Supporting Accessibility,

Inclusivity, and Retention in Energy Efficiency Programs - 2023

FINAL REPORT

Prepared for Natural Resources Canada

Supplier: Leger

Marketing Inc.

Contract Number: 2348-231017

Contract Value: $ 179,840.07 (including HST)

Award Date: February

21, 2023

Delivery Date: September

8, 2023

Registration Number: POR 138-22

For more information on

this report, please contact Natural Resources Canada at rop-por@ nrcan-rncan.gc.ca

Ce rapport est aussi disponible en

français

This public

opinion research report presents the results of a telephone survey conducted by

Léger Marketing Inc. on behalf of Natural

Resources Canada. The quantitative research study was

conducted with 2,082 Canadians who are homeowners residing in different regions

of Canada between March 16 and May 1st, 2023.

Cette publication

est aussi disponible en français sous le titre Soutenir l'accessibilité, l'inclusivité et la rétention dans les

programmes d'efficacité énergétique – 2023.

This publication

may be reproduced for non-commercial purposes only. Prior written permission

must be obtained from Natural Resources Canada. For more information on this

report, please contact: rop-por@ nrcan-rncan.gc.ca

Department of Natural Resources

DG S Office 15th Floor

580 Booth St.

Ottawa, Ontario

K1A0E5

Catalogue Number:

M4-226/2023E-PDF

International Standard Book Number

(ISBN):

978-0-660-49915-4

Related

publications (registration number: ROP 138-22):

·

M4-226/2023F-PDF

·

978-0-660-49916-1

© His majesty the King in Right of Canada, as represented by

the Minister of Natural Resources, 2023.

Table of contents

Executive

Summary. 5

1.1 Background and

Objectives. 5

1.2 Methodology. 6

1.3 Overview of the

Findings. 9

1.4 Notes on

Interpretation of the Research Findings. 18

1.5 Political

Neutrality Statement and Contact Information. 18

Detailed

Results. 19

2.1 Survey Results. 19

Type of home. 22

Indigenous primary

residences. 23

Residence square

footage. 24

Construction year of

the primary residence. 25

Last improvement of

energy efficiency. 26

Percentage of income

dedicated to paying monthly bills. 27

Monthly amount paid

for home energy bills. 29

Financial burden of

home energy costs. 30

Priority to improve

home energy efficiency. 31

Reasons for

improvements being a priority. 32

Reasons for

improvements NOT being a priority. 34

Disposable income

for a home improvement project 35

Planned energy

efficiency improvements. 37

Estimated Costs of

Energy Efficiency improvements. 39

Planned sources to

be used to minimize the financial burden of home energy improvement projects. 40

Awareness of

government resources and support programs for energy efficiency. 42

Familiarity with the

Canada Greener Home Grant 43

Application to the

Canadian Greener Home Grant 45

Reasons not to apply

to the Canadian Greener Home Grant 46

Reasons for making

home energy efficiency improvements. 46

Reasons or barriers

for not prioritizing home energy efficiency improvements. 49

On reserve

limitations to accessing home energy efficiency improvements. 52

Fair access to

government grants for visible minority communities. 52

Priorities when

choosing to make home improvements. 53

Incentives for less

home energy usage. 55

Psychographic

profile of respondents. 56

Main energy source

for home heating. 58

Possession of

energy-related items. 60

Likeliness of owning

energy-related items in the near-future. 62

Target Population

for the CGHG.. 68

Conclusion. 72

2.2 Methodological

recommendations. 74

Appendix. 75

A.1 Quantitative

Methodology. 75

A.2 Survey

Questionnaire. 82

Leger is pleased

to present Natural Resources Canada with this report on findings from a

quantitative survey designed to learn about Canadians who are homeowners

residing in different regions. This research follows the one conducted in 2022,

and some questions from the previous questionnaire were

removed as well as new questions were added to cover the gaps. This report was prepared by Léger Marketing Inc. who was contracted

by Natural Resources Canada (contract number 2348-23-1017 awarded February 21,

2023). This contract has a value of $159,150.50 (excluding HST).

Natural Resources Canada (NRCan) has a mandate through the Energy

Efficiency Act to promote energy efficiency, to make and enforce

regulations that prescribe standards and labelling requirements for

energy-using products and products that affect energy use, and to collect data

on energy use.

The Canada Greener Homes Grant (CGHG) program was launched in May

2021 to support homeowners in making energy efficiency, resiliency, and solar

retrofits for their homes while creating green jobs in the sector to advance

economic recovery. The program was immediately met with a high level of

interest from homeowners who quickly registered for the program.

However, many program applicants are ineligible for funding or are

unable to complete retrofits despite eligibility. Further research was needed

to inform program marketing to potential eligible applicants and reduce

barriers to accessing and completing the program.

A first study was launched in 2022 on this subject and the results

provided insight into who applied for this program and who did not. Natural

Resources Canada wanted to repeat this study, with a new sample, to see if

there have been any changes in the results over the past year.

The purpose of this study was to ensure that the CGHG program is

able to effectively reach homeowners and is inclusive of all demographic groups.

It is important for NRCan to have comprehensive data on who homeowners are,

where they live, characteristics of their households and homes, and their

attitudes and behaviours towards energy efficiency and conservation.

The research also covered the gaps from the previous research such

as affordability, possibility of taking on retrofit work and when, opinion of

Government programming, reasons why doing retrofit work, Indigenous

considerations, and types of retrofits of interest. Some questions from the

previous questionnaire were removed and new questions were added to cover the

gaps.

More specifically, the research objectives

were to combine elements of the 2021-22 survey with new

enquiry to expand the understanding of whom homeowners are, where they live,

characteristics of their households and homes, and their attitudes and

behaviours towards energy efficiency and conservation.

Overall, the research provided insights on the needs for, and

barriers to, accessing programs to enhance home energy efficiency. It also

provided behavioural insights on how homeowners make decisions in relation to

energy efficiency/conservation, which will inform NRCan program development and

implementation in this area.

The quantitative research

consisted of telephone interviews, which were conducted using a

computer-assisted telephone interviewing system (CATI technology).

To obtain reliable data for each

of the subgroups, we surveyed a total sample of 2,082 Canadian adults in all

regions of the country. Only one adult respondent was interviewed per

household. The national margin of error for this survey is +/- 2.15%, 19 times

out of 20.

Sample

Distribution

The sample frame

has been designed using a regional stratification scheme designed to accurately

reflect the geographic distribution of Canada’s population, including the North

(Yukon, Northwest Territories, and Nunavut). The following table describes the

regional quotas and the effective sample distribution achieved during the data

collection.

Table 1.

Sample Regional Distribution

|

Region

|

Quotas

|

Effective

Sample Size (n=)

|

Maximum

Margin of Error

|

|

Atlantic Canada

|

140

|

146

|

±8.1%

|

|

Quebec

|

450

|

453

|

±4.6%

|

|

Ontario

|

760

|

788

|

±3.5%

|

|

Prairies (MB, SK)

|

120

|

131

|

±8.6%

|

|

Alberta

|

240

|

248

|

±6.2%

|

|

British Columbia

|

260

|

286

|

±5.8%

|

|

Yukon, Northwest Territories and Nunavut

|

30

|

30

|

±17.9%

|

|

Total

|

2,000

|

2,082

|

2.1%

|

The population targeted in this

study was Canadian adults aged 18 and older who are homeowners. To meet the

objectives of this research, the sample also had to include sufficient

representation from the following key target groups:

· Indigenous

peoples (First Nations, Inuit, Métis);

· Members of the LGBTQ+ community;

· Those who identify as a visible minority;

· Newcomers to Canada (last 10 years was suggested as the cut-off

period);

· Persons living with a disability or in a household with someone who

is living with a disability.

Quotas Structure

As per the specific target groups

which need to be sufficiently represented to offer statistically valid results,

Leger proposed a structure with minimum quotas for each specific target.

The following table describes the

minimum quotas and the effective sample distribution achieved during the data

collection for each of those specific targets.

Table 2. Sample Size for

Specific Target Groups

|

Target Group (minimum quota)

|

Minimum Quotas

|

Effective

Sample Size (n=)

|

Maximum

Margin of Error

|

|

Indigenous peoples

|

100

|

101

|

±9.7%

|

|

Members of the LGTBQ

|

100

|

126

|

±8.7%

|

|

Those who

identify as a visible minority

|

220

|

293

|

±5.7%

|

|

Newcomers to

Canada

|

100

|

99

|

±9.8%

|

|

Persons

living with a disability

|

220

|

224

|

±6.5%

|

|

Total

|

640

|

717

|

±3.7%

|

Data

collection for this survey took place between March 16 and May 1st,

2023. The national response rate for the survey was 1.95%. The details of the

calculation of the response rate and the comprehensive distribution of calls are

presented in Appendix A. A pre-test of 42 interviews, in both official

languages, was conducted between on March 16, 2023. More specifically, 20

interviews were conducted in French and 22 in English. Since no problem was detected, data collection began

as planned. The pre-test responses were included in the overall results. The

interviews lasted an average of 20 minutes. The interviews were recorded to

assess the level of understanding of each issue in the population.

A proportion of the interviews were

conducted with a sample of cell-phone numbers (cell-phone-only household

members), in order to provide an adequate and reliable sample of the youth

cohort (18 to 34). In order to optimize the number of young Canadians who

participate in the survey, 250 interviews were conducted via a from lists of

cell-phone only households in Canada, as supplied by ASDE. While

the cell-phone sample did not exclusively target the youth cohort, this age

group was over-indexed in that target sample. The other interviews were

conducted with landline users.

According to 2021 national

census data from Statistics Canada, Leger weighted the results of this survey

by age, gender, region, and education level. Results were also weighted by specific

profile: Indigenous, immigrants, newcomers, visible minorities, respondents

living with a disability and LGBTQ2+ respondents in order to give back the real

weight of the respondents with this profile and prevent them from unbalancing

the whole sample due to the fact that they had been voluntarily overrepresented

in the sampling frame.

Leger

meets the strictest quantitative research guidelines. The questionnaire was

prepared in accordance with the Standards for the Conduct of Government of

Canada Public Opinion Research—Series D—Quantitative Research. Details on the

methodology, Leger’s quality control mechanisms, the questionnaire, and the

weighting procedures are provided in the appendix.

1.3 Overview of the Findings

Last

Improvement of Energy Efficiency

·

Just under half of Canadian homeowners (47%) indicated

that the last time that they upgraded their primary residence to make it more

energy efficient was less than 5 years ago.

·

Fewer than one out of five Canadian homeowners

(15%) indicated that their home was never renovated to improve energy

efficiency.

·

Homeowners aged 35 to 54 (50%), those living in

Ontario (51%), English-speaking homeowners (49%) who have an annual household

income higher than $150,000 (57%) have a significantly higher likelihood of

making energy efficiency improvements to their homes in the past 5 years.

· Homeowners residing in Alberta are more likely than other homeowners

to have indicated that their primary residence has never been improved for

energy efficiency (22%).

·

There are no significant variations compared to

last years’ results.

|

2022

|

2023

|

|

Sample size (n=)

|

2,919

|

2,082

|

|

Last 5 years

|

46%

|

47%

|

|

6 to 10 years ago

|

17%

|

18%

|

|

11 to 15 years ago

|

7%

|

8%

|

|

16 to 20 years ago

|

3%

|

3%

|

|

More than 20 years ago

|

3%

|

3%

|

|

Was never renovated to improve

energy efficiency

|

16%

|

15%

|

|

NET DK/REFUSAL

|

7%

|

6%

|

Q15: Based on what you know, when was the last time that a home

improvement was made to make your home more energy efficient? Base: All

respondents.

Energy

Efficiency

·

More than half of the respondents (53%) reported

that they spend more than $200 per month on home energy bills.

·

Homeowners in Alberta (74%), the Atlantic

Provinces (69%), and the territories (79%) are more likely than other

homeowners to report paying more than $200 per month for their primary

residence's energy bills.

· Homeowners whose primary residence is in a rural area are more

likely than homeowners living in urban areas to report paying more than $200

per month for their energy bill (59%).

·

There are no significant variations compared to

last years’ results.

|

2022

|

2023

|

|

Sample size (n=)

|

2,919

|

2,082

|

|

Under $50

|

2%

|

2%

|

|

Between $51 to $100

|

10%

|

10%

|

|

Between $100 to $200

|

32%

|

31%

|

|

Over $200

|

54%

|

53%

|

|

NET DK/REFUSAL

|

2%

|

4%

|

Q9: Based on your best guess, what is

the amount you pay each month for your home energy bills (electricity, gas,

etc.)? Is it…? Base: All respondents.

Financial

Burden of Energy Costs

·

Just over one in five Canadian homeowners (21%)

indicated that the energy costs of their primary residence are a significant

financial burden to them.

·

Homeowners living in Alberta (42%) and those who

have 35 to 54 years of age (25%) are statistically more likely to consider that

their primary residence's energy costs are a significant financial burden

(25%).

· There are no significant variations compared to last years’ results.

|

|

2022

|

2023

|

|

Sample size (n=)

|

2,919

|

2,082

|

|

My home energy costs are a significant

financial burden

|

21%

|

21%

|

|

My home energy costs are financially

manageable

|

51%

|

48%

|

|

My home energy costs are not a financial

burden

|

26%

|

27%

|

|

NET DK/REFUSAL

|

2%

|

4%

|

Q16. Which best describe your home energy costs (electricity, gas,

etc.): Base: All respondents.

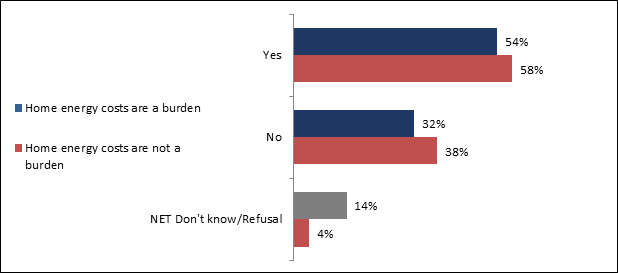

· Among Canadian homeowners whose home energy costs are a financial

burden, more than half (54%) consider it a significant enough burden that they

would make upgrading their home a priority to reduce energy bills and avoid

energy and heat loss. This proportion (58%) is similar among homeowners for

whom the energy cost of their home is not a financial burden.

· There are no significant variations compared to last years’ results.

|

Respondents for

whom home energy costs are a financial burden

|

Respondents for

whom home energy costs are NOT a financial burden

|

|

2022

|

2023

|

2022

|

2023

|

|

Sample size (n=)

|

538

|

392

|

2,333

|

1,611

|

|

Yes

|

55%

|

54%

|

58%

|

58%

|

|

No

|

31%

|

33%

|

37%

|

38%

|

|

NET DK/REFUSAL

|

15%

|

14%

|

5%

|

4%

|

Q17: You have mentioned that your home energy costs

are a burden to you. Is that burden significant enough that you would make it a

priority to upgrade your home to bring your home energy bills down or prevent

energy and heat loss? Base: Respondents for whom home energy costs are a

financial burden.

Q17B: Although you mentioned that energy costs are

not a burden to you, is it a priority for you to make energy efficiency

improvements to your home? Base: Respondents for

whom home energy costs are NOT a financial burden.

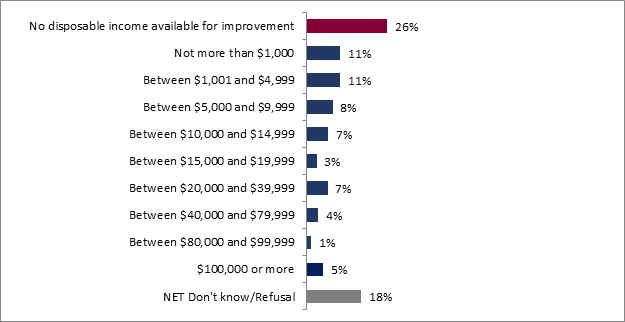

Disposable

Income for a Home Improvement Project

·

Around one quarter of Canadian homeowners (26%)

said they had no money available to make improvements to their primary

residence. Almost one in five homeowners (21%) reported having less than $5,000

available to make improvements to their property.

·

In comparison to last year's results, a

significantly higher number of homeowners indicated that they did not have more

than $1,000 saved aside to undertake a home improvement project, witnessing an

increase from 9% in 2022 to 11% in 2023.

·

Homeowners whose home is in Quebec and in the

Atlantic provinces are significantly more likely than others to have indicated

that they do not have any disposable income to make improvements to their

primary residence (36% and 37% respectively).

|

2022

|

2023

|

|

Sample size (n=)

|

2,919

|

2,082

|

|

No disposable income available for improvement

|

25%

|

26%

|

|

Not more than $1,000

|

9%

|

11%

|

|

Between $1,001 and $4,999

|

12%

|

11%

|

|

Between $5,000 and $9,999

|

9%

|

8%

|

|

Between $10,000 and $14,999

|

6%

|

7%

|

|

Between $15,000 and $19,999

|

3%

|

3%

|

|

Between $20,000 and $39,999

|

7%

|

7%

|

|

Between $40,000 and $79,999

|

5%

|

4%

|

|

Between $80,000 and $99,999

|

1%

|

1%

|

|

$100,000 or more

|

5%

|

5%

|

|

NET DK/REFUSAL

|

18%

|

18%

|

Q10: Approximately, how much disposable income do you have saved

aside if you needed or wanted to undertake a home improvement project?

Base: All respondents.

Familiarity

with the Canada Greener Homes Grant (CGHG)

·

A significantly higher number of homeowners indicated that they are aware of the Canada Greener

Home Grant, witnessing an increase from 21% in 2022 to 25% in 2023.

·

Homeowners residing in the Atlantic provinces,

as well as homeowners that identify themselves as being part of the LGBTQ2+

community are statistically more likely to know of the Canada Greener Homes

Grant (39% and 40% respectively).

·

A higher number of homeowners has also indicated

they are aware of the Energy Efficiency Regulations and Standards (from 26% in

2022 to 30% in 2023) and of the Energy Efficiency by Homes (from 34% in 2022 to

39% in 2023).

|

2022

|

2023

|

|

Sample size (n=)

|

1,617

|

1,131

|

|

Energy Savings ReABate Program

|

44%

|

48%

|

|

Energy Efficiency for Homes

|

34%

|

39%

|

|

Energy Efficiency for Products

|

30%

|

34%

|

|

Energy Efficiency Regulations:

Regulations and Standards

|

26%

|

30%

|

|

Canada Greener Home Grant

|

21%

|

25%

|

|

CMHC Green Home

|

22%

|

25%

|

|

Oil to Heat Pump Affordability

Grant*

|

-

|

19%

|

*New item

added in 2023 survey

Q21 and Q21B: Are you currently aware of

the following government resources and/or support programs for energy

efficiency? *Multiple answer allowed. Base: Respondents for whom making

upgrades to bring down home energy costs is a priority.

·

A significantly higher number of homeowners aware of the Canada Greener Home Grant indicated

that they are more familiar with this program compared to last year.

|

|

2022

|

2023

|

|

Sample size (n=)

|

351

|

285

|

|

Very familiar

|

9%

|

19%

|

|

Somewhat familiar

|

39%

|

39%

|

|

Somewhat unfamiliar

|

26%

|

28%

|

|

Very unfamiliar

|

23%

|

12%

|

|

NET DK/REFUSAL

|

3%

|

2%

|

Q22A and Q22B: How familiar are you with

the Canada Greener Home Grant Initiative? Base: Respondents who mentioned being

aware of the CGHG and for whom making upgrades to bring down home energy costs

is a priority.

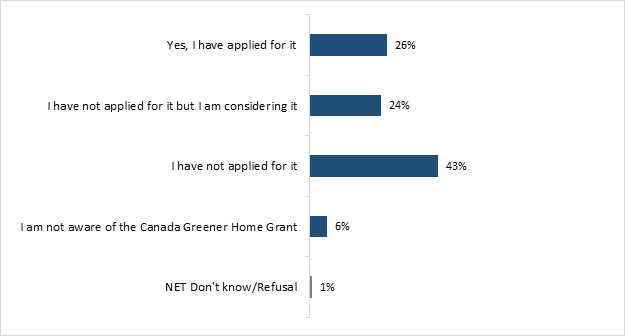

Application

to the Canada Greener Homes Grant (CGHG)

·

In comparison to last year's results, a

significantly higher number of homeowners indicated that they applied for the

CGHG, witnessing an increase from 18% in 2022 to 26% in 2023.

|

2022

|

2023

|

|

Sample size (n=)

|

340

|

280

|

|

Yes, I have applied for it

|

18%

|

26%

|

|

I have not applied for it, but I am

considering it

|

23%

|

24%

|

|

I have not applied for it

|

47%

|

43%

|

|

I am not aware of the Canada Greener Home

Grant

|

9%

|

6%

|

|

NET DK/REFUSAL

|

3%

|

1%

|

Q23 and Q23B:

Have you applied to the Canada Greener Home Grant? Base: Respondents who

mentioned being familiar, or unfamiliar with the CGHG, and for whom making

upgrades to bring down home energy costs is a priority.

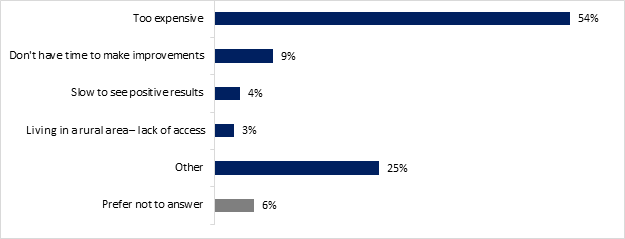

Reasons

Not to Apply to the Canada Greener Homes Grant

·

A few reasons were given by these homeowners for

not applying to the CGHG. They have indicated that the process is too

complicated (25%), that it is not needed (24%) that home improvements are too

expensive and out of their budget (16%), that they are not eligible or don’t

qualify (9%) or that the grant is that is available is too little to make a

difference (6%).

|

|

2022

|

2023

|

|

Sample size (n=)

|

158

|

123

|

|

Not needed (reno's are already

done, not renovating, new home, etc.)

|

28%

|

24%

|

|

Too complicated/unsure about the

process

|

28%

|

25%

|

|

Home improvements are too

expensive and outside my budget

|

12%

|

16%

|

|

Not eligible / Don't qualify

|

8%

|

9%

|

|

The grant that is available is too

little to make a difference

|

3%

|

6%

|

|

I don't trust that specific program

|

5%

|

5%

|

|

Don’t think the home improvements

will make a difference in home efficiency

|

3%

|

4%

|

|

Decision is up to the condo board

/ building administration

|

2%

|

1%

|

|

Too costly

|

2%

|

2%

|

|

Friend/family told me that this is

not useful for saving money or helping the environment

|

0%

|

1%

|

|

Other

|

4%

|

2%

|

|

Don't know

|

9%

|

12%

|

|

Prefer not to answer

|

1%

|

0%

|

Q24 and Q24B:

Why have you not applied for the Canada Greener Home Grant? *Multiple answer

allowed. Base: Respondents who mentioned not having applied to the CGHG.

Planned Energy

Efficiency Improvements

·

Replacing windows and doors, as well as

re-insulating are the two improvements most frequently mentioned by Canadian

homeowners. These are the same two priorities regardless of whether energy

costs are a financial burden to the respondent (52% and 48%) or not (38% and

35%). Other important improvements include air sealing the house (36% and 23%

respectively among those who consider home energy costs a financial burden and

those who do not), installing more energy efficient heating (36% and 28%).

·

Respondents for whom energy costs are not a

financial burden were less likely to plan to replace their windows and doors

compared to last year (from 46% in 2022 to 38% in 2023).

|

|

Respondents for

whom home energy costs are a financial burden

|

Respondents for

whom home energy costs are NOT a financial burden

|

|

2022

|

2023

|

2022

|

2023

|

|

Sample size (n=)

|

298

|

207

|

1319

|

924

|

|

Replacing windows and doors (This can include

Replacing doors and windows with Energy Star certified models)

|

57%

|

52%

|

46%

|

38%

|

|

Home insulation (This can include attic,

ceiling insulation, exterior wall insulation, exposed floor, basement, foundation)

|

43%

|

48%

|

35%

|

35%

|

|

Air Sealing a Home (This can include anything

that improves the air-tightness of your home)

|

30%

|

36%

|

21%

|

23%

|

|

More energy efficient heating (Can include

non-fossil fuel heating devices, installation of heat pumps)

|

36%

|

36%

|

27%

|

28%

|

|

Smart Thermostats

|

24%

|

29%

|

21%

|

22%

|

|

Updates that protect your home from

environmental damage (E.g. buying materials for home that protect it from

wildfires,

|

23%

|

25%

|

19%

|

16%

|

|

Installing solar panels

|

27%

|

22%

|

19%

|

16%

|

|

Roof / Shingles

|

1%

|

0%

|

1%

|

1%

|

|

Energy efficient appliances

|

0%

|

1%

|

0%

|

2%

|

|

Other – Specify

|

3%

|

1%

|

3%

|

2%

|

|

None / Nothing / Already done

|

2%

|

2%

|

5%

|

5%

|

|

Don’t know

|

8%

|

5%

|

8%

|

9%

|

|

Prefer not to answer

|

0%

|

1%

|

1%

|

1%

|

Q19 and Q19B: What energy efficiency improvements

do you plan to make to your home? *Multiple answers allowed.

Base: Respondents for whom home energy costs are a

financial burden and for whom making upgrades to bring down home energy costs

is a priority

Base: Respondents for whom home energy costs are NOT a

financial burden and for whom making upgrades to bring down home energy costs

is a priority.

Reasons

for Making Home Energy Efficiency Improvements

·

The first reason cited by respondents was the

desire to save money or reduce energy costs (81%) for those whose energy costs

are a burden versus 75% for those whose energy costs

are not a burden.

·

A higher number of homeowners indicated that

they are making their home more energy efficient to align with their values

(from 7% in 2022 to 13% in 2023).

·

A higher number of homeowners for whom energy

costs are not a burden indicated that they are making their home more energy

efficient to increase their property value (from 14% in 2022 to 18% in 2023)

and to take advantage of government incentives (7% in 2022 to 10% in 2023).

|

|

Respondents for whom home energy costs are a

financial burden

|

Respondents for whom home energy costs are NOT

a financial burden

|

|

|

2022

|

2023

|

2022

|

2023

|

|

Sample size (n=)

|

298

|

207

|

1,319

|

924

|

|

I have no specific reason to do it

|

2%

|

5%

|

2%

|

3%

|

|

Helping the environment - reducing

environmental footprint

|

27%

|

31%

|

39%

|

41%

|

|

Saving money - reducing operating costs/energy

costs

|

88%

|

81%

|

74%

|

75%

|

|

Increase property value

|

14%

|

14%

|

14%

|

18%

|

|

It aligns with my values

|

7%

|

13%

|

9%

|

14%

|

|

Replacing or updating old equipment

|

13%

|

12%

|

12%

|

14%

|

|

Aesthetic improvements toward energy efficient

updates

|

7%

|

8%

|

7%

|

6%

|

|

Emergency replacement

|

3%

|

2%

|

2%

|

3%

|

|

Taking advantage of government incentives

|

9%

|

9%

|

7%

|

10%

|

|

Increasing resiliency against environmental

factors (storms, floods, etc.)

|

7%

|

6%

|

7%

|

7%

|

|

Making my home more comfortable (less draughty

or stuffy, even temperatures)

|

24%

|

24%

|

25%

|

24%

|

|

To leave a better planet for future

generations

|

8%

|

7%

|

10%

|

13%

|

|

Save energy / Do not want to waste energy /

Use less energy / Energy efficient

|

0%

|

3%

|

3%

|

3%

|

|

Other – Specify

|

0%

|

1%

|

1%

|

1%

|

|

Don't Know

|

2%

|

0%

|

1%

|

1%

|

|

Prefer not to answer

|

0%

|

0%

|

1%

|

0%

|

Q27 and Q27B: What are your reasons for making your home more energy

efficient?

Base: Respondents for whom home energy costs are a financial burden

and for whom making upgrades to bring down home energy costs is a priority.

Base: Respondents for whom home energy costs are NOT a financial

burden and for whom making upgrades to bring down home energy costs is a

priority.

Reasons

for Not Prioritizing Home Energy Efficiency Improvements

·

The cost of improvements was the main reason

cited by homeowners whose energy costs are a burden (59%) compared to 19% for

those whose energy costs are not a burden.

·

Homeowners whose energy costs are a burden were also less likely to not prioritize energy efficiency

improvement because they are planning to make improvement in the future (from

13% in 2022 to 5% in 2023).

·

The fact that no improvements were needed at

this time was mentioned first by homeowners whose energy costs are not a burden

(45%), compared with 17% among the others. It was also mentioned by a higher

percentage of homeowners for whom energy costs are not a burden compared to

last year (38% in 2022 vs. 45% in 2023)

|

Respondents for whom home

energy costs are a financial burden

|

Respondents for whom home

energy costs are NOT a financial burden

|

|

Column %

|

2022

|

2023

|

2022

|

2023

|

|

Sample size (n=)

|

174

|

134

|

911

|

619

|

|

Improvements are too

costly

|

61%

|

59%

|

23%

|

19%

|

|

No improvements are

currently necessary

|

21%

|

17%

|

38%

|

45%

|

|

My home needs other

repairs before any energy efficiency improvements

|

14%

|

13%

|

14%

|

14%

|

|

Planning to sell

|

10%

|

12%

|

10%

|

8%

|

|

Energy efficiency is

not a valuable improvement

|

7%

|

10%

|

13%

|

10%

|

|

The home was

recently built

|

11%

|

9%

|

7%

|

6%

|

|

Do not have time

|

12%

|

6%

|

8%

|

8%

|

|

Planning to make

improvements in the future

|

13%

|

5%

|

11%

|

10%

|

|

The home was

recently purchased

|

5%

|

4%

|

16%

|

12%

|

|

Other – Specify

|

4%

|

4%

|

2%

|

2%

|

|

Decision is up to

the condo board / building administration

|

1%

|

0%

|

3%

|

2%

|

|

Don’t know

|

2%

|

0%

|

3%

|

1%

|

|

Prefer not to answer

|

0%

|

0%

|

0%

|

1%

|

Q28A and Q28B: What is the main reason or the

barriers for NOT prioritizing any energy efficiency improvements to your home?

Base: Respondents for whom home energy costs are a

financial burden and for whom making upgrades to bring down home energy costs

is not a priority

Base: Respondents for whom home energy costs are NOT

a financial burden and for whom making upgrades to bring down home energy costs

is not a priority

Likeliness

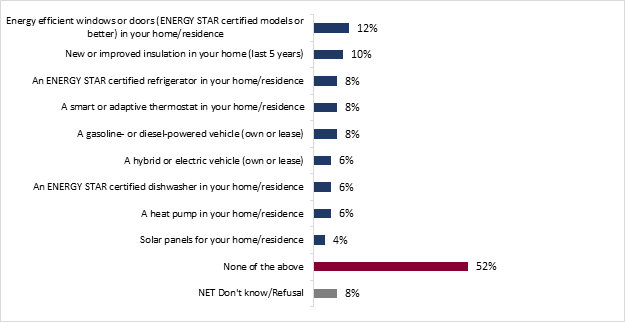

of Owning Energy-related Items in the Near-future

·

Half of the homeowners (52%) indicated that they

do not plan to purchase any energy efficient items or to improve the energy

footprint of their home. Slightly less than half (47%) of them indicated having

made home energy improvements in the last 5 years, while 15% of them stated

that no renovation was ever made to improve their home’s energy efficiency.

·

The likeliness of purchasing a hybrid or

electric vehicle, solar panels, or energy-efficient windows or doors has

decreased compared to last year.

|

2022

|

2023

|

|

Sample size (n=)

|

2,919

|

2,082

|

|

Energy efficient windows or

doors (ENERGY STAR certified models or better) in your home/residence

|

15%

|

12%

|

|

New or improved

insulation in your home

|

11%

|

10%

|

|

A gasoline- or

diesel-powered vehicle (own or lease)

|

8%

|

8%

|

|

A smart or adaptive

thermostat in your home/residence

|

9%

|

8%

|

|

An ENERGY STAR

certified refrigerator in your home/residence

|

9%

|

8%

|

|

A hybrid or electric

vehicle (own or lease)

|

10%

|

6%

|

|

A heat pump in your

home/residence

|

6%

|

6%

|

|

An ENERGY STAR

certified dishwasher in your home/residence

|

7%

|

6%

|

|

Solar panels for

your home/residence

|

6%

|

4%

|

|

None of the above

|

51%

|

52%

|

|

NET DK/REFUSAL

|

4%

|

8%

|

Q36: How likely are you to purchase any of the following in the NEXT

SIX MONTHS? *Multiple answer allowed. Base: All respondents.

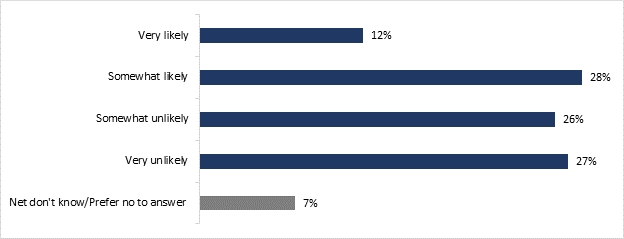

Impact of Current

Economic Context

·

While more than eight out of ten homeowners

(85%) are concerned about the current level of inflation in the economy, less

than half of them (40%) said that they are likely to prioritize their energy

efficiency upgrades for their home over other home improvements projects given

the economic context. Among those respondents, 12% claimed that they are very

likely to do so.

The opinions and

observations expressed in this document do not reflect those of Natural

Resources Canada. This report was compiled by Leger based on research conducted

specifically for this project. This research is probabilistic; the results can

be applied to the general population of Canada. The research was designed with

this objective in mind.

Leger certifies

that the final deliverables fully comply with the Government of Canada’s political

neutrality requirements outlined in the Policy on Communications and Federal

Identity and the Directive on the Management of Communications.

Specifically,

the deliverables do not include information on electoral voting intentions,

political party preferences, standings with the electorate, or ratings of the

performance of a political party or its leaders.

Signed by:

Christian Bourque

Executive Vice President and Associate

Leger

507 Place d’Armes, Suite 700

Montréal, Quebec

H2Y 2W8

cbourque@leger360.com

The composition of the sample collected for the research

project is detailed in table 3. Half of the sample (50%) identifies as female

while approximately half identifies as male (49%) and 1% identifies as another gender.

Two thirds of the survey respondents (67%) are 45 years of age or older, the

other third of respondents are 44 years of age or younger (33%). Approximately

one third of respondents (30%) have a university-level education, a little less

than half of respondents (43%) have a college or CEGEP-level education, and the

remaining respondents (26%) have less than a college or CEGEP-level education.

The regional distribution of respondents in Canada follows approximately the

distribution of the Canadian population. Three quarters of the sample lives in

an urban area (75%), while 21% lives in a rural area. Most respondents speak

English (78%), while around a quarter (23%) speaks French. Regarding incomes, a

quarter (26%) declares having an annual income of less than 60K, around half declare

having an annual income between 60k and 149K and less than a fifth (17%)

declare having an annual income of more than 150K.

Table 3. Demographic profile of the respondents

|

Gender

|

|

|

Female

|

50%

|

|

Male

|

49%

|

|

Other

|

1%

|

|

|

|

|

Age

|

|

|

18-24

|

3%

|

|

25-34

|

13%

|

|

35-44

|

17%

|

|

45-54

|

20%

|

|

55-64

|

21%

|

|

65+

|

26%

|

|

|

|

|

Education

|

|

|

High School or less

|

26%

|

|

Coll.

|

43%

|

|

Uni.

|

30%

|

|

|

|

|

Region of residence

|

|

|

British Columbia

|

13%

|

|

Alberta

|

12%

|

|

Saskatchewan

|

4%

|

|

Manitoba

|

3%

|

|

Ontario

|

38%

|

|

Quebec

|

20%

|

|

New Brunswick

|

2%

|

|

Nova Scotia

|

3%

|

|

Newfoundland and Labrador

|

2%

|

|

Prince Edward Island

|

1%

|

|

Yukon

|

1%

|

|

|

|

|

Urban or Rural Area

|

|

|

Urban

|

75%

|

|

Rural

|

21%

|

|

Language Spoken at Home*

|

|

|

English

|

78%

|

|

French

|

23%

|

|

Other

|

9%

|

|

*Multiple answer allowed.

|

|

|

Income

|

|

|

<60k$

|

26%

|

|

60K$-149k$

|

45%

|

|

150k+$

|

17%

|

The immigration status of survey respondents is detailed

in the next table. Eight out of ten respondents (80%) were born in Canada, and

one out of five (20%) were born outside the country.

Table 4. Immigration status

|

Born in Canada

|

80%

|

|

Born outside Canada

|

20%

|

Among respondents born outside of Canada, the majority (78%)

arrived in Canada before 2012. Of the remaining respondents who were born

outside of Canada, 18% arrived within the last ten years, and 4% chose not to

answer this question.

Table 5. Years of arrival in Canada

|

Before 2012

|

78%

|

|

2012-2023

|

15%

|

|

Prefer not to answer

|

4%

|

The composition of the sample by minority status is

presented in Table 6. Nearly two thirds of respondents (63%) do not belong to a

minority group. Among the respondents living in a minority situation, 19% claim

to belong to a visible minority, 11% claim to have a disability or limitation

of some kind, 4% identify as Indigenous (First Nations, Inuk (Inuit) or Metis)

and 6% identify as part of the LGBTQ2 community. A small proportion of

respondents (1%) chose not to answer this question.

Table 6. Minority profile

|

A member of the LGBTQ2 community

|

6%

|

|

A person with a disability

|

11%

|

|

A member of a visible minority group

|

19%

|

|

An Indigenous person (First Nations, Inuk (Inuit) or

Métis)

|

4%

|

|

None of the above

|

63%

|

|

Prefer not to answer

|

1%

|

Of the respondents who identified as Indigenous, most identified as

First Nations (63%), or Métis (33%). Few Indigenous respondents in the sample

identified themselves as Inuk (3%), while some (1%) preferred not to answer

this question.

Table 7. Indigenous profile

|

First Nations

|

63%

|

|

Inuk

|

3%

|

|

Metis

|

33%

|

|

Prefer not to answer

|

1%

|

Table 8 indicates the place of residence of these

respondents on or off reserve. The vast majority (81%) indicated that they

lived off reserve while just over one in ten (14%) indicated the opposite. A

small proportion of respondents (4%) chose not to answer this question.

Table 8. Living on reserve

|

Live on reserve

|

14%

|

|

Live off reserve

|

81%

|

|

Prefer not to answer

|

4%

|

The household composition of homeowners in Canada is detailed in table

9. Homeowners' households are mainly composed of more than one person. Only 20%

of homeowners reported living alone. Half (50%) reported having children under

the age of 18 living with them. Regarding the employment situation, more than 6

out of ten (61%) declare being employed, while around a third (29%) are

retired.

Table 9. Composition of the household

|

Household Size

|

|

|

1

|

20%

|

|

2

|

35%

|

|

3

|

19%

|

|

4+

|

26%

|

|

|

|

|

Children in the Household

|

|

|

Yes

|

50%

|

|

No

|

50%

|

|

|

|

|

Employment

|

|

|

Employed

|

61%

|

|

Unemployed

|

8%

|

|

Retired

|

29%

|

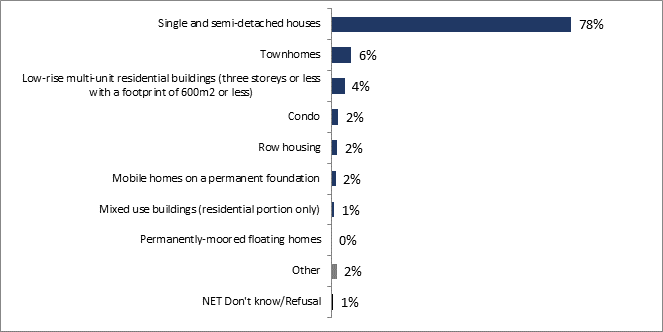

The majority of Canadian homeowners live in a single or

semi-detached home (78%) as their primary residence. Other types of primary

residences are less common. Less than 10% of homeowners live in townhouses

(6%), low-rise multi-unit residential buildings (three stories or less with a

footprint of 600 m2 or less) (4%), row houses (2%), mobile homes on a permanent

foundation (2%), condos (2%), mixed-use buildings (residential portion only)

(1%), or other types of residence (2%).

Figure 1: Type of home

Q11: What type of home (primary residence) do you currently live in?

Base: All respondents (n=2,082)

Notable subgroup differences regarding respondents’ type of home

include the following:

·

Younger homeowners

between 18 and 34 years of age were more likely than other homeowners to live

in row housing (18%). Homeowners aged 55 and older were more likely to live in

a single-family home (83%).

·

Homeowners living in

rural areas were more likely to live in single-family homes (91%), while

homeowners in urban areas were more likely to live in row housing (11%) and

apartment buildings (7%).

·

Homeowners who

identified themselves as visible minorities were more likely to live in row

houses (16%) while homeowners who did not identify as visible minorities were

more likely to live in single family homes (81%).

·

Immigrant homeowners

were more likely to live in row housing (23%), while non-immigrant homeowners

were more likely to live in single-family homes (79%).

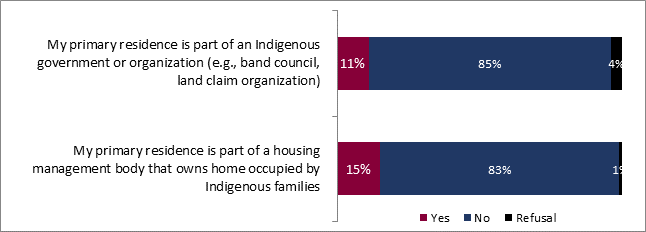

Approximately one out of ten (11%) indigenous

respondents report that their home is part of an Indigenous government or

organization (such as a band council or land claim organization), while 15% of

them report that their primary residence is part of a housing management

organization that owns housing occupied by Indigenous families.

Figure 2: Indigenous

primary residences

Q12: Do any of the following situations apply to you or your

principal residence? Base: Respondents who identify as Indigenous people (n=101)

No notable differences can be observed between different subgroups.

In comparison to last year's

report, a significantly lower number of homeowners indicated that their house

exceeded 2,400 sq. ft. (224 sq. meters or more), witnessing a decrease from 17%

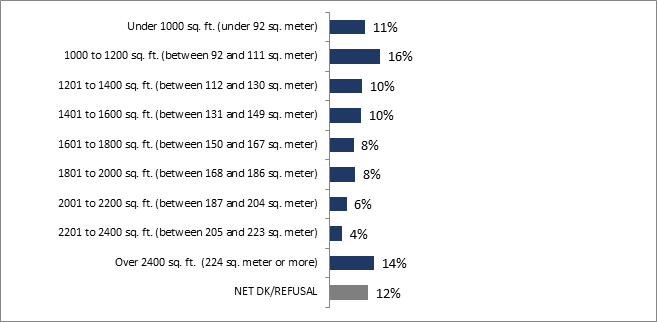

in 2022 to 14% in 2023.

This year, about one quarter of homeowners (24%) reported having

2001 square feet or more of living space, another quarter (26%) between 1401

and 2000 square feet, and the remaining 37% reported having less than 1400

square feet.

Figure 3: Living space square footage

of the residence.

Q14: What is the living space in square footage of your home? Base:

All respondents (n=2,082)

Notable subgroup differences regarding respondents’ type of home

include the following:

· Respondents who have an annual income of $150K or more are more likely

to have a home with a square footage of over 2400 sq. ft. (28%), while

respondent with an annual income of less than $ 60K are more likely to have a

home with a square footage of less than 1000 sq. ft. (28%)

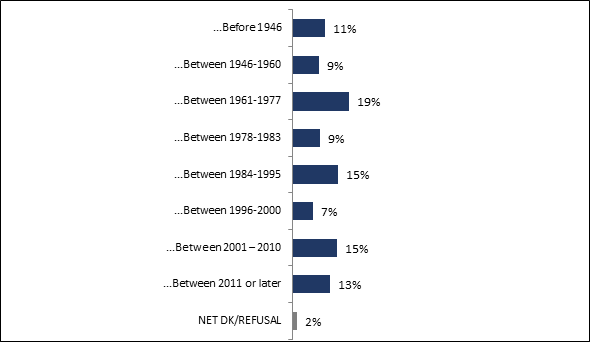

About one in ten (13%) Canadian

homeowners reported that their primary residence was built in or later than

2011. A little over one third of homeowners (37%) said their primary residence

was built between 1984 and 2010 and the same proportion (37%) said their

primary residence was built between 1946 and 1983. Finally, almost one out of ten

homeowners (11%) indicated that their primary residence was built before 1946.

Figure 4:

Construction year of the primary residence

Q13.1: In what year was your

residence built? Base: All respondents + Q13.2: Even if you do not know the exact year, would you say your

primary residence was built? (n=2,082)

Notable subgroup differences regarding respondents’

construction year of their primary residence include the following:

·

Men homeowners are

more likely to indicate that their home was built between 1961 and 1977 (17%), whereas

women homeowners tend to indicate that their home was built between 2001 and

2010 (16%).

·

Homeowners of 18 to

34 years old are more likely than other respondents to have mentioned that

their residence was built in the last 10 years (21%). Likewise, homeowners in

Alberta are more likely to have answered that their primary residence was built

in the last 10 years (23%).

·

Homeowners 55 and

older are more likely than other homeowners to have indicated that their home

was built between 1961 and 1995 (46%).

· Homeowners residing in Ontario are more likely than others to have

answered that the construction of their main residence occurred before 1946.

· Homeowners with a household income of less than $60,000 annually are

statistically more likely to have indicated that their home was built before 1946

(13%). Those with a household income of more than $150,000 annually are more

likely to live in a home that was built between 1984 and 1995 (19%) or within

the past 10 years (17%).

· Homeowners who identify as visible minorities are more likely than

non-minorities to have mentioned that their home was built between 2001 and

2010 (20%). Homeowners who immigrated to Canada are more likely to have

indicated that their home was built in 2011 or later (17%) and newcomers are

more likely to have indicated that their primary residence was built within the

past 10 years (27%).

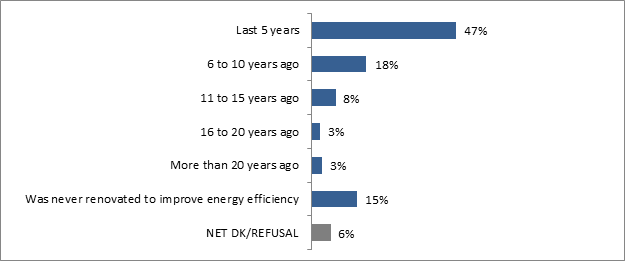

Nearly half of Canadian homeowners (47%) reported

upgrading their primary residence to improve energy efficiency in the last 5

years. Approximately one quarter of homeowners (26%) stated that their last

energy efficiency improvements were made between 6 and 15 years ago. A small

percentage of homeowners (6%) mentioned conducting energy efficiency retrofits

on their primary residence more than 15 years ago. Furthermore, 15% of

homeowners indicated that they never undertook any renovations to enhance

energy efficiency in their primary residence.

Figure 5: Last

improvement of energy efficiency

Q15: Based on what you know, when was the last time that a home

improvement was made to make your home more energy efficient? Base: All respondents (n=2,082)

Notable subgroup differences regarding respondents

last known renovations to improve their residence’s energy efficiency include

the following:

·

Homeowners aged 35 to

54 have a significantly higher likelihood (50%) of making energy efficiency

improvements to their homes in the last 5 years. Similarly, English-speaking

homeowners (49%) and those residing in Ontario (51%) also exhibit a greater

propensity for such enhancements. Additionally, homeowners with an annual

household income exceeding $150,000 are more likely (57%) to have made energy

efficiency improvements to their homes in the past 5 years.

·

Homeowners residing

in Alberta are more likely than other homeowners to have indicated that their

primary residence has never been improved for energy efficiency (22%).

In comparison to last year's results, a significantly

lower number of homeowners indicated that their monthly household income dedicated

to pay monthly bills was between 21% to 40%, witnessing a decrease from 24% in

2022 to 21% in 2023. The average percentage of the monthly household income

dedicated to pay monthly bills increased significantly, witnessing an increase

from 46,5% to 49,3%.

A little over a quarter (26%) of Canadian homeowners

reported that their monthly expenses (including all bills, mortgage, debt

payments and loans) exceeded 60% of their monthly household income. Almost one

out of five homeowners (21%) estimated this expense to be between 41% and 60%

of their household income. Another one fifth of homeowners (21%) estimated this

expense at between 21% and 40%, while 14% of respondents estimated this expense

at less than 20% of their household income.

Figure 6: Percentage of income dedicated to paying monthly

bills

Q8: Based on your best guess, what

percentage (%) of your total monthly household income is dedicated to paying

your monthly bills, including your mortgage and any other loans or debt

payments? Base: All respondents (n=2,082)

Notable subgroup differences regarding respondents’ percentage

of income dedicated to paying monthly bills include the following:

· Homeowners aged 55 years old and above are statistically more likely

to have reported that the percentage of their monthly income dedicated to

paying bills is 20% or less (19%).

· Homeowners who reside in the Atlantic provinces are among the

Canadian homeowners with the highest percentage of monthly income dedicated to

paying bills. They are statistically more likely to have indicated that 60% or

more of their monthly income is spent on bills (34%).

· Homeowners with household incomes over $150,000 per year have

indicated that they spend between 41% and 60% of their monthly income on bills

(26%) or 20% or less (21%). Homeowners with household incomes between $60,000

and $149,000 indicate that they spend between 21% and 40% of their monthly

income on bills (23%).

· English-speaking homeowners are statistically more likely to spend

60% or more of their monthly income on bills (27%).

· Homeowners who live in urban areas are more likely to spend between

21% and 40% of their monthly income on bills (23%) than homeowners who live in

rural areas.

With respect to monthly energy expenses (electricity,

gas, etc.), a very small number of Canadian homeowners (2%) reported having

energy costs of $50 or less per month. One in ten homeowners (10%) indicated

that their monthly energy costs for their primary residence were between $51

and $100, while almost one third of respondents (31%) estimated their monthly

energy costs to be between $100 and $200. More than half of the respondents (53%)

reported that they spend more than $200 per month on their home's energy needs.

A small proportion of respondents (4%) did not answer this question.

Figure 7: Monthly amount paid for home

energy bills

Q9: Based on your best guess, what is the

amount you pay each month for your home energy bills (electricity, gas, etc.)?

Is it…? Base: All respondents (n=2,082)

Notable subgroup differences regarding respondents’ monthly amount

paid for energy bills include the following:

· Homeowners in Alberta (74%), the Atlantic Provinces (69%), and the

territories (79%) are more likely than other homeowners to report paying more

than $200 per month for their primary residence's energy bills. Homeowners in

Quebec are more likely than others to report paying between $100 and $200 (37%)

or between $51 and $100 (18%) per month for their energy bills.

· Homeowners aged 18 to 34 years old are more likely than other age

groups to pay between $100 to $200 (40%) or between $51 to $100 (17%) per month

for their energy bills.

· French-speaking homeowners are more likely than others to pay

between $100 to $200 (38%) or between $51 to $100 (16%) per month for their

energy bills.

· Homeowners whose primary residence is in a rural area are more

likely than homeowners living in urban areas to report paying more than $200

per month for their energy bill (59%).

· Homeowners with an annual household income of more than $150,000 are

more likely to pay more than $200 per month for their energy bills (69%).

· Homeowners who identify themselves as LGBTQ2+ are more likely than

non-LGBTQ2+ homeowners to report paying between $51 to $100 (21%) and between $100

to $200 (41%) per month for their energy bills. However, they are less likely

to pay more than $200 per month (35%).

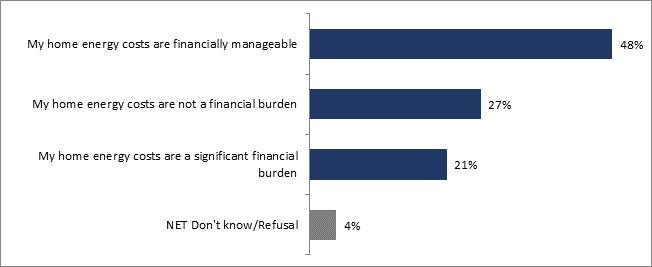

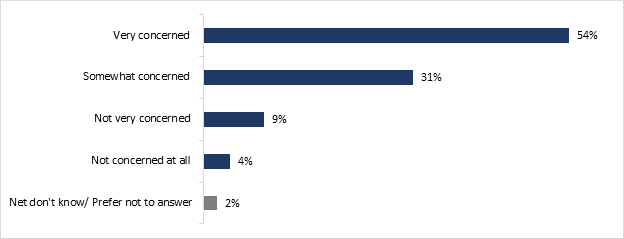

Just over one in five Canadian homeowners (21%) indicated that the

energy costs of their primary residence are a significant financial burden to

them. About one quarter (27%) of homeowners do not consider these costs to be a

financial burden. The remaining 48% of Canadian homeowners said that the energy

costs of their primary residence are manageable for their household.

Figure 8:

Financial burden of home energy costs

Q16: Which best describe your home energy costs (electricity, gas,

etc.):

Base: All respondents (n=2,082)

Notable differences among the subgroups regarding

their perception that their home energy costs are a financial burden are as follows:

·

Homeowners 35 to 54 years of age are

statistically more likely to have answered that their primary residence's

energy costs are a significant financial burden (25%). In contrast, homeowners

55 and older are statistically more likely to have said that home energy costs

are not a financial burden (31%).

·

French-speaking homeowners are statistically

more likely than others to have answered that their primary residence’s energy

cost are not a financial burden (39%).

·

Homeowners living in Alberta are significantly

more likely than other homeowners to have indicated that their home's energy

costs are a significant financial burden (42%), while homeowners living in

Quebec are significantly more likely to have answered that energy costs are not

a financial burden to their household (41%).

·

Homeowners with an annual household income of

less than $60,000 are more likely than other homeowners to consider their

home's energy costs a financial burden (28%) while those with an annual

household income of more than $150,000 are more likely than other homeowners

not to have considered their home's energy costs a burden (38%).

·

Homeowners with disabilities are statistically

more likely to have identified home energy costs as a significant financial

burden (36%).

·

Homeowners that identify as visible minorities

are statistically more likely than homeowners that don’t identify as a visible

minority to have identified home energy costs as a significant financial burden

(28%).

Among Canadian homeowners whose home energy costs are a

financial burden, more than half (54%) consider it a significant enough burden

that they would make upgrading their home a priority to reduce energy bills and

avoid energy and heat loss. This proportion (58%) is similar among homeowners

for whom the energy cost of their home is not a financial burden.

Figure 9: Priority

to upgrade home energy efficiency

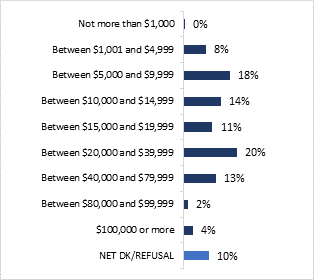

Notable subgroup differences regarding respondents estimated costs

of energy efficiency improvements among those who consider home energy costs a

financial burden include:

· Homeowners who identify as a visible minority, immigrant homeowners

as well as homeowners whose household income is less than $60,000 are

statistically more likely to have mentioned that they would need between $1,001

and $4,999 to make home improvements (18%, 24% and 17% respectively).

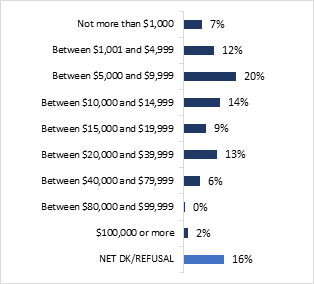

Notable subgroup differences regarding respondents estimated costs

of energy efficiency improvements among those who do not consider home energy

costs a financial burden include:

· French-speaking homeowners are statistically more likely to have

mentioned that they would need less than $10,000 to make home improvements

(46%). English-speaking homeowners are more likely to mention that that would

need between $20,000 and $39,999 to make home improvements (15%).

· Homeowners residing in British Columbia are statistically more

likely to have mentioned that they would need no more than $1,000 (13%), those

in Ontario are more likely to have mentioned that they would need between $10,000

and $14,999 (18%). Additionally, those in Quebec are more likely to have

mentioned that they would need less than $10,000 (47%) to make home

improvements.

· Homeowners with a disability are statistically more likely to have

mentioned that they would need between no more than $1,000 to make home

improvements (14%).

· Homeowners with an annual household income of less than $60,000 are

statistically more likely to have mentioned that they would need less than

$10,000 to make home improvements (47%).

· Homeowners with a college level degree are statistically more likely

to have mentioned that they would need between $5,000 and $9,999 (24%).

To finance their home improvement projects, homeowners

have slightly different plans depending on whether they consider their energy

expenses to be a burden or not. For those who consider home energy costs to be

a financial burden, taking advantage of government financial assistance and tax

credits for green retrofits (49%) was the preferred strategy followed by using

disposable income and savings (37%), using a personal line of credit (21%), financing

the retrofit through a mortgage (19%) or using a home-equity line of credit (16%).

For homeowners who did not consider energy expenses to be a burden, using

disposable income and savings (62%) was the preferred strategy, followed by

using government financial assistance and tax credits for green renovations (41%),

and using a home-equity line of credit (16%) or personal line of credit (14%).

Homeowners who viewed energy expenses as a burden were proportionally more

likely to report considering refinancing or remortgaging the home (14%)

compared to homeowners who did not view energy expenses as a burden (6%).

For those for

whom energy costs are a financial burden:

In comparison to

last year's results, a significantly lower number of homeowners indicated using

their home line of equity to minimize the financial burden of their home,

witnessing a decrease from 23% in 2022 to 16% in 2023.

Table 13: Planned sources to be used to minimize the financial

burden of your home energy improvement project

|

Home energy costs

are a financial burden

|

Home energy costs

are NOT a financial burden

|

|

Leveraging government financial assistance and

tax credits for eco-friendly home renovations

|

49%

|

41%

|

|

Disposable income and savings

|

37%

|

62%

|

|

Using a personal line of credit

|

21%

|

14%

|

|

Financing renovations into my mortgage

|

19%

|

12%

|

|

Using my home loan equity line of credit

|

16%

|

16%

|

|

Refinancing home/re-mortgage the house to pay

for renovations

|

14%

|

6%

|

|

Using money available through credit cards

|

6%

|

5%

|

|

None of the above

|

8%

|

8%

|

|

Unsure\Prefer not to answer

|

5%

|

2%

|

Q20 and Q20B: Which of the following sources do you plan to use to

minimize the financial burden of your home energy improvement project?

Base: Respondents for whom home energy costs are a financial burden

and for whom making upgrades to bring down home energy costs is a priority (n=207)

Base: Respondents for whom home energy costs are NOT a

financial burden and for whom making upgrades to bring down home energy costs

is a priority (n=924)

Notable subgroup differences regarding respondents’ planned sources

to be used to minimize the costs of home energy improvement projects among

those for whom energy costs are a financial burden include:

· Men homeowners are statistically more likely to have mentioned financing

renovations into their mortgage (25%)

· Homeowners aged 18 to 34 years old and those aged 35 to 54 are

statistically more likely not use any government financial assistance for home

renovations (88% and 79% respectively). Instead, homeowners in the 18 to 34 age

range predominantly rely on personal lines of credit (36%), whereas those aged

35 to 54 often opt refinancing or remortgaging their homes (20%) to fund their energy

renovation projects.

· English-speaking homeowners, as well as homeowners residing in urban

areas are statistically more likely to have mentioned using a personal line of

credit to fund their energy efficiency projects (24% and 26% respectively).

· Homeowners with a college level degree are more likely to use

government financial assistance and tax credits for eco-friendly home

renovations (57%).

· Homeowners with a household income of $60,000 to $149,000 are more

likely not to use any government financial assistance than others to fund their

energy renovation projects (84%).

Notable subgroup differences regarding respondents’ planned sources

to be used to minimize the costs of home energy improvement projects among

those for whom energy costs are not a financial burden include:

· Male homeowners are statistically more likely than women to finance

renovations into their mortgage (15%) and to refinance their home or

re-mortgage the house to pay for renovations (8%).

· Homeowners aged 35 to 54 years old are statistically more likely to use

government assistance to fund their energy renovation projects (47%).

· English-speaking homeowners are more likely than others to use

disposable income and savings (64%).

· Homeowners residing in Manitoba are statistically more likely to use

disposable income and savings than others to fund their energy renovation

projects (80%). Homeowners residing in Quebec are more likely to finance

renovations into their mortgage (21%).

· Homeowners residing in urban areas are more likely than homeowners

residing in rural areas to use their home loan equity line of credit to fund

their energy renovation projects (17%).

· Homeowners that identify themselves as a visible minority, immigrant

homeowners as well as homeowners with a household income of $60,000 to $149,000

are statistically more likely to finance renovations into their mortgages (23%,

17% and 15% respectively).

· Homeowners that identify themselves as being part of the LGBTQ2+

community are more likely to refinance their home or re-mortgage their house to

pay for renovations (20%).

· Homeowners with a household income of $150,000 and more and

homeowners with a university degree are statistically more likely to use

disposable income (74% and 69% respectively) and use government financial

assistance and tax for eco-friendly home renovations (50% and 49%

respectively).

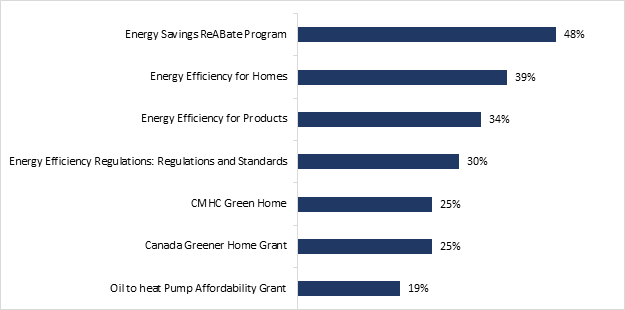

Of the federal programs available to provide resources

and support for improving energy efficiency in primary residences, the Energy

Saving Rebate Program (48%), the Energy Efficiency for Homes (39%), and the Energy

Efficiency for Products (34%) were the three most well-known programs. Energy

Efficiency Regulations: Regulations and Standards (30%), Canada Greener Home

Grant (CGHG) (25%), CMHC Green Home (25%) and Oil to Heat Pump Affordability

Grant (19%) were somewhat less known among Canadian homeowners.

In comparison to

last year's results, a significantly higher number of homeowners indicated they

are aware of the Energy Efficiency Regulations and Standards, witnessing an

increase from 26% in 2022 to 30% in 2023. A significantly higher number of

homeowners indicated that they are aware of the Energy Efficiency by Homes,

witnessing an increase from 34% in 2022 to 39% in 2023. A significantly higher

number of homeowners indicated that they are aware of the Canada Greener Home

Grant, witnessing an increase from 21% in 2022 to 25% in 2023.

Figure 12: Awareness of government resources and support programs

for energy efficiency

Q21 and Q21B: Are you currently aware of the following government

resources and/or support programs for energy efficiency?

Base: Respondents for whom home energy costs are a financial burden

and for whom making upgrades to bring down home energy costs is a priority (n=207)

Base: Respondents for whom home energy costs are NOT a

financial burden and for whom making upgrades to bring down home energy costs

is a priority (n=924)

Notable subgroup differences regarding

respondents’ awareness of federal government resources

and support programs for energy efficiency include:

·

British Columbia respondents and those whose

household income is over $150,000 were more likely to be aware of the Energy

Savings ReABate Program (58% and 63% respectively)

·

Homeowners residing in the Atlantic provinces, as

well as homeowners that identify themselves as being part of the LGBTQ2+

community are statistically more likely to know of the

Canada Greener Homes Grant (39% and 40% respectively).

·

English-speaking respondents were significantly

more likely to know of all the programs, but the Canada Greener Home Grant

compared to other respondents.

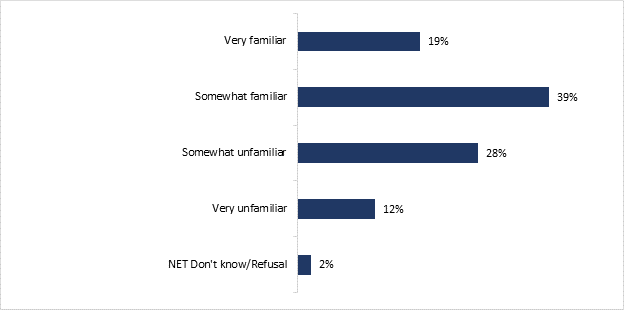

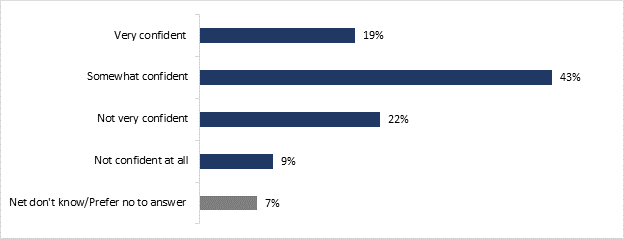

Familiarity with the CGHG is relatively split among

Canadian homeowners. About six homeowners out of ten (58%) said they were

familiar with the Grant, while four out of then (40%) said they were not

familiar with the CGHG. Almost one out of five homeowners are very familiar (19%)

with the program, while nearly one out of ten (12%) indicated that they are very

unfamiliar with the CGHG.

In comparison to

last year's results, a significantly higher number of homeowners indicated that

they were familiar with the Canada Greener Home Grant, witnessing an increase

from 49% in 2022 to 58% in 2023. A significantly higher number of homeowners

indicated that they are very familiar with the CGHG, witnessing an increase

from 9% in 2022 to 19% in 2023. A significantly lower number of homeowners

indicated that they were very unfamiliar with the CGHG, witnessing a decrease

from 23% in 2022 to 12% in 2023.

Figure 13: Familiarity with the Canada Greener Home Grant

Q22A and Q22B: How familiar are you with the Canada

Greener Home Grant Initiative?

Base: Respondents who mentioned being aware of the

CGHG and for whom making upgrades to bring down home energy costs is a priority

(and home energy costs are a financial burden n=52)

Base: Respondents who mentioned being aware of the

CGHG and for whom making upgrades to bring down home energy costs is a priority

(and home energy costs are NOT a financial burden n=233)

Note: A total familiar (very + somewhat familiar) and a total

unfamiliar (somewhat + very unfamiliar) were calculated for analysis purposes.

The following subgroups were especially likely to be

very or somewhat familiar with the CGHG:

·

Homeowners for whom English is the primary

language spoken at home are significantly more likely to have reported being

familiar with the Canada Greener Home Grant (64%) than other homeowners.

·

Homeowners residing in Atlantic provinces are

significantly more likely to have reported being familiar with the Canada

Greener Home Grant (76%) than other homeowners.