current Engagement in International Trade

Chart 15: Current Engagement in International Trade - Text Version

This chart of single bars shows the percentage of results for responses to ten statements. On the side, one column shows the percentage of results for 2019.

Respondents were asked: "Is your organization currently engaged in any of the following activities?"

Respondents selected:

Exporting goods and services to foreign markets: 67%; 2019: 52%

Engaged in a partnership with a foreign organization: 37%; 2019: 37%

Seeking research and development and/or technology partnerships: 35%; 2019: 33%

Soliciting foreign investments in your organization: 21%; 2019: 15%

Licensing a product, brand or tech to foreign org.: 21%; 2019: 19%

Licensing a product/brand/tech from foreign org.: 11%; 2019: 8%

Provide logistics/support/services to companies: 3%; 2019: 3%

Recruitment of international students for education: 1%; 2019: 2%

Other: 4%; 2019: --

Don't know/nor sure: 3%; 2019: 3%

Base: All respondents (n=2,978)

Only items with 3% or more shown

QA4. Is your organization currently engaged in any of the following activities?

Base: All respondents (n=2,978)

Only items with 3% or more shown.

Detailed Interview Findings

A. Interactions With TCS

Types of service requests

Interview participants were first asked to describe their last interaction with the TCS to provide context for the further discussion of how well the service worked for them, the most positive elements of the service and areas where they believe improvements are needed. While the 41 interview participants described various interactions, the type of service they requested generally fell under a few main areas.

Contacts and introductions

Many participants approached the TCS for suggestions about appropriate local buyers and, in a few cases, local investors or suppliers. A few asked the TCS to introduce them to potential clients, while a few others did their own research but wanted help from the TCS in doing some advanced research to vet potential contacts as legitimate buyers. A few were looking for strategic advice, guidance or recommendations from TCS staff about which contacts to pursue.

We were asking about financiers in Singapore to see if they had the capacity to be investors on a [sector] project there.

[The TCS] helped us arrange the meetings (business matchmaking) for the in-person, including prospective clients and also potential partners who could sell our software in Japan.

We felt it would be valuable to have local contacts to take the product to market.

At first I was asking about expansion into the U.S., the U.K., the EU and Japan. I was looking for contacts, but also a better understanding of the business landscape (what to do, how to enter, what areas, steps to follow).

There are a couple of companies in the Middle East we are interested in, and we knew that the only way to do that is in a guided way, to be introduced.

A few participants spoke about their participation in trade missions or trade shows. In some cases these events were put on by the TCS, and in other cases the TCS was attending or supporting them in their own events or the events of other organizations. They spoke of these events as important opportunities for visibility in order to connect with potential buyers and suppliers in target countries. A few of these individuals talked about the value of being introduced by the TCS at these events.

It was very successful. It was one of our biggest lead-generation events. Our team member was there for 2 weeks just taking meetings and follow-up.

[The TCS] engaged with our marketing team to produce events.

We were part of the [...] Show and there was a TCS matchmaking service that we used to try and meet international delegates who are buyers of services and products like ours.

Market intelligence and information on cultural business landscape

Some participants said they approached the TCS for market intelligence regarding their potential to be competitive in specific countries. A few others were looking for more general information about the local business culture and how things are done in a certain country, and possible barriers to moving forward in a market.

We needed to understand what the requirements were with the market.

Helping us do landscape mapping to understand the market.

[Working on a project expansion and] I needed to understand a few things, such as market size. I needed cultural contexts and habits in terms of consuming natural health products.

We often use them [the TCS] for insight into a country and how they do things (the business culture). They advise you on how to do things and how to communicate/not communicate, what timing would work best or what steps to take in what order.

Specific information related to rules and regulations

A few participants were looking for information about regulations in specific areas of target markets. Two participants were looking to the TCS for support in negotiations or litigations with parties in foreign countries.

[The TCS] helped us arrange a meeting with the federal money laundering watchdog.

I approached the TCS about an issue of payment from a large utilities company in [country], involving a sub-contractor.

Assistance or advice regarding funding

A few participants approached the TCS to ask about sources of funding or were looking for guidance about eligibility and the application process for CanExport.

Most helpful elements

Among those satisfied with their most recent interaction with the TCS, interview participants described a range of positive aspects of the service as particularly helpful. A theme often noted related to understanding the business culture in a target country. This included information on how to navigate the process and cultural norms within a market.

They know who to go to, know how to navigate the system.

Understanding of how these countries work [cultural approaches]. This was necessary to be able to close a contract. I could understand the speed at which things will operate and how international opportunities present themselves in those markets.

It was understanding the culture. Every country has its own culture and you have to know how do we respect it? How do they respect ours? It's important, getting that communication first in order to open doors and begin the relationship.

A second service that participants found to be useful is the provision of contacts and ability to help clients make local connections, open doors and support introductions. This includes the ability to "vet" organizations as identified by the participant, or make "warm" introductions to an organization in the market. Two participants talked about the value of having the TCS presence as "boots on the ground" in the foreign country or representation by the Government of Canada.

It was really helpful just getting the background and local introductions. We were face-to-face with prospective customers.

Developing contacts in the U.S. market. We received lists of people who could be potential clients for us. The TCS staff member helped us develop a client network in the U.S.

[We received information on] good match contacts for potential clients and partners. They helped set up meetings and did some advance work, which was very thorough. Giving us information about the contacts in advance was very useful for our business team to plan ahead of time.

[Information on] where people in the sector go, to learn the state of the industry. Key events in market. Help me whittle down where I have the best chance of meeting the people.

They represent Canada. We can't hop on a flight every problem we have. They are our voice sometimes.

Some participants found the level of engagement and commitment of the Trade Commissioner they were dealing with to be helpful. A few spoke of their keen interest, additional research and follow-up Trade Commissioner. A few spoke about the strategic advice they offered and the trust they earned.

The Trade Commissioner was very engaged and willing to assist. He took the time to understand what I was telling him and what the market looked like. Afterwards he did his own research. It resulted in two fairly targeted referrals. Having that engagement resulted in better information and referral. I felt like I had a strategic advisor on the ground in-country, who was looking out for me. That builds trust and confidence.

The TCS in Ontario was very strong on content, very effective in communication and very helpful. I was very pleased with the level of knowledge and expertise. It was as if you were talking to a real content expert.

The contact I have in Manitoba [...] linked me up with the right people and forwarded information about seminars, workshops. I'm in the loop. He updates me. This is a great help.

I've requested some custom solutions and I've always been satisfied with what I got. I feel they went the extra mile to respond to our needs.

A few participants felt that the TCS provided specific market intelligence related to the sector or advice on trade shows or other events to attend in order to connect with the most relevant contacts.

Understanding the market dynamics. How are the products sold. The criteria for success because it's one thing to export but it's an investment and risk to take. What is our pricing, messaging and product offering. I wanted to know what are the best-selling products and the brands and messaging from the competitors. [The TCS] gave us insights to [help us] prepare an offering to meet with buyers.

The most interesting stuff from the TCS is the resources that help provide insightful market research, reports on the [...] market and the [sub] sector. [More recent material] provided some separation [of specific sub-sectors] and that's where the value got more interesting.

[We received] a thorough analysis of the local marketplace, HR availability, salary comparison report, education institutions, finance options. It was very comprehensive, and gave us a good understanding of how we could set up our business from a technological standpoint.

Two participants spoke about the information they received that helped them with decision making:

I think they did as much as they could, and it helped me make the right decisions.

[The TCS] told us about a number of programs. We didn't get involved in any of those programs, but it did help us see the direction we should be going when we get big enough to be eligible for them.

Among those indicating dissatisfaction with their most recent services from the TCS, there was limited descriptions of elements that were particularly helpful. Many described what they would like to receive, which are outlined in the next section on additional needs and gaps. A few areas relate to being connected with local sources and networks and inclusion in social events that afforded opportunities to speak with local contacts. One noted the value of the TCS newsletter.

There have been social functions and networking functions that have been helpful. They got all the Canadians together at a dinner and people started working together that way.