Final Report

Prepared for Natural Resources Canada

Supplier Name: Phoenix SPI

Contract Number: CW2239573

Award Date: 2022-09-07

Contract Value: $78,553.08 (including applicable taxes)

Delivery Date: 2023-01-24

Registration Number: POR # 042-22

For more information, please contact: nrcan.por-rop.rncan@canada.ca

Ce rapport est aussi disponible en français.

This public opinion research report presents the results of a 15-minute telephone survey of 300 representatives of the Canadian freight transportation industry who were involved in or knowledgeable about the management or implementation of trucking fuel efficiency programs and policies within the business' fleet of vehicles. The fieldwork was conducted from October 24 to November 14, 2022.

Permission to Reproduce

The information in this publication may be reproduced, in part or in whole and by any means, without charge or further permission from Natural Resources Canada, provided that due diligence is exercised in ensuring the accuracy of the information reproduced; that Natural Resources Canada is identified as the source institution; and that the reproduction is not represented as an official version of the information reproduced or as having been made in affiliation with, or with the endorsement of Natural Resources Canada. For more information on this report, please contact Natural Resources Canada at: nrcan.por-rop.rncan@canada.ca.

Catalogue number: M144-321/2023E-PDF

International Standard Book Number (ISBN): 978-0-660-47397-0

Cette publication est aussi disponible en français sous le titre : 2022-2023 : Sondage des programmes de transport de marchandises éco-énergétiques sur l’industrie du transport de marchandises

Related Publication (Registration Number: POR 042-22):

Catalogue number: M144-321/2023F-PDF

ISBN: 978-0-660-47398-7

© His Majesty the King in Right of Canada, as represented by the Minister of Natural Resources, 2023

The department of Natural Resources Canada (NRCan) commissioned Phoenix Strategic Perspectives (Phoenix SPI) to conduct survey research to assess Freight Transportation Medium and Heavy-duty Vehicle (MHDV) industry awareness and uptake of Zero Emission Vehicles (ZEVs) and Retrofits.

The Greening Freight Programs (SmartWay, SmartDriver and the Green Freight Program) are three programs that provide training, tools, and resources to help Canada's fleets lower fuel consumption, operating costs, and harmful vehicle emissions. The purpose of the research was to assess perspectives on reducing fuel use and improving energy efficiency in freight transportation among the MDHV industry.

The specific research objectives included:

The results of this research will be used to: 1) enhance NRCan's understanding of inflection points and potential federal funding assistance needs to increase the uptake of ZEV purchases and retrofits; and 2) to inform program and policy development for natural resources or in relation to Government of Canada and Ministerial priorities.

A 15-minute telephone survey was conducted with a random sampling of 300 representatives of the Canadian freight transportation industry who occupy a position of owner/operator or senior level manager. The sampling frame was purchased from Dun & Bradstreet (D&B Canada) and drawn from NAICS code 4841 (General Freight Trucking)—specifically: 48411 (Local) and 48412 (Long Distance) and NAICS code 4842 (Specialized Freight [except Used Goods] Trucking Local—specifically: 484220 (Local) and 484230 (Long Distance).

All respondents were involved in, or knowledgeable about, the management or implementation of trucking fuel efficiency programs and policies within the business' fleet of vehicles. The results were weighted to reflect the actual distribution of businesses operating in this sector in Canada and can be considered accurate to within ±6%, 19 times out of 20. The margins of error are greater for results pertaining to subgroups of the total sample. The fieldwork was conducted from October 24 to November 14, 2022. More information on the methodology can be found in the Appendix: 1. Technical Specifications.

The contract value was $78,553.08 (including applicable taxes).

I hereby certify as a Senior Officer of Phoenix Strategic Perspectives that the deliverables fully comply with the Government of Canada political neutrality requirements outlined in the Communications Policy of the Government of Canada and Procedures for Planning and Contracting Public Opinion Research. Specifically, the deliverables do not contain any reference to electoral voting intentions, political party preferences, standings with the electorate, or ratings of the performance of a political party or its leader.

(original signed by)

Alethea Woods

President

Phoenix Strategic Perspectives Inc.

Company Profile

Retrofits

Fleet Energy Assessments

Government Funding Programs

Repowering

Concluding observations

The following are offered as concluding observations:

Companies are investing in upgrades to their fleet

Many of the companies surveyed have purchased new trucks for their fleet, including approximately one-third which have reportedly replaced more than half of their fleet within the last five years.

Retrofit cost is a barrier

An important finding is that most companies have not implemented any retrofits to their fleet in recent years. For a number of these companies, the cost associated with implementing retrofits is considered as a main barrier.

Awareness of government rebate programs aimed at fleet retrofits is low

Despite cost being identified as a hindrance to retrofitting, awareness and use of government funding programs aimed at encouraging fleet retrofits is low. Although participation in federal and provincial rebate programs is low, freight industry representatives attribute value to these programs, with more than two-thirds saying programs that support fleet retrofits are important.

Opportunity to increase participation in the rebate programs

The findings suggest there is significant opportunity to increase participation in the rebate programs because many companies that have not implemented retrofits would be motivated to do so by the availability of government funding. However, many of these companies would require government incentives to cover more than 50 percent of associated costs to make retrofitting financially feasible.

Opportunity to increase knowledge of repowering

There is also significant opportunity to increase knowledge of repowering existing engines as a cost-effective alternative to purchasing new vehicles. Although some companies have already repowered existing trucks, many of the freight industry representatives surveyed were not aware that this is a cost-saving alternative. Furthermore, when asked why their company is not interested in repowering, representatives pointed to the perception that doing so does not provide enough cost-savings benefit and/or that it is too expensive.

This section of the report provides a profile of the companies represented in the survey.

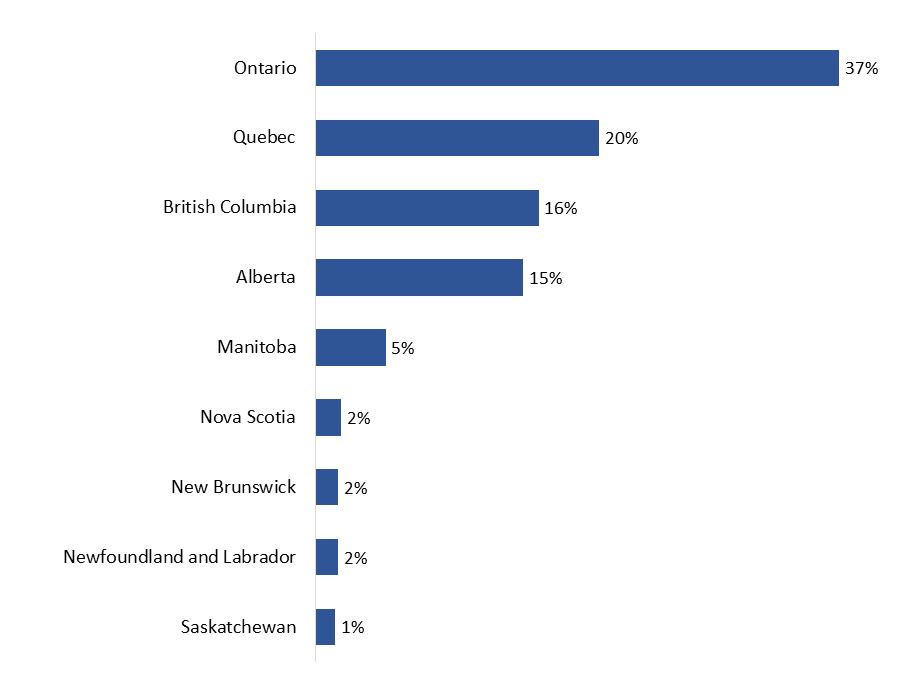

Thirty-seven percent of companies have head offices located in Ontario. Following this, one in five said their company's head office is in Quebec, 16% in British Columbia, and 15% in Alberta. Six percent of companies are headquartered in a province in Atlantic Canada and 6% are in Saskatchewan or Manitoba.

| Ontario | 37% |

| Quebec | 20% |

| British Columbia | 16% |

| Alberta | 15% |

| Manitoba | 5% |

| Nova Scotia | 2% |

| New Brunswick | 2% |

| Newfoundland and Labrador | 2% |

| Saskatchewan | 1% |

| Yukon Territory | 0% |

Q4. In which province or territory is your company's head office located? Base: n=300; All respondents.

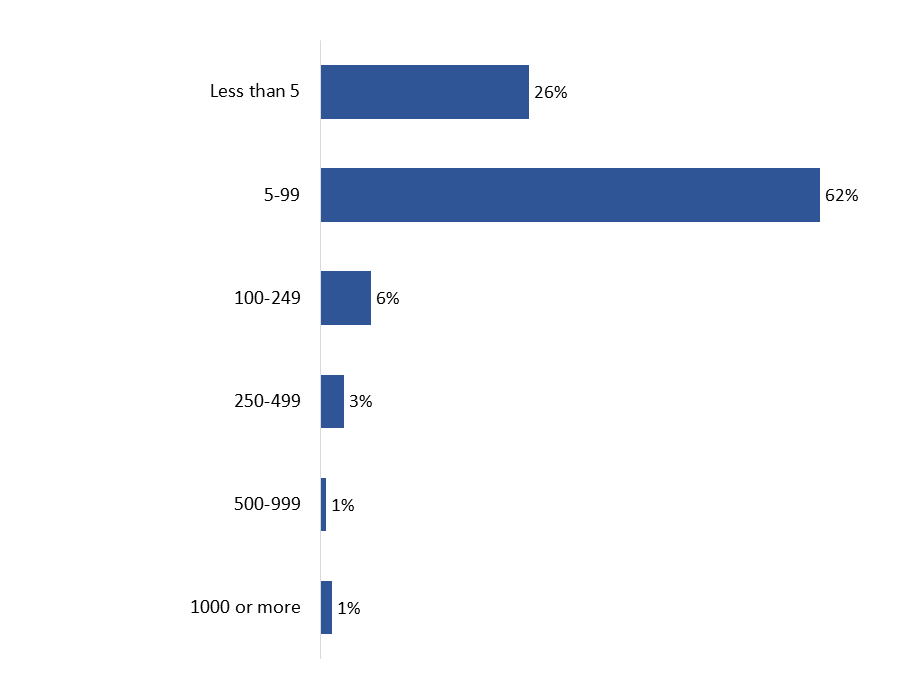

The single largest proportion of companies (62%) employ between five and 99 employees. Following this, one-quarter (26%) employ fewer than five employees. Even fewer companies surveyed employ 100 or more employees (11%).

| Less than 5 | 26% |

| 5-99 | 62% |

| 100-249 | 6% |

| 250-499 | 3% |

| 500-999 | 1% |

| 1000 or more | 1% |

Q5. How many employees work for your company? Base: n=300; All respondents.

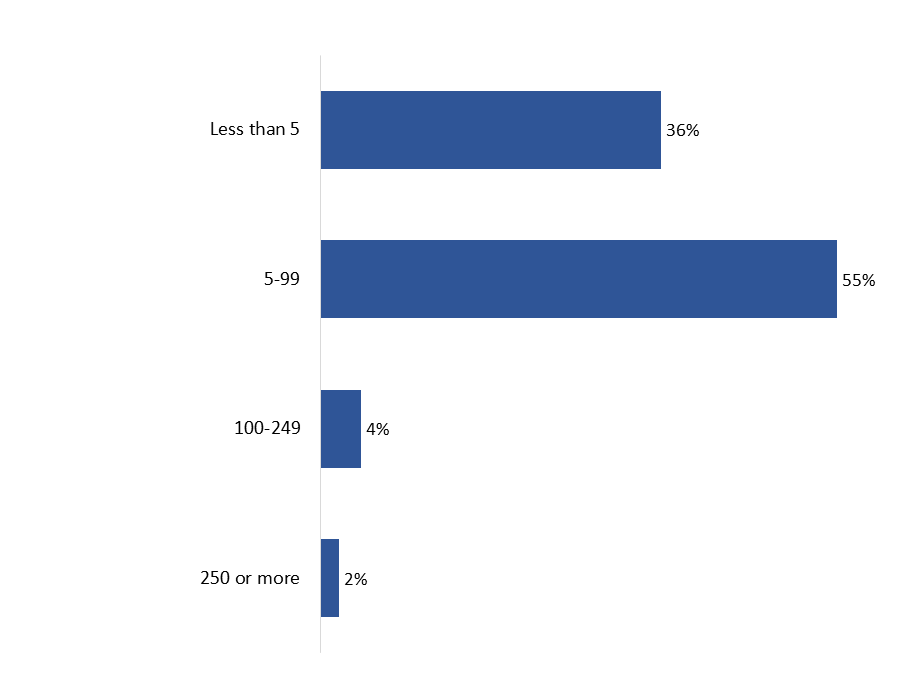

The vast majority (92%) of companies surveyed employ fewer than 100 drivers. Specifically, just over half (55%) employ between five and 99 drivers. Following this, approximately one-third (36%) employ fewer than five drivers. Six percent of companies employ 100 or more drivers.

| Less than 5 | 36% |

| 5-99 | 55% |

| 100-249 | 4% |

| 250 or more | 2% |

Q6. How many of these employees are employed as drivers for your company? Base: n=300; All respondents.

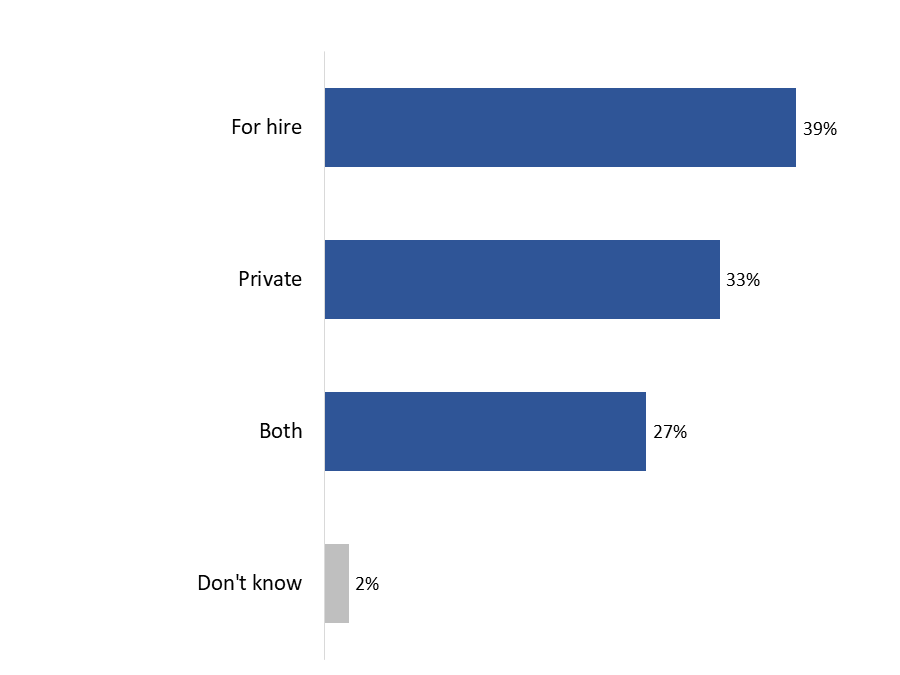

The type of fleet reported by companies is varied; 39% have exclusively for-hire fleets and 33% exclusively private fleets. Additionally, a little more than one-quarter (27%) have a combination for-hire and private fleet.

| For hire | 39% |

| Private | 33% |

| Both | 27% |

| Don't know | 2% |

Q7. Is your fleet...Base: n=300; All respondents.

Companies based in Quebec (89%) were far more likely to report a private fleet as compared to companies headquartered elsewhere in the country. Additionally, companies that have implemented retrofits to their fleet of trucks (49%) were more likely than those that have not done so (28%) to report an exclusively private fleet.

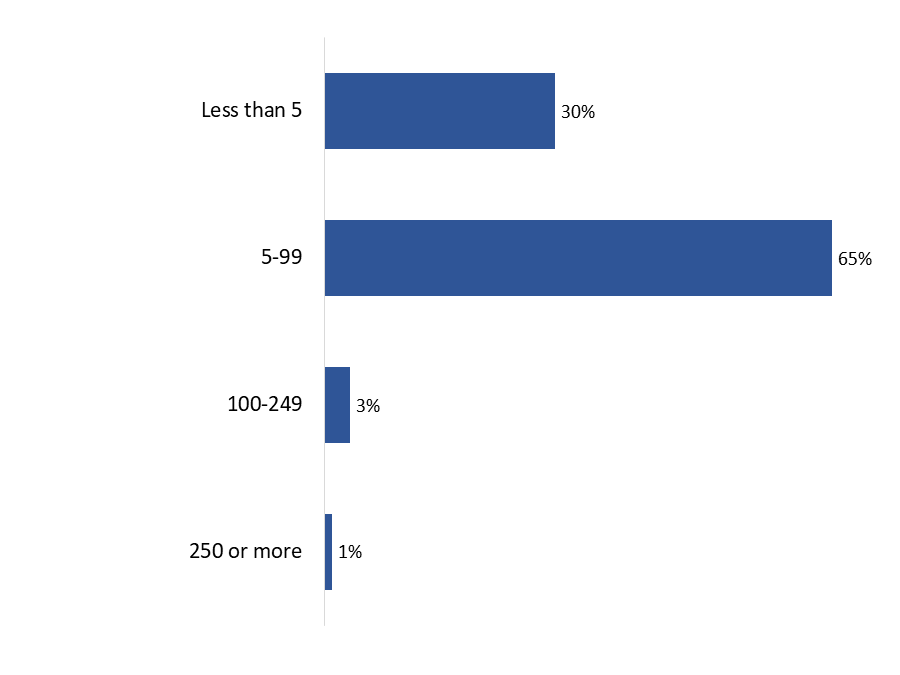

A majority (65%) of freight industry representatives surveyed said their company has between five and 99 trucks in its fleet. Most of the rest (30%) have fewer than five trucks. Very few companies (4%) have more than 100 trucks in their fleet.

| Less than 5 | 30% |

| 5-99 | 65% |

| 100-249 | 3% |

| 250 or more | 1% |

Q8. How many trucks are in your company's fleet? Base: n=300; All respondents.

Companies not offering eco-driving training to their drivers were more likely to report having fewer than five trucks in their fleet (36% versus 19% of companies that do offer eco-driving training). Additionally, companies that have implemented retrofits to their truck fleet (75%) were more likely than those that have not done so (61%) to have five to 99 trucks.

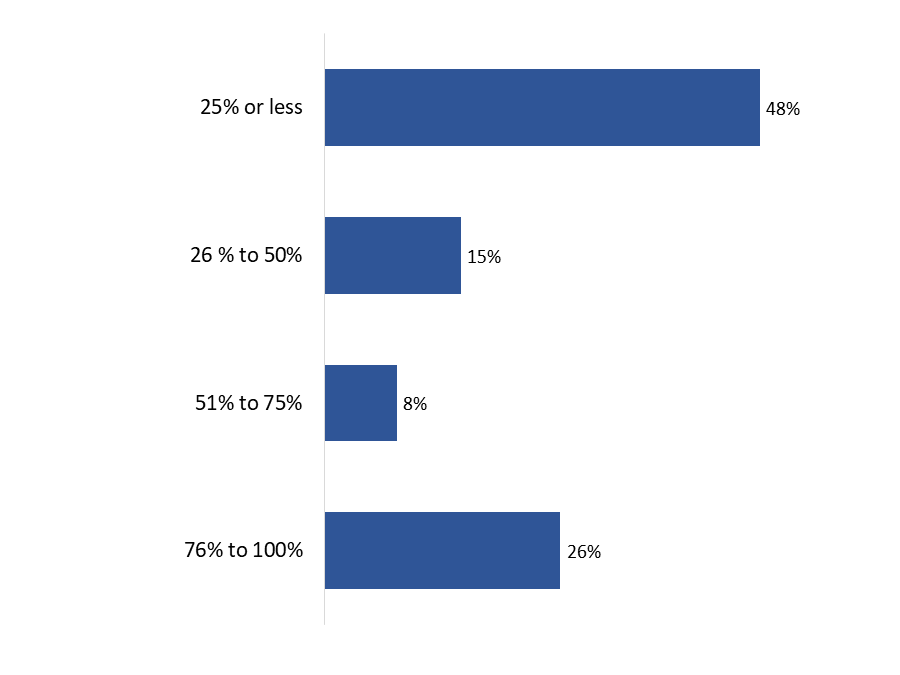

Nearly half (48%) of freight industry representatives said that up to one-quarter of their company's fleet is less than five years old. Following this, only 15% reported that 26 to 50 percent of the trucks in their company's fleet are less than five years old and approximately one-third (34%) said that more than half the trucks in their company's fleet met this criterion.

| 25% or less | 48% |

| 26 % to 50% | 15% |

| 51% to 75% | 8% |

| 76% to 100% | 26% |

Q9. Approximately what percentage of trucks in your fleet are less than five years old? Base: n=300; All respondents.

Companies not offering eco-driving training to their drivers were more likely to report having fewer trucks less than five years of age in their fleet (56% versus 37% of companies that do offer eco-driving training). In contrast, companies offering eco-driving training were more likely to report that more than three-quarters of their fleet is less than five years old (35% versus 20% of those that do not offer training).

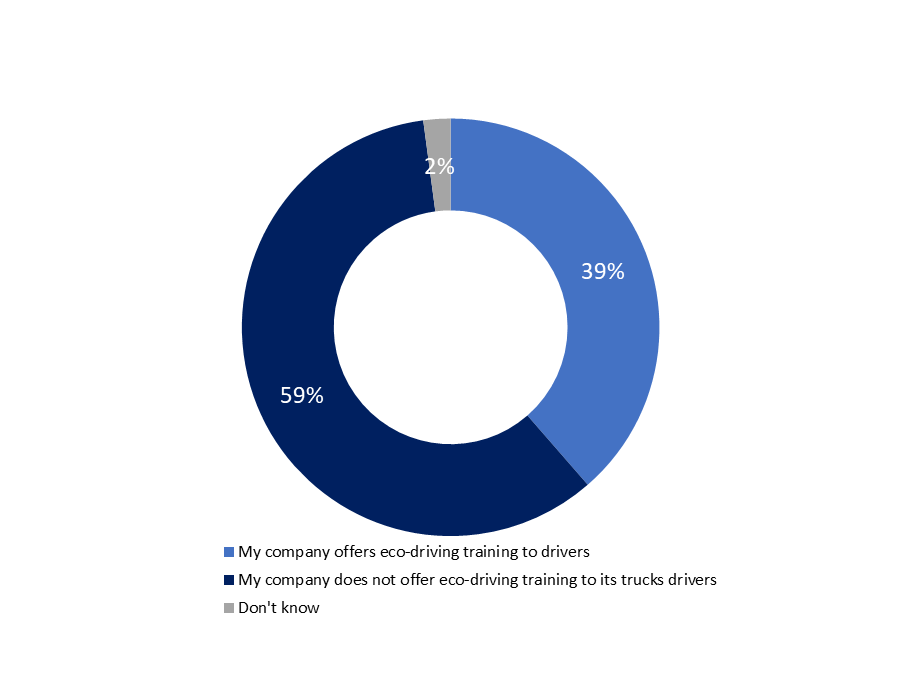

Thirty-nine percent of companies offer eco-driving training to their truck drivers. Conversely, 59% do not offer their drivers this training.

| My company offers eco-driving training to drivers | 39% |

| My company does not offer eco-driving training to its trucks drivers | 59% |

| Don't know | 2% |

Q37. Does your company offer eco-driving training to its truck drivers? Base: n=300; all respondents

This section of the report discusses the retrofits implemented by companies in the past three years.

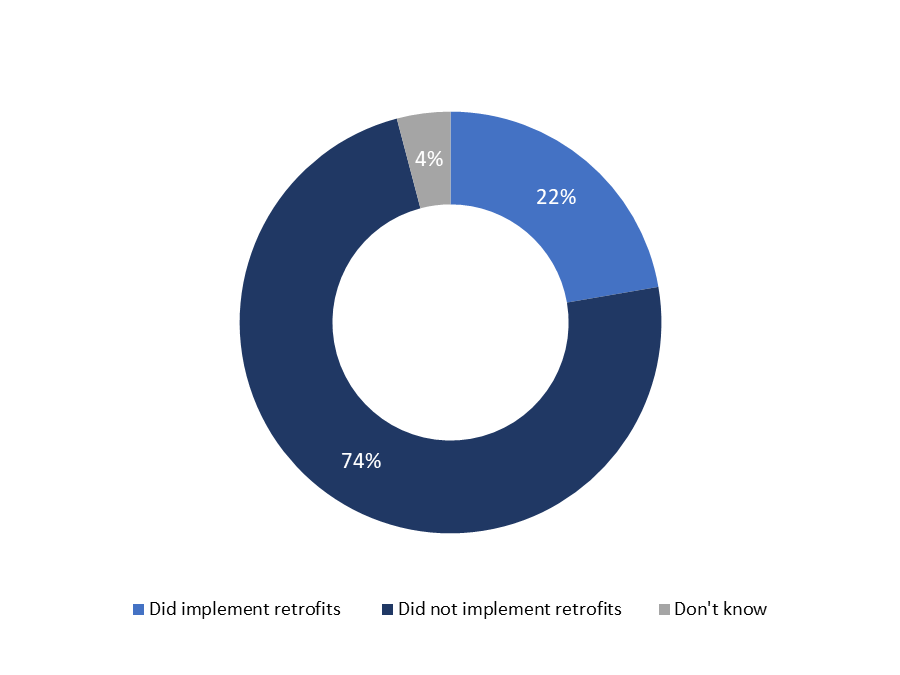

Nearly three-quarters (74%) of companies have not implemented any retrofits to the trucks in their fleet in the past three years. Conversely, about one in five (22%) have implemented retrofits within this time.

| Did implement retrofits | 22% |

| Did not implement retrofits | 74% |

| Don't know | 4% |

Q10. In the past 3 years, has your company implemented any retrofits to its truck fleet? Base: n=300; all respondents

Companies based in Quebec (51%) and those with exclusively private fleets (33%) were far more likely to report having implemented retrofits.

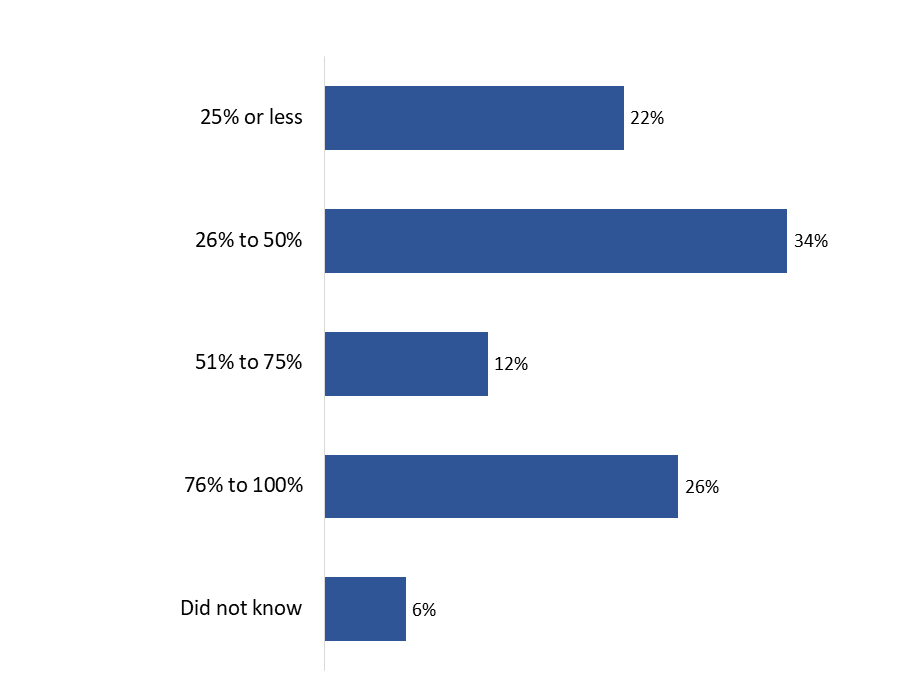

Among companies that have implemented retrofits in the past three years (n=65), approximately one in five (22%) have retrofitted up to 25 percent of their trucks. Following this, one-third (34%) have implemented retrofits to 26 to 50 percent of their fleet, while 38% have retrofitted more than three-quarters of the trucks in their fleet.

| 25% or less | 22% |

| 26% to 50% | 34% |

| 51% to 75% | 12% |

| 76% to 100% | 26% |

| Did not know | 6% |

Q11. What percentage of your company's truck fleet has been retrofitted in the past 3 years? Base: n=65; companies that implemented retrofits to its truck fleet in the past 3 years

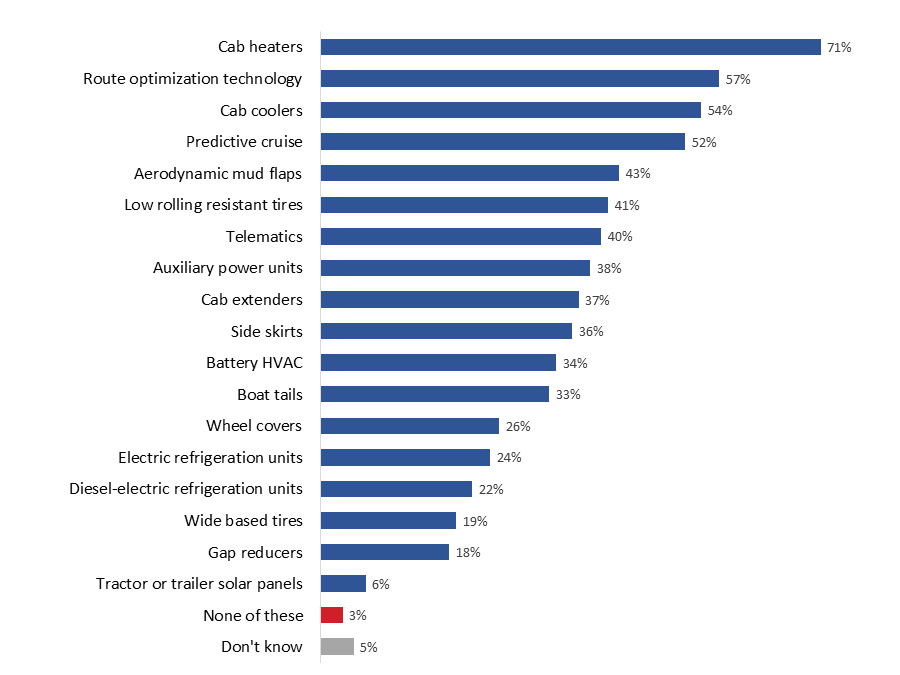

Most companies (71%) that have completed retrofitsFootnote 2 in the last three years implemented cab heaters. Following this, more than half the companies surveyed that completed retrofits in the past 3 years have implemented route optimization technology (57%), cab coolers (54%), and predictive cruise (52%). The full range of retrofits completed by companies can be found below in figure 10.

| Cab heaters | 71% |

| Route optimization technology | 57% |

| Cab coolers | 54% |

| Predictive cruise | 52% |

| Aerodynamic mud flaps | 43% |

| Low rolling resistant tires | 41% |

| Telematics | 40% |

| Auxiliary power units | 38% |

| Cab extenders | 37% |

| Side skirts | 36% |

| Battery HVAC | 34% |

| Boat tails | 33% |

| Wheel covers | 26% |

| Electric refrigeration units | 24% |

| Diesel-electric refrigeration units | 22% |

| Wide based tires | 19% |

| Gap reducers | 18% |

| Tractor or trailer solar panels | 6% |

| None of these | 3% |

| Don't know | 5% |

Q12. Which of the following retrofits, if any, has your company completed in the past 3 years? Base: n=65; those whose company implemented retrofits to their trucks. Multiple responses accepted.

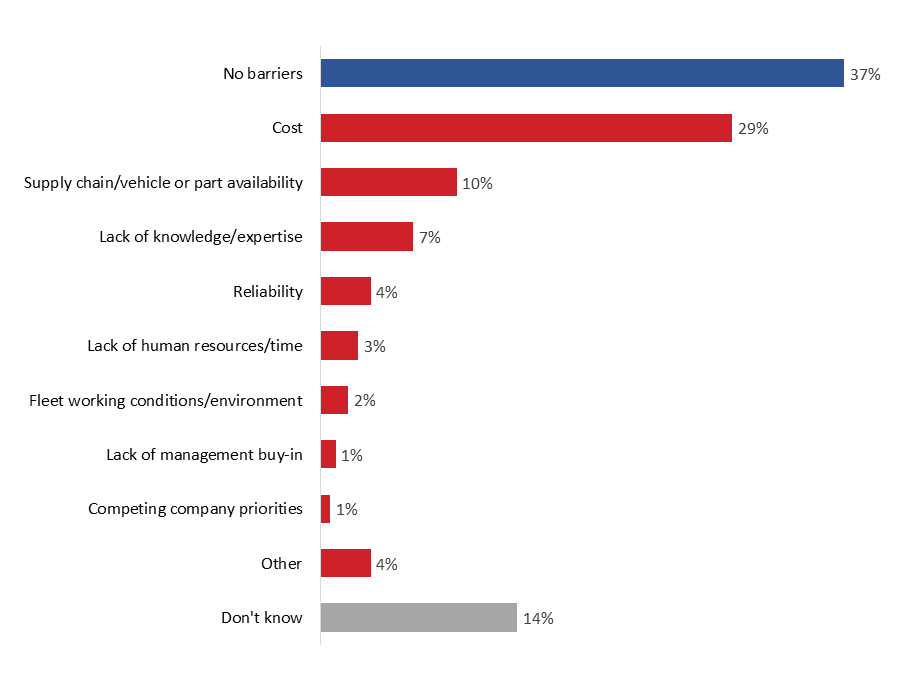

Most companies surveyed (60%) reported at least one barrier faced when it comes to retrofitting their fleet. Conversely, more than one-third (37%) of these companies face no barriers to retrofitting their trucks. Among the barriers to retrofitting reported, the most common is cost (29%), followed by supply chain and vehicle or part availability (10%) and lack of required knowledge or expertise (7%). The full range of barriers identified by respondents are detailed in figure 11.

| No barriers | 37% |

| Cost | 29% |

| Supply chain/vehicle or part availability | 10% |

| Lack of knowledge/expertise | 7% |

| Reliability | 4% |

| Lack of human resources/time | 3% |

| Fleet working conditions/environment | 2% |

| Lack of management buy-in | 1% |

| Competing company priorities | 1% |

| Other | 4% |

| Don't know | 14% |

Q13. What barriers, if any, does your company face when it comes to retrofitting its fleet? Base: n=300; all respondents. Multiple responses accepted.

Companies that have implemented retrofits to their trucks in the past three years (45%) were more likely than those that have not (26%) to report that cost is a barrier when it comes to retrofitting their fleet.

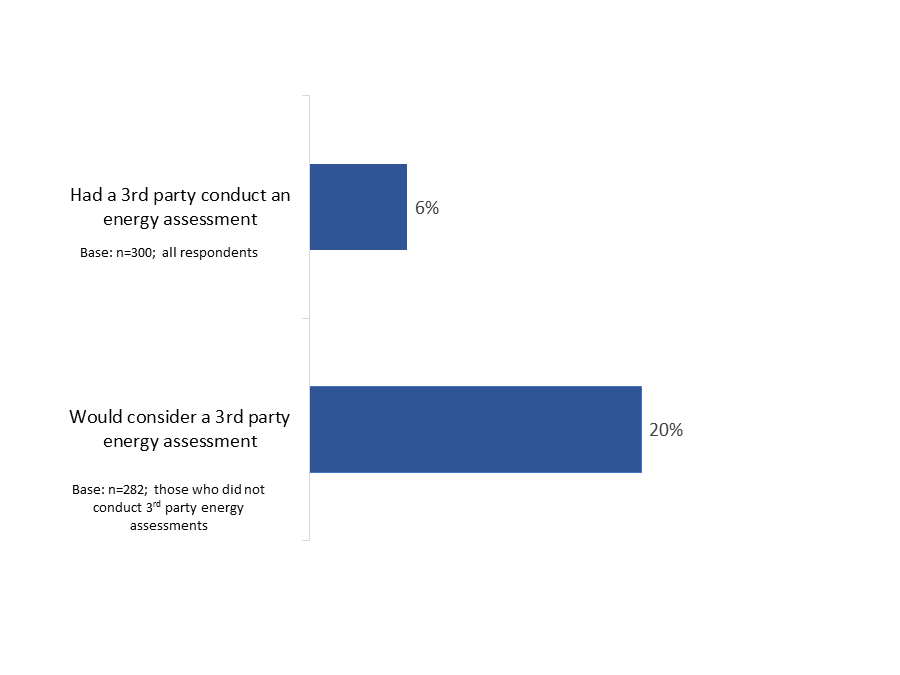

This section of the report discusses fleet energy assessments.

Very few (6%) companies have had a third party conduct an energy assessment of their fleet. Among companies that have not had an energy assessment (n=282), exactly one in five would consider having a third party conduct an energy assessment of their fleet.

| Had a 3rd party conduct an energy assessment | 6% |

| Would consider a 3rd party energy assessment | 20% |

Q14. Has your company ever had a third party conduct an energy assessment of your fleet? Q16. Would your company ever consider having a third party conduct an energy assessment of its fleet?

This section of the report presents respondents' views of government funding and awareness of government funding programs.

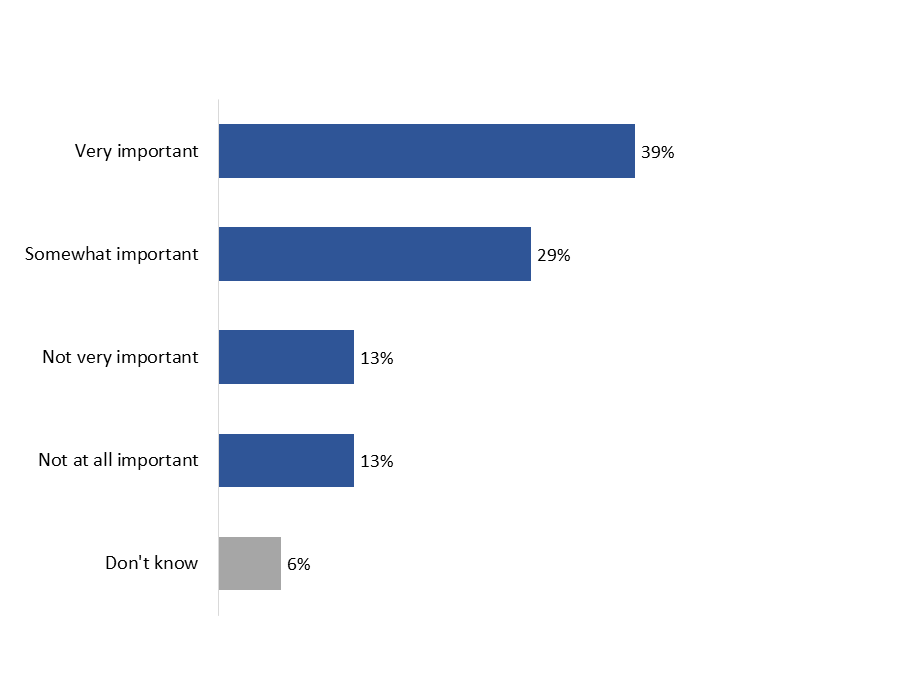

More than two-thirds (69%) of freight transportation representatives said that government funding programs are at least somewhat important. Specifically, 39% view these programs as very important and an additional 29% view them as somewhat important for fleet retrofits. At the other end of the spectrum, one-quarter consider government funding programs to be not very (13%) or not at all (13%) important.

| Don't know | 6% |

| Not at all important | 13% |

| Not very important | 13% |

| Somewhat important | 29% |

| Very important | 39% |

Q18. How important are government funding programs that support fleet retrofits? Base: n=300; all respondents

Companies that offer eco-driving training (80%) were significantly more likely than those that do not (61%) to report that government funding programs supporting fleet retrofits are important. Compared to companies headquartered elsewhere in the country, those in Ontario (76%) were more likely to attribute importance to government funding.

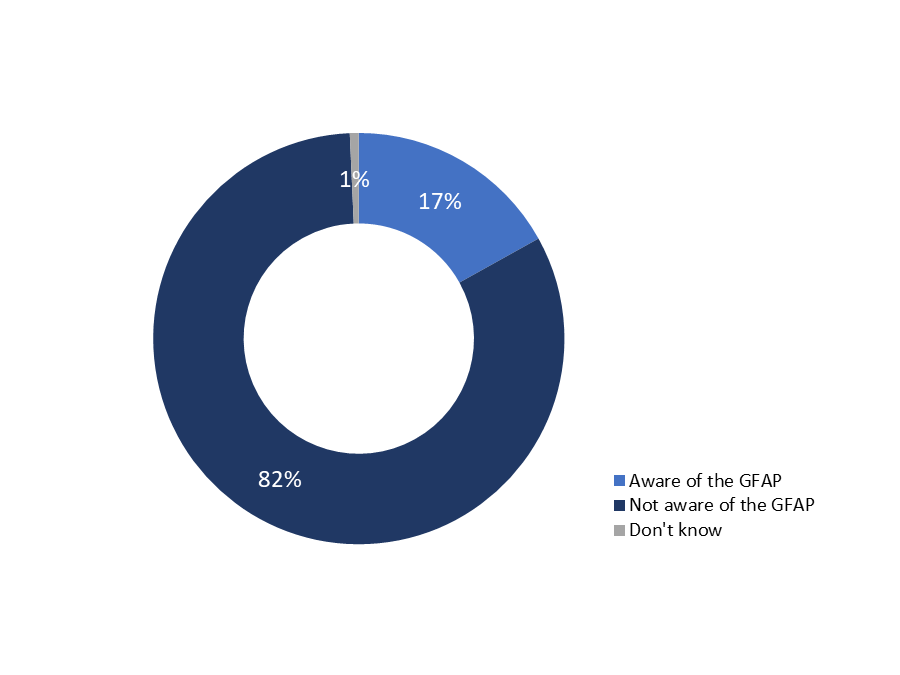

Close to one in five (17%) representatives of freight transportation companies are aware of the Government of Canada's Green Freight Assessment program (GFAP), which provided funding towards fleet assessments and retrofits between 2018-2022. This program has since been renamed the Green Freight Program, which relaunched on December 12, 2022.

| Aware of the GFAP | 17% |

| Not aware of the GFAP | 82% |

| Don't know | 1% |

Q19. Are you aware of the Government of Canada's Green Freight Assessment Program? Base: n=300; all respondents

Companies that offer eco-driving training (26%) and those aware of provincial/territorial rebate programs (57%) were more likely to be aware of the GFAP.

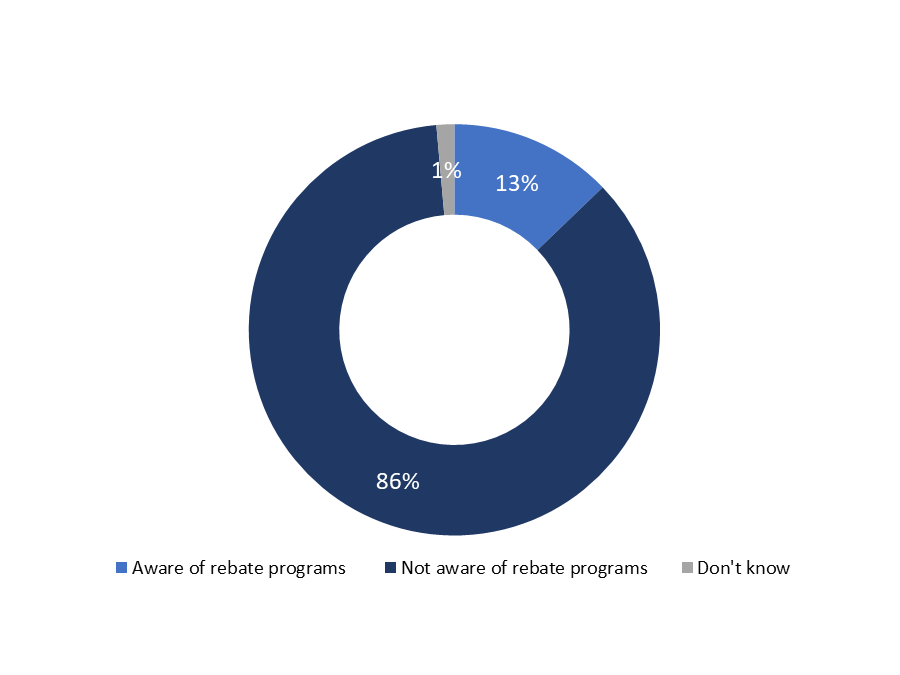

Awareness of provincial/territorial rebate programs for retrofits is not widespread. Thirteen percent of freight transportation companies surveyed are aware of these programs, while more than eight in 10 (86%) are not aware.

| Aware of rebate programs | 13% |

| Not aware of rebate programs | 86% |

| Don't know | 1% |

Q21. Are you aware of any [provincial/territorial] rebate programs for fleet retrofits? Base: n=300; all respondents

Companies that offer eco-driving training (21%) and those aware of the GFAP (43%) were more likely to be aware of provincial/territorial rebate programs (57%).

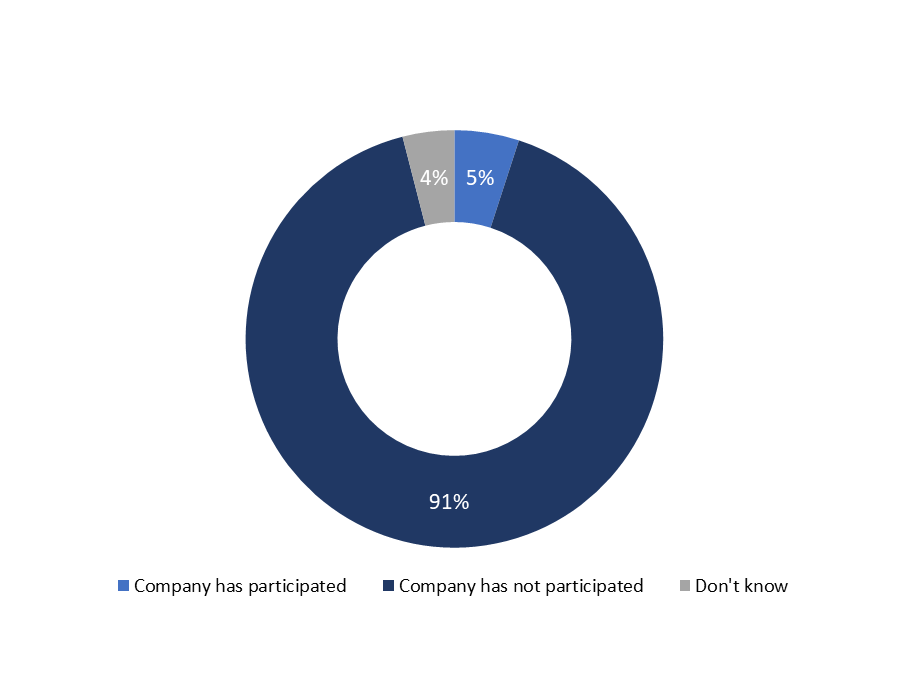

Use of government funded retrofit programs is limited. Specifically, 5% of the freight transportation representatives surveyed said their company has participated in one or more of these programs.

| Company has participated | 5% |

| Company has not participated | 91% |

| Don't know | 4% |

Q22. Has your company participated in any government funding programs for fleet retrofits? Base: n=300; all respondents

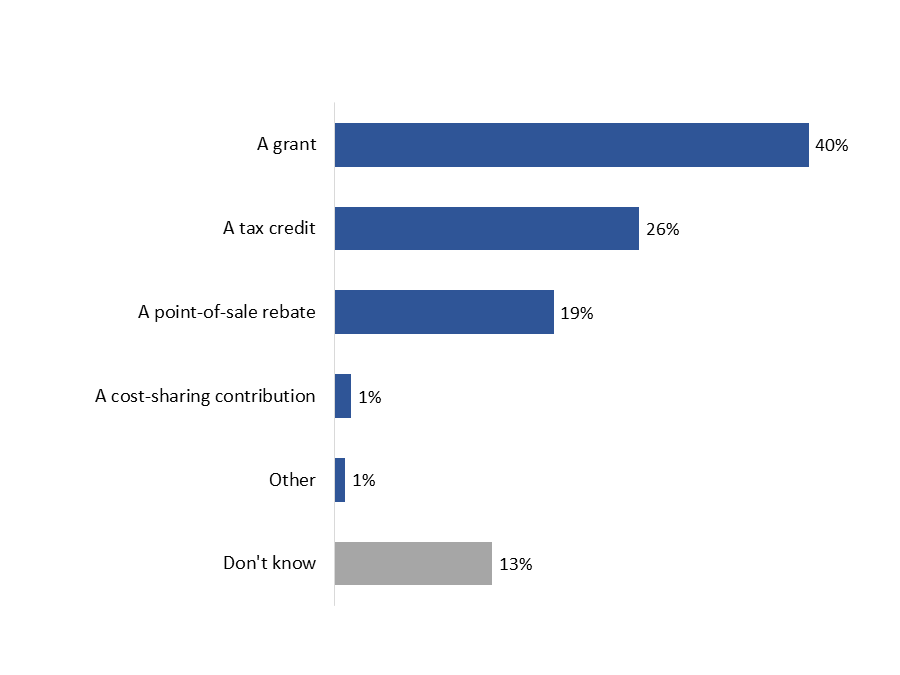

When asked what type of funding their company would prefer to receive when participating in a government funded program for fleet retrofits, 40% of respondents said their company would prefer to receive a grant. About one-quarter (26%) would prefer a tax credit, while 19% would prefer a point-of-sale rebate.

| A grant | 40% |

| A tax credit | 26% |

| A point-of-sale rebate | 19% |

| A cost-sharing contribution | 1% |

| Other | 1% |

| Don't know | 13% |

Q24. What type of funding would your company prefer to receive participating in a government funding program for fleet retrofits? Base: n=300; all respondents

Companies that have already implemented retrofits to their truck fleet (52%) were likely than those that have not (37%) to express a preference a grant.

Among companies that have not implemented retrofits and that report cost as a barrier to doing so (n=58), 70% of respondents said the availability of government funding would motivate their company to consider retrofits. Seventeen percent would not be motivated to implement retrofits despite availability of government funding.

| Would be motivated | 70% |

| Would not be motivated | 17% |

| Don't know | 14% |

Q25. Would the availability of government funding motivate your company to consider retrofitting its fleet? Base: n=58; those who did not retrofit their fleet and said cost is a barrier

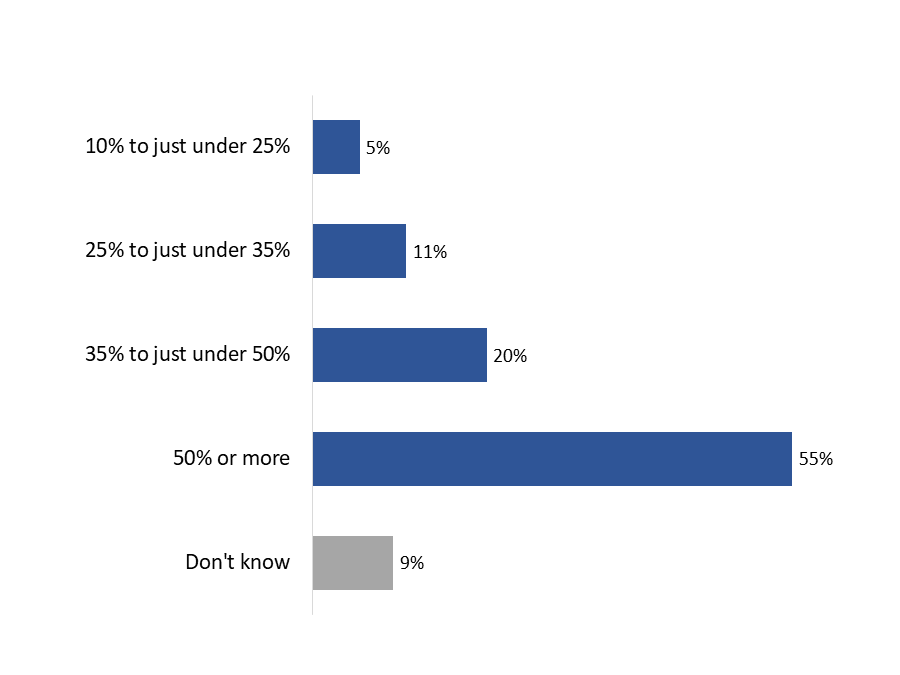

Among companies that would consider implementing retrofits with government funding (n=40), over half (55%) would require government incentives to cover 50 percent or more of the associated costs to make this financially feasible for their company. Following this, one in five companies would require government funding to cover between 35 percent to just under 50 percent of the costs. Fewer (16%) companies would require less than 35 percent of the costs of retrofitting to be covered by government funding.

| 10% to just under 25% | 5% |

| 25% to just under 35% | 11% |

| 35% to just under 50% | 20% |

| 50% or more | 55% |

| Don't know | 9% |

Q26. What percentage of the fleet retrofitting cost would your company need funded by government incentives to make retrofitting financially feasible? Base: n=39; those who would consider retrofitting if government funding is available

This section of the report presents respondents' views and actions in relation to repowering.

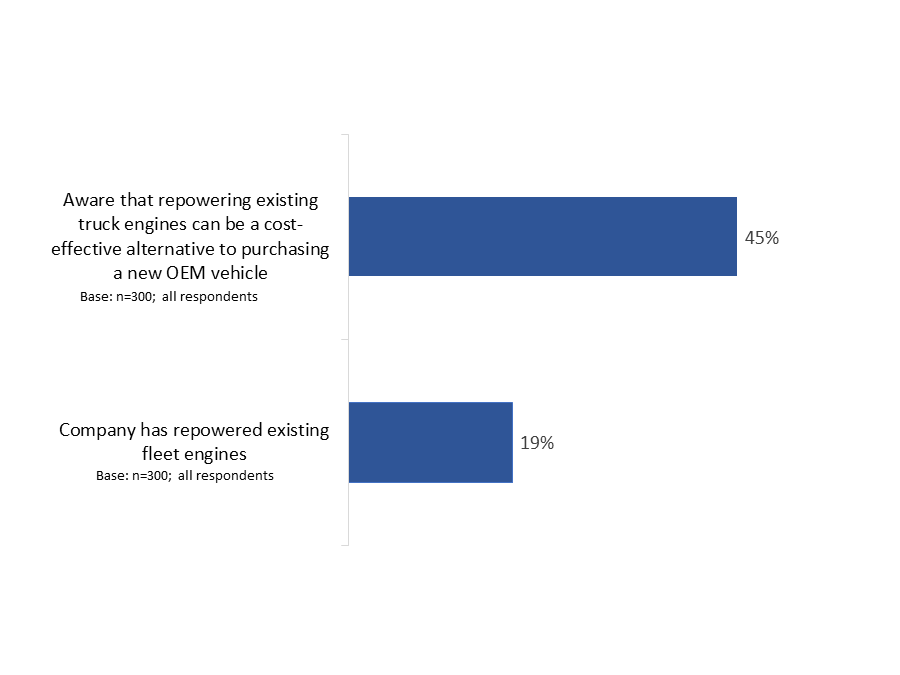

Forty-five percent of freight transportation companies surveyed are aware that repowering existing truck engines can be a cost-effective alternative to purchasing a new Original Equipment Manufacturer (OEM) vehicle. One in five (19%) companies have already repowered existing fleet engines.

| Aware that repowering existing truck engines can be a cost-effective alternative to purchasing a new OEM vehicle | 45% |

| Company has repowered existing fleet engines | 19% |

Q27. Are you aware that repowering your existing truck engines can be a cost-effective alternative to purchasing a new OEM vehicle?Q28. Has your company repowered any of existing fleet engines?

The following companies were more likely to be aware that repowering existing truck engines can be a cost-effective alternative to purchasing a new OEM vehicle:

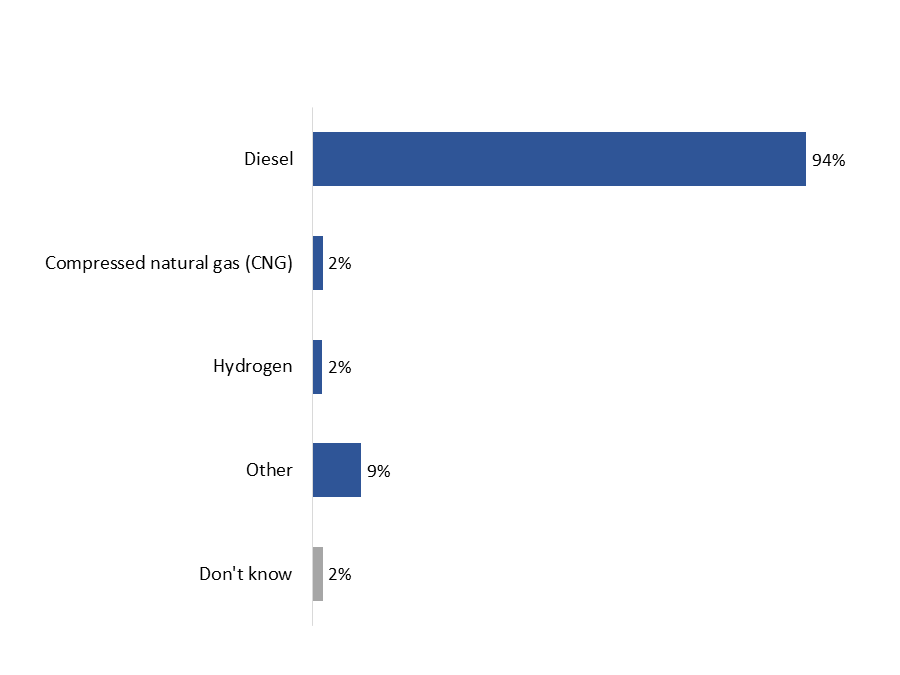

Among freight transportation companies that have repowered existing fleet engines (n=58), the vast majority (94%) use diesel fuel. Very few companies use compressed natural gas (CNG) (2%) or hydrogen (2%) to fuel their repowered fleets.

| Diesel | 94% |

| Compressed natural gas (CNG) | 2% |

| Hydrogen | 2% |

| Other | 9% |

| Don't know | 2% |

Q30. Which fuel types do your company's repowered fleet use? Base: n=58; those who repowered company's fleet engines. Multiple responses accepted.

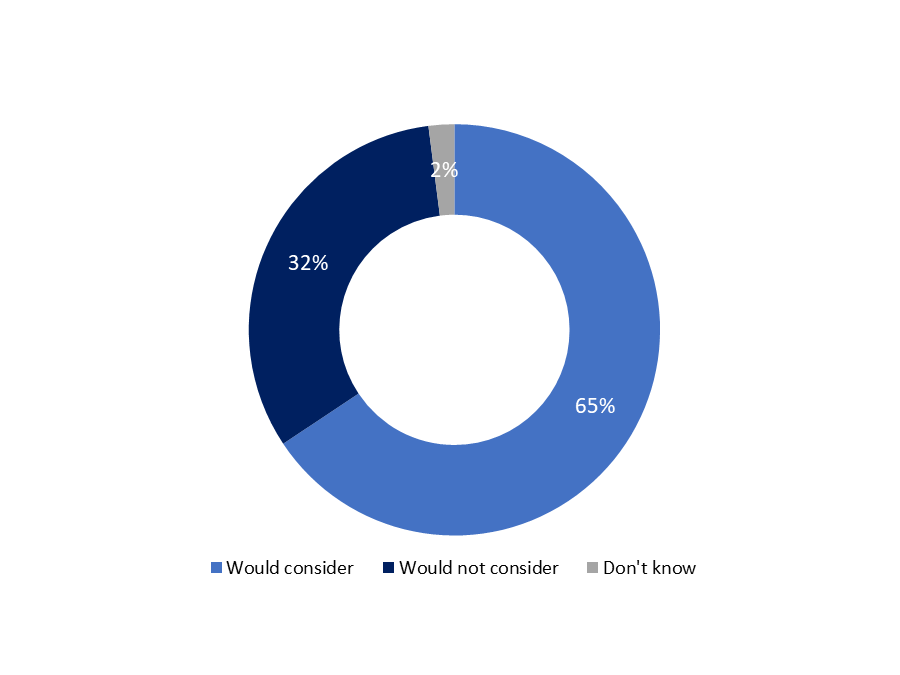

Among freight transportation companies that have repowered some of their fleet (n=48), two-thirds (65%) would consider repowering more engines if some type of government funding was available. Conversely, one-third (32%) of companies would not consider repowering more engines even if some type of government funding was available.

| Would consider | 65% |

| Would not consider | 32% |

| Don't know | 2% |

Q31. Would your company consider repowering more of its fleet engines if some type of government funding was available? Base: n=47; those who repowered <100% of their fleet engines

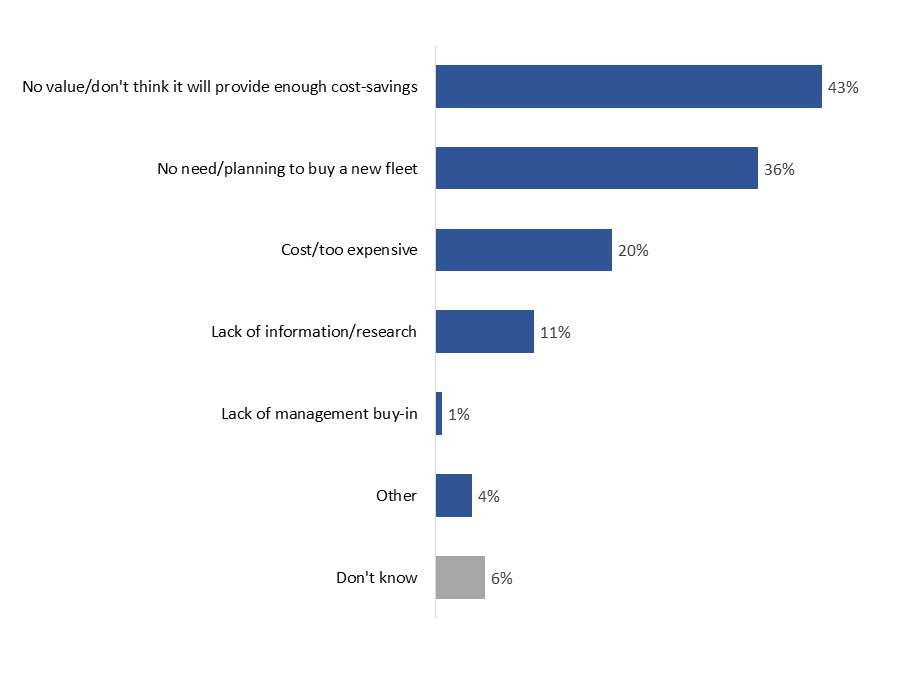

For companies not interested in repowering any fleet engines (n=181)Footnote 3, many believe this will not provide enough cost-savings to be of value (43%) and/or are already planning to buy a new fleet (36%). One in five (20%) said that their company believes repowering its fleet would be too expensive and one in 10 (11%) lack information or research to support decision-making.

| No value/don't think it will provide enough cost-savings | 43% |

| No need/planning to buy a new fleet | 36% |

| Cost/too expensive | 20% |

| Lack of information/research | 11% |

| Lack of management buy-in | 1% |

| Other | 4% |

| Don't know | 6% |

Q33. Why is your company not interested in repowering any of its fleet engines? Base: n=181; those whose company is not considering repowering. Multiple responses accepted.

This section of the report presents a profile of the truck fleets of responding companies.

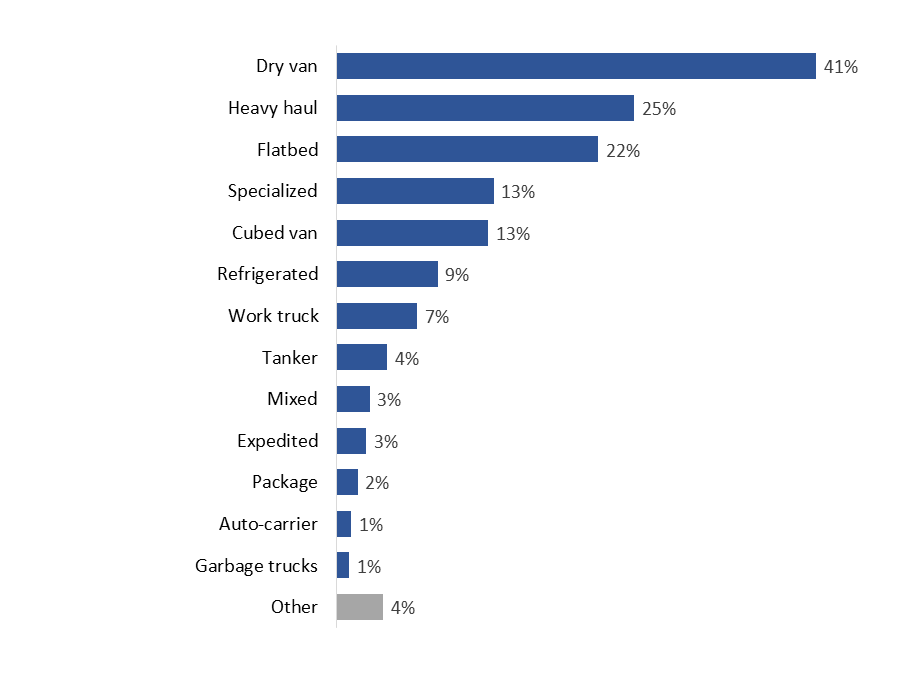

Forty-one percent of freight transportation companies surveyed have dry vans in their fleet. Following this, exactly one-quarter have heavy haul trucks, while 22% have flatbed trucks. The full list of trucks can be found below in figure 24.

| Dry van | 41% |

| Heavy haul | 25% |

| Flatbed | 22% |

| Specialized | 13% |

| Cubed van | 13% |

| Refrigerated | 9% |

| Work truck | 7% |

| Tanker | 4% |

| Mixed | 3% |

| Expedited | 3% |

| Package | 2% |

| Auto-carrier | 1% |

| Garbage trucks | 1% |

| Other | 4% |

Q34. What type of trucks are in your company's fleet? Base: n=300; all respondents. Multiple responses accepted.

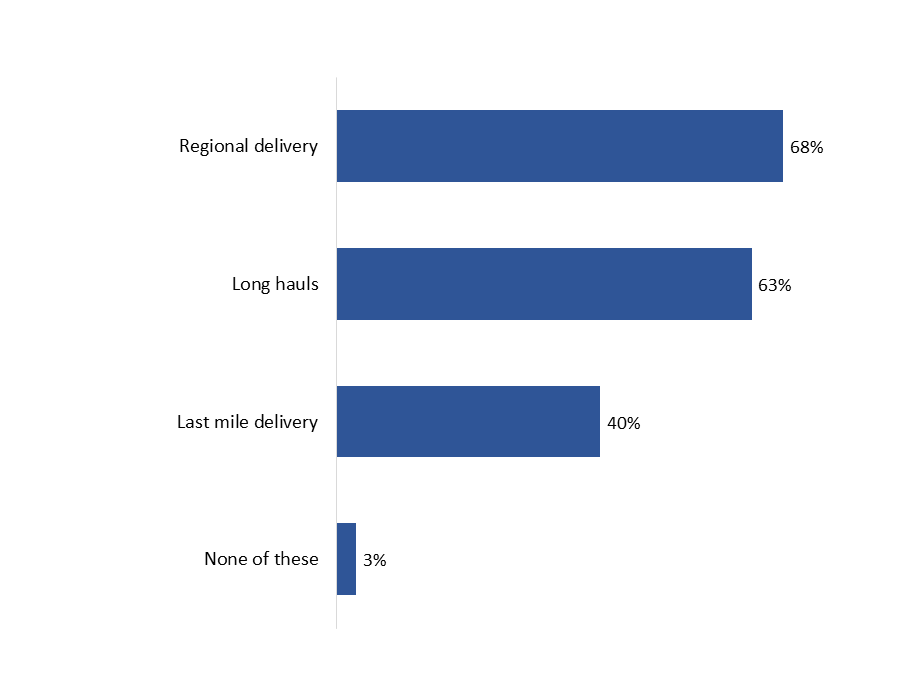

Sixty-eight percent of companies surveyed use their trucks for regional deliveries, 63% for long hauls, and 40% last mile deliveries.

| Regional delivery | 68% |

| Long hauls | 63% |

| Last mile delivery | 40% |

| None of these | 3% |

Q35. Are your trucks used for… Base: n=300; all respondents. Multiple responses accepted.

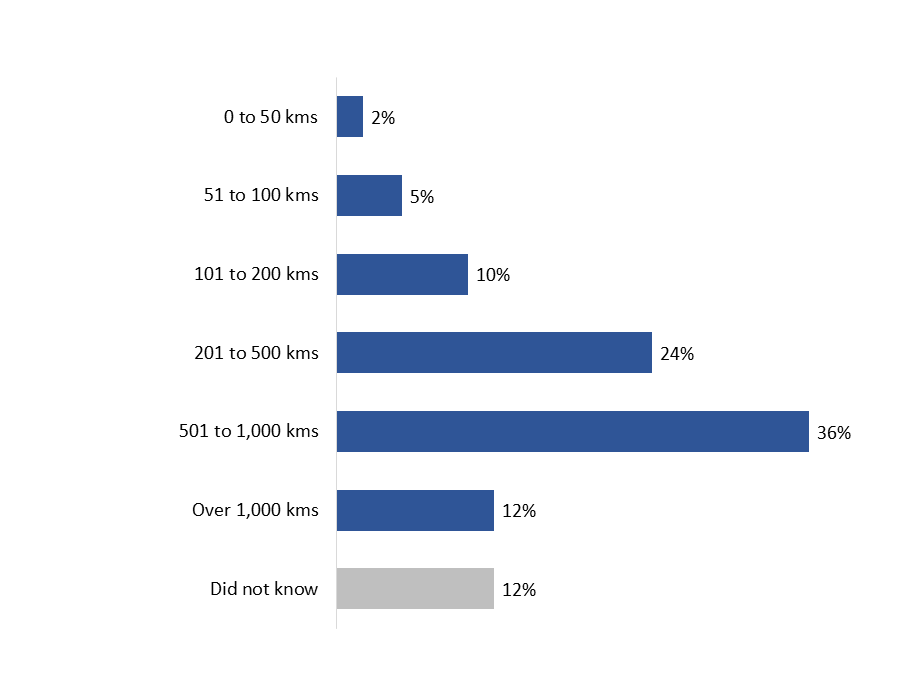

The majority (72%) of the companies surveyed noted that their trucks travel more than 200 kilometres daily. Specifically, 24% travel between 201 and 500 kms daily, 36% travel between 501 to 1,000 kms, and 12% travel more than 1,000 kms daily.

| 0 to 50 kms | 2% |

| 51 to 100 kms | 5% |

| 101 to 200 kms | 10% |

| 201 to 500 kms | 24% |

| 501 to 1,000 kms | 36% |

| Over 1,000 kms | 12% |

| Did not know | 12% |

Q36. In an average day, how many kilometers do your trucks travel? Base: n=300; all respondents.

The following specifications applied to this survey:

| NAICS code | No. of interviews |

|---|---|

| General freight: local (484110) | 129 |

| General freight: long distance (484121, 484122) | 133 |

| Specialized freight trucking excluding used goods (484220, 484230) | 38 |

| Total Numbers Attempted | 8,327 |

| Out-of-scope - Invalid | 1,638 |

| Unresolved (U) | 3,397 |

| No answer/answering machine | 3,397 |

| In-scope - Non-responding (IS) | 2,675 |

| Language barrier | 19 |

| Incapable of completing (ill/deceased) | 45 |

| Respondent refusal | 1,281 |

| Callback scheduled/not completed | 1,291 |

| Termination | 39 |

| In-scope - Responding units (R) | 617 |

| Completed interview | 300 |

| Quota reached | 2 |

| Not eligible | 315 |

| Response RateFootnote 4 [R=R/(U+IS+R)] | 10.16% |

| NAICS code | Unweighted | Weighted |

|---|---|---|

| General freight: local (484110) | 129 | 139 |

| General freight: long distance (484121, 484122) | 133 | 144 |

| Specialized freight trucking excluding used goods (484220, 484230) | 38 | 17 |

1st POINT OF CONTACT/GATEKEEPER:

Hello/bonjour, my name is [Interviewer's name]. Would you prefer to continue in English or French? / Préférez-vous continuer en anglais ou en français? May I speak to someone at your company who is most familiar with fuel efficiency tracking and management within your organization?

IF ASKED BY GATEKEEPER:

I'm calling on behalf of Phoenix SPI, a public opinion research company. We're conducting a survey for Natural Resources Canada about important issues facing the freight transportation industry across Canada. May I speak to the person who is most familiar with the fuel efficiency programs and policies within your company's fleet of vehicles?

RESPONDENT:

Hello/Bonjour, my name is [INSERT NAME]. I'm calling on behalf of Phoenix SPI, a public opinion research company. We're conducting a survey for Natural Resources Canada with people who have knowledge about fuel efficiency tracking and management within the freight transportation industry. The results of this study will help guide future public policy on clean energy technology and addressing climate change.

The survey takes about 15 minutes and is voluntary. Your responses will be kept confidential and anonymous, and the information provided will be administered according to the requirements of the Privacy Act, the Access to Information Act, and any other pertinent legislation.

This survey is registered with the Canadian Research Insights Council's survey validation system.

May I continue?

INTERVIEWER NOTE: IF A RESPONDENT ASKS ABOUT THE LEGITIMACY OF THIS SURVEY, SAY: This survey is registered with the Canadian Research Insights Council's survey validation system. The registration number is: 20221019-PH691.

A. Screening and Quotas

Before we start,

1. May I confirm that your company operates freight transportation trucks?

INTERVIEWER NOTE: IF ASKED WHAT FREIGHT TRANSPORTATION TRUCKS ARE, SAY: These typically include medium- and heavy-duty trucks used for moving goods and does not include vans.

2. How knowledgeable would you say you are with the fuel efficiency programs and policies within your company's fleet of vehicles? This includes the tracking, management or implementation of such programs and policies. Are you… [READ LIST]

3. [IF Q2=02] Can you direct me to someone at your company that is knowledgeable about the tracking, management or implementation of fuel efficiency programs and policies within your company?

4. In which province or territory is your company's head office located? [DO NOT READ LIST]

5. How many employees work for your company? Please include part-time employees as full-time equivalents. [DO NOT READ LIST]

6. And, how many of these employees are employed as drivers for your company?

B. Retrofits

These next questions are about retrofits to your company's freight transportation trucks.

To start,

7. Is your fleet… [READ LIST]

8. How many trucks are in your company's fleet?

9. Approximately what percentage of trucks in your fleet are less than five years old?

10. In the past 3 years, has your company implemented any retrofits to its truck fleet? [INTERVIEWER NOTE: IF ASKED, SAY: 'By retrofits we are referring to upgrades made to your truck(s) with energy efficient devices'.]

11. [IF Q10=01] How many of your company's truck fleet has been retrofitted in the past 3 years?

12. [IF Q10=01] Which of the following retrofits, if any, has your company completed in the past 3 years? [RANDOMIZE/READ LIST; ACCEPT MULTIPLE RESPONSES] [INTERVIEWER NOTE: IF ASKED, PLEASE REMIND RESPONDENTS THAT WE ARE ASKING ABOUT RETROFITS TO EXISTING TRUCKS.]

13. What barriers, if any, does your company face when it comes to retrofitting its fleet? [DO NOT READ LIST; ACCEPT MULTIPLE RESPONSES]

C. Fleet Energy Assessments

14. Has your company ever had a third party conduct an energy assessment of your fleet? [INTERVIEWER NOTE: IF ASKED, SAY: 'An energy fleet assessment is an analysis of your fleet's performance that can be used to help your company decide whether to invest in fuel-reducing technologies and retrofit your fleet.']

15. [IF Q14=01] How important are fleet energy assessments when determining which retrofits should be made to your fleet? [READ LIST]

SKIP TO Q18 UNLESS Q14=02 OR 03

16. [IF Q14=02,03] Would your company ever consider having a third party conduct an energy assessment of its fleet?

17. [IF Q16=02,03] Why hasn't your company considered a fleet energy assessment? [DO NOT READ LIST; ACCEPT MULTIPLE RESPONSES]

D. Government Programs

18. In your view, how important, if at all, are government funding programs that support fleet retrofits? [READ LIST]

19. Are you aware of the Government of Canada's Green Freight Assessment Program?

20. [IF Q19=02,03] The Green Freight Assessment Program, or GFAP, provides funding to companies for fleet retrofits and fleet energy assessments. Have you heard of this program?

21. Are you aware of any [INSERT BASED ON Q4: provincial / territorial] rebate programs for fleet retrofits?

22. Has your company participated in any government funding programs for fleet retrofits?

23. [IF Q22=01] Thinking about the government funding programs your company has participated in for fleet retrofits, how was funding provided? Was it… [READ LIST]

24. What type of funding would your company prefer to receive [IF Q22=02,03: if / Q22=01: when] participating in a government funding program for fleet retrofits? [READ LIST]

25. [IF Q10 ≠ 1 AND Q13=01] Earlier you said that cost is a barrier to retrofitting your company's fleet. Would the availability of government funding motivate your company to consider retrofitting its fleet?

26. What percentage of the fleet retrofitting cost would your company need funded by government incentives to make retrofitting financially feasible? Would you say… [READ LIST]

E. Repowering

Changing topics,

27. Are you aware that repowering your existing truck engines can be a cost-effective alternative to purchasing a new OEM vehicle? An engine repower consists of replacing an existing engine with a new one that has been certified to meet cleaner emission standards. [INTERVIEWER NOTE: IF ASKED, 'OEM' REFERS TO ORIGINAL EQUIPMENT MANUFACTURER]

28. Has your company repowered any of existing fleet engines?

29. [IF Q28=01] What percentage of your company's fleet engines have been repowered?

30. [IF Q28=01] Which fuel types do your company's repowered fleet use? [DO NOT READ; ACCEPT MULTIPLE RESPONSES]

SKIP TO Q34 UNLESS Q29=LESS THAN 100%

31. [IF Q29=<100%] Would your company consider repowering more of its fleet engines if some type of government funding was available?

SKIP TO Q34

32. [IF Q28=02,03] Is your company thinking about repowering any of its fleet engines in the next 2 to 3 years?

33. [IF Q32=02] Why is your company not interested in repowering any of its fleet engines? [DO NOT READ LIST; ACCEPT MULTIPLE RESPONSES]

F. Fleet Profile

These last questions are about your company's fleet.

34. What type of trucks are in your company's fleet? [IF HELPFUL, PROMPT BY READING SOME ITEMS; ACCEPT MULTIPLE RESPONSES]

35. Are your trucks used for… [READ LIST; ACCEPT MULTIPLE RESPONSES]

36. In an average day, how many kilometers do your trucks travel?

37. Does your company offer eco-driving training to its truck drivers? Eco-driving training refers to any training designed to improve drivers' knowledge of fuel efficiency techniques.

Finally,

38. What's your position within the company? [DO NOT READ LIST. ACCEPT ONE RESPONSE]

Thank you very much for your time and participation. The results of the research will be available to the general public, on the Library and Archives website, in the coming months.