Common menu bar

Piste de navigation

- Accueil >

- Revenu total de bien-être social : Étape 1 >

- CHAPTER 6 - ASSET EXEMPTIONS

Chapter 6

ASSET EXEMPTIONS

Mary and Shannon’s story

Mary is a 43-year old lone parent who worked in the automotive sector in Windsor for most of her working life. She has one child, Shannon, who is 15. Ten years ago she made a small down payment on a house. She put some money into a Registered Education Savings Plan for her daughter and built up $8,000 in her own Registered Retirement Savings Plan. She also usually had about $1,000 in her bank account.

In 2008, Mary was laid off and started to receive Employment Insurance benefits. She kept looking for work, but with unemployment running at over 10 percent in her area she wasn’t able to find a job. She soon had nothing left in her bank account. When her EI ran out, she applied for welfare. But Mary wasn’t eligible.

Mary was told that she would have to cash in her RRSP before she would be eligible for welfare. With food, a mortgage and bills to pay, she did so. Now the proceeds are almost all gone. Mary is now eligible for welfare. But she faces the prospect of having to sell her home because she won’t be able to make her mortgage payments. When she does sell it, any profit that she makes will be counted as an asset and she may be denied welfare again.

Mary and her daughter face a daunting and grim future. No job prospects, losing their home and most likely going back on welfare.

Mary’s troubles aren’t over yet. She doesn’t realize it, but next year she’ll have to pay additional taxes on the RRSP that she cashed in. If she has sold her home and made any profit, she may be able to pay. But how will she pay if she’s on welfare? Mary may have to agree to a reduction in Shannon’s federal child benefits to pay the tax she owes, leaving her and Shannon with even less to live on.

Anyone applying for welfare must undergo an asset test in order to qualify. This test looks at fixed assets and liquid assets. Fixed assets generally include the residence, household and personal effects, a vehicle (up to a certain value), and items required for employment. Liquid assets include cash on hand and in a bank account, plus other types of investments and securities that can be readily converted into cash. Applicants whose assets exceed the limits set by the provinces and territories are not eligible for welfare.

Provinces and territories decide which types of assets are exempt. In recent years, they have all exempted Registered Education Savings Plans and Registered Disability Savings Plans from the liquid asset test. However, Registered Retirement Savings Plans are still considered a liquid asset in most jurisdictions. Only Newfoundland and Labrador, Quebec and Alberta exempt RRSPs up to a specified amount.1

In this chapter, we focus on liquid asset exemption provisions. We look at the 2009 levels and how they have changed over the last 20 years.

2009 LIQUID ASSET EXEMPTION LEVELS

Table 6.1 shows the liquid asset exemption levels as of January 2009. We have noted where there are different levels for people applying for welfare compared to those already receiving welfare.

There were few changes between 2008 and 2009. In Ontario and Alberta, the limits for the single employable person, the lone parent with one child and the couple with two children increased slightly because they are linked to the benefit levels. Alberta also increased the limit for the single person with a disability for the same reason. Manitoba is the notable exception. In January 2009, Manitoba increased its asset exemption level to a flat rate of $4,000 per person in a household (to a maximum of $16,000), regardless of the reason for assistance. With the exception of the single person with a disability, Manitoba’s asset exemption levels are now the highest across the country.

For a single person considered employable, the maximum allowable liquid assets in 2009 ranged from $0 in Nunavut to $4,000 in Manitoba. For a single person with a disability, the lowest amount was $500 in Nova Scotia and the highest was $5,000 in Ontario, the Northwest Territories and Nunavut. For a lone parent with one child, amounts ranged from a low of $0 in Nunavut to a high of $8,000 in Manitoba. For a couple with two children, Nunavut had the lowest amount at $0 and Manitoba the highest at $16,000. In most cases, the amounts are barely enough to live on for a month in a large Canadian city.

LIQUID ASSET EXEMPTION LEVELS, 1989 to 2009

We looked at how provincial liquid asset exemption levels have changed over the past 20 years, based on our Welfare Incomes reports. Many of the levels shown for 1989 may already have been in place for several years.

Table 6.2 shows the provincial levels in effect at five-year intervals from 1989 to 2009 for those applying for welfare. In Manitoba and Nova Scotia, single employable persons and couples with two children were not allowed to have any assets until recently. In many provinces, there has been no change over the full 20-year period, and in several there has actually been a decrease.

| Table 6.1: Liquid asset exemption levels as of January 2009Provisions for applicants and recipients* | ||||

|---|---|---|---|---|

| Single Person Considered Employable | Single Person with a Disability | Lone Parent, One Child | Couple, Two Children | |

| Newfoundland and Labrador | $500 | $3,000 | $1,500 | $1,500 |

| Prince Edward Island | $50 to $200 | $900 | $50 to $1,200 | $50 to $1,800 |

| Nova Scotia | $500 | $500 | $1,000 | $1,000 |

| New Brunswick | $1,000 | $3,000 | $2,000 | $2,000 |

| Quebec | Applicants: $862Recipients: $1,500 | Applicants: $862Recipients: $2,500 | Applicants: $1,232Recipients: $2,870 | Applicants: $1,757Recipients: $2,975 |

| Ontario | $572 | $5,000 | $1,550 | $2,130 |

| Manitoba | $4,000 | $4,000 | $8,000 | $16,000 |

| Saskatchewan | $1,500 | $1,500 | $3,000 | $4,000 |

| Alberta | $583 | $1,530 | $1,062 | $1,533 |

| Alberta – Assured Income for the Severely Handicapped (AISH) Program2 |

Not applicable | $100,000 | Not applicable | Not applicable |

| British Columbia | Applicants: $150Recipients: $1,500 | $3,000 | Applicants: $250Recipients: $2,500 | Applicants: $250Recipients: $2,500 |

| Yukon | $500 | $1,500 | $1,000 | $1,600 |

| Northwest Territories | $300 | $5,000 | $380 | $560 |

| Nunavut | $0 | $5,000 | $0 | $0 |

* Applicants are those applying for welfare; recipients are those already receiving welfare.

See Table 1 in the Appendix for more details.

|

Table 6.2: Liquid asset exemption levels for applicants |

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

|

Single employable applicants |

||||||||||

|

NL |

PE |

NS |

NB |

QC |

ON* |

MB |

SK |

AB |

BC |

|

|

1989 |

40 |

50 |

0 |

500 |

1,500 |

227 |

0 |

1,500 |

50 |

160 |

|

1994 |

40 |

50 |

0 |

500 |

1,500 |

306 |

0 |

1,500 |

50 |

2,500 |

|

1999 |

40 |

50 |

0 |

1,000 |

712 |

520 |

0 |

1,500 |

50 |

500 |

|

2004 |

500 |

50 |

0 |

1,000 |

1,500 |

520 |

0 |

1,500 |

50 |

150 |

|

2009 |

500 |

50 |

500 |

1,000 |

862 |

572 |

4,000 |

1,500 |

583 |

150 |

|

Single applicants with a disability |

||||||||||

|

NL |

PE |

NS |

NB |

QC |

ON |

MB |

SK |

AB |

BC |

|

|

1989 |

3,000 |

900 |

3,000 |

1,000 |

2,500 |

3,000 |

400 |

1,500 |

3,000 |

2,500 |

|

1994 |

3,000 |

900 |

3,000 |

1,000 |

2,500 |

3,000 |

2,000 |

1,500 |

1,500 |

3,000 |

|

1999 |

3,000 |

900 |

3,000 |

3,000 |

712 |

5,000 |

2,000 |

1,500 |

1,500 |

3,000 |

|

2004 |

3,000 |

900 |

500 |

3,000 |

2,500 |

5,000 |

2,000 |

1,500 |

1,500 |

3,000 |

|

2009 |

3,000 |

900 |

500 |

3,000 |

862 |

5,000 |

4,000 |

1,500 |

1,530 |

3,000 |

|

Lone parent applicants with one child |

||||||||||

|

NL |

PE |

NS |

NB |

QC |

ON |

MB |

SK |

AB |

BC |

|

|

1989 |

2,500 |

1,200 |

2,500 |

1,000 |

-- |

5,000 |

800 |

3,000 |

2,500 |

1,500 |

|

1994 |

5,000 |

1,200 |

2,500 |

1,000 |

-- |

5,000 |

2,000 |

3,000 |

2,500 |

5,000 |

|

1999 |

2,500 |

1,200 |

2,500 |

2,000 |

1,037 |

1,457 |

2,000 |

3,000 |

2,500 |

5,000 |

|

2004 |

1,500 |

1,200 |

1,000 |

2,000 |

2,845 |

1,457 |

2,000 |

3,000 |

2,500 |

250 |

|

2009 |

1,500 |

50 |

1,000 |

2,000 |

1,232 |

1,550 |

8,000 |

3,000 |

1,062 |

250 |

|

Couple applicants with two children |

||||||||||

|

NL |

PE |

NS |

NB |

QC |

ON* |

MB |

SK |

AB |

BC |

|

|

1989 |

100 |

50 |

0 |

1,000 |

2,500 |

2,291 |

0 |

3,000 |

250 |

1,500 |

|

1994 |

100 |

50 |

0 |

1,000 |

2,500 |

3,188 |

0 |

3,000 |

250 |

5,000 |

|

1999 |

100 |

50 |

0 |

2,000 |

1,478 |

2,030 |

0 |

3,000 |

250 |

5,000 |

|

2004 |

1,500 |

50 |

0 |

2,000 |

2,943 |

2,030 |

0 |

4,000 |

250 |

250 |

|

2009 |

1,500 |

50 |

1,000 |

2,000 |

1,757 |

2,130 |

16,000 |

4,000 |

1,533 |

250 |

*amounts for 1989 and 1994 estimated by the National Council of Welfare

-- not available

LIQUID ASSET EXEMPTION LEVELS ADJUSTED FOR INFLATION

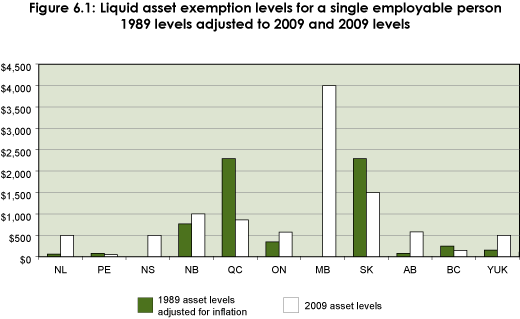

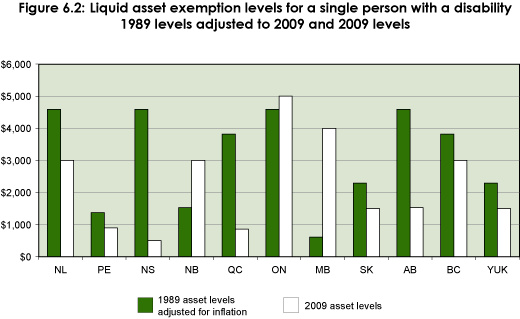

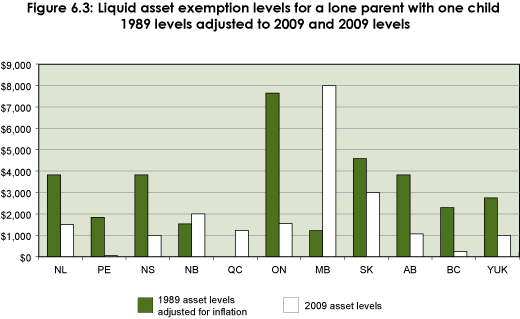

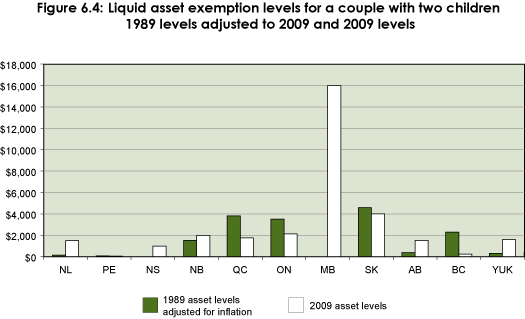

Between 1989 and 2009, inflation increased by 52.9 percent. We calculated how much the 1989 provincial liquid asset exemption levels for applicants would have been in 2009 had they been regularly increased in line with the cost of living. Figures 6.1 to 6.4 show the 1989 levels adjusted for inflation compared to the actual 2009 asset exemption levels for our four household types.

In many provinces, the 1989 asset exemption levels adjusted for inflation exceed the 2009 levels. This is most prevalent for the single person with a disability and the lone parent with one child. This means that it has become harder to qualify for welfare over time. Even though the cost of living has increased substantially, the liquid asset exemption levels have not kept pace. Manitoba’s flat rate exemption of $4,000 per person as of 2009 is a marked contrast to the other provinces.3

What is particularly striking is the high degree of variability across the country, as well as over the 20-year time frame. It is difficult to see the logic in jurisdictions’ approach to liquid asset exemption policies.

For a single employable applicant, most of the 1989 asset exemption levels were so low that even when adjusted for inflation they were still extremely low. In seven out of 10 provinces they fall below $500. In Quebec and Saskatchewan, the indexed amounts were considerably more than the levels in effect in January 2009.

For the single applicant with a disability, the 2009 liquid asset exemption levels have not kept up with inflation. The losses range from just under $500 in Prince Edward Island to nearly $4,100 in Nova Scotia. Only New Brunswick, Ontario and Manitoba had higher levels in January 2009 than the 1989 indexed ones.

For the lone parent with one child, there have been substantial decreases in the liquid asset levels in seven provinces. These range from just under $1,600 in Saskatchewan to nearly $6,100 in Ontario. We were not able to compare Quebec’s levels since data for 1989 were not available.

The 1989 liquid asset levels for a couple with two children were so low that even when indexed to inflation, the levels in five provinces were still below $500. There were decreases of nearly $1,400 in Ontario and more than $2,000 in both Quebec and British Columbia. Manitoba’s 2009 level was $16,000, a striking contrast to the other provinces.

It has become harder to qualify for welfare over time. Even though the cost of living has increased substantially, the liquid asset exemption levels have not kept pace, and in some cases they have decreased.

THE CURRENT REALITY

Welfare programs have traditionally had low liquid asset exemption levels. Because welfare was designed to be a program of last resort, applicants have had to exhaust their sources of income, including savings, before they could qualify for welfare. The recent move towards exempting certain types of assets – Registered Education Savings Plans and Registered Disability Savings Plans – gives those on welfare with children or a family member with a disability the assurance that these funds will be protected. But for many, by the time they are eligible for welfare, they are nearly destitute. This has come to be known as ‘asset stripping’.

With the current recession, asset stripping is a growing problem for people who never expected to have to turn to welfare. Many people who have lost their jobs are not eligible for Employment Insurance (EI) benefits in the first place. Others are exhausting their EI benefits and are still unable to find work. Still others are only able to find part-time work, which often isn’t enough to make ends meet. Some have to turn to welfare for support while they try to get back on their feet.

These are people who have worked most of their lives and accumulated savings, often in the form of registered retirement savings. Now they have to liquidate and use up these assets before they can qualify for welfare. Not only do current policies ensure these people are destitute before they can qualify for welfare, they also rob them of their retirement savings, potentially leading to greater reliance on government supports in their senior years.

Recent Canadian studies4,5 have focused on asset retention initiatives as a way to overcome poverty. Encouraging people to save, even modest amounts, provides them with opportunities for a better future and allows them to better manage life transitions. Allowing people to retain modest assets helps them pay costs associated with the search for employment, investing in their education or skills development, or providing a cushion against unforeseen circumstances. However, this is not possible for people on welfare subject to asset stripping.

Once on welfare, it is harder for people with few assets to get off. Often, they are doomed to a cycle of persistent poverty and dependency.

The National Council of Welfare feels that low liquid asset exemption policies are counter productive. Allowing applicants to retain modest assets provides them with the resources to make the transition back towards greater self-sufficiency.

We urge provinces and territories to increase their liquid asset exemption levels. Manitoba has taken the lead by exempting $4,000 per person. We ask other provinces to follow their lead. We further propose that all provinces and territories increase their asset exemption levels each year by the cost of living.

“…welfare policy is caught in a trap of its own making that strips applicants of the same productive assets they will need to leave and stay off welfare later on”.

Wealth, Low-Wage Work and Welfare: The Unintended Costs of Provincial Needs-tests, 2008

(Social and Enterprise Development Innovations)

| Table 6.3: 1989 Liquid asset exemption levels adjusted for inflation compared to actual 2009 levels | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Single employable applicants | ||||||||||

| NL | PE | NS | NB | QC | ON* | MB | SK | AB | BC | |

| 1989 adjusted for inflation | $61 | $76 | $0 | $765 | $2,294 | $347 | $0 | $2,294 | $76 | $245 |

| 2009 actual | $500 | $50 | $500 | $1,000 | $862 | $572 | $4,000 | $1,500 | $583 | $150 |

| Single applicants with a disability | ||||||||||

| NL | PE | NS | NB | QC | ON | MB | SK | AB | BC | |

| 1989 adjusted for inflation | $4,587 | $1,376 | $4,587 | $1,529 | $3,823 | $4,587 | $612 | $2,294 | $4,587 | $3,823 |

| 2009 actual | $3,000 | $900 | $500 | $3,000 | $862 | $5,000 | $4,000 | $1,500 | $1,530 | $3,000 |

| Lone parent applicants with one child | ||||||||||

| NL | PE | NS | NB | QC | ON | MB | SK | AB | BC | |

| 1989 adjusted for inflation | $3,823 | $1,835 | $3,823 | $1,529 | $0 | $7,645 | $1,223 | $4,587 | $3,823 | $2,294 |

| 2009 actual | $1,500 | $50 | $1,000 | $2,000 | $1,232 | $1,550 | $8,000 | $3,000 | $1,062 | $250 |

| Couple applicants with two children | ||||||||||

| NL | PE | NS | NB | QC | ON* | MB | SK | AB | BC | |

| 1989 adjusted for inflation | $153 | $76 | $0 | $1,529 | $3,823 | $3,503 | $0 | $4,587 | $382 | $2,294 |

| 2009 actual | $1,500 | $50 | $1,000 | $2,000 | $1,757 | $2,130 | $16,000 | $4,000 | $1,533 | $250 |

*amounts for 1989 estimated by the National Council of Welfare

Mary and Shannon’s story revisited with a liquid asset exemption of $10,000.

Mary, the 43-year old lone parent and her daughter Shannon, who were described at the beginning of this chapter now have more flexibility. Recall that Mary had $8,000 in RRSPs when she lost her job and claimed Employment Insurance benefits.

This time when Mary’s EI ran out and she applied for welfare, she qualified right away because her total assets, including her RRSP, were below $10,000. Mary’s welfare entitlement was $913 a month, and with Shannon’s federal and provincial child benefits, they had nearly $1,300 to live on. It wasn’t much, but they could get by for awhile.

A couple of months later, Mary found a part-time job working 12 hours a week at minimum wage. This was an extra $500 a month for her! When she told the welfare office they said they would be reducing her monthly cheque by half of what she earned. She was disappointed, but financially she was still ahead. Now she had nearly $1,550 to live on each month. When she files her income taxes, she’ll get refundable tax credits, including some federal Working Income Tax Benefit, and none of these will affect her welfare cheque.

Mary doesn’t like living on welfare, but she still has her home and her RRSP, is keeping her attachment to the labour force, which will help her get more work when the economy picks up, and she can pay her bills and put food on the table.

1 In Newfoundland and Labrador, RRSPs with a value of less than $10,000 are exempt for the first 90 days. In Quebec, $60,000 from all eligible sources, including RRSPs, is exempt. In Alberta, $5,000 per adult is exempt.

2 In addition to its Income Support Program, Alberta also has a distinct program for persons with severe and permanent disabilities: the Assured Income for the Severely Handicapped (AISH) program. The AISH program differs from the other social assistance programs referenced in this report in that clients are provided with a flat rate living allowance benefit which is not contingent on family size. All other programs in this report are needs tested – including Alberta’s Income Support Program - with benefits based on family size and other factors. The $100,000 asset exemption level reflects the total value of all non-exempt assets owned by an applicant or recipient and their cohabiting partner.

3 To a family maximum of $16,000.

4 Wealth, Low-Wage Work and Welfare: The Unintended Costs of Provincial Needs-tests, Jennifer Robson, SEDI, April 2008. See http://www.sedi.org/DataRegV2-unified/sedi-Publications/Final%20welfare% 20paper.pdf

5 Why don’t we want the poor to own anything? John Stapleton for the Metcalfe Foundation, 2009. See http://www.metcalffoundation.com/downloads/Why_don't_we_want_the_poor_to_own_anything.p df