Chapter 7

WELFARE AND EARNINGS

Each province and territory decides how to treat income from other sources – for example, pensions, earnings or Employment Insurance benefits - when calculating a household's welfare benefit. Some income is fully exempt (e.g., most tax credits) and welfare is not reduced. Other income may be partially exempt or not exempt at all. In these cases, the income – or a portion of it – is deducted from the welfare cheque.

In this chapter, we focus on how provinces and territories treat the earnings of welfare recipients. We look at how much they can earn before their welfare benefit is reduced. We then look at how welfare households with earnings benefit from the federal Working Income Tax Benefit (WITB).

EARNINGS EXEMPTIONS

Most provinces and territories allow welfare recipients to earn a certain amount – either a flat rate amount, a percentage of earnings, or a combination of the two - before their welfare benefits are reduced. These are known as earnings exemption provisions.

All provinces and territories require welfare recipients to seek and accept employment, where they are able to do so. However, those who are able to find paid work have their earnings treated quite differently, depending on where they live. In some cases, the obligation to work is paramount and there are limited, if any, earnings exemptions. In other cases, earnings exemptions are seen as a way to encourage welfare recipients to pursue employment, while enabling them to be better off financially. In these cases, the earnings exemption provisions tend to be more generous.

2009 EARNINGS EXEMPTION PROVISIONS

Table 7.1 shows the earnings exemption provisions in each province and territory as of January 2009 for the NCW's four types of households.

The provisions vary widely across the country. Some jurisdictions have different policies for people applying for welfare compared to those already receiving benefits.

- Five provinces – Nova Scotia, New Brunswick, Ontario1, Saskatchewan2 and British Columbia – reduce an applicant's welfare benefit by the full amount of earnings. This means that applicants with any earned income have their welfare reduced dollar for dollar when they first go on assistance.

- Manitoba and the Yukon have lower earnings exemption levels for people applying for welfare than for those already receiving welfare.

| Table 7.1: Monthly earnings exemption levels as of January 2009 Provisions for applicants and recipients* |

||||

|---|---|---|---|---|

| Single Person Considered Employable | Single Person with a Disability | Lone Parent, One Child | Couple, Two Children |

|

| NEWFOUNDLAND AND LABRADOR | 100% of income up to $75 plus 20% of income over $75 | 100% of income up to $150, plus 20% of income over $150 | 100% of income up to $150, plus 20% of income over $150 | 100% of income up to $150, plus 20% of income over $150 |

| PRINCE EDWARD ISLAND | $75 of net earned income plus 10% of the balance | $75 of net earned income plus 10% of the balance | $125 of net earned income plus 10% of the balance | $125 of net earned income plus 10% of the balance |

| NOVA SCOTIA3 | Applicants: no exemption Recipients: 30% of net wages | Applicants: no exemption Recipients: $150 from supported employment plus 30% of net wages remaining | Applicants: no exemption Recipients: 30% of net wages | Applicants: no exemption Recipients: 30% of net family wages |

| NEW BRUNSWICK | Applicants: no exemption Recipients: $300 | Applicants: no exemption Recipients: $250 | Applicants: no exemption Recipients: $200 | Applicants: no exemption Recipients: $200 |

| QUEBEC | $200 | $100 | $200 | $300 |

| ONTARIO | Applicants: no exemption for first 3 months on assistance Recipients: 50% of net earnings after 3 months of continuous assistance | 50% of net earnings in addition to a monthly $100 Work-Related Benefit for each eligible adult family member who is employed | Applicants: no exemption for the first 3 months on assistance Recipients: 50% of net earnings after 3 months of continuous assistance | Applicants: no exemption for the first 3 months on assistance Recipients: 50% of net earnings after 3 months of continuous assistance |

| MANITOBA | Applicants: $200 of net earnings Recipients: after one month, $200 of net earnings plus 30% of net earnings over $200 | Applicants: $200 of net earnings Recipients: after one month, $200 of net earnings plus 30% of net earnings over $200 | Applicants: $200 of net earnings Recipients: after one month, $200 of net earnings plus 30% of net earnings over $200 | Applicants: $200 of net earnings for each earner Recipients: after one month, $200 of net earnings plus 30% net earnings over $200, for each earner |

| SASKATCHEWAN4 | No earnings exemption (TEA clients) | $100 plus 25% of the next $500 for a maximum of $225 (Saskatchewan Assistance Plan [SAP] clients) | No earnings exemption (TEA clients). Clients with earnings over $125 are eligible for the Saskatchewan Employment Supplement | No earnings exemption (TEA clients). Clients with earnings over $125 are eligible for the Saskatchewan Employment Supplement |

| ALBERTA | $230 of net income plus 25% of the remaining net income | $230 of net income plus 25% of the remaining net income | $230 of net income plus 25% of the remaining net income | $115 of net income plus 25% of remaining net income for each adult |

| ALBERTA – Assured Income for the Severely Handicapped (AISH) program5 | Not applicable | $400 of net income plus 50% above $400 up to $1,500 for a maximum of $950 | Not applicable | Not applicable |

| BRITISH COLUMBIA | No earnings exemption | Applicants: no exemption for first 3 months Recipients: $500 | No earnings exemption | No earnings exemption |

| YUKON | Applicants: $100 Recipients: 50% of gross income for first 36 months; 25% afterwards | Applicants: $100 Recipients: 50% of gross income for first 36 months; 25% afterwards | Applicants: $150 Recipients: 50% of gross income for first 36 months; 25% afterwards | Applicants: $150 Recipients: 50% of gross income for first 36 months; 25% afterwards |

| NORTHWEST TERRITORIES | $200 plus 15% of remaining earned income | $200 plus 15% of remaining earned income | $400 plus 15% of remaining earned income | $400 plus 15% of remaining earned income |

| NUNAVUT | $200 | $200 | $400 | $400 |

See Table 3 in the Appendix for more detail.

*Applicants are those applying for welfare; recipients are those already receiving welfare.

In Newfoundland and Labrador, Prince Edward Island, Quebec, Alberta, the Northwest Territories and Nunavut, earnings exemption provisions are the same for applicants and recipients.

In Saskatchewan and British Columbia, there are no earnings exemption provisions other than for people with disabilities. Households on welfare have their welfare reduced by the full amount of any earned income for as long as they remain on assistance.6

In Ontario, once recipients have been on assistance for three months, 50% of their net earnings are exempt.

It is difficult to fully understand what these provisions mean for welfare clients with earnings. Even though the recipient still has all of his or her earned income, the welfare benefit is usually reduced. The following scenario helps put it into perspective.

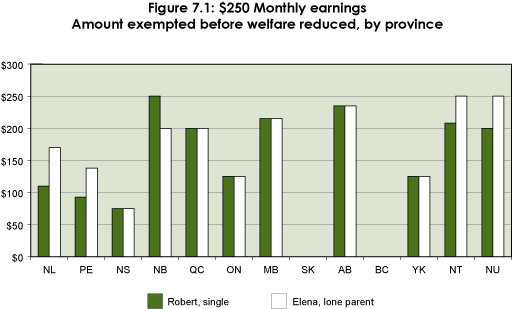

Elena, a lone parent with a 12-year old daughter, and Robert, a single 40-year old man, have both been on welfare for six months. They each have a part-time job that brings in $250 a month. The following chart shows, by province and territory, how much of that money is exempted before their welfare cheque is reduced.

The chart illustrates the impact of the different earnings exemption approaches adopted across Canada. In Saskatchewan and British Columbia, there is no financial incentive for Elena and Robert to be employed. They would not see any increase in their overall income because their welfare cheques would be reduced by the full amount of their earnings. Bear in mind, as well, that additional costs for items such as transportation or clothing have to be paid by clients to get to work.

On the other hand, in New Brunswick, Quebec, Manitoba, Alberta, the Northwest Territories and, Nunavut, Elena and Robert would see their monthly income increase by $200 or more. Not only would they see a boost in their overall monthly income, they would also gain valuable work experience.

The National Council of Welfare views earnings exemptions as an important bridge from welfare to paid employment. Not only do they allow welfare recipients to increase their overall income and ability to meet their needs, they also enable them to gain experience which can help them move from welfare to the labour market on a permanent basis.

THE WORKING INCOME TAX BENEFIT (WITB)

In 2007, the federal government introduced the Working Income Tax Benefit. It is a refundable tax credit with a dual purpose: to provide a financial support to low-income workers to stay in the work force, and to help reduce the disincentives7 that welfare recipients face when they leave welfare for work. The WITB helps those with low earnings by supplementing their wages.8 For those on welfare who qualify, the WITB further increases their income because it is fully exempt: welfare benefits are not reduced.

From the outset, the federal government invited provinces and territories to modify the WITB design to harmonize best with their income security programs. Quebec, British Columbia and Nunavut have had their own WITB model since 2007. Alberta developed its own model in 2009.9

The WITB provides income benefits that vary according to earnings and total net family income. In 2008, maximum annual benefits under the federal model were $510 for a single person and $1,019 for a family. To be eligible, earnings had to exceed $3,000. Maximum benefits were paid to a single person with earnings between $5,500 and $9,681 and to a family with earnings between $8,095 and $14,776. Benefits ceased once a single person's net income exceeded $13,081 and a family's net income exceeded $21,569. In 2009 the WITB was enhanced. The maximum annual benefit increased to $925 for a single person and $1,680 for a family. The upper income thresholds were also increased, making it available to more low-income earners. In order to receive the WITB, people must apply when they file their income taxes.

WELFARE AND THE WITB

In this section we look at the interaction between welfare, earnings and the Working Income Tax Benefit. The WITB is intended to help break down the welfare wall by providing additional financial support to offset the loss of income support benefits and the additional costs of taking on a job.

Welfare recipients face considerable challenges in their transition from welfare to employment. When they leave welfare they lose in-kind benefits such as dental, vision and drug coverage. Once employed, they face additional costs for transportation, clothing, as well as income taxes and payroll taxes. Those with young children may face high child care costs. Often, they find themselves financially worse off employed than they were on welfare.

In general, as earnings increase, welfare benefits decrease. All provinces and territories deduct a certain amount of a recipient's earnings from the welfare cheque. However, once earnings are combined with the welfare benefit, overall income usually increases. Welfare recipients who are eligible for the WITB see their income increase even more, because the WITB is considered exempt income.

Welfare recipients with earnings over $3,00010 a year are eligible for the WITB. However, because the WITB is based on a combination of earnings and total net income, welfare recipients do not all benefit in the same way. Some welfare incomes, particularly when combined with earnings, are much higher than others. As a result, in some provinces, the WITB is reduced while the recipient is still on welfare.

Table 7.2 looks at a hypothetical situation of a single welfare recipient with four different earnings levels in each of the provinces.11 We look at the total income of a single recipient with no earnings, earnings of $462.50 a month (the point at which maximum WITB benefits are paid using the federal model), $600 a month, and $800 a month. We show the combined amount of welfare and earnings, the WITB that would be paid at each of these earnings levels and the total overall monthly income. We have used the 2008 WITB levels since this is the benefit that would have been paid to welfare recipients during 2009.12

The table highlights the fact that the structure of each province's welfare program – both its rates and earnings exemption policies – determines the amount of WITB that is paid.

| Table 7.2: ESTIMATED TOTAL MONTHLY INCOME FOR A SINGLE EMPLOYABLE PERSONWELFARE. EARNINGS AND THE WITB* 2009 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| TOTAL MONTHLY EARNINGS | ||||||||||

| $462.50 | $600 | $800 | ||||||||

| Maximum welfare. no earnings* | Welfare plus earnings | WITB | Total income | Welfare plus earnings | WITB | Total income | Welfare plus earnings | WITB | Total income | |

| NL | $774 | $927 | $26.30 | $953 | $954 | $22.18 | $976 | $994 | $16.18 | $1.010 |

| PE | $555 | $669 | $42.50 | $712 | $683 | $42.50 | $726 | $800 | $42.50 | $843 |

| NS | $510 | $649 | $42.50 | $691 | $690 | $42.50 | $732 | $800 | $42.50 | $843 |

| NB | $294 | $594 | $42.50 | $637 | $600 | $42.50 | $643 | $800 | $42.50 | $843 |

| QC | $589 | $789 | $31.50 | $820 | $789 | $48.00 | $837 | $800 | $72.00 | $872 |

| ON | $573 | $804 | $42.50 | $847 | $873 | $34.36 | $907 | $973 | $19.36 | $992 |

| MB | $548 | $827 | $42.50 | $869 | $868 | $38.19 | $906 | $928 | $29.19 | $957 |

| SK | $693 | $693 | $42.50 | $736 | $693 | $42.50 | $736 | $800 | $42.50 | $843 |

| AB | $583 | $871 | $42.50 | $914 | $906 | $42.50 | $949 | $956 | $42.50 | $999 |

| BC | $613 | $613 | $11.33 | $624 | $613 | $34.71 | $648 | $800 | $68.33 | $868 |

*Maximum average monthly welfare benefit for 2009.

Some jurisdictions provide additional financial benefits to welfare recipients with earnings. These are not included in this table.

Quebec and British Columbia figures based on their respective 2008 WITB models.

Dark green shaded cells mean that the client is no longer eligible for welfare due to excess income.

A number of patterns stand out for 2009:

- In four provinces – Newfoundland and Labrador, Ontario, Manitoba, and Alberta – single recipients continue to receive some welfare benefits with earnings of $800/month. In the six other provinces, they were no longer eligible for welfare and consequently their total incomes with WITB were lower.

- The two provinces with their own WITB models – Quebec and British Columbia - paid maximum benefits at higher income levels than under the federal model. In both cases, a single recipient with earnings became ineligible for welfare before reaching the maximum WITB level.

- In Newfoundland and Labrador, the single person could not receive the maximum WITB while on welfare, because welfare benefits were relatively high.

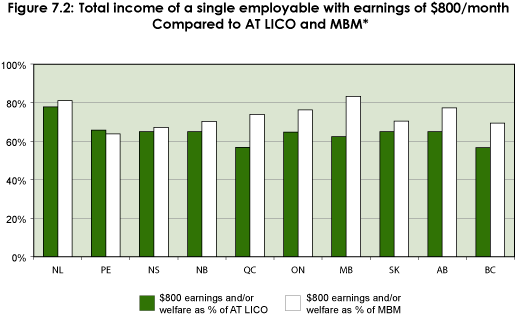

In Figure 7.2, we compare the total income of those singles earning $800/month, whether they were still eligible for welfare or not, with the after tax LICO and the MBM. In all provinces, the amounts were still well below both low-income measures.

*Estimated

IS THE WITB ACHIEVING ITS GOALS?

The 2009 increases to the WITB will certainly put more money in the hands of the Canadian women and men who are employed and still living in poverty. This includes those on welfare who have enough employment earnings to qualify for the WITB.

Whether the WITB is in fact encouraging welfare recipients to pursue additional employment, we don't know. We do know that only a small percentage of welfare households (estimated to be about 10%) report earnings. Information on how much they earn or if they even qualify for the WITB is not readily available.

The National Council of Welfare would like to see the federal government undertake an evaluation of the extent to which the WITB is achieving its objectives, in particular in helping social assistance recipients scale the welfare wall. We also propose that the government streamline the WITB application process, to make it as easy as possible for eligible recipients to receive the WITB.

In our view, the current WITB amounts still need to be raised to help welfare recipients, particularly singles, avoid or overcome the welfare wall.

Income supports outside of welfare are a key to leaving welfare. Equally important are transitional assistance measures, such as drug and dental coverage and assistance with employment-related expenses. Scaling the welfare wall needs a comprehensive approach to both income support and the provision of appropriate services. We are encouraged by poverty reduction strategies that are taking this approach and are confident these kinds of investments will pay off for all Canadians.

1 Ontario Works only.

2 Transitional Employment Allowance only.

3 Families can earn up to $3,000 per year.

4 Employable clients can be on either Saskatchewan Assistance Plan (SAP) or Transitional Employment Allowance (TEA), depending on assessment. Employable singles, lone parents or couples with children are eligible for earnings exemptions if they are on SAP.

5 Alberta's distinct program for persons with severe and permanent disabilities: the Assured Income for the Severely Handicapped (AISH) program differs from the other social assistance programs referenced in this report in that clients are provided with a flat rate living allowance benefit. All other programs in this report are needs tested – with benefits based on family size and other factors. See text box in Chapter 3.

6 Does not apply to disabled persons receiving Saskatchewan Assistance Plan benefits or BC Disability Assistance.

7 Disincentives include the loss of medical and dental benefits, employment-related costs such as transportation and clothing, and higher taxes. This is often referred to as the "welfare wall".

8 A Disability Supplement is also available to those eligible for the Disability Tax Credit with annual earnings over $1,150.

9 For detailed information on the WITB, including provincial/territorial variations, see http://www.cra-arc.gc.ca/bnfts/wtb/menu-eng.html

10 Based on federal model.

11 Data on the territories are excluded because clients are not eligible for the WITB due to high welfare benefit levels.

12 In most cases, the WITB is based on the previous year's income as declared on the federal income tax form.