22-26 James Street South

THE HEART OF THE CITY

CANADA LIFE ASSURANCE COMPANY

22-26 James Street South

CURRENT STATUS (1999) Demolished in 1972

BUILDING INFORMATION

Date Built: Pre-1883; rebuilt after fire in 1929

Original Owner: Canada Life Assurance Co.

Original Use: Same

Subsequent Uses: Fidelity Management Ltd.

Size: Five-storey

Architect, Builder: Architect Richard Waite of New York

Design and Style: Gothic

Construction Materials: Connecticut brown stone

Main Architectural Feature: Copper roof; display windows; charging horsemen clock

The Canada Life Assurance Company was the first life insurance company in Canada. It was founded by Hugh Cossart Baker Sr., a Hamilton bank manager, who wanted some sort of financial protection for his family. He travelled on horseback to New York to secure a life insurance policy at a premium of one per cent above the normal rates due to "climactic hazards of living in Canada". It was during his travels that Baker thought about the nature of the service for which he had to travel great distances to receive. He decided that such a service was necessary in Canada, and decided to organize a company to fulfill the need.

The young British immigrant began to organize a

company and won the support of a group of important Hamilton professionals and

businessmen. These individuals included Burton, Cartwright, Kerr, MacNab, Thomas, and

Young. Their first meeting took place in November of 1846. By May of the following year,

it was announced that the company had been founded. The Canada Life Assurance Company

officially opened on August 21, 1847. The capitol required was 50,000 pounds in 500 shares

of 100 pounds each. Only two months after the opening, Baker and 62 other individuals from

Hamilton, Toronto, and Montreal became shareholders.

The young British immigrant began to organize a

company and won the support of a group of important Hamilton professionals and

businessmen. These individuals included Burton, Cartwright, Kerr, MacNab, Thomas, and

Young. Their first meeting took place in November of 1846. By May of the following year,

it was announced that the company had been founded. The Canada Life Assurance Company

officially opened on August 21, 1847. The capitol required was 50,000 pounds in 500 shares

of 100 pounds each. Only two months after the opening, Baker and 62 other individuals from

Hamilton, Toronto, and Montreal became shareholders.

At the first meeting of the shareholders, 20 directors were elected. At the mere age of 29, Hugh was the President, General Manager and Actuary of the company. The directors met once a week in a rented office located on the top floor of the Mechanics’ Institute relying heavily on the President’s self-taught knowledge of insurance and actuarial techniques.

The idea of purchasing life insurance was a relatively new notion to the people of Hamilton. The company, in order to become successful and profitable, had to sell this strange idea to the public. In order for this task to be accomplished, an advertising department was established. Hugh Baker arranged lectures on the importance and usefulness of life insurance. Baker worked hard in an attempt to secure public support and often faced with great difficulty when attempting to convince his board members of the efficiency of his new techniques.

Baker was President of the company from 1847 until his death in 1859. George C. Burton became the first legal advisor. In the early days, the company was continually surrounded by an air of skepticism. Many people believed that Canada was too small to have such a company. In response to such accusations, Baker argued that the company, being located in the country, allowed policyholders to avoid delays associated with claims processed abroad by other companies. Buying insurance at home would stop the flow of capitol out of the country and strengthen Canada’s economy.

At the company’s first annual meeting, held on August 1, 1848, it was announced that 166 policies had been issued. A total coverage available to purchasers was 59,650 pounds, and the revenue gained by the company was 1,850 pounds. The total receipts for the first year was estimated at 2,153 pounds while expenses incurred were valued at 380 pounds. Policies issued by the company were equipped with a cancellation clause whereby the agreement could be cancelled if the insured individual drank too much which would increase chance of accident. There were also travelling restrictions placed on policies.

Baker was also President of the Bank of Montreal. The stress of occupying this position as well as being President of the Life Assurance Company was overwhelming. He eventually resigned from the Bank of Montreal in April of 1850, and later accepted an appointment as Managing Director of the Great Western Railway, after gaining the Board’s approval. He was also appointed as Corresponding Member for Canada of the Institute of Actuaries in England. Baker received remarkable distinction for a self-taught insurance man.

![]() A coat-of-arms was bought for the

company at a cost of 5 pounds. The central image of the coat-of-arms was a pelican feeding

its young. This image came to symbolize the charity and piety in ecclesiastical heraldry.

This symbol is still used by the company in present day.

A coat-of-arms was bought for the

company at a cost of 5 pounds. The central image of the coat-of-arms was a pelican feeding

its young. This image came to symbolize the charity and piety in ecclesiastical heraldry.

This symbol is still used by the company in present day.

On April 25, 1849, the Company received a charter from the Province of Canada which included the French name "La Compagnie d’assurance du Canada sur la vie". The charter allowed an increase in the capitol stock to an amount of 250,000 pounds. The charter was carried out in 1858. By 1852, the company had fifty men in the field, covering the Province of Canada, Newfoundland, New Brunswick and even parts of the United States (Michigan and Detroit). An advisory board was formed in Montreal. In 1854, a reciprocity treaty was signed.

Seven years after its opening, the company was in need of a new building. Their

financial success enabled them to purchase both the property and building where the

Pigott Building is currently located on James Street South. In October 1852, the

Company’s tenth annual meeting was held in the new quarters. In 1858, as new

businesses slowed, rules were released to help policyholders maintain protection.

purchase both the property and building where the

Pigott Building is currently located on James Street South. In October 1852, the

Company’s tenth annual meeting was held in the new quarters. In 1858, as new

businesses slowed, rules were released to help policyholders maintain protection.

In March of 1859, after being defeated in a bid for a seat in the Provincial Legislature, Hugh Baker died of tuberculosis at the young age of 41 years. The company, finding itself without the guidance of its leader, struggled to maintain financial stability at a time of economic depression, which was aggravated by a succession of regional crop failures.

John Young was elected President, succeeding Baker. Board members agreed that the general manager had to possess knowledge of insurance. In order to find the right man, five directors sailed to Britain. The man they found was Alexander Gillespie Ramsay, Secretary of the Scottish Amicable Assurance Society of Glasgow. Following long negotiations, the directors and Ramsay agreed on a three-year period of service at a starting salary of 600 pounds, which would increase by 100 pounds annually. He arrived in August and his career as actuary lasted 40 years.

Young, from his first day in Hamilton, established

new objectives for the company. These included an increase in liberalization of service to

policyholders and a more positive expression of the company’s investment policy. Many

of his innovative decisions became cornerstones upon which further growth of the company

was founded. Under Young, a same cost coverage was made available to people travelling to

populated areas in many parts of North America and parts of Europe. On October 1860, just

fifteen months after his arrival, Young announced a record year for premiums collected and

new policies issued.

Young, from his first day in Hamilton, established

new objectives for the company. These included an increase in liberalization of service to

policyholders and a more positive expression of the company’s investment policy. Many

of his innovative decisions became cornerstones upon which further growth of the company

was founded. Under Young, a same cost coverage was made available to people travelling to

populated areas in many parts of North America and parts of Europe. On October 1860, just

fifteen months after his arrival, Young announced a record year for premiums collected and

new policies issued.

In 1861, George A. Cox in association with the Canada Life Assurance Company, created a Contact Agency in Peterborough. Cox ran this agency with his sons over a period of 86 years. In 1869, Canada Life Assurance’s new business passed the million-dollar mark for the first time ever. The company established regional advisory boards and increased the number of agents associated with the company.

Directors were expected to keep in touch with every aspect of the company including the activities of personnel. Under the direction of Ramsay, the business force had tripled, assets had doubled, and the business was three times larger than its original size. The company purchased land on the north side of Toronto’s King Street.

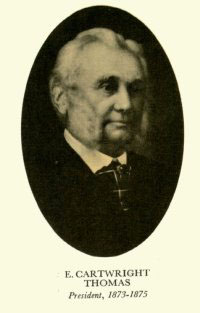

In 1873, Young died and was replaced by E. Cartwright Thomas who previously served as

Vice-President. Ramsay was elected to the Board and named Managing

Director. George Cox, the aggressive agent in Peterborough was showing interest in

politics. His influence in the Liberal Party continued and he was eventually appointed to

the Senate.

was elected to the Board and named Managing

Director. George Cox, the aggressive agent in Peterborough was showing interest in

politics. His influence in the Liberal Party continued and he was eventually appointed to

the Senate.

In May of 1875, Cartwright Thomas died and Alexander Ramsay was appointed as President. His first three years as president coincided with Canada’s struggle to offset reduced exports and falling prices. In 1879, the Company’s charter was amended to give an increased share of profits to policyholders and entered the mortgage market.

In 1883, the company sold policies to British Columbia. That same year they moved into a new brownstone building on the southeast corner of Hamilton’s King and James Streets. In 1887 the travel restriction was lifted from policies that were older than two years. George Cox eventually travelled to Hamilton and set up his office. By 1891, Cox was directing operations from the new Canada Life Building on King Street West. Directors met weekly and at one sitting would consider from 50 to 200 policy applications.

The United States division of the Canada Life Assurance Company was established in 1889. It was during the 1892 meeting that the President announced that Michigan was the fourteenth American agency of a total of 342. Minnesota and Ohio joined in 1893 and two years later, Illinois joined.

In 1899, only four years after the Quebec branch of

the Life Assurance company opened in Montreal, the Directors voted in favor of moving the

head office from Hamilton to Toronto. The agreement was not unanimous. President Ramsay

and several others opposed the proposed move by George Cox (then senator and company

Director). All staff members were compensated with a moving expense account and an

increase in salary. The Canada Life Assurance Company sold their Hamilton property to

Henry Birks.

In 1899, only four years after the Quebec branch of

the Life Assurance company opened in Montreal, the Directors voted in favor of moving the

head office from Hamilton to Toronto. The agreement was not unanimous. President Ramsay

and several others opposed the proposed move by George Cox (then senator and company

Director). All staff members were compensated with a moving expense account and an

increase in salary. The Canada Life Assurance Company sold their Hamilton property to

Henry Birks.

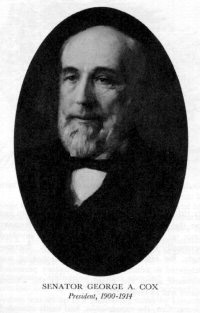

In December of that year (1893), Mr. Ramsay retired rather than moving from Hamilton to

Toronto. Senator Cox was chosen as the next President of the company in January of 1900.

The Cox era began with the launch of a spectacular expansion of the company’s agency

operations into Canada, the United States and Britain. The first branch of the agency in

the American West was established in Washington State in 1901. That same year, the

company entered New York State.

Washington State in 1901. That same year, the

company entered New York State.

In 1902 the success of the company received Royal approval. A policy had been issued on the life of King Edward VII. In 1903 a branch was established in Britain. It was not long after that a network was established across England, Scotland and Ireland marking the beginning of the division that today served the United Kingdom and the Republic of Ireland.

In New York State, new insurance laws were passed which required companies to pay dividends annually. Rather than comply with the implemented program, the Canada Life Assurance Company left the United States in 1906 and did not return for a period of 20 years. In response to their departure, Canadian newspapers launched an aggressive attack on the life insurance industry demanding an investigation into operations. A government commission was appointed to investigate the affair. Senator Cox appeared before the inquiry along with a brilliant young lawyer named Leighton McCarthy, who later became one of the Company’s outstanding Presidents. In the end, the company was found to be operating within established parameters .

In 1910, an amendment to the Dominion Insurable Act ruled that Canadian life insurance companies had to appropriate 90 per cent of their surplus to the policyholders and 10 per cent to its shareholders. This ratio had been established by the Canada Life Assurance Company thirty years earlier.

In 1925, the Directors voluntarily raised the

policyholder’s share to 95 per cent. By 1913, the internal administration of

the company had lost the personal touch that once characterized the Baker-Ramsay days. The

top executives could no longer be personally involved in daily transactions and

responsibility for decision-making was transferred to administrative personnel that were

scattered across the country. In 1913, George Cox handed the post of General Manager over

to his eldest son Edward W. Cox, who had acted as Vice-President since 1906. George Cox

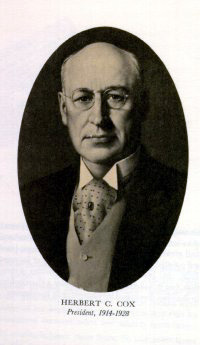

died the following year, only four days after his retirement. His son took over in and

acted as President until early June when he failed to recover from an operation he had

undergone in England. The Directors quickly elected a third member of the Cox family to

the presidency. This time it was the youngest son, Herbert C. Cox.

In 1925, the Directors voluntarily raised the

policyholder’s share to 95 per cent. By 1913, the internal administration of

the company had lost the personal touch that once characterized the Baker-Ramsay days. The

top executives could no longer be personally involved in daily transactions and

responsibility for decision-making was transferred to administrative personnel that were

scattered across the country. In 1913, George Cox handed the post of General Manager over

to his eldest son Edward W. Cox, who had acted as Vice-President since 1906. George Cox

died the following year, only four days after his retirement. His son took over in and

acted as President until early June when he failed to recover from an operation he had

undergone in England. The Directors quickly elected a third member of the Cox family to

the presidency. This time it was the youngest son, Herbert C. Cox.

It was around this same time that the dark clouds of the First World War hung overhead. The company was soon confronted with a test. One

of Herbert’s first decisions was the introduction of new training courses to improve

the efficiency of those agents who were not able to work overseas. The education program

was successfully implemented. In Great Britain, the Canada Life Assurance Company had been

one of the few companies to maintain its dividends during the war years. From 1919-1920,

the company doubled its new business.

The company was soon confronted with a test. One

of Herbert’s first decisions was the introduction of new training courses to improve

the efficiency of those agents who were not able to work overseas. The education program

was successfully implemented. In Great Britain, the Canada Life Assurance Company had been

one of the few companies to maintain its dividends during the war years. From 1919-1920,

the company doubled its new business.

The company was launching new services such as group life insurance. Such ideas arose in New York approximately nine years previous. The first group life insurance plan was issued in November 1919. Under the plan, 300 workers of a leather company were secured for a total of $300,000. The contract was viable for over 40 years until the company was bought by a larger organization. Within months, the first municipal contract was written covering employees of the City of Calgary for $1,000,000. By 1928, the Canada Life Assurance Company had over $1,000,000,000 of group life insurance profits.

In 1920, the company was examined by insurance commissioners from Michigan, Illinois, Pennsylvania and Minnesota. The result was a confirmation of the company’s financial soundness and approval of its selection of investments and services. That same year, the company celebrated its 75th anniversary. The company, with ever increasing profits, came to be respected on the Pacific Coast from the Mexican border to Prince Rupert, British Columbia and received widespread acceptance in the United States. The company was one of few pioneering companies who introduced non-medical insurance in 1922.

In 1926, the company re-entered New York with great success and a recorded high level of performance. In July of 1928, Herbert, after having strengthened the company during the financial crises of the war and post-war years, submitted his resignation. The next President was Leighton Goldie McCarthy, a lawyer and former Member of Parliament. He was appointed as Director, Vice-President and General-Council of the company. Under his direction, the company acquired a new home in Toronto located at University Avenue and Queen Street West.

On the 29th of October, 1929, the Stock Market crashed, leaving many without work and investors ruined. Many people, because of financial problems, were forced to borrow on policies or allow them to lapse. Despite the economic conditions, the Canada Life Assurance Company and its 626 employees, moved into the new Toronto building. In 1932, the decline of insurance policies fell to half the level attained in the two pre-depression years. Loans on policies and cash surrender values were made available as a source of income for the insured. The company paid out more than $106 million dollars. The company hit its lowest point in 1934, but was saved by a sound investment program. By the end of 1935, the Canada Life Assurance Company’s assets exceeded $250 million dollars, for the first time ever. By 1938, the company was on the road to a safe recovery.

Leighton McCarthy resigned from his previous

positions but remained on as Acting Chairman for another eight years. McCarthy’s

personal friendship with President Roosevelt played an important role in cementing

Canada-U.S. relations. Alfred Michell then became President.

Leighton McCarthy resigned from his previous

positions but remained on as Acting Chairman for another eight years. McCarthy’s

personal friendship with President Roosevelt played an important role in cementing

Canada-U.S. relations. Alfred Michell then became President.

The outbreak of World War II again challenged the stability of the company. The divisions serving Great Britain and Ireland had to be moved while inflation was being fought in Canada. The company directors made speeches in order to alert the public of the damaging effect of inflation. Despite lowered business, the company managed to survive.

In 1946, Alfred Mitchell retired as President but remained on as Director. He died in

1963, at the age of 87 years. In January of the following year, St. Clair McEvenue became

President and resigned in 1948 because of failing health. Edwin G. Baker, who was related

to the company’s founder, became President, after serving as Vice-President for eight

years. It was under his administration that the company

experienced steady growth, particularly in the United States. The Canada Life Assurance

Company was one of the companies which supported the American College of Life Underwriters

and The Life Underwriters Association of Canada.

It was under his administration that the company

experienced steady growth, particularly in the United States. The Canada Life Assurance

Company was one of the companies which supported the American College of Life Underwriters

and The Life Underwriters Association of Canada.

In 1951, Edwin G. Baker resigned and was succeeded by Emert C. Gill, a brilliant mathematician and gold medallist at Queen’s University. Under his direction, the company entered into real estate and mortgage loans. By 1953, 33 branch offices and 14 mortgage offices had been established in Canada, and 23 branch offices had been established in the United Kingdom and the Republic of Ireland.

Federal legislation, passed in December 1957 allowed all the assets belonging to the company to be owned by the policyholders. This was the focal point of Gill’s activities. In 1964, A. Hazlett Lemmon was appointed President.

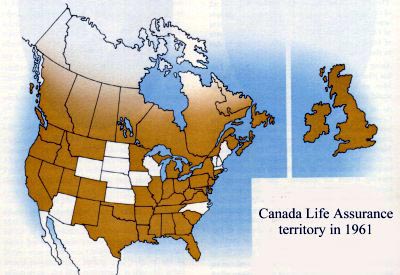

Today, Canada Life Assurance Company is among the top 30 North American insurers providing services to more than eight million policyholders throughout Canada, the United States, the United Kingdom, and Ireland. The maintenance of financial strength and stability while growing and serving the changing needs of the marketplace has always been a fundamental to their management approach. Conservative management practices have served policymakers in both good and bad economic times. The company is noted for consistently earning high ratings from independent financial rating agencies. Today, Canada Life is a member of CompCorp, a federally incorporated private company responsible for the administration of a Customer Protection Plan.

See also: http://205.150.149.18/