Evaluation of the Receiver General for Canada—Volume 1 (final report)

March 31, 2016

On this page

Main points

i. The Receiver General for Canada (RG) is one of the oldest functions in the administration of government and can be traced back through Canada's history to 1764. The Minister of Public Works and Government Services is the designated RG and as such is the Custodian of the Consolidated Revenue Fund, the account into which the Government deposits taxes, tariffs, excises and other revenues, once collected, and from which it withdraws the money it requires to cover its expenditures. The RG has 3 client groups: federal departments and agencies, Parliamentarians, and the Canadian Public.

ii. In fulfillment of their role as the RG, the Minister of Public Works and Government Services is responsible for providing crucial treasury and accounting functions to Canadian citizens and businesses on behalf of federal departments and agencies, which result in annual cash flow transactions totaling more than $2.3 trillion through the Consolidated Revenue Fund. There are 3 mandatory services that are provided under these treasury and accounting functions: processing of payments to the public (over 313 million payments per year); processing of deposits for the receipt of payments from the public (over 40 million transactions per year); and the maintenance of the Accounts of Canada and the preparation of the Public Accounts of Canada (the annual financial report of the Government of Canada).

iii. This evaluation is reported in 2 volumes. Volume 1 examines the RG's 3 mandatory treasury and accounting services noted above. In addition to these mandatory services, the RG also provides Receiver General Services, which includes the Bill Payment Service Program and an optional departmental financial and materiel management system offering. These services are examined in Volume 2 of this evaluation with the exception of the optional departmental financial and materiel management system offering which is being phased out as client departments and agencies transition to the SAP system.

iv. There is an ongoing need for the centralized delivery of the RG's services. The RG supports critical government programming (for example Old Age Security, Canada Pension Plan, and Employment Insurance) upon which many Canadians rely to sustain their livelihood (approximately 60% of payments issued to Canadians by the RG were the only or main source of income for the recipients) or fulfill their civic duty (for example paying taxes). The centralized provision of these treasury and accounting services also supports Parliament in fulfilling its role of ensuring sound stewardship of the management and administration of public funds.

v. The services provided by the RG support the priorities of Public Works and Government Services Canada and the federal government as a whole. By providing treasury and accounting services on behalf of other government departments and agencies that help ensure the sound stewardship of public funds, the RG supports the strategic outcome of Public Works and Government Services Canada. Additionally, it supports key values, such as ensuring fiscal prudence and efficiently delivering services in a way that makes citizens feel respected and valued, that were outlined in the Prime Minister's 2015 Ministerial Mandate Letter for the Minister of Public Works and Government Services.

vi. The provision of the RG's services by Public Works and Government Services Canada complements the functions of other federal organizations. Per the Government of Canada's legislative and policy framework, Public Works and Government Services Canada is a common services agency mandated to provide services on behalf of other federal departments and agencies. The RG's key partners (the Treasury Board of Canada Secretariat, Office of the Comptroller General, and Department of Finance) provide policy and functional guidance which ultimately supports the RG's delivery of its services. This model is aligned with practices in international jurisdictions.

vii. The RG is achieving its outcomes in that it is efficiently delivering its treasury and accounting services in a timely and accurate manner. Client perceptions of the timeliness and accuracy of services provision were high. While it was noted that the Public Accounts process was difficult and the layout was hard to understand, these issues are beyond the RG's realm of influence. Ultimately, the RG is delivering its services in a manner that supports Public Works and Government Services Canada's achievement of its Strategic Outcome of delivering high-quality, central programs and services that ensure sound stewardship on behalf of Canadians and meet the program needs of federal institutions.

viii. Additionally, the RG operates in an efficient and economical manner. Significant cost pressures for the Program were identified for remittances and payments. As such, resources were managed economically. Expenditures and full-time-equivalents were relatively stable and within budget. Evidence indicated that the treasury outputs (remittances and payments) were provided in an efficient manner. It was noted that further centralization of services could improve efficiencies; this is being examined as part of the RG's Modernization Initiative.

ix. Given the strong performance of the RG, the lack of identified issues in the achievement of outcomes, the economical and efficient delivery of the Program, and in recognition that the RG Modernization Initiative is expected to addresses issues noted in the evaluation, recommendations were not provided to the management of the Accounting, Banking, and Compensation Branch.

Introduction

1. This evaluation examined the ongoing relevance and performance of the Receiver General for Canada (RG). The RG is located as sub-program 1.3 in the 2014 to 2015 Program Alignment Architecture for Public Works and Government Services Canada (PWGSC). This evaluation was divided into 2 volumes: Volume 1: Stewardship of Consolidated Revenue Fund and Accounts of Canada (sub-program 1.3.1), and Volume 2: RG Services (sub-program 1.3.2). The Program is administered by the Accounting, Banking and Compensation Branch.

Profile

Background

2. The RG is one of the oldest functions in the administration of government and can be traced back through Canada's history to 1764. While it has seen its roles and functions evolve since that time, the RG has served as the Government's treasurer, custodian, and accountant for the past 250 years.

3. The RG is the Custodian of the Consolidated Revenue Fund, the account into which the Government deposits taxes, tariffs, excises and other revenues, once collected, and from which it withdraws the money it requires to cover its expenditures. As the RG and custodian of the Consolidated Revenue Fund, the Minister of Public Works and Government Services is responsible for providing 3 crucial services to Canadian citizens and businesses, discussed in detail below, which result in annual cash flow transactions totaling more than $2.3 trillion.

4. First, the RG issues payments to government, individuals and businesses out of the Consolidated Revenue Fund on behalf of federal government departments and some provincial governments. These payments are made to other government departments and other levels of government, as well as to Canadian citizens and businesses, both in Canada and around the world in support of critical government programs (for example Old Age Security, Canada Pension Plan, and Employment Insurance). Approximately 60% of RG payments issued to Canadians were the only or main source of income for the recipients. Payments can be made in Canadian funds or in a multitude of other currencies. The RG processes over 313 million payments to the public on an annual basis.

5. Second, the RG accepts payments to the Government of Canada into the Consolidated Revenue Fund. The RG manages all banking arrangements with financial institutions (banks, credit unions, trust companies, caisses populaires) to accept and process payments to the federal government. The RG processes approximately 800,000 deposits which represents more than 40 million transactions annually.

6. Finally, the RG is responsible for maintaining the Accounts of Canada and preparing the Public Accounts of Canada. More specifically, the Public Accounts of Canada is the financial report of the Government of Canada prepared annually by the Receiver General that covers the fiscal year of the Government, which ends on March 31. As part of this role, the RG must publish the Public Accounts of Canada as required by section 64 of the Financial Administration Act.

7. The fundamental purpose of the Public Accounts of Canada is to provide information to Parliament, and thus to the public, which will enable them to understand and evaluate the financial position and transactions of the government. Two constitutional principles underlie the public accounting system: that duties and revenues accruing to the Government of Canada form one Consolidated Revenue Fund, and that the balance of the Fund after certain prior charges is appropriated by the Parliament of Canada for the public service.

8. The information contained in the Public Accounts of Canada originates from 2 sources of data:

- the summarized financial transactions presented in the Accounts of Canada, maintained by the Receiver General

- the detailed departmental/agency account records of individual transactions, maintained by departments and agencies

9. The departmental/agency account records must show all expenditures made under each appropriation, all government revenues, and all other payments into and out of the Consolidated Revenue Fund, together with the assets and liabilities, the contingent liabilities of Canada and the related reserves that are deemed necessary to present a fair picture of the country's financial position.

Authority

10. The Department of Public Works and Government Services Act identifies the Minister of Public Works and Government Services as the Receiver General for Canada. The authority for the RG function derives from the Financial Administration Act.

Roles and responsibilities

11. The Accounting, Banking and Compensation Branch of PWGSC is responsible for the delivery of the Stewardship of the Consolidated Revenue Fund and Accounts of Canada Sub-Program. Within the Branch, responsibility for the administration of the Program is shared between the Central Accounting and Reporting Sector; Banking and Cash Management Sector; and Cheque Redemption Control Directorate.

12. The RG has 3 levels of clients. First, the RG's operational clients are all departments and agencies with which they work as part of the maintenance of the Accounts of Canada and preparation of the Public Accounts of Canada. It should be noted that the consolidated financial statements are prepared under the joint direction of the President of the Treasury Board, the Minister of Finance, and the Receiver General for Canada (Minister of Public Works and Government Services) in compliance with governing legislation. Additionally, the Government presents the consolidated financial statements to the Auditor General of Canada, who audits them and provides an independent audit opinion to the House of Commons.

13. Second, under Standing Orders, the Public Accounts of Canada are deemed permanently referred to the Standing Committee on Public Accounts as soon as they are tabled in the House of Commons. As the decision-making client for the RG, Parliamentarians use the information provided in the Public Accounts to understand and evaluate the financial position and transactions of the government. The House of Commons uses the Public Accounts to ensure that federal money is spent in the amounts and for the purposes authorized by Parliament.

14. Finally, as Custodian of the Consolidated Revenue Fund, the RG manages federal funds on behalf of the ultimate client, the Canadian public.

Resources

15. The RG has a net-voted budget. Net voting is an alternative means of funding selected programs or activities wherein Parliament authorizes a department to apply revenues towards costs incurred and votes the net financial requirements (estimated total expenditures minus estimated revenues). In 2014 to 2015, the RG expenditures, as Custodian of the Consolidated Revenue Fund, were $130 million and the services were delivered by 332 employees (full time equivalents).

Logic model

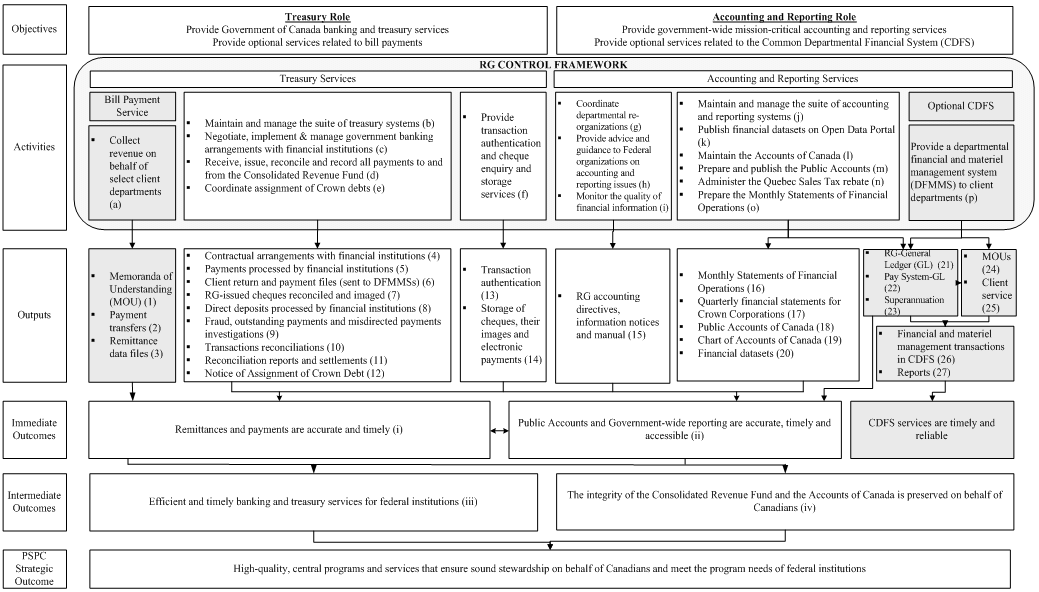

16. A logic model is a visual representation that links a program's activities, outputs and outcomes; provides a systematic and visual method of illustrating the program theory; and shows the logic of how a program is expected to achieve its objectives. It also provides the basis for developing the performance measurement and evaluation strategies, including the Evaluation matrix.

17. A logic model for the Program was developed based on a detailed document review, meetings with program managers and interviews with key stakeholders. It was subsequently validated with program staff. The logic model is provided in Exhibit 1: Logic model. The services not examined as part of this evaluation are indicated by the grey boxes.

Exhibit 1: logic model

Description for Exhibit 1

Exhibit 1 depicts the logic model of the Receiver General for Canada. Going from the top down, the model describes the program's roles, objectives, activities, outputs, immediate outcomes, intermediate outcomes, strategic outcome, and the linkages between them.

Roles

The logic model separates the Program into 2 roles: a treasury role and an accounting and reporting role.

Objectives

The Program has 2 objectives under the treasury role:

- provide Government of Canada banking and treasury services

- provide optional services related to bill payments

The Program has 2 objectives under the accounting and reporting role:

- provide government-wide mission-critical accounting and reporting services

- provide optional services related to the Common Department Financial System (CDFS)

Activities and outputs

In the logic model, the activities are divided into 2 sections:

- Treasury Services

- Accounting and Reporting Services

The treasury service activities are separated into 3 different textboxes.

The first textbox includes the following activity:

- Bill Payment Service: Collect revenue on behalf of select client departments (a)

This activity leads to the following outputs:

- Memorandums of Understanding (MOUs) (1)

- payment transfers (2)

- remittance data files (3)

The second textbox includes the following activities:

- maintain and manage the suite of treasury systems (b)

- negotiate, implement & manage government banking arrangements with financial institutions (c)

- receive, issue, reconcile and record all payments to and from the Consolidated Revenue Fund (CRF) (d)

- coordinate assignment of Crown debts (e)

These activities lead to the following outputs:

- contractual arrangements with financial institutions (4)

- payments processed by financial institutions (5)

- client return and payment files (sent to Departmental financial and materiel management system (DFMMSs)) (6)

- RG-issued cheques reconciled and imaged (7)

- direct deposits processed by financial institutions (8)

- fraud, outstanding payments and misdirected payments investigations (9)

- transactions reconciliations (10)

- reconciliation reports and settlements (11)

- notice of Assignment of Crown Debt (12)

The third textbox includes the following activity:

- provide transaction authentication and cheque enquiry and storage services (f)

This activity leads to the following outputs:

- transaction authentication (13)

- storage of cheques, their images and electronic payments (14)

The accounting and reporting services activities are separated into 4 different textboxes.

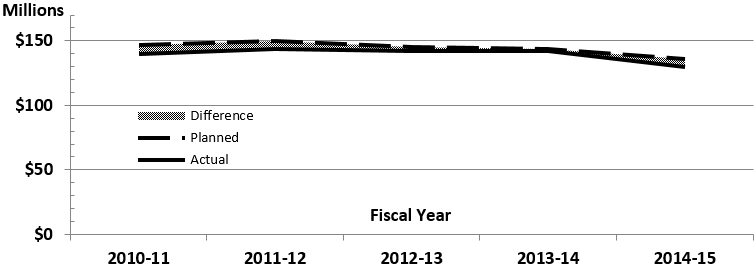

The first textbox includes the following activities:

- coordinate departmental re-organizations (g)

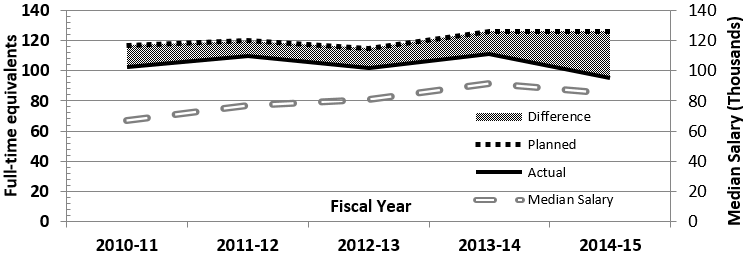

- provide advice and guidance to Federal organizations on accounting and reporting issues (h)

- monitor the quality of financial information (i)

These activities lead to the following output:

- RG Accounting directives, information notices and manual (15)

The second textbox includes the following activities:

- maintain and manage the suite of accounting and reporting systems (j)

- publish financial datasets on Open Data Portal (k)

- maintain the Accounts of Canada (l)

- prepare and publish the Public Accounts (m)

- administer the Quebec Sales Tax rebate (n)

- prepare the Monthly Statements of Financial Operations (o)

These activities lead to the following outputs:

- Monthly Statements of Financial Operations (16)

- quarterly financial statements for Crown Corporations (17)

- Public Accounts of Canada (18)

- Chart of Accounts of Canada (19)

- financial datasets (20)

The third textbox includes the following activity:

- Optional CDFS: Provide a departmental financial and materiel management system (DFMMS) to Client Departments (p)

This activity leads to the following outputs that are contained in 2 textboxes:

- RG General Ledger (21)

- Pay system (PS) General Ledger (22)

- superannuation (23)

- MOUs (24)

- client service (25)

The outputs contained in these 2 textboxes lead to the following outputs:

- financial and materiel management transactions in CDFS (26)

- reports (27)

Immediate outcomes

The program has 3 immediate outcomes.

The treasury services outputs lead to the following outcome:

- Remittances and payments are accurate and timely (i)

The accounting and reporting services outputs lead to the following 2 outcomes:

- Public Accounts and Government-wide reporting are accurate, timely and accessible (ii)

- CDFS services are timely and reliable

Intermediate outcomes

The program has 2 intermediate outcomes.

The treasury services immediate outcome leads to the following intermediate outcome:

- efficient and timely banking and treasury services for Federal Institutions (iii)

The accounting and reporting services immediate outcome leads to the following intermediate outcome:

- the integrity of the Consolidated Revenue Fund and the Accounts of Canada is preserved on behalf of Canadians (iv)

Public Works and Government Services Canada Strategic Outcome

The 2 intermediate outcomes lead to the following PWGSC strategic outcome:

- high-quality, central programs and services that ensure sound stewardship on behalf of Canadians and meet the program needs of federal institutions

Program activities

18. Optional Bill Payment Service (the optional, non-banking, components of the Bill Payment Service) – this activity is examined in Volume 2 of this evaluation.

- Collect revenue on behalf of select client departments and agencies: Provides value-added services in support of the Bill Payment Service Program. The Bill Payment Service Program offers a range of electronic services as well as optional paper-based services to participating Bill Payment Service departments

19. Treasury services:

- Maintain and manage the suite of treasury systems: Provides operational support, change management and configuration/release management for the treasury systems

- Negotiate, implement & manage government banking arrangements with financial institutions: Manages all banking arrangements with financial institutions to accept and process payments to and from the federal government

- Receive, issue, reconcile and record all payments to and from the Consolidated Revenue Fund:

- issues payments on behalf of federal government departments and some provincial governments and provides post-issue support

- reconciles payments cleared through the Bank of Canada

- Coordinate assignment of Crown debts: Coordinates the assignment of Crown debts under part VII of the Financial Administration Act

- Provide transaction authentication and cheque enquiry and storage services:

- ensures that requisitions for cheques, direct deposits, and Large Value Transfer System and Electronic Data Interchange payments are authentic and certified by an authorized person

- provides fraud detection services, secure storage of all cheques, cheque imaging and electronic payments

20. Accounting and reporting services:

- Coordinate departmental re-organizations: Provides general accounting and reporting requirements for departments or agencies impacted by reorganization. Coordinates set-up, testing, and implementation of information management systems that support accounting and reporting requirements

- Provide advice and guidance to federal organizations on accounting and reporting issues: Provides advice and direction on accounting and reporting issues, which includes the RG Manual, Directives, and Information Notices

- Monitor the quality of financial information: Monitors the quality of financial information in the departmental trial balances submitted monthly to the RG

- Maintain and manage the suite of accounting and reporting systems: Manages and maintains the suite of central accounting systems

- Publish financial datasets on Open Data Portal: Publishes financial datasets on Open Data Portal, as a participant in the Government's Open Data initiative

- Maintain the Accounts of Canada: This function includes maintaining and publishing the government-wide Chart of Accounts:

- departments and agencies are required to submit their summarized financial transactions on a monthly basis, which are added to the Accounts of Canada, the primary information source for government-wide financial reports

- the Chart of Accounts provides the framework for identifying, collecting, and reporting the government's financial transactions

- Prepare and publish the Public Accounts: Prepares and publishes the Public Accounts of Canada which includes the annual audited consolidated financial statements of the Government of Canada for each fiscal year which ends on March 31

- Administer the Quebec Sales Tax rebate: Submits a monthly claim for rebate to Revenu Québec and upon receipt, distributes the rebate to government departments on behalf of the Government of Canada

- Prepare the Monthly Statements of Financial Operations: Prepares the monthly financial statements for the Government of Canada which are used by the Department of Finance to prepare its monthly Fiscal Monitor

21. Optional Common Departmental Financial System

- Provide a departmental financial and materiel management system (DFMMS) to client departments and agencies: In 2012, the Treasury Board's Standard on Enterprise Resource Planning Systems required that new investments in or upgrades to existing financial or materiel management systems result in the implementation of SAP in accordance with the policy direction of the Office of the Comptroller General and the Government of Canada's Chief Information Officer Branch which both reside at the Treasury Board of Canada Secretariat. As a result of this requirement, the RG's offering of an optional DFMMS is being phased out as its client departments and agencies transition to the SAP system. As a result, the Evaluation did not assess the relevance or the performance of the optional DFMMS Program

Focus of the evaluation

22. The objective of this evaluation was to determine the Program's relevance and performance in achieving its expected outcomes in an economical and efficient manner in accordance with the Treasury Board Policy on Evaluation. The Evaluation assessed the Program for the period of April 2010 to March 2015. It is the first evaluation of the RG.

Approach and methodology

23. Five lines of evidence were used to assess the Program. These were:

- Program document review: Documents reviewed provided information on the Program and its context for the planning phase of the Evaluation and also provided information for the assessment of the Evaluation questions

- Literature review: Literature was reviewed to obtain information on the Program and its context for the planning phase of the Evaluation and also provided information for the assessment of the Evaluation questions

- Financial analysis: Financial data related to the Program's budgets, revenues, expenditures, banking fees, and staff resources were reviewed

- Survey: In lieu of conducting interviews with departmental and agency clients, the Evaluation conducted 2 surveys of RG departmental and agency clients: a client survey for the RG treasury (Banking and Cash Management Sector and Cheque Redemption Control Directorate) and accounting services (Central Accounting and Reporting Sector)

- Interviews: Six structured interviews with a total of 10 participants were held with key stakeholders from central agencies and other federal organizations that interacted with the RG on matters pertaining to its government-wide financial reporting roles, responsibilities, and products

24. More information on the approach and methodologies used to conduct this evaluation can be found in the About the evaluation section at the end of this report.

Findings and conclusions

25. The findings and conclusions below are based on multiple lines of evidence that were used during the Evaluation. They are presented by evaluation issue (relevance and performance).

Relevance

26. Relevance involved an assessment of the extent to which the Program addressed a continuing need, was aligned with federal priorities and departmental strategic outcomes and was an appropriate role and responsibility for the federal government.

Continuing need

27. Continuing need assessed the extent to which the RG programs and services continue to address a demonstrable need for its clients. The Evaluation found that the need persists for the centralized treasury and accounting services administered by the RG.

28. The custodianship of the Consolidated Revenue Fund is a critical function that has existed for over 250 years; there continues to be a need for the core treasury and accounting services provided by the RG. These activities are an essential service that provides payments totaling over $1.13 trillion on behalf of the federal government and which supports critical government programs (for example Old Age Security, Canada Pension Plan, and Employment Insurance). Approximately 60% of RG payments issued to Canadians were the only or main source of income for the recipients. Additionally, the inward flow of $1.23 trillion into the Consolidated Revenue Fund, which comes from sources such as citizens and businesses paying taxes, is also managed by the RG. As such, a Custodian of the Consolidated Revenue Fund is important to ensure efficient and economical administration of these services to Canadians.

29. In addition, the centralized provision of these services by one service provider supports Parliament, in particular the Standing Committee on Public Accounts, in fulfilling its role of ensuring that: public money is spent for the purposes authorized by Parliament; extravagance and waste are minimized; and sound financial practices are encouraged in estimating and contracting, and in administration generally. By ensuring payments into and out of the Consolidated Revenue Fund are managed in a timely and accurate manner and departments and agencies are provided with appropriate accounting guidance and advice, Parliamentarians are provided with accurate information thereby enabling them to fulfill their mandate.

30. Finally, all of the stakeholder interviewees (n=10) stated that the centralized provision of services was advantageous, because a single point of contact provides consistency in the delivery of treasury and accounting services including policy direction, guidance, and overall oversight of the Consolidated Revenue Fund; reduced duplication of RG activities including, for example, the maintenance of the Chart of Accounts and management of fraud detection; and reduced errors in issuing and processing payments and in the preparation of the Public Accounts of Canada. Additionally, the centralized delivery of treasury and accounting services was found to be aligned with international practices.

Federal priorities and departmental strategic outcomes

31. The Evaluation assessed the extent to which the objectives of the RG programs and services aligned with the PWGSC Strategic Outcome and with federal priorities. Based on these criteria, the Evaluation found that RG programs and services were aligned with the PWGSC Strategic Outcome and federal priorities.

Alignment with the Public Works and Government Services Canada Strategic Outcome

32. The RG's delivery of the centralized accounting and treasury services as Custodian of the Consolidated Revenue Fund aligns with the PWGSC Strategic Outcome of delivering high-quality, central programs and services that ensure sound stewardship on behalf of Canadians and meet the program needs of federal institutions. With respect to ensuring sound stewardship, the RG helps ensure sound stewardship of public funds through the establishment of the RG Control Framework and subsequent guidance and advice (such as the RG Manual). As the Custodian of the Consolidated Revenue Fund, the RG provides a critical financial leadership function that ensures value for money through the effective management of over 313 million payments on behalf of federal and provincial governments and approximately 800,000 deposits which represents more than 40 million transactions annually which together total over $2.3 trillion in cash flow.

33. Regarding the RG's services meeting the needs of federal institutions, as the Custodian of the Consolidated Revenue Fund, the RG delivers accounting and treasury services on behalf of client departments and agencies in order to meet their programming needs (for example payments on behalf of programs such as Old Age Security are issued to the public). With respect to the RG's other clients (Parliamentarians and the Canadian Public), the RG provides these clients with the information they need to understand Canada's financial position and, in the case of Parliamentarians, effectively scrutinize the economy and efficiency of the administration of government policy. Additionally, the centralized delivery model allows for more efficient and consistent implementation of initiatives that meet client needs, such as the Direct Deposit Initiative for the issuance of payments to the public.

34. The RG also aligns with PWGSC's Service Management and Value for Money Priorities. As the RG continues with its transformation and modernization initiatives, the Program's service integration will increase, thereby better enabling departments and agencies to more effectively achieve their mandates to serve Canadians, an integral component of PWGSC's Service Management Priority, which is rooted in the Treasury Board Policy on Service.

Alignment with federal priorities

35. The Prime Minister's 2015 Ministerial Mandate Letter to the Minister of Public Works and Government Services emphasized the importance of efficient delivery of services in a way that makes citizens feel respected and valued. Through the preservation of the integrity of the Consolidated Revenue Fund and the provision of secure and reliable payment (313 million payments issued in 2014 to 2015) and remittance services (approximately 800,000 deposits which represents more than 40 million transactions annually in 2014 to 2015) on behalf of federal and provincial governments, the RG provides critical services directly to Canadians. Further, many of those receiving these payments rely heavily on the services rendered (such as Old Age Security, Canada Pension Plan, and Employment Insurance). Additionally, through the delivery of services to monitor and address fraudulent activities and the maintenance of the RG Control Framework and associated guidance and advice, the RG helps ensure fiscal prudence of public funds, a key value highlighted in the Prime Minister's 2015 Ministerial Mandate Letter to the Minister of Public Works and Government Services.

36. The RG also produces 2 important accountability and reporting documents: the Public Accounts of Canada and the Monthly Statement of Financial Operations, which provide the necessary fiscal results for the Government of Canada to support Parliament in its decision making in addition to assuring fiscal prudence of public funds. The RG supports the federal priorities relating to the streamlining of government operations, Information Technology (IT) infrastructure renewal, expanding electronic services for Canadians, and support for regional development, through its activities in the areas of the modernization of RG systems, the increasing use of electronic payments/remittances, and the regional delivery of the Cheque Redemption and Control Directorate.

Appropriate role and responsibility for the federal government

37. To determine if the Program is an appropriate role and responsibility for the federal government and PWGSC, the Evaluation reviewed the extent to which RG programs and services complement, duplicate or overlap with other federal government functions. The Evaluation found that the RG programs and services complemented the functions of other federal organizations without duplication or overlap.

38. Most notably, the Financial Administration Act designates the Receiver General for Canada with the responsibilities for managing the flow of public money in and out of the Consolidated Revenue Fund, maintaining the Accounts of Canada, and publishing the Public Accounts of Canada. PWGSC's role as the RG is also legislated by the Department of Public Works and Government Services Act. Overall, there is strong legislative authority for the RG programs and services with a total of 112 Acts and 108 Regulations supporting or referencing the RG as the provider of these services.

39. In addition to establishing the Minister of Public Works and Government Services as the Receiver General of Canada, the Department of Public Works and Government Services Act establishes PWGSC as a common service agency for the Government of Canada, whose activities are to be directed mainly toward providing the departments, boards and agencies of the Government of Canada with services in support of their programs. The RG provides common, centralized services delivered on behalf of other federal departments and agencies (as well as provinces for the issuance and acceptance of payments).

40. The organizations outlined below in paragraph 41 play a crucial role in ensuring public funds are appropriately managed; however, they are not mandated to deliver services on behalf of other federal departments or agencies, nor on behalf of the provinces. The work of the RG supports these organizations in the delivery of their work and ultimately the achievement of their outcomes without duplication or overlap.

41. The RG delivers services in a manner that is complementary to the mandates of its key partners, specifically:

- The Treasury Board of Canada Secretariat provides advice and makes recommendations to the Treasury Board committee of ministers on how the government spends money on programs and services, how it regulates and how it is managed

- The Office of the Comptroller General of Canada supports the Treasury Board of Canada Secretariat by providing functional direction and assurance for financial management across the federal government through the development of policies and directives

- The Department of Finance helps the Government of Canada develop and implement strong and sustainable economic, fiscal, tax, social, security, international and financial sector policies and programs. In relation to the work of the RG, the Department of Finance prepares the Annual Financial Report of the Government of Canada and, in cooperation with the Treasury Board of Canada Secretariat and the RG, the Public Accounts of Canada

42. Interviews with key stakeholders support this analysis; while not directly asked if PWGSC was the appropriate place for the RG, almost half of the interview participants specifically noted that the RG was appropriately placed in PWGSC. Additionally, evidence indicates that the RG's model of centralized treasury and accounting services is aligned with the practices of international jurisdictions. A review conducted by the RG found that more than half of the jurisdictions had centralized treasury structures (11/18) and integrated systems (12/18).

Conclusions: Relevance

43. There continues to be a need for the RG. The RG programs and services are aligned with the PWGSC Strategic Outcome and federal priorities. There is strong legislative authority for the RG programs and services to be provided by PWGSC. The RG's services complement the work of key federal stakeholders for ensuring fiscal prudence of public funds. The Evaluation also found that the RG's centralized delivery of services and overall placement within PWGSC is appropriate and aligned with international jurisdictional practices.

Performance

44. Performance measures the extent to which the Program is able to achieve its objectives and the degree to which it is able to do so in a cost-effective manner that demonstrates efficiency and economy.

Outcome achievement

45. The Evaluation examined the degree to which this Program achieved its intended immediate, intermediate, and ultimate outcomes. The intended outcomes of the Program are identified below, followed by an assessment of the extent to which they were achieved. While the Logic Model (Exhibit 1: Logic model—Evaluation of the Receiver General for Canada) includes an outcome for the Common Departmental Financial System, the achievement of this outcome was not assessed. In 2012, the Treasury Board's Standard on Enterprise Resource Planning Systems required that new investments in or upgrades to existing financial or materiel management systems result in the implementation of SAP in accordance with the policy direction of the Office of the Comptroller General and the Government of Canada's Chief Information Officer Branch which both reside at the Treasury Board of Canada Secretariat. As a result of this requirement, the Common Departmental Financial System is being phased out as its client departments and agencies transition to the SAP system.

Immediate outcome #1: Remittances and payments are accurate and timely

46. The Evaluation examined the extent to which the Program has processed remittances and payments through the Consolidated Revenue Fund in a timely and accurate manner. The Evaluation found that the collection of revenues and payments were processed through the Consolidated Revenue Fund in a timely and accurate manner, and that errors – while they infrequently occurred – were addressed with department and agency clients in a timely manner.

Remittances from the Public to the Receiver General for Canada

47. The RG, on behalf of federal departments and some provinces, receives, reconciles, and records all payments made from the public into the Consolidated Revenue Fund. There are targets established to monitor the performance of RG's processing of remittances from the public to the Consolidated Revenue Fund. While not responsible for the accuracy of the remittances (this is the responsibility of the payers), the RG does assist other government departments in addressing remittance errors. The performance of the RG regarding these activities is discussed in detail below.

48. The RG has high standards for the timeliness of its processing of remittances from the public. From 2010 to 2011 to 2014 to 2015, the RG met or exceeded its target (95%) for reconciling remittances to the RG within 2 business days. In addition to the RG meeting its targets, departmental and agency clients of the treasury services perceived the RG's processing of remittances to have been done in a timely manner, as outlined in Exhibit 2: Departmental and agency client perceptions of the timeliness and accuracy of the Receiver General for Canada's processing of remittances from the public below.

49. Regarding the accuracy and verification of the accuracy of the remittances, this is the responsibility of the payers (that is the public), depository financial institutions, and department and agency payees and therefore not attributable to the RG. That said, Exhibit 2: Departmental and agency client perceptions of the timeliness and accuracy of the Receiver General for Canada's processing of remittances from the public indicates that departmental and agency clients perceived that the RG accurately delivered the services pertaining to its specific role in the processing of remittances, which includes assisting to address remittance errors.

Exhibit 2: Departmental and agency client perceptions of the timeliness and accuracy of the Receiver General for Canada's processing of remittances from the public

Source: Office of Audit and Evaluation survey of RG departmental and agency clients (2015)

| Indicator | Perceived timeliness (%) | Perceived accuracy (%) |

|---|---|---|

| RG's facilitation of the initial set-up of deposit services for the acceptance of remittances | 100 | 95 |

| RG's provision of services pertaining to remittances (reconciliations, deposit summary, remittance details file, and control data file and report) | 96 | 100 |

| RG provision of remittance details for above services | 90 | 90 |

| RG provision of advice and direction on remittance issues | 89 | 100 |

| RG review of discrepancies in remittances (upon client request) | 71 | 82 |

50. While departmental and agency client perceptions of timeliness in regards to the RG's review of discrepancies in remittances upon request was lower than for all other indicators, the RG is currently in the process of making improvements to its business processes as part of the RG Modernization Initiative in order to address these issues.

Payments from the Receiver General for Canada to the Public

51. The RG, on behalf of federal departments and some provinces, issues, reconciles, and records all payments made from the Consolidated Revenue Fund to the public, which includes reconciling payments cleared through the Bank of Canada. Additionally, the RG conducts a validation exercise automatically to determine if the signatory has the appropriate authority for the total amount of the payments being requisitioned and for the specific type of payment product being used. If not, the payment is rejected and the RG then conducts follow-up activities. Additionally, the RG assists departments with post-payment activities such as investigation and recovery activities, when required.

52. With respect to the RG making payments to the public, performance targets are in place and being monitored. In addition to making payments, the RG has built into its system alerts to notify departments of issues with payments and a process in place with product officers who assist departments with post-payment activities. The RG also undertakes activities to monitor and address fraudulent activities. The performance of the RG in these areas is discussed below.

53. The RG processed payments to the public, for the most part, in a timely manner. According to the PWGSC publication "Our Services, Our Standards" and the Deputy Minister Scorecard, PWGSC for the most part met or exceeded its targets for the last 5 years for which data is available (Exhibit 3: Receiver General for Canada's achievement of performance targets). However, according to the results communicated in the Departmental Performance report, the RG marginally missed its targets for the same period with respect to the issuance of payments within established timeframes (Exhibit 3: Receiver General for Canada's achievement of performance targets). The shortfall (0.09%) in 2012 to 2013 was due to delays by the service provider; the RG took a risk-based approach by releasing a batch of non-time sensitive paymentsFootnote 1 3 days later than scheduled in order to compensate for this delay. The high performance targets are set at 99.99% due to the fact that approximately half of these payments are socio economic payments with legislated timelines, and delays can create financial hardship for recipients.

Exhibit 3: Receiver General for Canada's achievement of performance targets

Exhibit summary

Exhibit 3 presents the RG's achievement of its performance targets for fiscal years 2010 to 2011 to 2014 to 2015.

| Indicator | Target/Actual | 2010 to 2011 | 2011 to 2012 | 2012 to 2013 | 2013 to 2014 | 2014 to 2015 |

|---|---|---|---|---|---|---|

| Process all federal payments daily as per established schedules. Footnote 2 | Target | N/A | 99.90% | 99.99% | 99.99% | 99.99% |

| Actual | N/A | 100% | 99.98% | 99.99% | 99.99% | |

| Percentage of Receiver General payments issued within established time-frames. Footnote 3 | Target | 99.99% | 99.99% | 99.99% | 99.99% | 99.99% |

| Actual | 99.97% | 99.94% | 99.90% | 99.98% | 99.99% | |

| Percentage of daily settlement instructions sent, according to schedule, to the Bank of Canada for all outflows from the Consolidated Revenue Fund. Footnote 3 | Target | 95% | 95% | 95% | 95% | 95% |

| Actual | 100% | 99.6% | 100% | 99.8% | 95% |

54. From 2010 to 2011 to 2014 to 2015, the RG also met or exceeded its target for sending daily payment settlement instructions according to schedule to the Bank of Canada for all outflows from the Consolidated Revenue Fund. The achievement of this target facilitated the Bank of Canada's timely transfer of funds from the Consolidated Revenue Fund to financial institutions. While not a specific performance target, from 2011 to 2012 to 2014 to 2015 the RG sent settlement instructions to financial institutions according to schedule 99.99% of the time, which compares favorably to the results for other performance indicators that pertain to RG payments. Additionally, the survey of treasury service departmental and agency clients found that most respondents perceived the payment services to have been provided by the RG in a timely manner (see Exhibit 4: Departmental and agency client perceptions of the timeliness and accuracy of the Receiver General for Canada's processing of payments).

55. The overall accuracy of payments was out of the scope of the Evaluation, as the RG is not responsible for the accuracy of the payment information that it receives from client departments and agencies. The RG processes the payment amounts as requisitioned by the department or agency. As well, data pertaining to the percentage of errors or rejects in the payment lifecycle that were attributable to the RG's Standard Payment System was not available. The RG Standard Payment System does not maintain or publish this data for more than a 6 month period, because payments are archived after they are processed or cancelled. However, most departmental and agency clients that responded to the survey of treasury services indicated that payments were processed in an accurate manner by the RG (Exhibit 4: Departmental and agency client perceptions of the timeliness and accuracy of the Receiver General for Canada's processing of payments).

Exhibit 4: Departmental and agency client perceptions of the timeliness and accuracy of the Receiver General for Canada's processing of payments

| Indicator | Perceived timeliness (%) | Perceived accuracy (%) |

|---|---|---|

| RG processing of domestic payments | 94 | 97 |

| RG processing of foreign payments | 97 | 100 |

| RG processing of priority payments | 100 | 100 |

56. While data pertaining specifically to the Standard Payment System payment rejects was not available for more than a 6 month period, when there is a reject or error for a specific payment, departments and agencies are advised automatically by the Standard Payment System with a payment advice notice or a post-issue file. When an entire payment requisition sent to the Standard Payment System is rejected, an error report is created and sent to Payment Products and Services Directorate, who follow up with the appropriate department for corrective action. Although Program data was unavailable, corrective action taken by the RG to address errors was perceived by most departmental and agency clients to be, for the most part, timely (79%) and accurate (93%).

57. Regarding the RG's process to assist departments with post-payment activities, most of the treasury services client departments and agencies surveyed perceived the post-payment activity enquiry process as timely (96%) and accurate (96%).

58. With respect to the post-payment investigation and recovery activities, as outlined in Exhibit 5: Change in investigations and recoveries from 2010 to 2011 to 2014 to 2015, there was a decrease in the volume of fraudulent and non-fraudulent cheque payments that the RG investigated and recovered. In total, $45 million in duplicated or investigated cheque payments was recovered in this period. Regarding misdirected direct deposit payments from the RG, there was an increase in recovery notices where, on average, 7,200 of the investigations resulted in a total of $12 million being recovered for misdirected direct deposit payments during the period of 2010 to 2011 to 2014 to 2015.

Exhibit 5: Change in investigations and recoveries from 2010 to 2011 to 2014 to 2015

| Indicator | Change from 2010 to 2011 to 2014 to 2015 |

|---|---|

| Number of cheque payments investigation | -30% |

| Number of cheque payments recovered | -15% |

| Amount recovered | -43% |

| Number of cheque payments issued | -32% |

| Number of recovery notices for misdirected direct deposit payments | 29% |

| Number of direct deposits issued | 20% |

59. The decrease in investigations and recoveries for cheque payments may, in part, be related to the reduction in cheque payments issued over this same period. Regarding direct deposit recoveries, the largest amount ($4.5 million or 38% of all recoveries made during the 2010 to 2011 to 2014 to 2015 period) recovered was in 2014 to 2015; the increase over this period could be explained by the increased use of direct deposit over this period.

60. The client departments and agencies who responded to a questionnaire prepared by the RG suggested methods to improve fraud detection. The suggestions centred primarily on improving access to, and analysis of, payment-related data. In particular, the suggestions included sharing more information among departments; working with the Canada Revenue Agency and the Office of the Comptroller General to improve processes; and increasing data analytics capabilities, quality assurance, reviews, and audits. Improvements to fraud detection are being explored as part of the RG Modernization Initiative.

Immediate outcome #2: Public Accounts and government-wide reporting are accurate, timely and accessible

61. The Evaluation examined the extent to which the Public Accounts of Canada and related accounting services were provided in an accurate, timely and accessible manner. The RG provides advice and guidance to federal organizations on accounting and reporting issues while monitoring the quality of financial information. The RG does this by maintaining and managing a suite of accounting and reporting systems. Additionally, the RG maintains the Accounts of Canada from which the Public Accounts are then produced and published. The Evaluation found that the Public Accounts were produced in an accurate and timely manner; however, clients and stakeholders indicated the Public Accounts process was notably difficult and the layout was difficult to understand. These issues are beyond the RG's realm of influence.

Accuracy

62. Departmental and agency client views on the accuracy of the RG accounting services were high: 92% or more of the respondents were satisfied with each of the RG's accounting services.

63. Program data demonstrates that the Public Accounts were prepared and reported upon in the RG in an accurate manner. From 2010 to 2011 to 2013 to 2014, any audit issues identified during the Auditor General of Canada's annual audit of the Public Accounts relating to the RG were satisfactorily addressed and as such, the RG did not receive any management letters raising audit issues. Additionally, there were no errors identified by the Office of the Auditor General on the summary of unadjusted differences for the RG.

64. There were relatively few changes made to the Public Accounts (referred to as errata) after the initial tabling of the report. During the period of 2010 to 2011 to 2013 to 2014, more than half of these errata (10/16 or 63%) were not attributable to the RG; the changes were attributable to other departments and agencies.

Timeliness Immediate outcome #2

65. Overall, client departments and agencies' perception of the timeliness was high with 93% or more of the respondents being satisfied with the timeliness of the provision of each of the RG's accounting services. A previous survey that was conducted by the RG in 2013 found 87% or more of the respondents were satisfied with timeliness of the provision of accounting services.

66. Some of the RG's departmental and agency clients and stakeholders have noted some issues with the timeliness of the Public Accounts preparation process. For instance, it was noted that the timelines for some deliverables were too short and/or lacked sufficient clarity and the overall length of the Public Accounts preparation process was too long. However, given the nature of the information contained in the Public Accounts (that is the detailed fiscal records of over 100 departments and agencies, representing over $2.3 trillion, consolidated into one financial statement for the Government of Canada), and the audience in question (that is: Parliamentarians and the Canadian public), it is understandable that these issues, which are largely beyond the RG's control, exist.

67. The Public Accounts were produced and reported upon in a timely manner. For the period of 2010 to 2011 to 2013 to 2014, the RG met its performance targets for producing the Public Accounts according to schedule and submitting the Public Accounts to the House of Commons by December 31. The RG also met its objective for posting the Public Accounts on the web within 24 hours of its submission to the House of Commons.

68. The only issue identified with the timeliness of the Public Accounts production process was that the RG cannot automatically (that is within the 24 hour timeframe) produce a version of the Public Accounts that meets Web Content and Accessibility Guidelines, because more time consuming, manual production processes are required to transform the Public Accounts into an accessible format.

Accessibility

69. Overall, 95% or more of the respondents perceived accounting services to have been provided in an accessible manner for all services assessed in the client survey. That said, the majority of the organizations interviewed as part of this evaluation noted that the Public Accounts preparation process was difficult, long, and heavy. Given the complexity and nature of the government revenues and expenditures, it is understandable that the preparation process is difficult.

70. Some departmental and agency clients indicated during RG-led consultations that the layout and structure of the Public Accounts were difficult to understand. The Public Accounts are designed by the Office of the Comptroller General to contain all the pertinent financial data required to assist Parliamentarians and the public in their understanding and evaluation of the very complex financial position and transactions of the government. As such, the observations related to accessibility are both beyond the RG's realm of control.

Intermediate outcome #1: Efficient and timely banking and treasury services for federal institutions

71. The Evaluation examined the extent to which the banking and treasury services were provided in an efficient and timely manner. The RG, as Custodian of the Consolidated Revenue Fund, is essentially the bookkeeper for federal institutions in that it manages the processing of remittances and payments on behalf of federal programs through the delivery of its banking and treasury services. The Evaluation found that these services were efficiently meeting timeliness performance targets.

Efficiency

72. The efficiency of the RG's delivery of its treasury services was assessed based on the degree to which the services were delivered effectively and within planned spending. Evidence demonstrated that the RG delivered the treasury services in a manner that achieved most performance targets while remaining within the planned spending limits. While the RG does not have efficiency benchmarks, client departments and agencies are satisfied with the services provided by the RG and perceive them to be timely and accurately delivered. Additionally, available evidence indicates that RG's centralized service model aligns with international practices and further centralization of services for RG Stewardship could improve efficiencies. The RG is examining the feasibility of further centralization of services as part of its RG Modernization Initiative.

Timeliness Immediate outcome #1

73. Treasury services were provided, for the most part, in a timely manner. As discussed earlier in the assessment of the achievement of Immediate Outcome #1, from 2010 to 2011 to 2014 to 2015 the RG met, for the most part, its performance targets relating to timeliness of service delivery. Departmental and agency client perceptions of timeliness were high, with all but 2 of the treasury services perceived as timely by most (more than 89%) of the client survey respondents. The 2 services with lower, albeit still relatively high, perceived timeliness were:

- client requests to the RG to review remittance discrepancies (71%)

- corrective action to address processing errors or rejects impacting timeliness or accuracy that occurred while loading the payment files into the Standard Payment System (79%)

Intermediate outcome #2: The integrity of the Consolidated Revenue Fund and the Accounts of Canada is preserved on behalf of Canadians

74. The Evaluation examined the extent to which the integrity of the Consolidated Revenue Fund and the Accounts of Canada were preserved.

75. The Control Framework describes the key controls in place for the RG's Central IT Systems and is supported by guidance and direction provided to departments and agencies available in the RG Manual, 10 Directives, and 3 Information Notices:

- RG Manual – provides guidance and information on reporting requirements and central systems procedures

- RG Directives – provide instructions to departments and agencies

- RG Information Notices – provide information and advice related to treasury functions to departments and agencies, as well as supplementary information or clarifications on accounting issues and procedures that were not addressed in the RG Manual

76. Through the effective delivery of the above guidance and direction, which supports a strong control framework, the RG is contributing to the preservation of the integrity of the Consolidated Revenue Fund and the Public Accounts. The degree to which this guidance and direction is appropriately followed by the client departments and agencies, however, is beyond the RG's realm of direct influence.

77. As noted in the discussion for Immediate Outcome #2, from 2010 to 2011 to 2013 to 2014, the RG did not receive any management letters raising audit issues in relation to the Auditor General of Canada's annual audit of the Public Accounts. During this period, any issues with the accounting systems used by the RG to maintain the Accounts of Canada and report on the Consolidated Revenue Fund were satisfactorily addressed. As such, it can be concluded that the RG is preserving the integrity of the Consolidated Revenue Fund and the Public Accounts.

Ultimate outcome: High-quality, central programs and services that ensure sound stewardship on behalf of Canadians and meet the program needs of federal institutions

78. The Evaluation found that through the timely and accurate provision of accounting and treasury services and production of the Public Accounts, the RG is meeting the needs of federal institutions and thereby contributing to PWGSC's achievement of its strategic outcome, which is the overarching outcome for all Departmental programs. In addition, the RG contributes to the preservation of the integrity of the Consolidated Revenue Fund and the Public Accounts; in doing so, the RG is doing its part in ensuring sound stewardship on behalf of Canadians of $2.3 trillion cash flow of public funds while ensuring the efficient and effective processing of 313 million payments to Canadians and businesses and approximately 800,000 deposits which represents more than 40 million transactions annually.

Conclusions: Outcome achievement

79. Immediate outcomes were achieved: The RG is achieving its immediate outcomes. Program data and client surveys demonstrated that remittances and payments were, for the most part, processed in a timely manner and were perceived by departmental and agency clients as accurate. Processing exceptions were addressed appropriately and in a timely manner. Additionally, the Evaluation found that the Public Accounts were produced in an accurate and timely manner and clients perceived accounting services to be provided in an accessible manner. It was noted that the Public Accounts process was notably difficult and the layout was hard to understand, however these issues are beyond the RG's realm of influence.

80. Intermediate outcomes were achieved: The Evaluation found that the treasury services were meeting timeliness performance targets and doing so in a cost effective manner. The RG is contributing to the preservation of the integrity of the Accounts of Canada and Consolidated Revenue Fund through the established RG Control Framework and corresponding guidance and advice the RG provides to client departments and agencies. During the Auditor General of Canada's annual audit of the Public Accounts, the RG satisfactorily addressed issues identified by the audit team and as such, no management letters raising issues were provided to the RG from 2010 to 2011 to 2013 to 2014.

81. Contribution towards achievement of ultimate outcome: Through the achievement of the immediate and intermediate outcomes, the RG is contributing to PWGSC's achievement of its Strategic Outcome of sound stewardship on behalf of Canadians that meets the program needs of federal institutions.

Economy and efficiency

82. Demonstration of economy and efficiency is defined as an assessment of resource utilization in relation to the production of inputs and outputs. Economy refers to minimizing the use of program inputs. Efficiency refers to the extent to which resources are used such that a greater level of output is produced with the same level of financial resources or a lower level of financial resources are used to produce the same level of output. A program has high economy and efficiency when financial resources maximize outputs and minimize inputs.

Economy

83. The Evaluation examined the extent to which the treasury and accounting services are delivered economically, which was measured through an examination of RG's resource inputs. The Evaluation found that despite significant cost pressures beyond the RG's control (such as card acceptance and postage fees), RG services were delivered economically.

84. Overall, the RG has used its salary and operating resource inputs in an economical manner. As shown in Exhibit 6: Receiver General for Canada planned versus actual expenditures, expenditures for RG Stewardship were within budget for the 2010 to 2011 to 2014 to 2015 fiscal years (less than 5% below planned expenditures in each fiscal year).

Exhibit 6: Receiver General for Canada planned versus actual expenditures

Description for Exhibit 6

This exhibit 6 shows the RG's planned versus actual expenditures for fiscal years 2010 to 2011 to 2014 to 2015. The vertical axis displays the dollar values, ranging from zero to 150 million dollars, and the horizontal axis displays the fiscal years 2010 to 2011 to 2014 to 2015. The graph shows that the planned and actual expenditures both decreased by approximately 10 million dollars from fiscal years 2010 to 2011 to 2014 to 2015. During this period, planned spending decreased from approximately 146 million dollars to approximately 136 million dollars and actual expenditures decreased from approximately 140 million dollars to approximately 130 million dollars. The graph also shows that in each fiscal year the actual expenditures were slightly below the planned expenditures by 7 million dollars or less.

Source: RG documents

85. While there was also a notable increase in the average salary costs for accounting services (27%) over this period, the full time equivalent volumes and salary costs were within the planned volumes and expenditures (see Exhibit 7: Accounting services—planned versus actual full-time equivalents and average (median) salary). As demonstrated in Exhibit 7: Accounting services—planned versus actual full-time equivalents and average (median) salary, there was a consistent differential in the staffing resources for accounting services, as full time equivalents were below planned volumes. The differential was caused by the phasing out of the optional Common Departmental Financial System offering, changes to the implementation of the Modernization Initiative, as well as a variety of other staffing adjustments.

Exhibit 7: Accounting services—planned versus actual full-time equivalents and average (median) salary

Description for Exhibit 7

Exhibit 7 displays the planned versus actual full-time equivalents and average median salary for RG Accounting Services. The graph includes 2 vertical axis. The vertical axis on the left measures the number of full-time equivalents, ranging from zero to 140 and the vertical axis on the right measures the median salary, ranging from zero to 140,000 dollars. The horizontal axis displays the fiscal years from 2010 to 2011 to 2014 to 2015.

The graph shows that the planned full-time equivalents have trended upwards over the 5 fiscal years, increasing slightly from 120 to 126. The actual expenditures have fluctuated up and down over the 5 fiscal years, increasing from 103 in 2010 to 2011 to 110 in 2011 to 2012, decreasing to 102 in 2012 to 2013, increasing to 111 in 2013 to 2014 and then decreasing to 95 in 2014 to 2015. During these fiscal years, the number of actual full-time equivalents was between 10 and 29 less than the actual number of full-time equivalents. The graph also shows that the median salary increased over the 5 fiscal years from about 67,000 dollars in 2010 to 2011 to about 85,000 dollars in 2014 to 2015.

Source: RG documents

86. While there were no major cost pressures identified for inputs for the Accounting Function, a few cost pressures were identified for inputs for the Treasury Function. In particular, the Accounting, Banking, and Compensation Branch's Integrated Business Plan for 2014 to 2015 identified banking fees as a significant cost pressure due to the increased use of card acceptance by department and agency clients for remittances. Adding to this significant cost pressure is an increase in postage fees.

87. Additionally, the central systems used to support the processing of payments were identified as areas impacting the economy of the Program. The limited availability of scarce legacy system development expertise and application institutional expertise was identified in RG documents as an area that could contribute to increased costs for system development and maintenance. However, this issue is expected to be mitigated through the enhancement of the Central Systems, which is one of the priorities of the RG Modernization Initiative.

Efficiency

88. The Evaluation examined the extent to which the RG is undertaking activities and delivering services and products in an efficient manner, which was measured by the efficiency of the RG's outputs and service delivery methods. The Evaluation found that despite a lack of available benchmarks, treasury outputs were delivered in an efficient manner, the centralized service model aligned with international practices, and further centralization of services could improve efficiencies.

Benchmarking

89. There were few performance metrics available for program efficiency. In 2007, a benchmarking study was completed for the RG by an external consultant. The study found that due to the RG's uniqueness and operational complexity, there were few valid benchmarking metrics from other public organizations. More specifically, industry benchmarks for banking fees could not be identified because financial institutions were reluctant to disclose information. RG planned on conducting another study to develop valid benchmarks in the 2014 to 2015 fiscal year; however, completion of the study was deferred to the 2016 to 2017 fiscal year.

Efficiency of remittance processing

90. For remittance services, the RG gains efficiencies through the centralized nature of its delivery model, as the centralized management of banking services leverages economies of scales and the RG receives multiple bids for its banking services needs through competitively tendered processes.

91. From 2010 to 2011 to 2014 to 2015, banking fees for remittances increased by $10.5 million, an increase of 20% relative to the cost in 2010 to 2011 ($46 million), although remittance volumes had also increased over the same period. It should be noted that this increase does not reflect a decrease in the cost-effectiveness of banking services; rather, remittance volumes increased by a similar amount and, on average, the rates for banking service fees did not increase.

Efficiency of payment processing

92. With respect to RG payments, evidence indicates that they are being efficiently processed by the RG, as measured by the program support costs and direct and indirect costs relative to the number of payments processed. From 2011 to 2012 to 2014 to 2015, the RG either met or was below the targeted cost for the average unit cost per payment. The unit cost was slightly above target in 2012 to 2013 (by one cent, on average, for 315 million payments totaling approximately $3 million) and was due to a change in the costing methodology.

93. However, the RG was not able to maximize some payment efficiencies because it did not meet its targeted cheque payment reductions in 2013 to 2014 and 2014 to 2015, which on average, cost $0.82 per payment issued, compared to $0.13 per payment for direct deposits. As a result, there was a delay in the planned reductions to the salary costs for cheque processing by the Cheque Redemption Control Directorate. The RG is undertaking activities to increase the direct deposit adoption rate in order to meet future performance targets and reduce cost pressures, which should increase the efficiency of payment processing.

Efficiency of centralized delivery model

94. The centralized delivery of treasury and accounting services is aligned with the practices of international jurisdictions. A review conducted by the RG found that more than half of the jurisdictions had centralized treasury structures (11/18) and integrated systems (12/18). All those interviewed as part of this evaluation also believed that the centralized provision of treasury and accounting services was advantageous and more efficient than decentralized provision.

95. Evidence indicated that further centralization of services could improve efficiencies. The RG's jurisdictional review identified trends among international jurisdictions towards increased centralization of services (for example Payee data, pay systems, data collection, storefront, common Chart of Accounts), as well as trends towards increased transparency, automation, and integration and the offsetting of payments against receivables for debt collection. Client departments and agencies who participated in the RG's consultation activities suggested increased efficiency could be obtained through the further centralization of other services, such as vendor/customer database, invoice submissions, accounts payable/ receivable, debt collection, and departmental Chart of Accounts. RG documents also identified that the centralization of these functions could improve efficiencies by addressing ongoing payment and remittance efficiency issues. Further centralization of RG functions is currently being examined as part of the RG Modernization Initiative.

96. The RG payment infrastructure has been adequately maintained, but could benefit from modernization and consolidation. For example, in 2011, the Standard Payment System was assessed by the PWGSC's Secretariat's Chief Information Officer Branch as satisfying ongoing and new requirements; however, it was noted that significant investment would be required to ensure performance and availability beyond 5 years. Additionally, Chief Information Officer Branch documents noted that the number of systems used to support the treasury and accounting functions could be reduced. The analysis found that replacing the current accounting and reporting systems with the SAP financial system would greatly reduce and consolidate accounting systems. A further study is currently being conducted on the suitability of SAP for treasury functions within the context of the RG's Modernization Initiative.

Conclusions: Economy and efficiency

97. With respect to Program Economy, significant cost pressures for Program were identified for remittances and payments. As such, resources were managed economically. Expenditures and full-time-equivalents were relatively stable and within budget.

98. With respect to Program efficiency, evidence indicated that the treasury outputs (remittances and payments) were provided in an efficient manner. Evidence also demonstrated that the RG model of centralized treasury services aligns with international practices, while multiple lines of evidence indicated that further centralization of services could improve efficiencies.

Conclusions: Performance

99. The RG is achieving its outcomes and thereby contributes to PWGSC's achievement of its Departmental Strategic Outcome by providing services that meet the needs of clients while also ensuring the sound stewardship of $2.3 trillion cash flow of public funds. The RG is delivering its services in an economical and efficient manner despite significant cost pressures.

General conclusions

100. There remains a need for RG services, which align with PWGSC and other federal priorities. The centralized delivery model of RG services by PWGSC is appropriate and in line with the practices of international jurisdictions. RG has achieved its immediate and intermediate outcomes, thereby contributing to PWGSC's achievement of its Strategic Outcome and has done so in an economical and efficient manner. As part of its Modernization Initiative, the RG is addressing the areas where some areas for improvement were noted.

101. Given the strong performance of the RG, the lack of identified issues in the achievement of outcomes, the economical and efficient delivery of the Program, and in recognition that the RG Modernization Initiative is expected to address issues noted in the evaluation, recommendations were not provided to the management of the Accounting, Banking, and Compensation Branch.

About the evaluation

Authority

The Deputy Minister for Public Works and Government Services Canada (PWGSC) approved this Evaluation, on recommendation by the Audit and Evaluation Committee, as part of the 2013 to 2018 Risk-Based Multi Year Audit and Evaluation Plan.

Evaluation objectives

This Evaluation examined the Receiver General for Canada (RG). The RG is located as sub-program 1.3 in the 2014 to 2015 Program Alignment Architecture for PWGSC and includes sub-program 1.3.1, Stewardship of Consolidated Revenue Fund & Accounts of Canada, and sub-program 1.3.2, RG Services. The RG is administered by the Accounting, Banking and Compensation Branch. This Evaluation had 2 objectives:

- to determine the relevance of the Program: the continued need for the Program, its alignment with governmental priorities and departmental outcomes and its alignment with federal roles and responsibilities

- to determine the performance of the Program: the achievement of its intended outcomes and a demonstration of economy and efficiency by the Program

Approach of the evaluation

The Evaluation was conducted in accordance with the Standard on Evaluation for the Government of Canada. The Evaluation took place between April 2014 and August 2015 and was conducted in 4 phases: pre-planning, planning, examination, and reporting. The Evaluation Directorate completed a risk-based calibration assessment to determine the best approach for the conduct of this Evaluation. The Evaluation of the 2 sub-programs' relevance and performance is presented in 2 volumes:

- volume 1: Stewardship of the Consolidated Revenue Fund and Accounts of Canada presented in traditional report format;

- volume 2: Receiver General Services presented in a matrix style report

An evaluation matrix was developed using the Treasury Board's 5 core issues to be addressed in evaluations. The following data sources were used to inform the lines of evidence to answer the questions in the Evaluation Matrix:

- Program document review: The Program document review involved an assessment of primary documents that provided information on the Program and its context for the planning phase and also provided information for the assessment of the Evaluation questions. The primary documents included program administration, monitoring and reporting documents, such as reports, meeting minutes, client surveys, program-led studies as well as financial records