Our Portfolio – Our Story 2012-2013

Our Portfolio – Our Story 2012-2013 (PDF 4.8Mb) is also available in a PDF version (alternative formats and plug-ins)

Real Property Portfolio

This document presents the state of Public Works and Government Services Canada's (PSPC) real property portfolio for 2012-13, both nationally and in its six regions: Atlantic, Québec, National Capital, Ontario, Western and Pacific. Also included are the department's engineering assets.

All building space figures are in rentable square metres. Building rentable area is calculated by subtracting building services and inside parking areas from the total inside gross area. Areas outside the exterior walls, such as balconies, terraces, or corridors, are also excluded.

National Portfolio

PSPC provides work environments for 110 federal departments and agencies, accommodating approximately 272,000 employees. The national portfolio is managed by six regions: Atlantic, Québec, National Capital (Ottawa-Gatineau and Nunavut), Ontario, Western and Pacific.

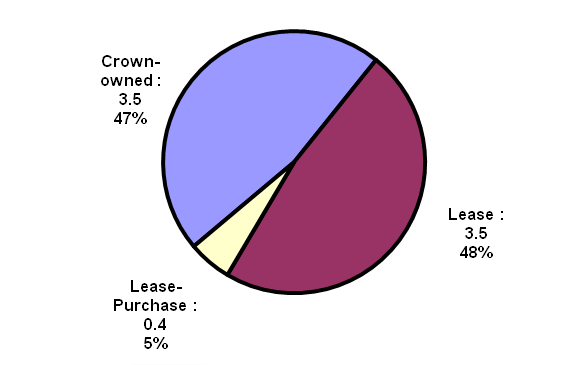

With nearly 1,800 locations across Canada, the Department's portfolio consists of 331 Crown-owned buildings, over 1,977 leases in 1,455 locations and nine lease-purchase buildings. The total PSPC accommodation portfolio is approximately 7.4 million square metres (m²), of which 3.5 million m² (47%) is Crown-owned, 3.5 million m² (48%) is leased, and 0.4 million m² (5%) is under lease-purchase agreements.

Approximately 6.5 million m² (87%) of the Department's 7.4 million m² of real property is office space, with the remaining 924,000 m² (13%) being comprised of common-use buildings (e.g. warehouses), special properties (e.g. training centres) and designated properties (e.g. the Parliament Buildings). The national portfolio also includes central heating and cooling plants, engineering assets (e.g. bridges and dams) and housing.

National Portfolio Profile by Property Type (m² in millions)

Text description for the chart National Portfolio Profile by Property Type (m² in millions)

This chart displays the proportions of PSPC national portfolio profile under the following three categories: Crown-owned, Lease and Lease-purchase.National Portfolio Profile

Table Summary

This table represents the entire PSPC real property portfolio of office and non-office by regions and property type.| Property Type |

Data | Pacific | Western | Ontario | National Capital Region | Québec | Atlantic | Total |

|---|---|---|---|---|---|---|---|---|

| Crown- owned |

# of buildings | 37 | 38 | 44 | 103 | 36 | 73 | 331 |

| Space (m²) | 256,193 | 222,212 | 350,186 | 2,059,753 | 283,813 | 286,134 | 3,458,292 | |

| % of total | 3.5 | 3.0 | 4.7 | 27.9 | 3.8 | 3.9 | 46.9 | |

| Lease- purchaseFootnote 2 |

# of buildings | 1 | 0 | 2 | 4 | 2 | 0 | 9 |

| Space (m²) | 25,524 | 0 | 12,926 | 288,165 | 70,746 | 0 | 397,360 | |

| % of total | 0.3 | 0.00 | 0.2 | 3.9 | 1.0 | 0.0 | 5.4 | |

| Lease | # of locations | 202 | 261 | 255 | 237 | 203 | 297 | 1,455 |

| Space (m²) | 272,755 | 489,511 | 486,264 | 1,690,062 | 296,267 | 288,556 | 3,523,414 | |

| % of total | 3.7 | 6.6 | 6.6 | 22.9 | 4.0 | 3.9 | 47.7 | |

| Total | # of buildings / locations | 240 | 299 | 301 | 344 | 241 | 370 | 1,795 |

| Space (m²) | 554,472 | 711,724 | 849,376 | 4,037,980 | 650,825 | 574,690 | 7,379,066 | |

| % of total | 7.5 | 9.6 | 11.5 | 54.7 | 8.8 | 7.8 | 100 |

Crown-owned Office Portfolio

The Crown-owned office portfolio has a significant concentration in eight major urban centres, namely: Halifax, Montréal, Ottawa-Gatineau, Toronto, Winnipeg, Calgary, Edmonton and Vancouver. Currently, more than half of the national Crown-owned office building inventory (in m²) is found in the National Capital Region (NCR), and includes the Crown-owned office buildings that serve the needs of parliamentarians.

Over the years, the size of the portfolio fluctuated as buildings were sold or removed from the inventory and new properties were acquired. The portfolio currently consists of 214 Crown-owned office buildings, totalling 2.8 million m² of the Department's total office space inventory of 6.5 million m². Nationally, the average size of a Crown-owned office building is 13,000 m². Significant regional variations exist; for example, 66 % of buildings in Atlantic Region are below 5,000 m² whereas the average office building size in the NCR is more than 35,000 m².

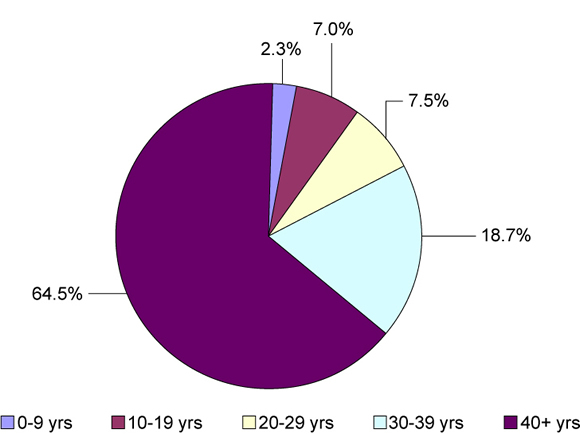

The average age of PSPC Crown-owned buildings is now 52 years, with nearly two-thirds of the buildings being more than 40 years old. However, the "effective age" of the portfolio is much lower as PSPC continuously maintains, repairs and upgrades its assets to meet high standards for federal accommodation.

Table Summary

This table is a 5 years summary chart of PSPC's crown-owned buildings by the total office buildings number, the size and the average age of buildings.| 2008-09 | 2009-10 | 2010-11 | 2011-12 | 2012-13 | |

|---|---|---|---|---|---|

| # Office buildings | 233 | 224 | 226 | 221 | 214 |

| Space (m² in 000s) | 2,405 | 2,352 | 2,495 | 2,655 | 2,781 |

| Average age (years) | 49 | 50 | 50 | 51 | 52 |

Note: Buildings in the Parliamentary Precinct are included in these numbers

Age of PSPC's Crown-owned Office Portfolio - % of total PSPC Crown-owned office facilities

Text description for the chart Age of PSPC's Crown-owned Office Portfolio

This chart display the percentage of the age of PSPC's crown-owned office facilitiesOperating and Maintenance Expenses

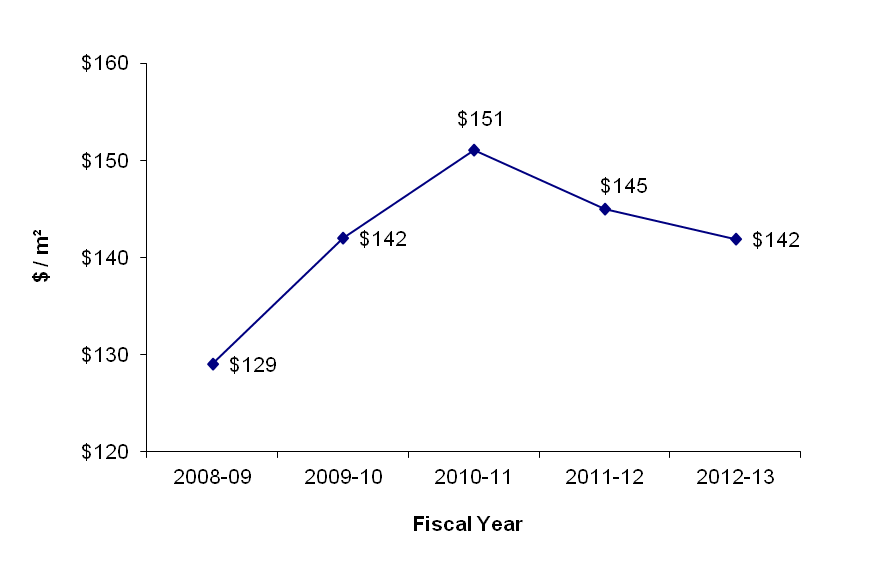

Operating and maintenance expenses include costs associated with cleaning, utilities, administration, repair/maintenance, security/roads/grounds, leasing (cost of managing commercial operations inside the buildings) and preparing space for tenants.

The national portfolio's average operating and maintenance expenses were $142/m² in 2012-13.

The five-year trend shows a substantial increase in average operating and maintenance expenses in 2009-10 and 2010-11. This increase can be largely explained by the expenditures under the Accelerated Infrastructure Program Footnote3 which enabled a number of backlog repair projects. Repair/maintenance costs represent the largest portion (around 37%) of the total operating and maintenance expenses, followed by utilities, administration, cleaning, security/roads/grounds and leasing.

As 2010-11 was the last year of the Accelerated Infrastructure Program funding, average operating and maintenance expenses have decreased in 2011-12 and 2012-13.

Operating and Maintenance Expenses (O&M) of PSPC's Crown-owned Office Portfolio

Text description for the graph Operating and Maintenance Expenses (O&M) of PSPC's Crown-owned Office Portfolio

This line graph illustrates the average operating and maintenance expenses (O&M) of PSPC's crown-owned office portfolio by fiscal year since 2008.Capital Expenditures

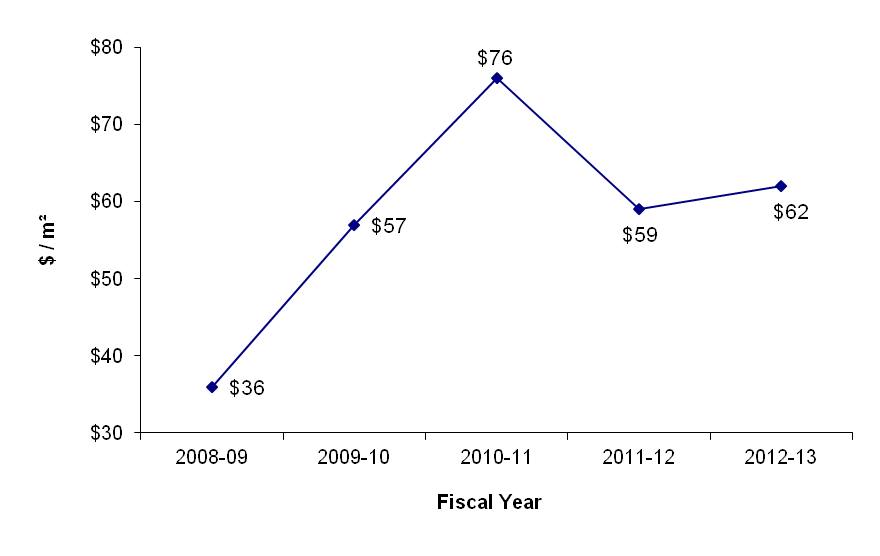

PSPC follows generally accepted accounting principles and applies set criteria to record expenditures as "capital." Capital expenditures are costs that meet one or more of the following criteria: are greater than $25,000 and extend the original life expectancy of the asset, improve the quality of the asset's output, increase its service capacity, or lower its operating costs.

Capital expenditures increased from $59/m² in 2011-12 to $62/m² in 2012-13. This equates to an increase in expenditures from $157 million in 2011-12 to $172 million in 2012-13. The amount of capital expenditures on real property assets increased in 2009-10, 2010-11, due to Economic Action Plan funding for the Accelerated Infrastructure Program. The fiscal stimulus enabled PSPC to address numerous capital projects carried over from previous years and also addressed some projects originally scheduled for future years.

Capital Expenditures of PSPC's Crown-owned Office Portfolio

Text description for the graph Capital Expenditures of PSPC's Crown-owned Office Portfolio

This line graph delineates capital expenses of PSPC`s crown-owned office portfolio by fiscal years between 2008 to 2013.Vacancy

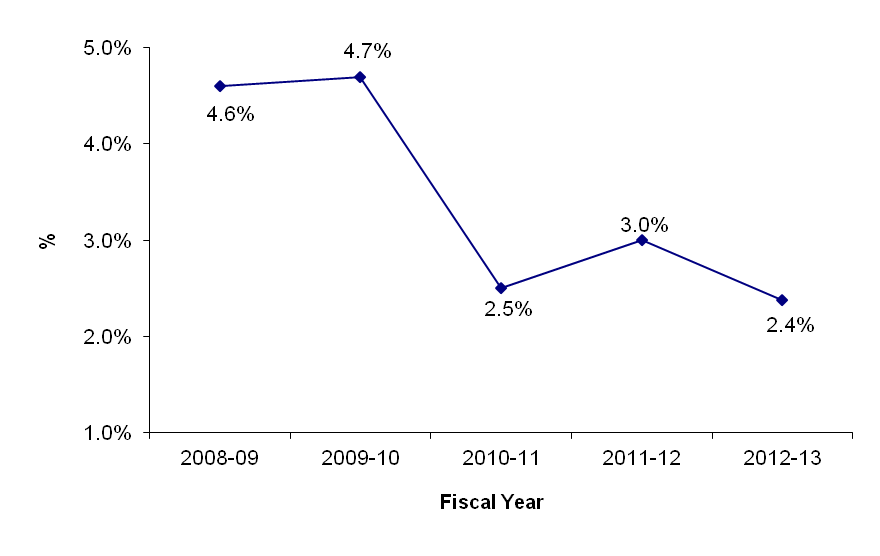

PSPC's mandate is to provide office accommodation and real property services to federal departments and agencies which, in turn, deliver programs and services to Canadians. PSPC manages its real property portfolio to achieve best value for taxpayers. As such, vacancy is tracked to identify potential space efficiencies and consolidation opportunities, and to evaluate the Department's performance. PSPC benchmarks its vacancy rate performance against external organizations. While there are differences in respective approaches, PSPC vacancy rates are typically lower than private sector rates.

PSPC requires a degree of flexibility and vacancy in its portfolio to respond to constantly changing client requirements that can include the need to quickly acquire space to deliver a new program or service to Canadians. Changing client requirements can also lead to small pockets of space scattered throughout the portfolio that cannot be easily back-filled by other clients.

PSPC limits the space it leases out commercially ("lettings") to businesses offering services (e.g. food, retail) to federal employees. While offering space to other private sector tenants (e.g. a technology firm) could reduce vacancy, this would fall outside the mandate of PSPC as a provider of office space to federal departments and agencies.

Vacant space is tracked for the entire PSPC portfolio of office and non-office (e.g. conference or training centres, storage) facilities in Crown-owned, lease-purchase and leased buildings. PSPC evaluates its performance based on "marketable vacancy" as opposed to "total unoccupied" space.

The marketable vacancy rate for Crown-owned office space is the percentage of total Crown-owned office building space that is vacant and marketable (i.e. space that is suitable for occupancy by any federal or non-federal client/tenant). This figure is PSPC's official metric on vacant space.

In comparison, total unoccupied space consists of vacant marketable space and space that is currently unsuitable for occupancy. This includes, but is not limited to, office space being fit-up for clients, buildings/offices under renovation, buildings in a non-usable condition and buildings that have been approved for disposal.

The marketable vacancy rate of the Crown-owned office portfolio in 2012-13 was 2.4%, a decrease from 3.0 % in 2011-12.

Vacancy Rate of PSPC's Crown-owned Office Portfolio

Text description for the graph Vacancy Rate of PSPC's Crown-owned Office Portfolio

This line graph pictures the vacancy rate of PSPC's crown-owned office portfolio by fiscal years between 2008 to 2013.Market Value

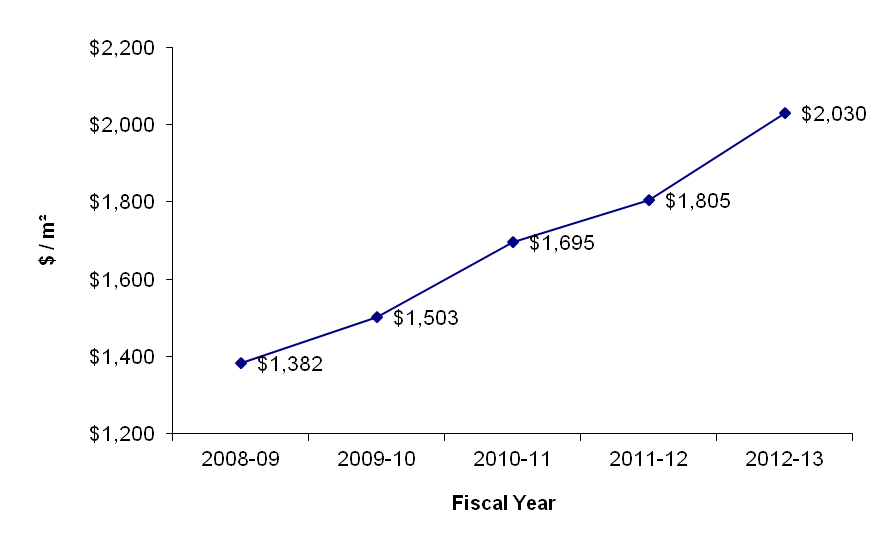

Market values for 2012-13 were calculated using an index that was applied to the previous year's valuations.

Due to an economic downturn in 2008-09, market values declined that year for the first time in 12 years (since 1996-1997), but recovered in 2009-10. In 2012-13, the average national market value of PSPC's Crown-owned office portfolio was $2,030/m², representing a 1 % increase from the previous year.

Market Value of PSPC's Crown-owned Office Portfolio

Text description for the graph Market Value of PSPC's Crown-owned Office Portfolio

This line graph pictures the average national market value of PSPC's crown-owned office portfolio by fiscal years between 2008 to 2013.Heritage Inventory Profile and Performance

Of all Crown-owned office buildings currently in the portfolio, 77 (36%) have been designated as federal heritage buildings following an evaluation by the Federal Heritage Buildings Review Office.

The average age of the designated heritage buildings is 29 years older than the non-designated buildings. The heritage buildings are also 3% more expensive to operate and maintain.

The market values of the heritage designated vs. non-designated buildings only differ slightly on a per m² basis.

The higher than average vacancy rate for designated buildings reflects several in-progress disposal projects, where buildings are being vacated prior to leaving the PWGSC inventory.

The table below summarizes the performance of the designated heritage portfolio versus the non-designated portfolio. While the portfolio of designated heritage office buildings presents some performance challenges, the buildings' prominent central locations contribute to a strong federal presence and are often prized locations for tenants.

Table Summary

This table summarizes PWGSC designated heritage portfolio profile and performance versus the non-designated portfolio.| Fiscal Year 2012-2013 | Building Count (#) | Average Age (yrs) | Space (m²) | Vacancy (%) | Market Value ($/m²) |

O&M Expenses ($/m²) |

Capital Expenses ($/m²) |

|---|---|---|---|---|---|---|---|

| Designated Federal Heritage Office Buildings | 77 | 69.9 | 911,693 | 3.53 | $1,995 | $127.7 | $55.1 |

| Other Office Buildings | 137 | 40.8 | 1,869,057 | 1.82 | $2,048 | $123.8 | $65.3 |

| All Office Buildings | 214 | 51.5 | 2,780,750 | 2.38 | $2,030 | $142 | $61.9 |

Sustainable Development

Sustainable Buildings

- As of March 2013, there were 6 Leadership in Energy and Environmental Design buildings and one Green Globes building under PWGSC custody.

Greenhouse Gas Emissions

- In 2012-13, PWGSC reduced its emissions by 1.0 % from the reported 2005-06 baseline of 264 kilotonnes.

- Approximately 99 % of PWGSC's greenhouse gas emissions come from its buildings portfolio.

Contaminated Sites

- As of March 31, 2013, PWGSC has completed remediation or risk management plans at 75.6 % of known contaminated sites.

Office Accommodation

National – Office Accommodation Metrics

In April 2012, PWGSC introduced new, more efficient office space standards based on industry best practices. As the Government of Canada's centre of expertise for real property, PWGSC has been working with client departments to implement these new standards to ensure the most efficient and economical use of government facilities.

Table Summary

This table presents RPB office accommodation metric based on three core accountability indicators ; square metres per employees, cost of office space per employee and cost of office space per square metre.| Indicator | 2008-09 | 2009-10 | 2010-11 | 2011-12 | 2012-13 |

|---|---|---|---|---|---|

| Square metres per employee (m²/employee) | 19.3 | 18.9 | 18.9 | 19.0 | 18.4 |

| Cost of office space per employee ($[rent]/employee) | $5,499 | $5,572 | $5,689 | $5,868 | $5,918 |

| Cost of office space per square metre ($[rent]/m²) | $284 | $295 | $300 | $309 | $321 |

The size of the national portfolio is relatively stable (modest increase) whereas market costs of accommodation are increasing. This explains the increase in cost per employee year over year.

National – Principal Clients

Office space location, and size, is important to client departments to ensure effective delivery of their programs. The Real Property Branch (RPB) acquires space on behalf of its clients and ensures the space provided is safe and adequate for the client's requirements, affords the maximum long-term economic advantage for government, and is consistent with environmental objectives and relevant government policies.

The ten largest clients in PWGSC's portfolio, based on m², are listed in the table below. The space they occupy represents over 52 % of the total space that PWGSC manages.

Table Summary

This table displays the ten largest clients in PWGSC`s portfolio based on space they occupy in square metres by property type.| Client department/agency | Crown-owned (m²) | Lease-purchase (m²) | Lease (m²) | Total space (m²) |

|---|---|---|---|---|

| Canada Revenue Agency | 423,727 | 1,140 | 518,499 | 943,366 |

| Human Resources & Skills Development Canada | 252,205 | 27,918 | 415,145 | 695,268 |

| National Defence | 179,904 | 76,503 | 209,569 | 465,976 |

| Royal Canadian Mounted Police | 229,361 | 71,677 | 98,753 | 399,791 |

| Public Works and Government Services Canada | 197,527 | 9,449 | 147,493 | 354,468 |

| Health Canada | 115,415 | 5,932 | 113,126 | 234,473 |

| Library and Archives Canada | 148,639 | 84,159 | 232,798 | |

| Canada Border Services Agency | 52,716 | 2,499 | 155,072 | 210,287 |

| Environment Canada | 53,519 | 18,906 | 117,951 | 190,375 |

| Fisheries and Oceans Canada | 64,166 | 114,090 | 178,255 | |

| Total | 1,717,179 | 214,023 | 1,973,855 | 3,905,057 |

Regional Portfolios

This section provides information on the Crown-owned office portfolio, in each of the six regions: Atlantic, Québec, National Capital, Ontario, Western and Pacific.

Atlantic Region

The Atlantic Region consists of the provinces of Newfoundland and Labrador, Nova Scotia, Prince Edward Island and New Brunswick. Key urban markets include Halifax, Moncton, St. John's and Charlottetown.

In 2012-13, the Atlantic Region represented 28 % of the national Crown-owned office portfolio based on building count, and 10 % of the national Crown-owned office portfolio's building floor area (m²).

Over the past five years, the Atlantic Region's Crown-owned office portfolio has steadily decreased, reflecting the disposal of assets in rural locations where demand has been decreasing. The region's overall inventory has remained comparatively stable over this period with an increasing reliance on the lease market to supply office space requirements.

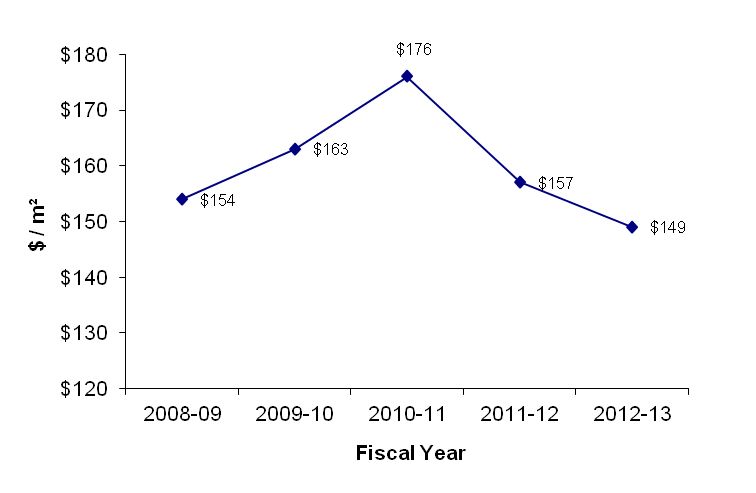

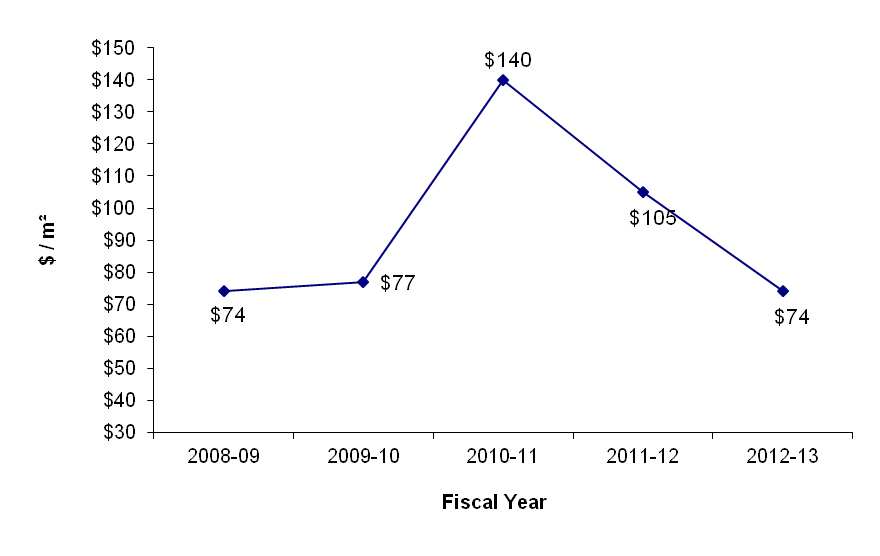

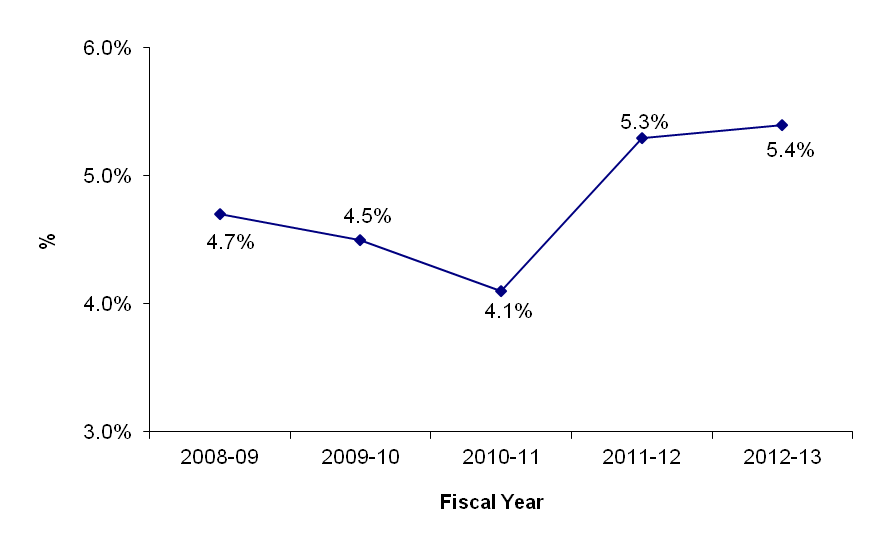

The Atlantic Crown-owned office portfolio currently consists of 60 office buildings totalling 275,615 m². As illustrated in the table and graphs below, there was an increase in the Atlantic portfolio's average operating and maintenance expenses and capital expenditures in 2009-10 and 2010-11, due in large part to the Accelerated Infrastructure Program. Average operating and maintenance expenses and capital expenditures have since decreased each of the last two fiscal years. Portfolio vacancy remained relatively unchanged in 2012-13.

Table Summary

This table provides information on the crown-owned office portfolio for the Atlantic region over the past five years. The information consist of the number of office buildings, the size and the average age of the buildings, the market value, the average operating and maintenance expenses and capital expenditures and the vacancy rate.| Indicator | 2008-09 | 2009-10 | 2010-11 | 2011-12 | 2012-13 |

|---|---|---|---|---|---|

| # Office Buildings | 71 | 67 | 63 | 62 | 60 |

| Space (m² in 000s) | 287 | 283 | 277 | 277 | 276 |

| Average Age (years) | 44 | 44 | 45 | 46 | 47 |

| Market Value ($/m²) | $834 | $840 | $995 | $882 | $958 |

| O&M ($/m²) | $154 | $163 | $176 | $157 | $149 |

| Capital ($/m²) | $74 | $77 | $140 | $105 | $74 |

| Vacancy Rate (%) | 4.7% | 4.5% | 4.1% | 5.3% | 5.4% |

O&M ($/m²)

Text description for the graph Section O&M ($/m²)

This graph illustrates the average operating and maintenance expenses (O&M) of PWGSC's crown-owned office portfolio for Atlantic Region, by fiscal years between 2008 to 2013.Capital ($/m²)

Text description for the graph Capital ($/m²)

This graph delineates capital expenses average for Atlantic Region of PWGSC`s crown-owned office portfolio, by fiscal years between 2008 to 2013.Vacancy Rate (%)

Text description for the graph Vacancy Rate (%)

This graph lists by percentage the Atlantic Region vacancy rate of PWGSC`s crown-owned office portfolio, by fiscal years between 2008 to 2013.Québec Region

The Québec Region consists of the province of Québec, with the exception of Gatineau, which is part of the National Capital Region. Key urban markets include Montréal and Québec City. Approximately 48 % of the region's inventory is located in Montréal, 14 % in Québec City and 38 % throughout the rest of the province.

In 2012-13, the Québec Region represented 15 % of the national Crown-owned office portfolio based on building count and 9 % of the national Crown-owned office portfolio's building floor area (m²).

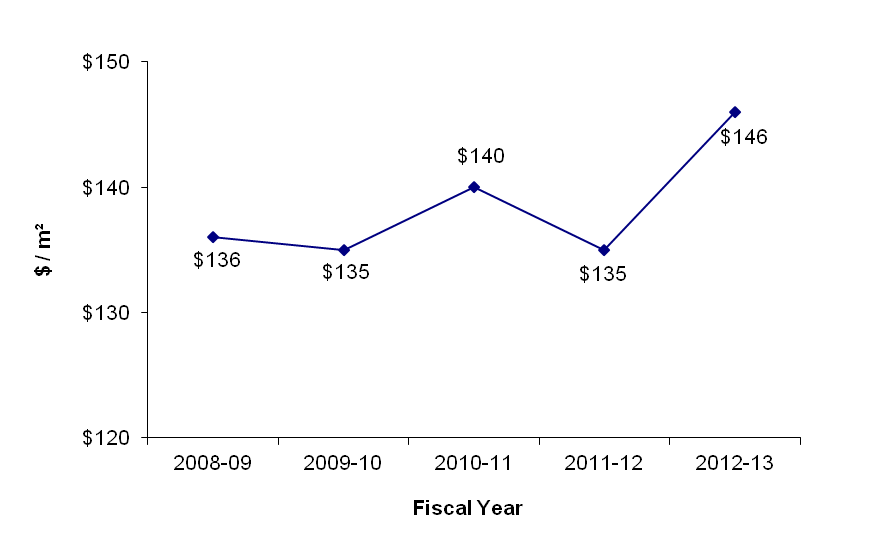

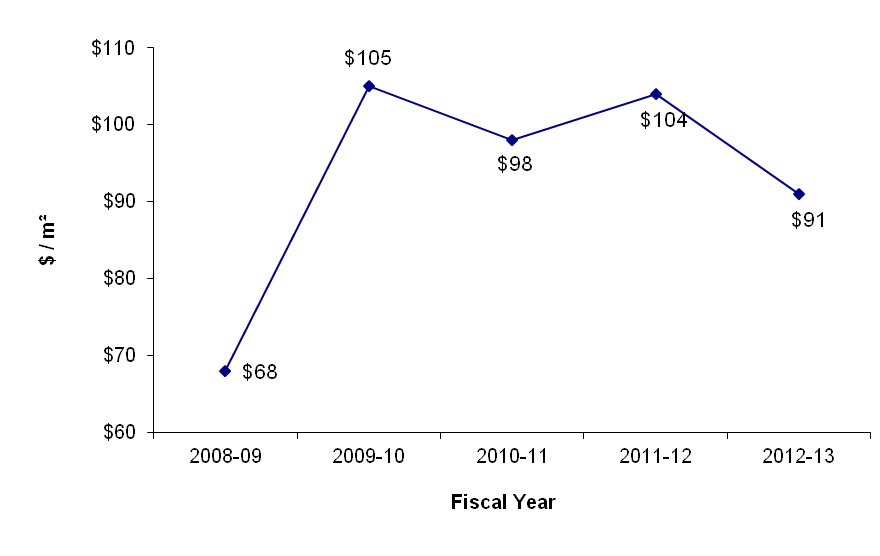

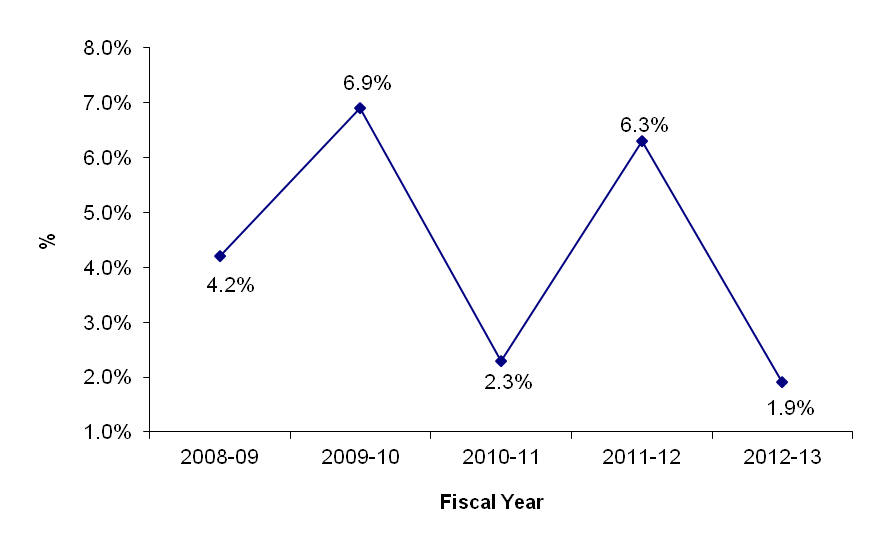

Over the past five years the Québec Region's Crown-owned office portfolio decreased slightly. It currently consists of 31 office buildings totalling 254,706 m². As illustrated in the table and graphs below there was an increase in the portfolio's average operating and maintenance expenses, due in large part to the Accelerated Infrastructure Program. A moderate increase in O&M cost ($/m²) was offset by a similar decrease in capital cost ($/m²) in 2012-13. The vacancy rate improved dramatically in 2012-13 due to disposal/ demolition of a number of buildings from the regional portfolio.

Table Summary

This table provides information on the crown-owned office portfolio for the Québec region over the past five years. The information consist of the number of office buildings, the size and the average age of the buildings, the market value, the average operating and maintenance expenses and capital expenditures and the vacancy rate.| Indicator | 2008-09 | 2009-10 | 2010-11 | 2011-12 | 2012-13 |

|---|---|---|---|---|---|

| # Office Buildings | 35 | 34 | 34 | 33 | 31 |

| Space (m² in 000s) | 275 | 272 | 272 | 272 | 255 |

| Average Age (years) | 51 | 53 | 55 | 57 | 58 |

| Market Value ($/m²) | $841 | $907 | $965 | $891 | $1,271 |

| O&M ($/m²) | $136 | $135 | $140 | $135 | $146 |

| Capital ($/m²) | $68 | $105 | $98 | $104 | $91 |

| Vacancy Rate (%) | 4.2% | 6.9% | 2.3% | 6.3% | 1.9% |

O&M ($/²)

Text description for the graph O&M ($/²)

This graph illustrates the average operating and maintenance expenses (O&M) of PWGSC's crown-owned office portfolio for Québec Region, by fiscal years between 2008 to 2013.Capital ($/m²)

Text description for the graph Capital ($/m²)

This graph delineates average capital expenses for Québec Region of PWGSC's crown-owned office portfolio, by fiscal years between 2008 to 2013.Vacancy Rate (%)

Text description for the graph Vacancy Rate (%)

This graph lists by percentage the Québec Region vacancy rate of PWGSC's crown-owned office portfolio, between 2008 to 2013.National Capital Region

The National Capital Region consists of the National Capital Area (comprised of Greater Ottawa and Gatineau), as well as Nunavut.

In 2012-13, the National Capital Region represented 19 % of the national Crown-owned office portfolio based on building count and 54 % of the national Crown-owned office portfolio's building floor area (m²).

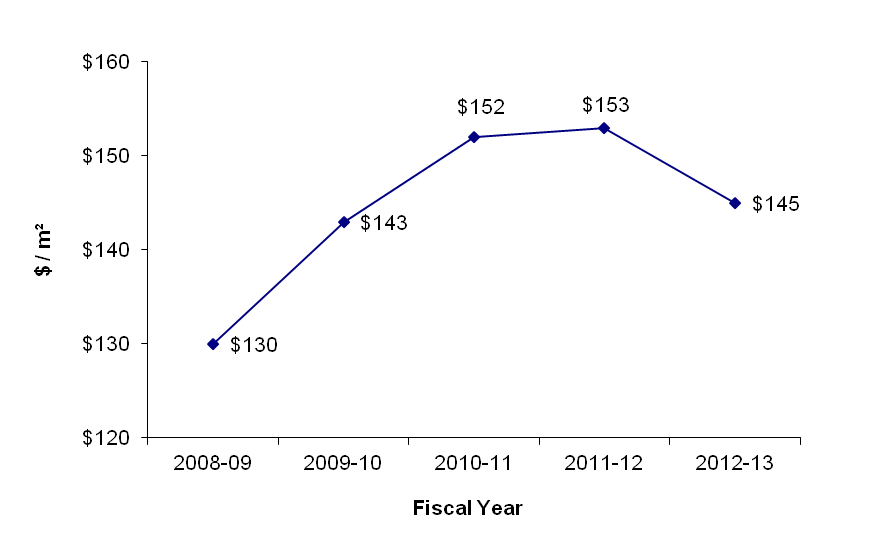

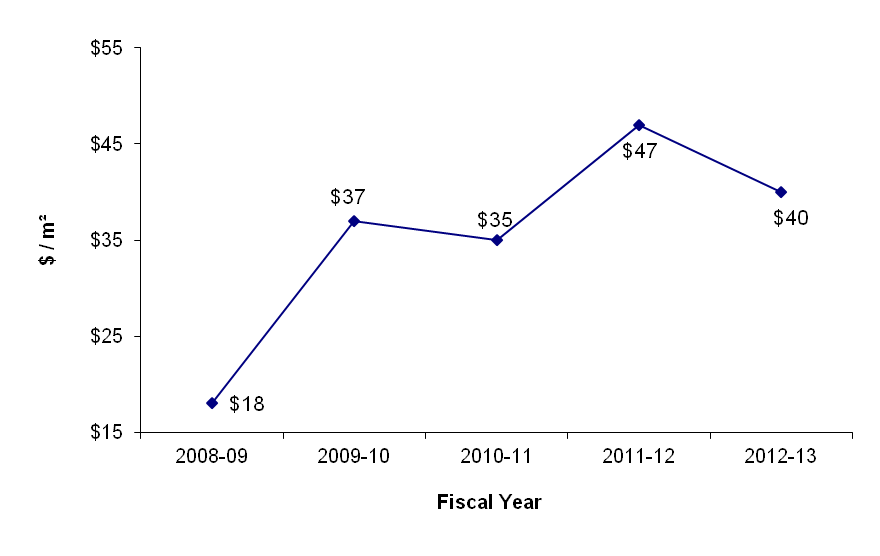

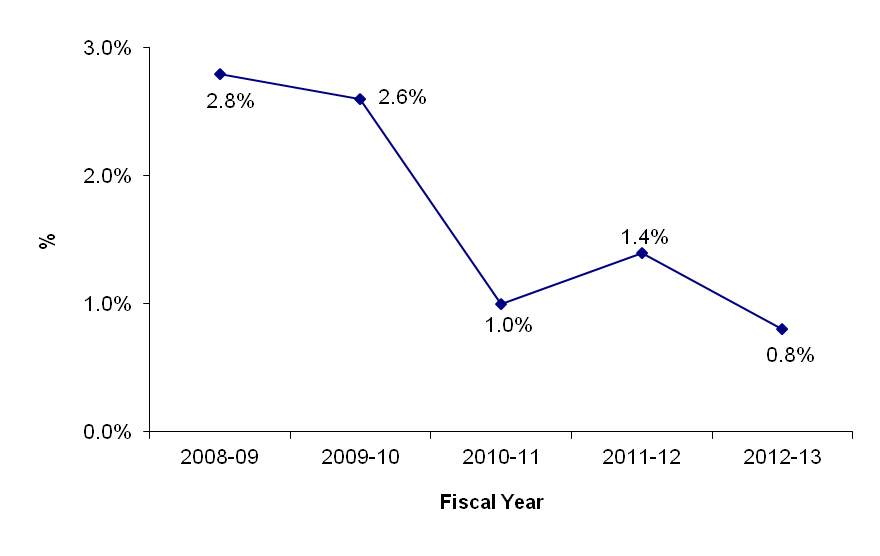

Over the past five years, as presented in the table below, the National Capital Region's Crown-owned office portfolio has stayed relatively constant. It currently consists of 40 office buildings totalling 1,494 million m². As illustrated in the graphs below, there was an increase in the portfolio's average operating and maintenance expenses and capital for the period 2008-09 to 2011-12, due in large part to the Accelerated Infrastructure Program. In 2012-13, both O&M and capital expenditures fell, while the vacancy rate dropped below 1%.

Table Summary

This table provides information on the crown-owned office portfolio for the National Capital Region over the past five years. The information consist of the number of office buildings, the size and the average age of the buildings, the market value, the average operating and maintenance expenses and capital expenditures and the vacancy rate.| Indicator | 2008-09 | 2009-10 | 2010-11 | 2011-12 | 2012-13 |

|---|---|---|---|---|---|

| # Office Buildings | 39 | 36 | 41 | 40 | 40 |

| Space (m² in 000s) | 1,148 | 1,101 | 1,242 | 1,405 | 1,494 |

| Average Age (years) | 55 | 53 | 49 | 50 | 50 |

| Market Value ($/m²) | $1,694 | $1,906 | $1,979 | $1,990 | $2,272 |

| O&M ($/m²) | $130 | $143 | $152 | $153 | $145 |

| Capital ($/m²) | $18 | $37 | $35 | $47 | $40 |

| Vacancy Rate (%) | 2.8% | 2.6% | 1.0% | 1.4% | 0.8% |

O&M ($/m²)

Text description for the graph O&M ($/m²)

This graph lists the National Capital Region operating and maintenance expenses (O&M) of PWGSC's crown-owned office portfolio, by fiscal years between 2008 to 2013.Capital ($/m²)

Text description for the graph Capital ($/m²)

This graph delineates the average capital expenses for the National Capital Region of PWGSC's crown-owned office portfolio, by fiscal years between 2008 to 2013.Vacancy Rate (%)

Text description for the graph Vacancy Rate (%)

This graph lists by percentage the National Capital Region vacancy rate of PWGSC's crown-owned office portfolio by fiscal years between 2008 to 2013.Ontario Region

The Ontario Region consists of the province of Ontario, with the exception of the Greater Ottawa Area. The Greater Toronto Area dominates the Ontario Region inventory. Other notable urban markets include Hamilton, London, Windsor, Sudbury and Kingston.

In 2012-13, the Ontario Region represented 15 % of the national Crown-owned office portfolio based on building count and 12 % of the national Crown-owned office portfolio's building floor area (m²).

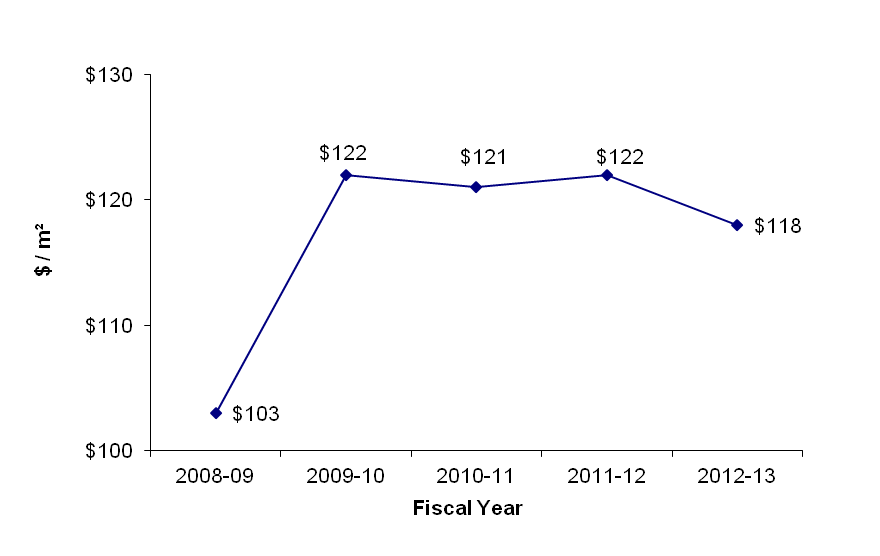

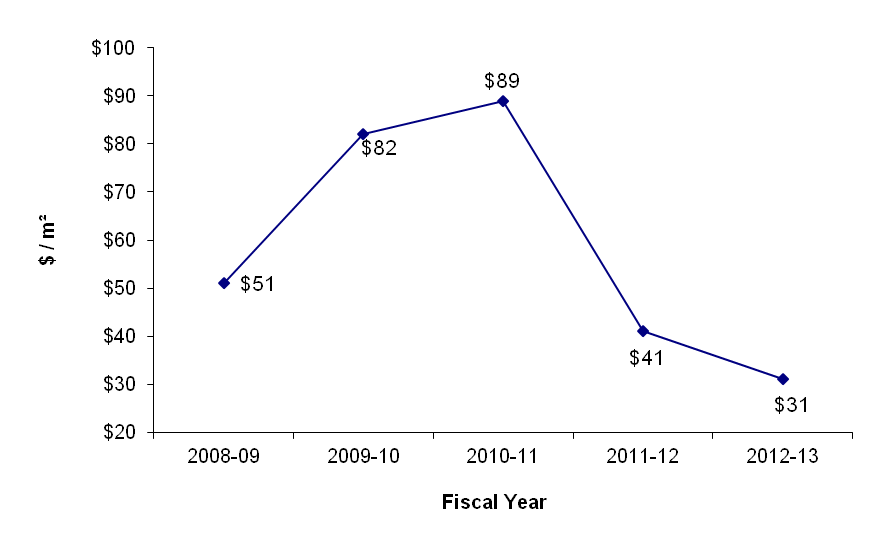

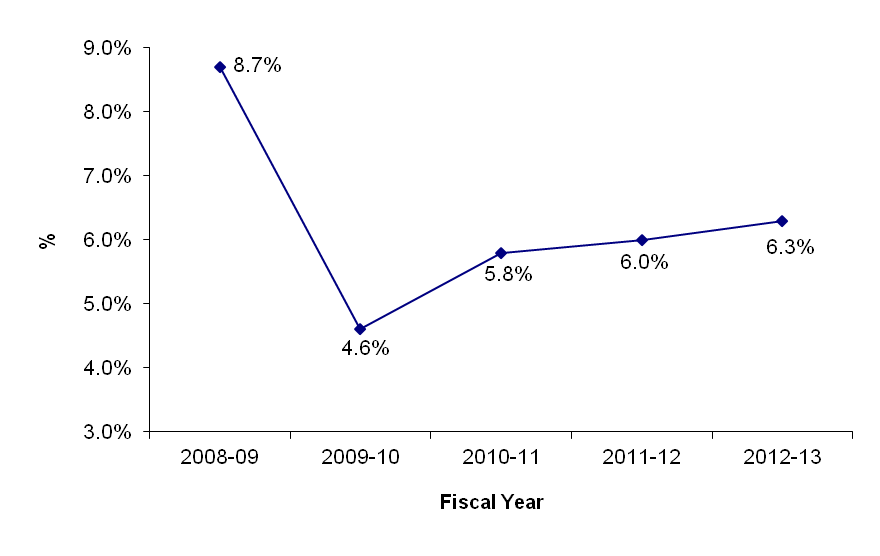

Over the past five years, as presented in the table below, the Ontario Region's Crown-owned office portfolio has steadily decreased. It currently consists of 33 office buildings totalling 326, 811m². As illustrated in the graphs below, O&M expenditures and vacancy rates have remained relatively stable, while capital expenditures have decreased substantially.

Table Summary

This table provides information on the crown-owned office portfolio for the Ontario region over the past five years. The information consist of the number of office buildings, the size and the average age of the buildings, the market value, the average operating and maintenance expenses and capital expenditures and the vacancy rate.| Indicator | 2008-09 | 2009-10 | 2010-11 | 2011-12 | 2012-13 |

|---|---|---|---|---|---|

| # Office Buildings | 38 | 37 | 38 | 37 | 33 |

| Space (m² in 000s) | 335 | 334 | 342 | 341 | 327 |

| Average Age (years) | 57 | 59 | 60 | 62 | 62 |

| Market Value ($/m²) | $768 | $863 | $1,124 | $1,721 | $1,849 |

| O&M ($/m²) | $103 | $122 | $121 | $122 | $118 |

| Capital ($/m²) | $51 | $82 | $89 | $41 | $31 |

| Vacancy Rate (%) | 8.7% | 4.6% | 5.8% | 6.0% | 6.3% |

O&M ($/m²)

Text description for the graph O&M ($/m²)

This graph lists the Ontario Region operating and maintenance expenses (O&M) of PWGSC's crown-owned office portfolio, by fiscal years between 2008 to 2013.Capital ($/m²)

Text description for the graph Capital ($/m²)

This graph delineates the average capital expenses for the Ontario Region of PWGSC's crown-owned office portfolio, by fiscal years between 2008 to 2013.Vacancy Rate (%)

Text description for the graph Vacancy Rate (%)

This graph lists by percentage of the Ontario Region vacancy rate of PWGSC's crown-owned office portfolio, by fiscal years between 2008 to 2013.Western Region

The Western Region consists of the provinces of Manitoba, Saskatchewan and Alberta, as well as the Northwest Territories. Key urban markets include Winnipeg, Regina, Saskatoon, Calgary, Edmonton and Yellowknife.

In 2012-13, the Western Region represented 10 % of the national Crown-owned office portfolio based on building count and 6.5 % of the national Crown-owned office portfolio's building floor area (m²).

Western Region also manages a housing portfolio of 350 Crown-owned and 45 leased units.

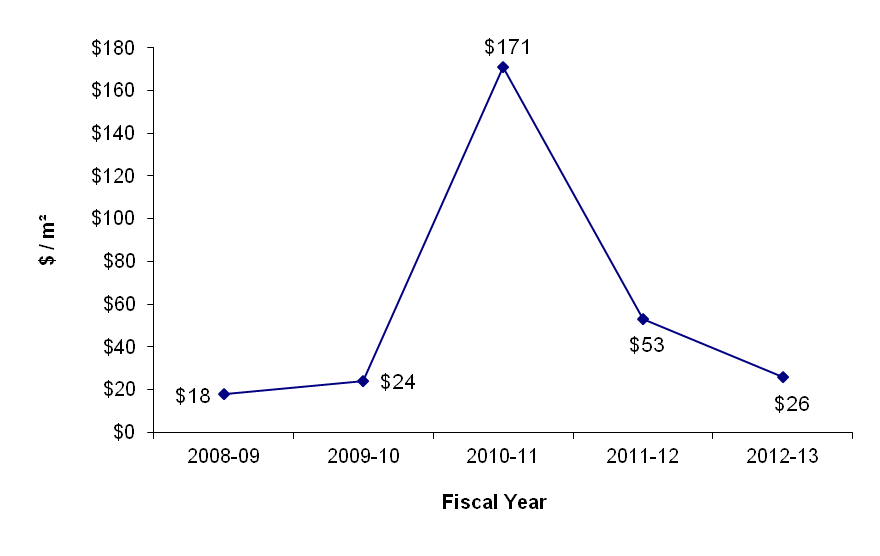

Over the past five years, as presented in the table below, the Western Region's Crown-owned office portfolio stayed relatively constant. It currently consists of 22 assets totalling 181,566 square metres. As illustrated in the graphs below, the portfolio's operating and maintenance expenses increased gradually over the years while capital expenditures have fluctuated sharply. Vacancy rate has increased in 2012-13 but remains below the long term average.

Table Summary

This table provides information on the crown-owned office portfolio for the Western region over the past five years. The information consist of the number of office buildings, the size and the average age of the buildings, the market value, the average operating and maintenance expenses and capital expenditures and the vacancy rate.| Indicator | 2008-09 | 2009-10 | 2010-11 | 2011-12 | 2012-13 |

|---|---|---|---|---|---|

| # Office Buildings | 22 | 22 | 22 | 22 | 22 |

| Space (m² in 000s) | 181 | 182 | 182 | 182 | 182 |

| Average Age (years) | 46 | 47 | 49 | 50 | 51 |

| Market Value ($/m²) | $1,340 | $1,265 | $1,578 | $1,736 | $1,921 |

| O&M ($/m²) | $135 | $134 | $139 | $148 | $140 |

| Capital ($/m²) | $18 | $24 | $171 | $53 | $26 |

| Vacancy Rate (%) | 9.7% | 4.9% | 2.2% | 1.7% | 3.7% |

O&M ($/m²)

Text description for the graph O&M ($/m²)

This graph illustrates the average operating and maintenance expenses (O&M) of PWGSC's crown-owned office portfolio for the Western Region, by fiscal years between 2008 to 2013.Capital ($/m²)

Text description for the graph Capital ($/m²)

This graph delineates average capital expenses for the Western Region of PWGSC's crown-owned office portfolio, by fiscal years between 2008 to 2013.Vacancy Rate (%)

Text description for the graph Vacancy Rate (%)

This graph lists by percentage the Western Region vacancy rate of PWGSC's crown-owned office portfolio, by fiscal years between 2008 to 2013.Pacific Region

The Pacific Region serves British Columbia and the Yukon. Key urban markets include Vancouver, Victoria and Whitehorse.

In 2012-13, the Pacific Region represented 13 % of the national Crown-owned office portfolio based on building count and 9 % of the national Crown-owned office portfolio's building floor area (square metres).

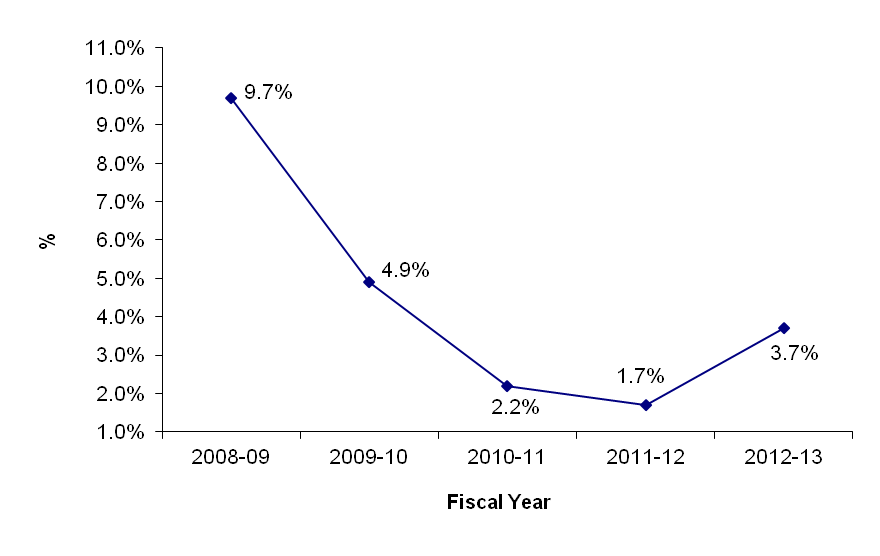

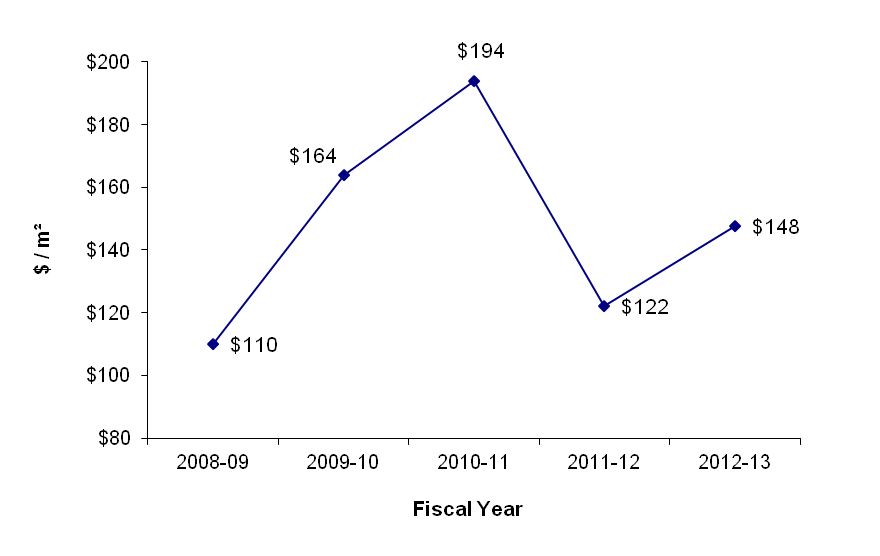

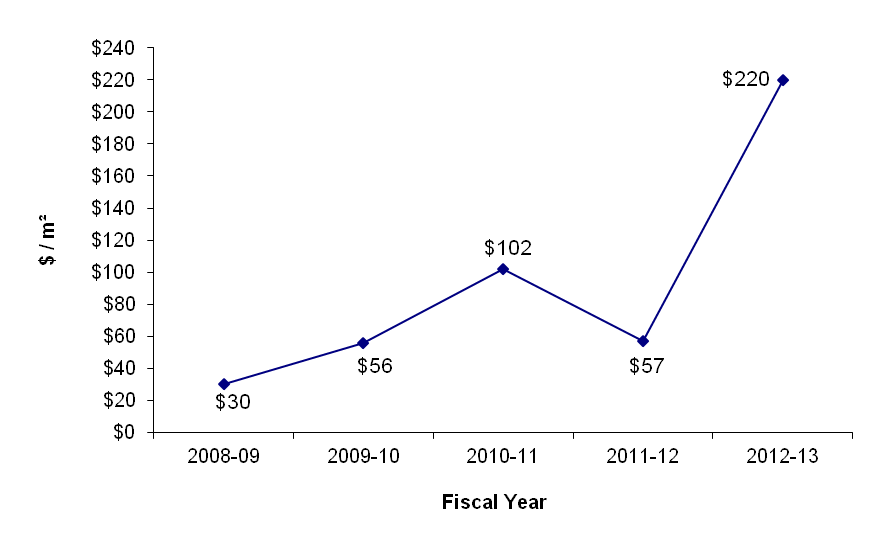

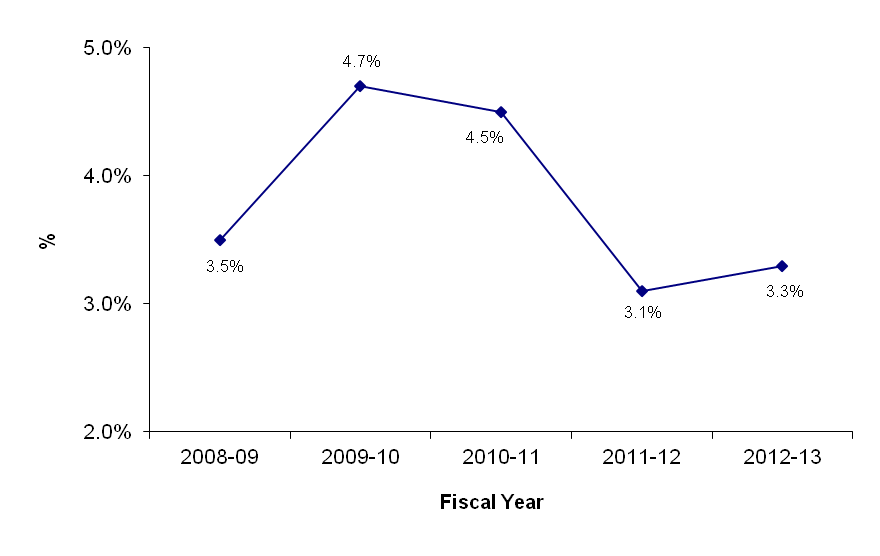

Over the past five years, as presented in the table below, the Pacific Region's Crown-owned office portfolio has stayed relatively constant. It currently consists of 28 office buildings totalling 248,031 m². As illustrated in the graphs below, there was an increase in the portfolio's average operating and maintenance expenses and capital expenditures in 2009-10 and 2010-11, due in large part to the Accelerated Infrastructure Program. 2011-12 witnessed a significant reduction in both O&M and capital expenditures. The significant increase in capital costs is largely attributable to the construction of a new RCMP headquarters (E Division) building in Surrey, British Columbia. The portfolio's vacancy rate fluctuated and is now 3.3%.

Table Summary

This table provides information on the crown-owned office portfolio for the Pacific Region over the past five years. The information consist of the number of office buildings, the size and the average age of the buildings, the market value, the average operating and maintenance expenses and capital expenditures and the vacancy rate.| Indicator | 2008-09 | 2009-10 | 2010-11 | 2011-12 | 2012-13 |

|---|---|---|---|---|---|

| # Office Buildings | 28 | 28 | 28 | 27 | 28 |

| Space (m² in 000s) | 179 | 179 | 180 | 178 | 248 |

| Average Age (years) | 43 | 44 | 44 | 44 | 43 |

| Market Value ($/m²) | $2,283 | $2,413 | $3,118 | $3,405 | $2,867 |

| O&M ($/m²) | $110 | $164 | $194 | $122 | $148 |

| Capital ($/m²) | $30 | $56 | $102 | $57 | $220 |

| Vacancy Rate (%) | 3.5% | 4.7% | 4.5% | 3.1% | 3.3% |

O&M ($/m²)

Text description for the graph O&M ($/m²)

This graph illustrates the average operating and maintenance expenses (O&M) of PWGSC's crown-owned office portfolio for the Pacific Region, by fiscal years between 2008 to 2013.Capital ($/m²)

Text description for the graph Capital ($/m²)

This graph delineates average capital expenses for the Pacific Region of PWGSC's crown-owned office portfolio, by fiscal years between 2008 to 2013.Vacancy Rate (%)

Text description for the graph Vacancy Rate (%)

This graph lists by percentage the Pacific Region vacancy rate of PWGSC's crown-owned office portfolio, by fiscal years between 2008 to 2013.Engineering Assets Portfolio

PWGSC portfolio of engineering assets consists of seven bridges, four dam complexes, nine specialized assets and an inventory of marine assets.

PWGSC engineering assets are unique structures located throughout Canada. The majority of these assets are vital to the public they serve, from the "Camere-style" St. Andrews Lock and Dam in Manitoba, to the picturesque Alexandra Bridge, in the National Capital Area, to the Alaska Highway, an artery woven into the heart of the North.

The 1985 Nielsen Task Force directed departments to divest themselves of assets no longer required for program purposes. Since 1985, PWGSC has divested itself of 16 assets, leaving 19 surplus assets in its inventory.

In 2012-13, $47.3 million in capital projects were delivered and further expanded our understanding of the complexities of our unique portfolio, through the completion of 21 studies and 9 inspection reports.

The Department was also able to reduce its inventory of wharf and marine assets from 68 in 2011-12 to 33 in 2012-13.

- Date modified: