Prepared for the Canadian Radio-television and Telecommunications Commission

POR 068-17

Contract # 82082-180158/001/CY

Produced by Kantar TNS

Contract Award Date: December 22, 2017

Report Date: March 1, 2018

Ce rapport est aussi disponible en français.

communications@crtc.gc.ca

The Wireless Code, which was established in 2013 by the CRTC, is a mandatory code of conduct for wireless service providers and applies to all retail mobile wireless voice and data services provided to individual and small business consumers in Canada. The Wireless Code applied to all wireless contracts as of June 3, 2015.

The CRTC committed to evaluating the effectiveness of the Wireless Code and recently completed a review to assess whether the Wireless Code meets and continues to meet its objectives, which includes ensuring that consumers are empowered to make informed decisions about wireless services. On June 15, 2017, the CRTC announced multiple changes to the Wireless Code, which came into effect on December 1, 2017.

The information collected in the 2018 Wireless Code public opinion research (POR) will help the CRTC assess whether Canadians are satisfied with the changes and whether further changes are required to ensure the objectives of the Wireless Code continue to be met. Additionally, the 2018 Wireless Code POR continues to monitor trends related to the perceptions of the CRTC and has added a number of questions related to Canadians’ understanding and satisfaction with the new Television Service Provider (TVSP) Code, which came into effect on September 1, 2017.

The methodology was designed to ensure consistency with previous iterations of Wireless Code PORs conducted in the Fall and Spring of 2016.

This POR was designed to address the following objectives:

Wireless Data Usage

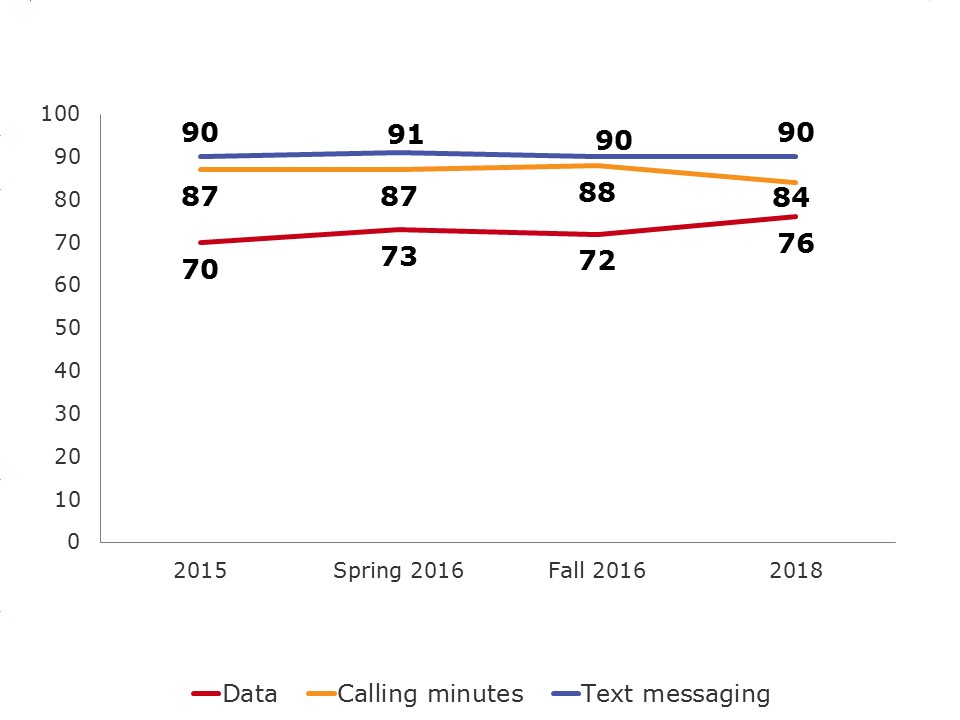

The composition of wireless plans has remained stable when compared to the Fall 2016 results. More specifically, wireless plans that include data continue to be common in Canada (76%). The majority of wireless plans have limited data (85%), which results in most Canadians (94% compared to 91% in Fall 2016) attempting to manage their data so as not to incur additional costs.

Canadians report finding it easy to manage their data (77%) and use tools to track their usage (59%). Despite this, a considerable portion (49%) of wireless owners report having paid data overages in the last 12 months, suggesting that data management may in fact be harder than anticipated for many Canadians.

Bill shock and Roaming fees

Almost a quarter of Canadians (24%) continue to experience bill shock suggesting that there continues to be room for improvement in this area moving forward. This is a slight, although not statistically significant increase, from Fall 2016 (21%). Some Canadians continue to struggle to track how much data they use, to understand the cost of international roaming and to understand the cost of long distance calling.

Younger Canadians (18-54) continue to be more likely to experience bill shock compared to those who are 55 years of age or older (21-63% vs. 15%), as are those with tab contracts (29% vs. 21%), and not unexpectedly, those who find data management difficult (62% vs. 19%).

The amount of unexpected charges varies greatly – from less than $50 to over $1 000 in one billing cycle. Most of the unexpected charges continue to be $100 or less (61%).

Almost one in every five Canadians (17%) finds it quite difficult to manage roaming fees while travelling. Men find managing roaming fees easier to manage than women (56% vs. 48%), as well as those with a higher income (68% vs. 39-53%).

Understanding of Contracts

A majority of Canadians (61%) find their contracts clear and easy to understand. This is truer for those aged 18-34 when compared to older Canadians (74% vs. 55-56%). Unlimited data contracts seem to be easier to understand (70% vs. 42%) for many Canadians and those who find data management easy also find their contracts easier to understand (70% vs. 42%).

The newly instated trial period explanation is somewhat unclear to many Canadians. It was found clear and easy to understand by only one in three Canadians (36%). There is also some indication that the trial period may be more confusing for those with a higher education. Those with higher education levels are more likely to find the explanation unclear or difficult to understand compared to those with lower education levels (44% vs. 31%). A more thorough investigation into this would be required.

Some Canadians are also having some challenges related to the explanation of cancellation fees. One in four Canadians find the explanation unclear. Interestingly, the data also shows that Canadians with higher educations are more likely to find the cancellation fee explanation unclear (32% vs. 18%) which raises a red flag as to how well this clause is really understood.

Changes

When it comes to changes to contracts, a small number of wireless owners report changes being made to their contracts without prior notification (12%).

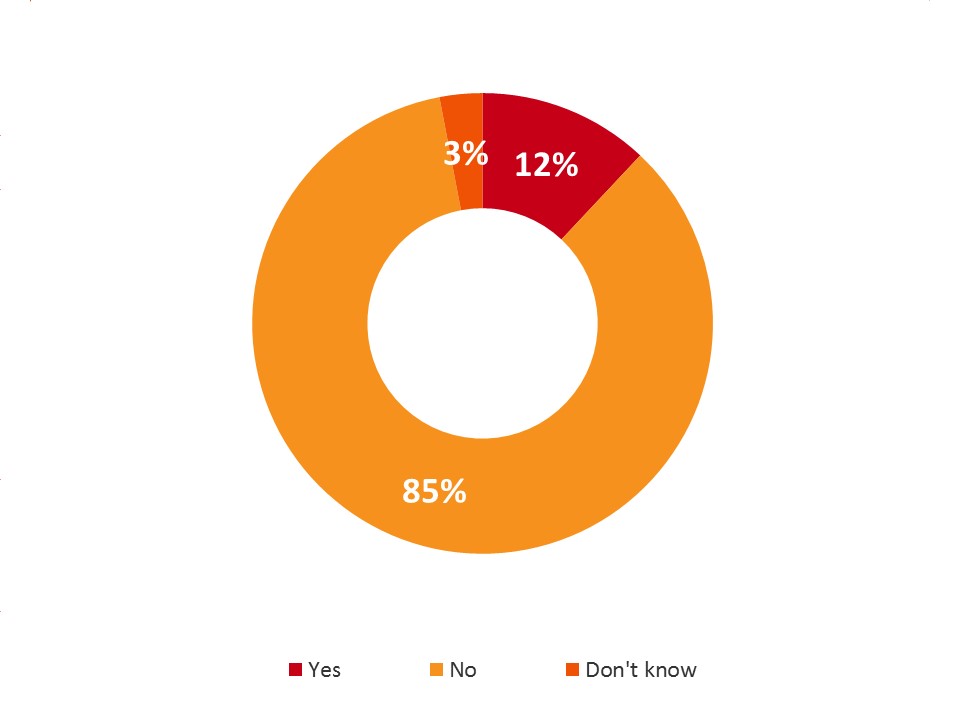

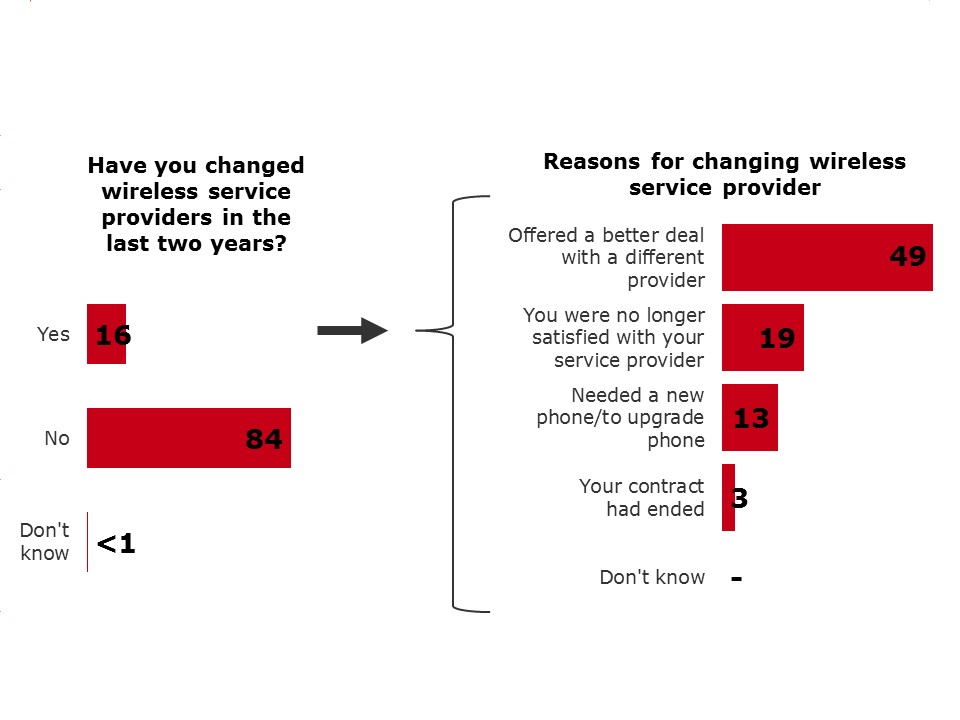

A small number of Canadians (16%) have switched service providers in the last two years with the main reason being a better deal (49%).

Complaints

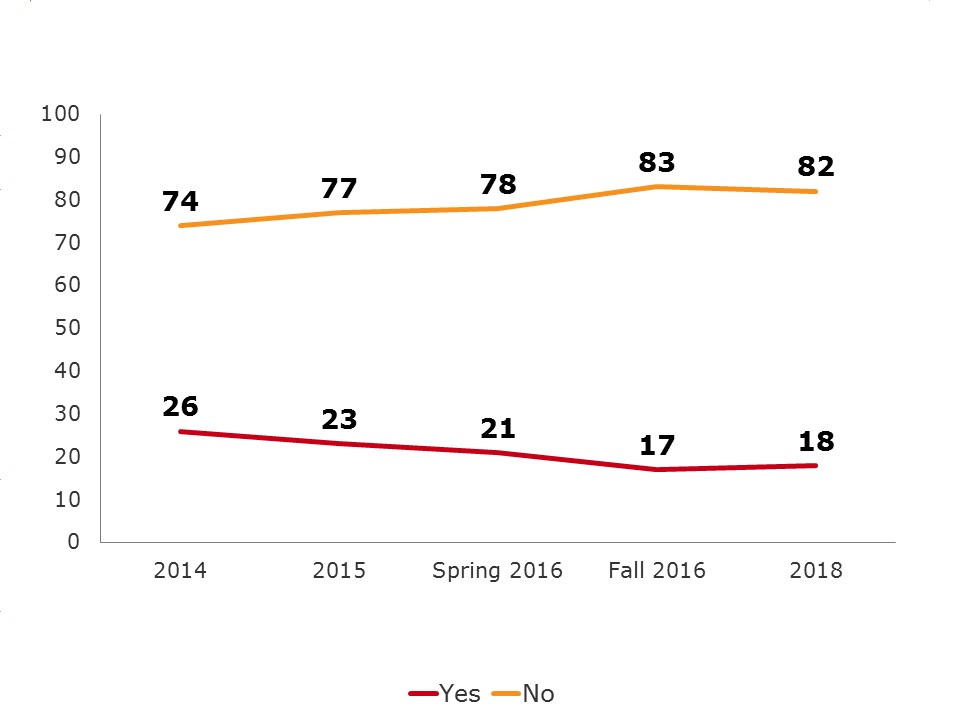

Canadians are making fewer complaints than in the past suggesting the Wireless Code is having a positive impact for wireless consumers. Eighteen per cent of Canadians have made a complaint in the last year resulting in a decrease of eight per cent since 2014. The reasons for complaints are changing with only one of the previous four main reasons now being mentioned (compared to Fall 2016) – previous main reasons for complaints comparing Fall 2016 with 2018 results, were incorrect charges on their bill (45% vs. 17%), inadequate quality of service (25% vs. 16%) and misleading information about the terms of contract (23% vs. 12%). In 2018 data charges seem to be the biggest thorn in consumers’ sides (29%), which was the fourth highest reason for complaining in Fall 2016 (32%). Consumers continue to primarily complain to their service providers (97%) with 5% of these complaints also going to the Commissioner for Complaints for Telecommunications Services (Canada) (CCTS). The CCTS responds to complaints from consumers if the consumer believes the complaint remains unresolved by the service provider.

Demographic Differences

A number of additional demographic analyses were also undertaken including age, gender, education, income and language. The most significant differences were related to age and education.

Age:

Canadians aged 18-54 are substantially different than their older counterparts (55+) in a number of ways:

Education:

Canadians with a higher level of education (university degree or higher) have slightly different outcomes compared to those with lower levels of education. More specifically:

Television Service Provider Code

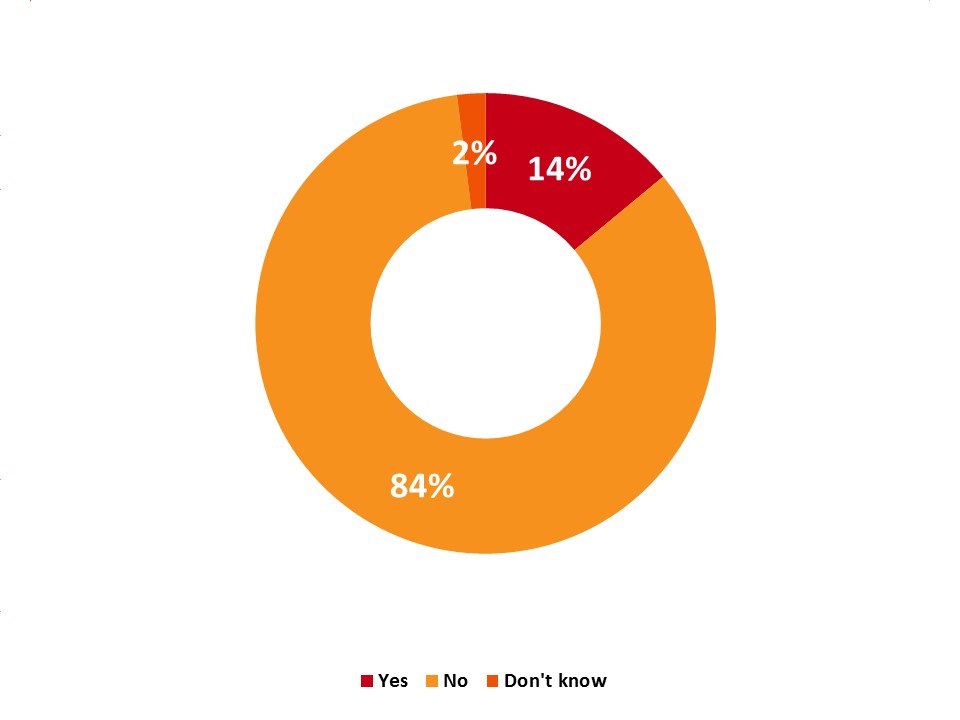

Due to the relatively recent introduction of the Television Service Provider (TVSP) Code, it is not surprising that only half of Canadians have heard of the TVSP Code (56%). It is however, surprising that only half of TV subscribers (54%) believe they have been informed of their entry-level service offering, especially given the requirement that all customers should have been informed.

At an overall level many Canadians find their TV contracts clear and easy to understand (57%) and only 14% have experienced difficulties related to TV service calls. TV subscribers are usually informed of price changes (76%) and only one in four consumers have made a complaint about their TV service in the last 12 months.

CRTC

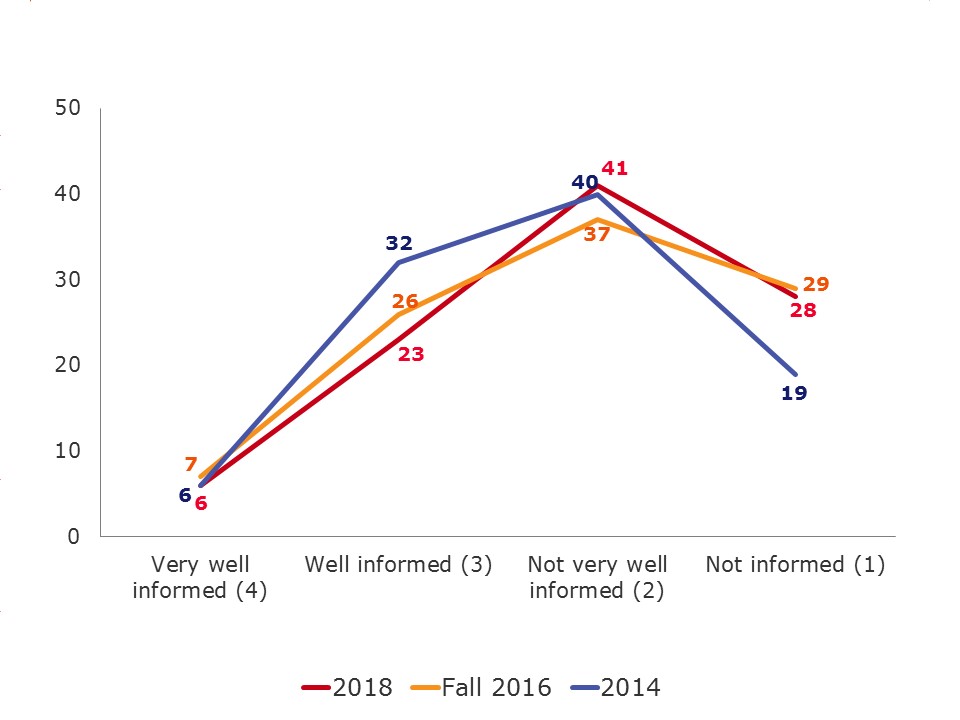

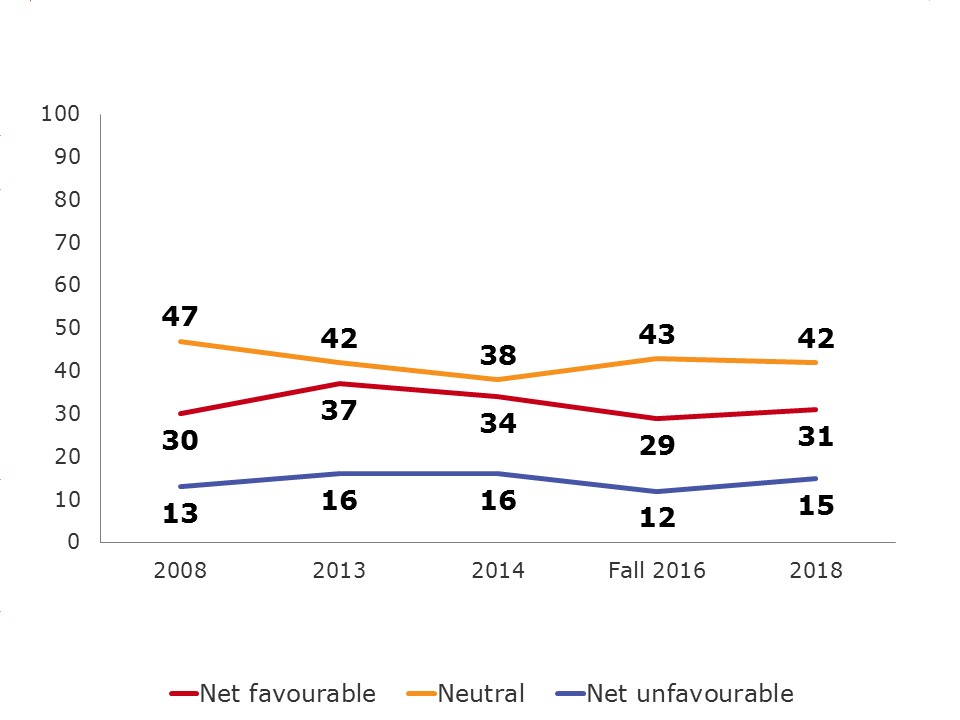

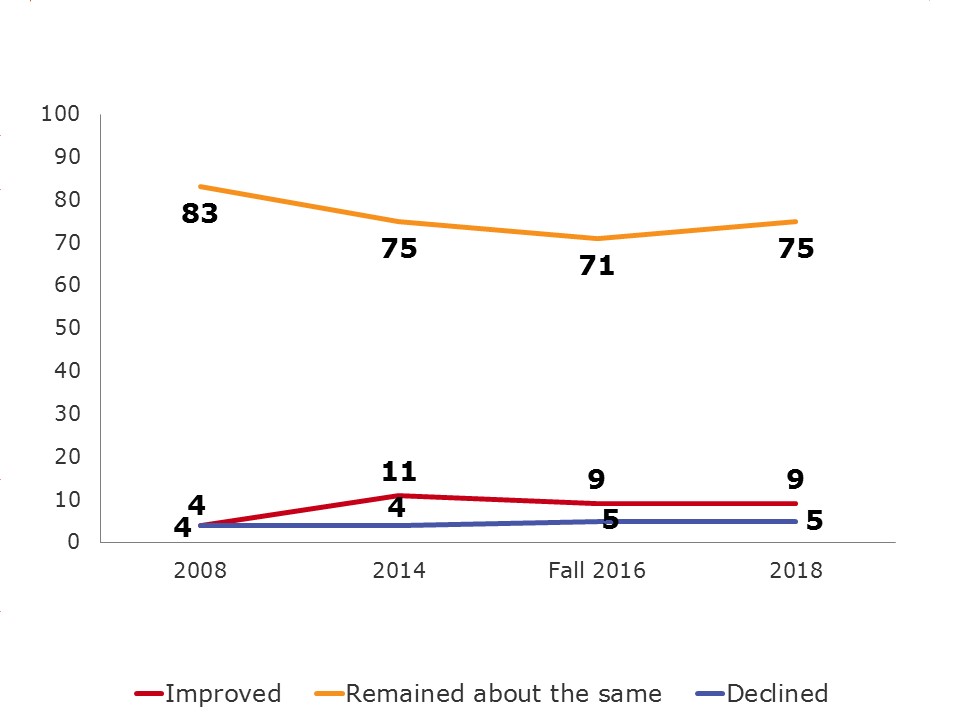

Over the past five years, Canadians’ understanding of the mandate and role of the CRTC has declined. In 2014, 38 per cent of Canadians considered themselves informed about the mandate and role of the CRTC while in 2018, only 29 per cent consider themselves informed.

Overall Canadians’ impressions of the CRTC continue to be more neutral in 2018 than they were in 2014. However, it is necessary to take into consideration that only one in three Canadians report being well informed of the CRTC’s role which implies that two in three consumers’ impressions of the CRTC are based on very little to no knowledge. In fact, when looking at the opinions of those who consider themselves very well or well informed about the CRTC’s role, 50-55% are positive about the CRTC. This implies that there is still work to be done to not only inform the public of the CRTC and its role, but also to address public perceptions.

Strategic implications

The results of this research provide evidence that suggests the Wireless Code continues to have positive impacts on Canadians[1]. It also provides information to be considered for future updates of the Wireless Code and/or the Television Service Provider Code.

The methodology was designed to ensure consistency with previous waves of Wireless Code surveys conducted by TNS in the Fall and Spring of 2016. A telephone survey was conducted among 1,345 Canadians age 18 years and older; 1,152 with those who have their own wireless plan and 193 with those who do not have a wireless plan. The sample was split into two distinct segments: Canadians who currently have a personal wireless plan covering services such as voice, text and data and Canadians who do not currently have a personal wireless plan. Interviews were conducted using random landline telephone sampling sources. Only landline phones were targeted for this survey as results from previous research indicate there are no discernible differences of opinions based on landline versus cell phone respondents.

Included within the sample are 1,034 Canadians that are under contract with TV service providers.

A pre-test consisting of 10 completed English interviews and 10 completed French interviews was completed before fielding the survey on January 25th, 2018. The survey was in field from January 26th to February 8th, 2018. The sample for this study was a probability sample and as such the findings can be extrapolated to the Canadian population with a margin of error of +/3 per cent, 19 times out of 20.

The total contract value for this project was $79,903.66 including HST.

I hereby certify as a Representative of Kantar TNS that the deliverables fully comply with the Government of Canada political neutrality requirements outlined in the Communications Policy of the Government of Canada and Procedures for Planning and Contracting Public Opinion Research. Specifically, the deliverables do not include information on electoral voting intentions, political party preferences, standings with the electorate or ratings of the performance of apolitical party or its leaders.

Tanya Whitehead

Kantar TNS

Senior Research Director & Public-Sector Practice Lead

The Wireless Code, which was established in 2013 by the CRTC, is a mandatory code of conduct for wireless service providers and serves two primary goals: to ensure consumers are empowered to make informed decisions about wireless services; and to make it easier for consumers to take advantage of competitive offers. The Wireless Code includes provisions that address clarity; contracts and related documents; changes to contracts; bill management; mobile device issues; and cancellation.

The Wireless Code started to apply to new contracts as of December 2013 and applied to all contracts for retail mobile wireless voice and data services (wireless services) provided to individual and small business consumers in Canada as of June 3, 2015.

The CRTC committed to evaluating the effectiveness of the Wireless Code and recently completed a review to assess whether the Wireless Code has met and continues to meet its objectives, which includes ensuring that consumers are empowered to make informed decisions about wireless services.

On June 15, 2017, the CRTC announced multiple changes to the Wireless Code, which came into effect on December 1 2017 for all contracts.

The information collected in the 2018 Wireless Code public opinion research (POR) will help the CRTC assess whether Canadians are satisfied with the changes and whether further changes are required to ensure the objectives of the Wireless Code continue to be met.

Additionally, the 2018 Wireless Code POR continues to monitor trends related to the perceptions of the CRTC and has added a number of questions related to Canadians’ understanding and satisfaction with the new Television Service Provider (TVSP) Code, which came into effect on September 1st, 2017.

The overall objective of this research was to obtain tracking data on how consumers understand their wireless service contracts and their related rights as well as to further explore a variety of topics such as wireless complaints, data usage, bill shock, and ease of switching service providers.

The methodology was designed to ensure consistency with previous waves of Wireless Code surveys conducted in the Fall and Spring of 2016. This iteration of the research also explores Canadians’ satisfaction with the June 15th changes to the Wireless Code, general satisfaction with the CRTC and a number of issues related to the new TVSP Code.

More specifically, the survey was designed to address the following objectives:

For tracking purposes and comparability over time, some questions remained the same or similar to the ones used for the Wireless Code POR published in the Spring and Fall of 2016. To keep the survey no longer than 15 minutes, questions not needed for tracking purposes were removed and several new questions were added to the survey to obtain the additional informational requirements.

A telephone survey was conducted among 1,345 Canadians aged 18 years and older; 1,152 with those who have their own wireless plan and 193 with those who do not have a wireless plan. Interviews were conducted using random landline telephone sampling sources. A pre-test consisting of 10 completed English interviews and 10 completed French interviews was done before fielding the survey on January 25th, 2018. The survey was in field from January 26th to February 8th, 2018. The sample for this study was a probability sample and as such the findings can be extrapolated to the Canadian population with a margin of error of +/-3 per cent, 19 times out of 20. A detailed methodology can be found in Chapter 5.

Please note: Analysis was undertaken to establish the extent of the relationship among variables such as gender, age, region, level of education attained, language spoken, household income, type of plan (family vs. individual; prepaid vs, postpaid; employee; subsidized phone/device; limited vs. unlimited data), complaints and bill shock. Only differences significant at the 95% confidence level are presented in this report. Any differences that are statistically significant between subgroups are indicated with an uppercase letter to refer to the applicable column.

The numbers presented throughout this report are rounded to the closest full number. Due to this rounding, in some cases it may appear that ratings collapsed together are different by a percentage point from when they are presented individually, and totals may not add up to 100%. Also, the data for 2014 and 2015 was taken directly from the 2014 and 2015 Wireless Code Public Opinion Research reports. TNS has incorporated these results as well as results from Spring and Fall 2016 into the 2018 report for year-over-year comparison where possible.

Wireless Data Usage

The composition of wireless plans has remained stable when compared to the Fall 2016 results. More specifically, wireless plans that include data continue to be common in Canada (76%). The majority of wireless plans have limited data (85%), which results in most Canadians (94% compared to 91% in Fall 2016) attempting to manage their data so as not to incur additional costs.

Canadians report finding it easy to manage their data (77%) and use tools to track their usage (59%). Despite this, a considerable portion (49%) of wireless owners report having paid data overages in the last 12 months, suggesting that data management may in fact be harder than anticipated for many Canadians.

Bill shock and Roaming fees

Almost a quarter of Canadians (24%) continue to experience bill shock suggesting that there continues to be room for improvement in this area moving forward. This is a slight, although not statistically significant increase, from Fall 2016 (21%). Some Canadians continue to struggle to track how much data they use, to understand the cost of international roaming and to understand the cost of long distance calling.

Younger Canadians (18-54) continue to be more likely to experience bill shock compared to those who are 55 years of age or older (21-63% vs. 15%), as are those with tab contracts (29% vs. 21%), and not unexpectedly, those who find data management difficult (62% vs. 19%).

The amount of unexpected charges varies greatly – from less than $50 to over $1 000 in one billing cycle. Most of the unexpected charges continue to be $100 or less (61%).

Almost one in every five Canadians (17%) finds it quite difficult to manage roaming fees while travelling. Men find managing roaming fees easier to manage than women (56% vs. 48%), as well as those with a higher income (68% vs. 39-53%).

Understanding of Contracts

A majority of Canadians (61%) find their contracts clear and easy to understand. This is truer for those aged 18-34 when compared to older Canadians (74% vs. 55-56%). Unlimited data contracts seem to be easier to understand (70% vs. 42%) for many Canadians and those who find data management easy also find their contracts easier to understand (70% vs. 42%).

The newly instated trial period explanation is somewhat unclear to many Canadians. It was found clear and easy to understand by only one in three Canadians (36%). There is also some indication that the trial period may be more confusing for those with a higher education. Those with higher education levels are more likely to find the explanation unclear or difficult to understand compared to those with lower education levels (44% vs. 31%)). A more thorough investigation into this would be required.

Some Canadians are also having some challenges related to the explanation of cancellation fees. One in four Canadians find the explanation unclear. Interestingly, the data also shows that Canadians with higher educations are more likely to find the cancellation fee explanation unclear (32% vs. 18%) which raises a red flag as to how well this clause is really understood.

Changes

When it comes to changes to contracts, a small number of wireless owners report changes being made to their contracts without prior notification (12%).

A small number of Canadians (16%) have switched service providers in the last two years with the main reason being a better deal (49%).

Complaints

Canadians are making fewer complaints than in the past suggesting the Wireless Code is having a positive impact for wireless consumers. Eighteen per cent of Canadians have made a complaint in the last year resulting in a decrease of eight per cent since 2014. The reasons for complaints are changing with only one of the previous four main reasons now being mentioned (compared to Fall 2016) – previous main reasons for complaints comparing Fall 2016 with 2018 results, were incorrect charges on their bill (45% vs. 17%), inadequate quality of service (25% vs. 16%) and misleading information about the terms of contract (23% vs. 12%). In 2018 data charges seem to be the biggest thorn in consumers’ sides (29%), which was the fourth highest reason for complaining in Fall 2016 (32%). Consumers continue to primarily complain to their service providers (97%) with 5% of these complaints also going to the Commissioner for Complaints for Telecommunications Services (Canada) (CCTS). The CCTS responds to complaints from consumers if the consumer believes the complaint remains unresolved by the service provider.

Demographic Differences

A number of additional demographic analyses were also undertaken including age, gender, education, income and language. The most significant differences were related to age and education.

Age:

Canadians aged 18-54 are substantially different than their older counterparts (55+) in a number of ways:

Education:

Canadians with a higher level of education (university degree or higher) have slightly different outcomes compared to those with lower levels of education. More specifically:

Television Service Provider Code

Due to the relatively recent introduction of the Television Service Provider (TVSP) Code, it is not surprising that only half of Canadians have heard of the TVSP Code (56%). It is however, surprising that only half of TV subscribers (54%) believe they have been informed of their entry-level service offering, especially given the requirement that all customers should have been informed.

At an overall level many Canadians find their TV contracts clear and easy to understand (57%) and only 14% have experienced difficulties related to TV service calls. TV subscribers are usually informed of price changes (76%) and only one in four consumers have made a complaint about their TV service in the last 12 months.

CRTC

Over the past five years, Canadians’ understanding of the mandate and role of the CRTC has declined. In 2014, 38 per cent of Canadians considered themselves informed about the mandate and role of the CRTC while in 2018, only 29 per cent consider themselves informed.

Overall Canadians’ impressions of the CRTC continue to be neutral in 2018 than they were in 2014. However, it is necessary to take into consideration that only one in three Canadians report being well informed of the CRTC’s role which implies that two in three consumers’ impressions of the CRTC are based on very little to no knowledge. In fact, when looking at the opinions of those who consider themselves very well or well informed about the CRTC’s role, 50-55% are positive about the CRTC. This implies that there is still work to be done to not only inform the public of the CRTC and their role, but also to address public perceptions.

Strategic implications

The results of this research provide evidence that suggests the Wireless Code continues to have positive impacts on Canadians[2]. It also provides information to be considered for future updates of the Wireless Code and/or the Television Service Provider Code.

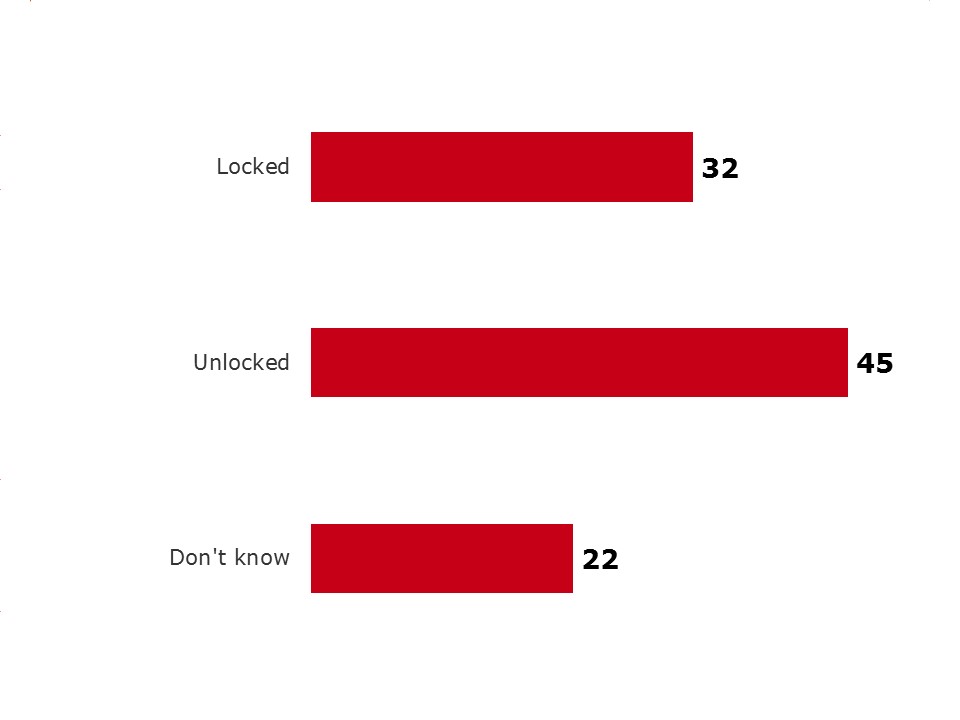

The Wireless Code came into effect in 2013 and was updated in 2017. As a result, the Wireless Code now ensures that customers will be provided with unlocked devices, gives families more control over data overages, sets minimum usage limits for the trial period that correspond to at least half of the monthly usage limits of the customer’s plan, and clarifies that data is a key contract term that cannot be changed during the commitment period without the customer’s consent.

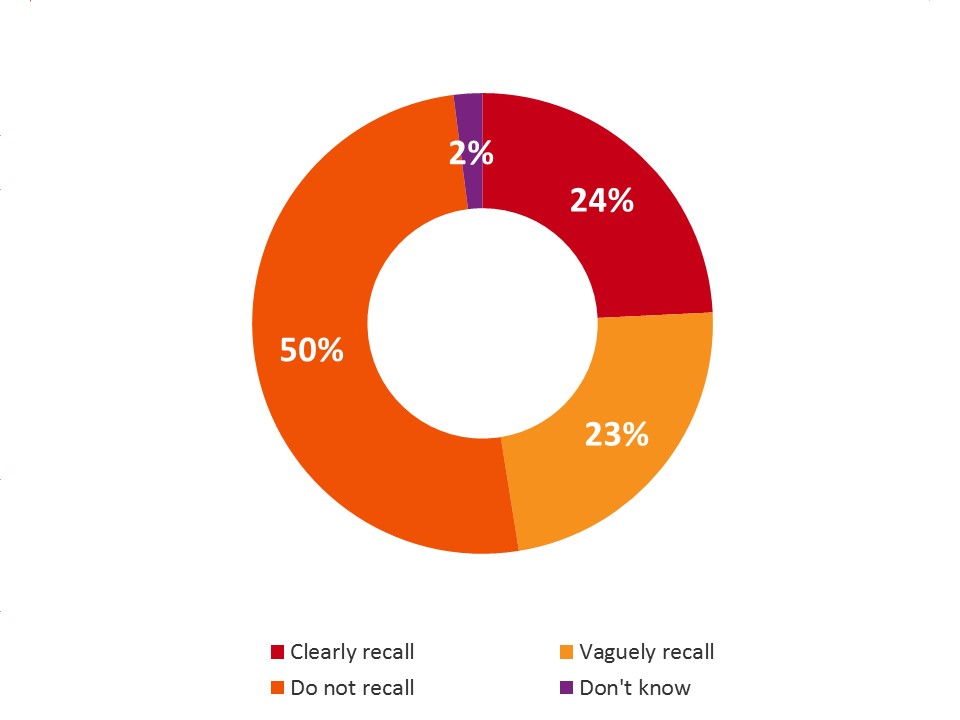

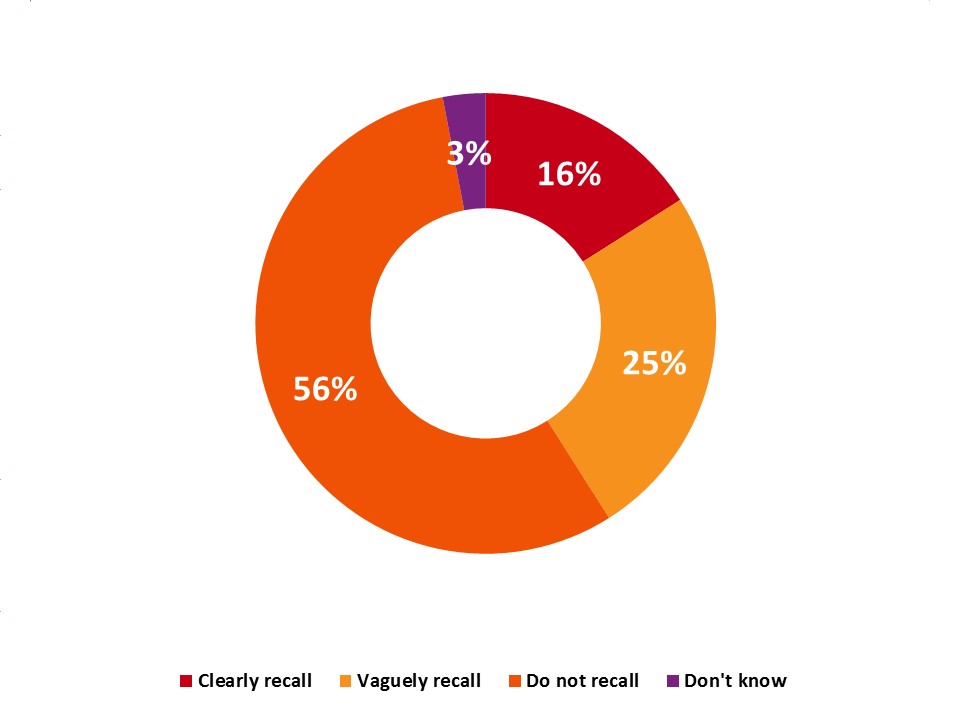

Despite the Wireless Code being in effect for nearly 5 years, half of Canadians (50%) do not recall hearing or seeing anything about it. There is higher awareness of the Wireless Code among those with a higher education level (clear recall 24-31% for College or University graduates vs. 12% for those with no tertiary education) as well as those with a higher income (clear recall 29-39% for those who earn more than $60k per year vs. 12-14% for those with an income of less than $60k per year).

Exhibit 4.1.a Recall of the Wireless Code

Recall of the Wireless Code - text version

WC1. In 2013 a Wireless Code came into effect establishing guidelines for wireless service providers. The Code ensures that wireless consumers are empowered to make informed decisions and that there is a more competitive wireless marketplace. The Code was updated in 2017 to end unlocking fees and offer longer trial periods for new contracts. To what extent, if any would you say you recall hearing or seeing anything about this Code? Would you say you clearly recall, vaguely recall or do not recall?

Base: Total respondents (n=1,345)

Exhibit 4.1.b Recall of the Wireless Code by education and income

Data included in wireless plan |

Total (A) |

Income | Education | ||||||

|---|---|---|---|---|---|---|---|---|---|

| <$40K (E) |

$40K- <$60K (F) |

$60K- <$100K (G) |

$100K- <$150K (H) |

$150K+ (I) |

High school or less (P) |

College (Q) |

University or more (R) |

||

| Base=actual | (1,345) % |

(286) % |

(210) % |

(296) % |

(183) % |

(154) % |

(382) % |

(366) % |

(576) % |

| Clearly Recall | 24 | 12 | 14 | 30 EF | 29 EF | 39 EF | 12 | 24 P | 31 P |

| Vaguely Recall | 23 | 17 | 21 | 28 E | 24 | 26 | 18 | 25 | 25 |

| Do not recall | 50 | 66 GHI | 60 GHI | 41 | 46 | 33 | 67 QR | 50 R | 41 |

| Don’t know | 2 | 4 | 5 | 1 | 1 | 1 | 3 | 1 | 3 |

QWC1. In 2013 a Wireless Code came into effect establishing guidelines for wireless service providers. The Code ensures that wireless consumers are empowered to make informed decisions and that there is a more competitive wireless marketplace. The Code was updated in 2017 to end unlocking fees and offer longer trial periods for new contracts. To what extent, if any would you say you recall hearing or seeing anything about this Code? Would you say you clearly recall, vaguely recall or do not recall?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

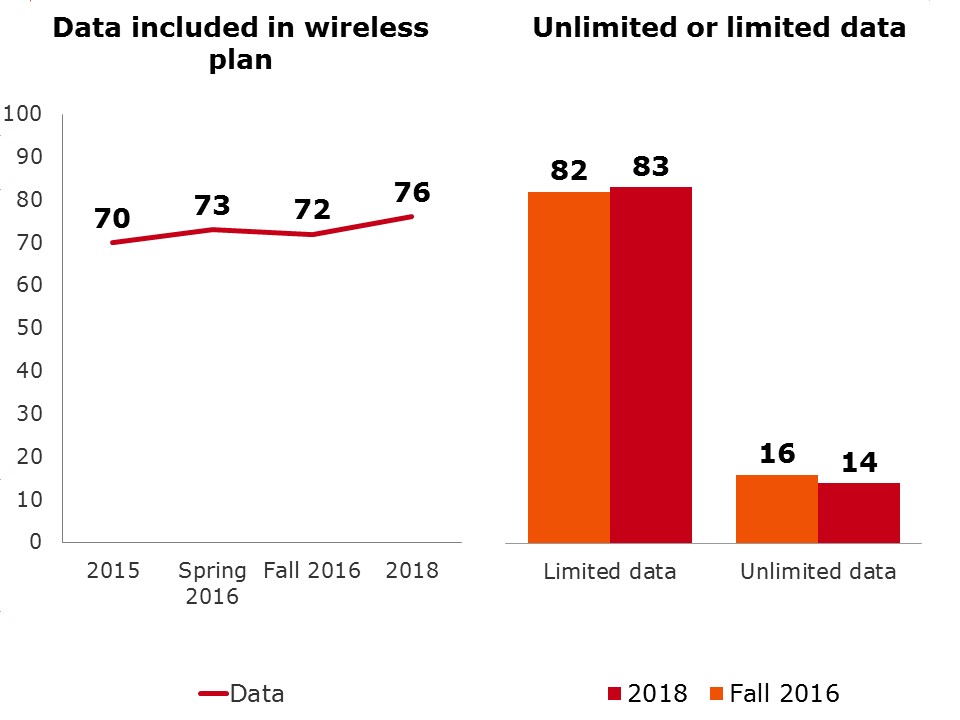

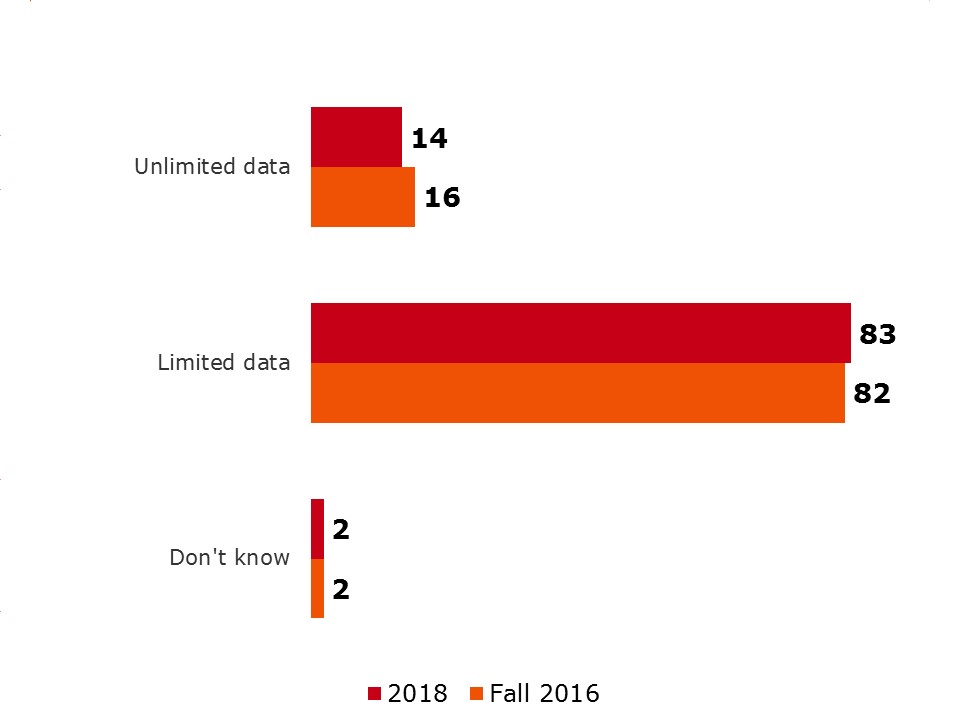

Wireless plans that include data continue to be increasingly common in Canada. Now more than three quarters of Canadians (76% compared to 72% in Fall of 2016) have wireless plans that include data. The clear majority still have limited data (83%) while a small but significant proportion have unlimited wireless data (14%).

Exhibit 4.2.a. Data included in wireless plan over time and limited or unlimited plans

Data included in wireless plan over time and limited or unlimited plans - text version

QB2a. Which of the following are included in your wireless plan?

Base: Respondents who own a cell phone, fall 2016 (n=1,277), 2018 (n=1,111)

QB9c3. Is Data included as part of your plan?

Base: Total Respondents Spring 2016 (n=925), 2015 (n=1,005)

QB4. Does your plan include unlimited or limited data?

Base: Respondents who have data included in the wireless plan, fall 2016 (n=831), 2018 (n=796)

A variety of demographic factors continue to influence whether or not Canadians have wireless plans that include data:

Exhibit 4.2.b. Data included in wireless plan by age and region

| Data included in wireless plan | Total (A) |

Age | Region | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 18-34 (D) |

35-54 (E) |

55+ (F) |

Atl (G) |

Que (H) |

Ont (I) |

Pra (J) |

BC (K) |

Terr (O) |

||

| Base=actual | (1,111) % |

(141) % |

(359) % |

(594) % |

(102) % |

(224) % |

(301) % |

(310) % |

(126) % |

(48) % |

| Yes | 76 | 83 F | 87 F | 60 | 70 | 71 | 75 | 81 GH | 79 | 90 GH |

QB2a. Which of the following are included in your wireless plan?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.2.c. Data included in wireless plan by income and education

| Data included in wireless plan | Total (A) |

Income | Education | ||||||

|---|---|---|---|---|---|---|---|---|---|

| <$40K (E) |

$40K- <$60K (F) |

$60K- <$100K (G) |

$100K- <$150K (H) |

$150K+ (I) |

High school or less (P) |

College (Q) |

University or more (R) |

||

| Base=actual | (1,111) % |

(199) % |

(168) % |

(261) % |

(163) % |

(141) % |

(278) % |

(314) % |

(501) % |

| Yes | 76 | 61 | 73 | 75 E | 92 EFG | 95 EFG | 65 | 78 P | 81 P |

QB2a. Which of the following are included in your wireless plan?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.2.d. Data included in wireless plan by language and tab contract

Data included in wireless plan |

Total (A) |

Language | Tab contracts | |||

|---|---|---|---|---|---|---|

| English (B) |

French (C) |

Other (D) |

Yes (E) |

No (F) |

||

| Base=actual | (1,111) % |

(741) % |

(219) % |

(144) % |

(293) % |

(744) % |

| Yes | 76 | 78 C | 69 | 77 | 88 F | 71 |

QB2a. Which of the following are included in your wireless plan?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

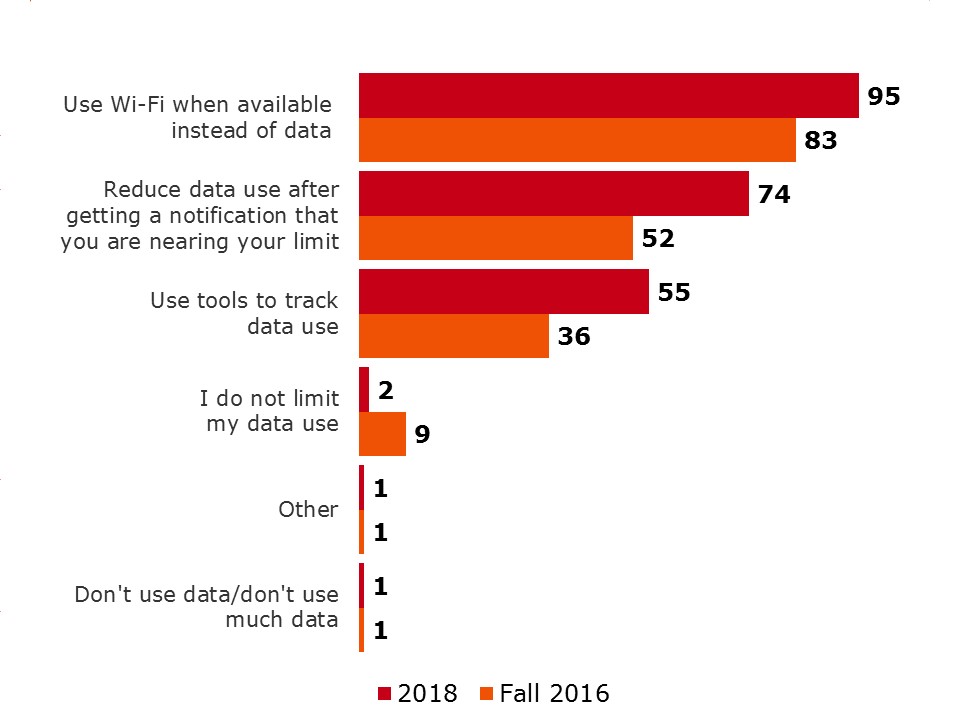

Almost all Canadians who have data in their wireless plans try to manage or limit their data use (94%). The extent of the activities undertaken to manage data varies and continues to mostly involve using Wi-Fi when available (95%). However, there is a significant increase in those who reduce data use when notified (74% vs. 52%) or actively monitor usage (55% vs. 36%) when comparing fall 2016 to 2018.

The younger age groups (18-54) are more likely to employ activities to manage or limit data usage. This is true for switching to Wi-Fi when available (97-98% for 18-54 year olds vs. 88% for 55+), using tools to track data (56-68% for 18-54 year olds vs. 35% for 55+) as well as reducing data usage when notified (75-84% for 18-54 year olds vs. 61% for 55+). This might well be due to a more limited understanding of the older age group of how to manage and limit data usage as opposed to a resistance to do so.

Not surprisingly, those who report data management to be easy are more likely to use tools to track data than those who find data management difficult (59% vs. 43%). A reduction in data usage is more likely to occur by those who have family plans (81% vs. 68%).

Exhibit 4.2.1.a. Activities to manage or limit data use

Activities to manage or limit data use - text version

QB5a. Which of the following activities, if any, do you do to manage or limit your data use? Select all that apply.

Base: Respondents who have limited data included in the wireless plan, fall 2016 (n=831), winter 2017 (651).

Exhibit 4.2.1.b. Activities to manage or limit data use by age

Activities done to manage or limit data use |

Total (A) |

Age | ||

|---|---|---|---|---|

| 18-34 (D) |

35-54 (E) |

55+ (F) |

||

| Base=actual | (651) % |

(99) % |

(267) % |

(278) % |

| Use Wi-Fi when available instead of data | 95 | 98 F | 97 F | 88 |

| Reduce data use after getting a notification | 74 | 84 F | 75 F | 61 |

| Use tools to track data use | 54 | 68 F | 56 F | 35 |

| I do not limit my data use | 2 | 4 | 1 | 2 |

QB5A. Which of the following activities, if any, do you use to manage or limit your data use? Select all that apply.

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.2.1.c. Activities to manage or limit data use data management and family plans

| Activities to manage or limit data use | Total (A) |

Manage Data | Plan | ||

|---|---|---|---|---|---|

| Easy (F) |

Difficult (G) |

Family (J) |

Individual (K) |

||

| Base=actual | (651) % |

(498) % |

(85) % |

(267) % |

(376) % |

| Use Wi-Fi when available instead of data | 95 | 96 | 95 | 97 | 94 |

| Reduce data use after getting a notification | 74 | 72 | 83 | 81 K | 68 |

| Use tools to track data use | 55 | 59 G | 43 | 59 | 51 |

| I do not limit my data use |

2 | 1 | 2 | 1 | 2 |

| Other | 1 | 1 | 1 | 2 | <1 |

| Don't use data/don't use much data | 1 | 1 | 2 | 1 | 2 |

QB5a. Which of the following activities, if any, do you do to manage or limit your data use? Select all that apply.

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

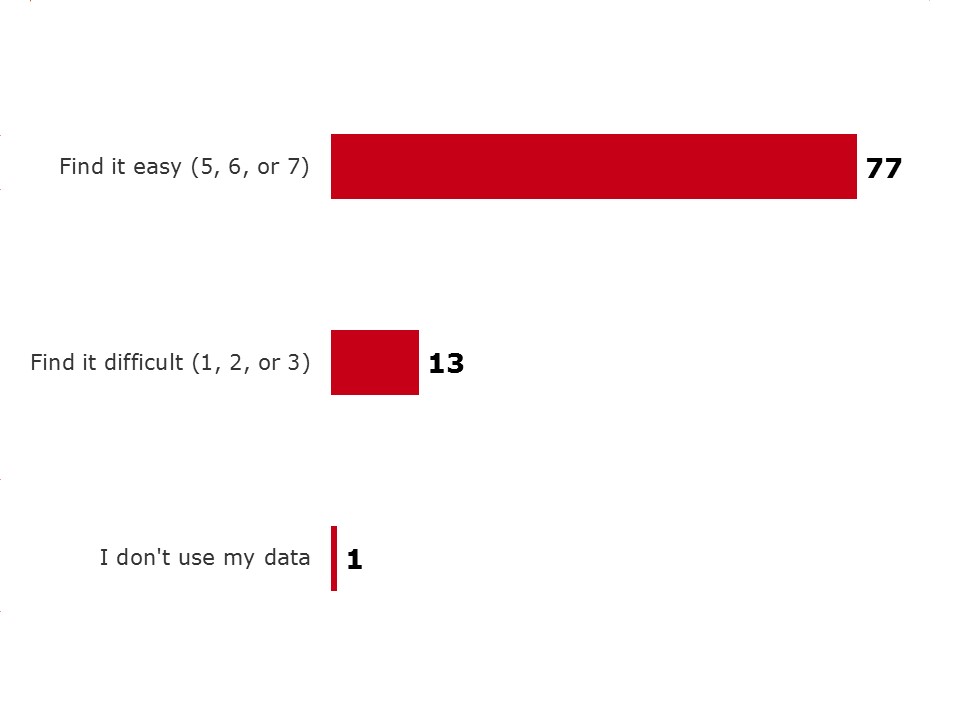

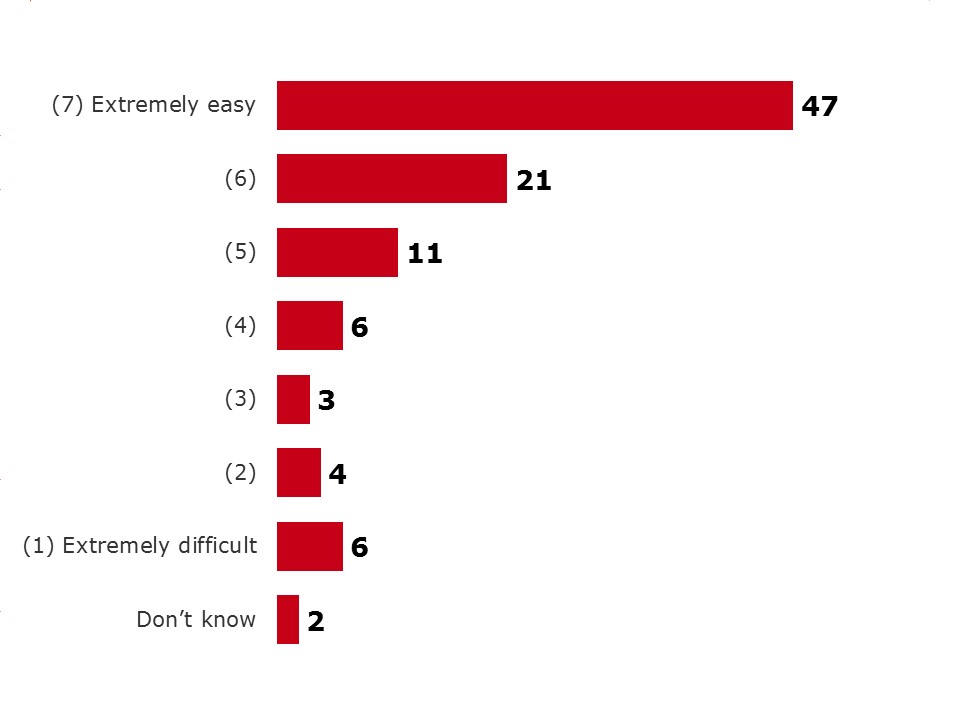

Most Canadians report finding it easy to manage their data each month. More than three in four Canadians (77%) consider it easy (5, 6 or 7 on a scale of 1-7).

However, we have seen in the previous section that older people (55+) are less likely to use data management strategies. Despite that, there is no significant differences in the reporting of ease of data management between the younger and older age groups.

Canadians who have lodged a complaint (19%) however, continue to find it more difficult to manage data use (26% vs. 8%) (1, 2 or 3 on a scale of 1-7).

Exhibit 4.2.2.a. Level of difficulty managing data use each month among those with data and those with data in a shared plan

Activities to manage or limit data use - text version

QB6. How easy do you find it to manage your data use each month? Please use a 7-point scale where 1 means extremely difficult and 7 means extremely easy. Base: Respondents who have data included in the wireless plan, fall 2016 (n=831)

WC6. How easy do you find it to manage the data used by yourself and/or your family each month?

Base: Respondents who have data included in their plan, winter 2017 (n=792)

Exhibit 4.2.2.b. Level of difficulty managing data use each month by lodged a complaint

| Level of difficulty to manage data use | Total (A) |

Lodged Complaint | ||

|---|---|---|---|---|

| Yes (S) |

No (T) |

|||

| Base=actual | (792) % |

(148) % |

(642) % |

|

| Find it easy to manage data each month (5, 6 or 7) | 77 | 60 | 82 S | |

| Find it difficult to manage data each month (1, 2 or 3) | 13 | 26 T | 9 | |

QWC6. How easy do you find it to manage the data used by yourself and/or your family each month? Please use a 7-point scale where 1 means extremely difficult and 7 means extremely easy.

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

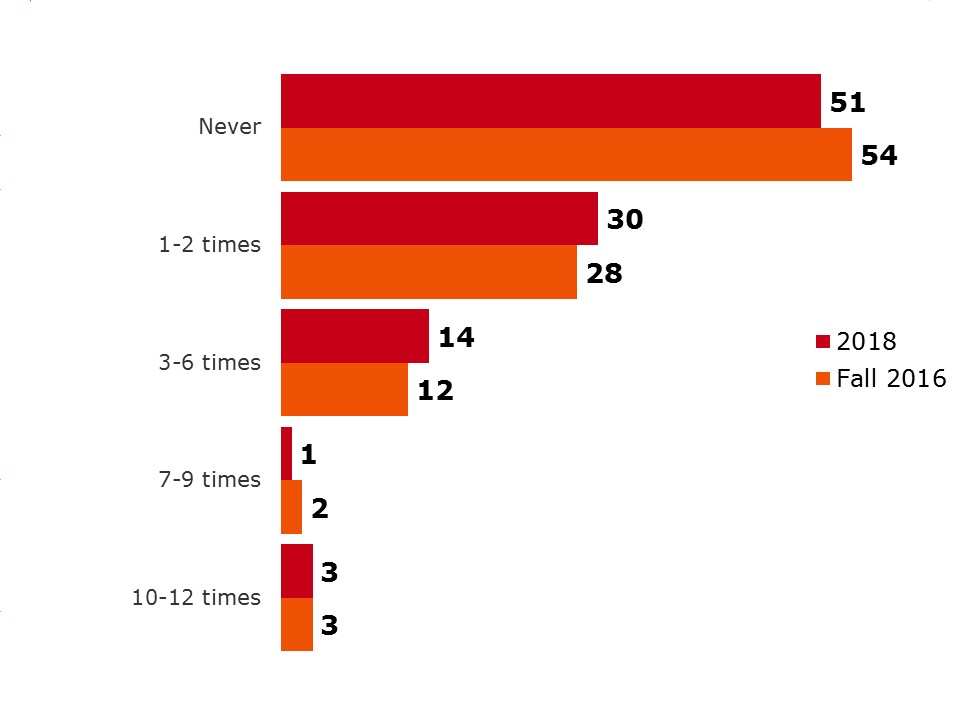

While many Canadians consider it easy to manage their data, a considerable portion (49%) continue to have paid data overages in the past 12 months suggesting that some Canadians are, in fact, struggling to manage their data in a way that prevents additional fees. Although not significant, there is a slight increase since Fall 2016 (46%). Most of those (74%) that have paid data overages have done so only once or twice in the past 12 months.

While the 2016 results showed no skews towards any particular demographic group, the picture has changed considerably in 2018 with a variety of demographic factors that influence whether or not Canadians have paid data overage fees:

There are a number of other factors that impact whether or not Canadians have paid data overage fees. These include what type of plan they have, whether or not they manage their data and how informed they are about the CRTC.

Consistent with previous year’s results, those with a family plan are more likely to have paid data overage fees in the last 12 months compared to those on an individual plan (58% vs. 42%).[3] Canadians with an employee purchase plan are less likely to have paid data overage fees (32% vs. 50%) compared to those who do not have an employee purchase plan. This is also true for those with unlimited data compared to those with limited data (33% vs. 63%).

Not surprisingly, those who find data management difficult are more likely to have paid data overage fees in the past 12 months (81% vs. 42%). However, this may also be due to a difference in perception of ease of data management. As one would expect, those who find data management easy are less likely to have paid data overage fees. In fact, only 13 percent of those who find data management easy have paid data overage fees 3 times or more in the past 12 months.

The data also shows that Canadians who are very well informed of the role of the CRTC are less likely to have paid data overage fees (25%) compared to those who are less informed of the role or do not understand its role very well (52-54%). While, the CRTC doesn’t manage data for consumers, it did specifically examine the tools available to help consumers manage their data and expects wireless service providers to offer those tools. Thus, it is not surprising that a more informed consumer tends to have a greater ability to steer clear of data overage fees.

Exhibit 4.2.3.a. Data overage fees paid in the past 12 months

Data overage fees paid in the past 12 months - text version

QB8. In the past 12 months, how often have you paid data overage fees?

Base: Respondents who have data included in the wireless plan, fall 2016 (n=831)

Exhibit 4.2.3.b. Data overage fees paid in the past 12 months by plan and data

Data overage fees paid in the past 12 months |

Total (A) |

Plan | Data | ||

|---|---|---|---|---|---|

| Family (J) |

Individual (K) |

Unlimited (D) |

Limited (E) |

||

| Base=actual | (796) % |

(326) % |

(460) % |

(122) % |

(651) % |

| Never | 51 | 42 | 58 J | 67 E | 47 |

| 1-2 times | 30 | 32 | 28 | 23 | 32 |

| 3-6 times | 14 | 20 K | 10 | 7 | 16 |

| 7-9 times | 1 | 2 | * | - | 1 |

| 10-12 times | 3 | 3 | 3 | 2 | 4 |

* denotes less than 1%.

QB8. In the past 12 months, how often have you paid data overage fees?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.2.3.c. Data overage fees paid in the past 12 months by age and region

Data overage fees paid in the past 12 months |

Total (A) |

Age | Region | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 18-34 (D) |

35-54 (E) |

55+ (F) |

Atl (G) |

Que (H) |

Ont (I) |

Pra (J) |

BC (K) |

Terr (O) |

||

| Base=actual | (796) % |

(120) % |

(313) % |

(353) % |

(71) % |

(141) % |

(219) % |

(226) % |

(96) % |

(43) % |

| Never | 51 | 39 | 52 D | 63 DE | 55 O | 62 IO | 47O | 56 O | 48 O | 26 |

| 1-2 times | 30 | 34 F | 31 F | 23 | 25 | 25 | 32 | 28 | 33 | 33 |

| 3-6 times | 14 | 19 F | 13 | 10 | 10 | 10 | 16 | 10 | 15 | 35 GHIJK |

| 7-9 times | 1 | 1 | 1 | 1 | 3 | - | 1 | 1 | 2 | - |

| 10-12 times | 3 | 6 | 2 | 2 | 8 | 2 | 3 | 4 | 1 | 6 |

QB8. In the past 12 months, how often have you paid data overage fees?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.2.3.d. Data overage fees paid in the past 12 months by language, employee purchase plan, and data

| Data overage fees paid in the past 12 months | Total (A) |

Language | Employee purchase plan | Data | ||||

|---|---|---|---|---|---|---|---|---|

| English (B) |

French (C) |

Other (D) |

Yes (N) |

No (O) |

Unlimited (D) |

Limited (E) |

||

| Base=actual | (796) % |

(550) % |

(137) % |

(106) % |

(62) % |

(728) % |

(122) % |

(721) % |

| Never | 51 | 51 | 62 D | 46 | 68 O | 50 | 67 E | 47 |

| 1-2 times | 30 | 27 | 23 | 42 BC | 21 | 31 | 23 | 32 |

| 3-6 times | 14 | 17 | 11 | 8 | 8 | 14 | 7 | 16 |

| 7-9 times | 1 | 2 | - | - | - | 1 | - | 1 |

| 10-12 times | 3 | 3 | 2 | 4 | 3 | 3 | 2 | 4 |

QB8. In the past 12 months, how often have you paid data overage fees?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.2.3.e. Data overage fees paid in the past 12 months by manage data and CRTC mandate

| Data overage fees paid in the past 12 months | Total (A) |

Manage data | Informed role of CRTC | ||||

|---|---|---|---|---|---|---|---|

| Easy (F) |

Difficult (G) |

Very well (K) | Well (L) |

Not very well (M) |

Not (N) |

||

| Base=actual | (796) % |

(610) % |

(98) % |

(51) % |

(204) % |

(333) % |

(197) % |

| Never | 51 | 58 G | 19 | 75 MN | 57 | 46 | 48 |

| 1-2 times | 30 | 29 | 31 | 19 | 22 | 37 L | 28 |

| 3-6 times | 14 | 10 | 36 F | 4 | 18 | 12 | 17 |

| 7-9 times | 1 | 1 | 3 | 1 | 2 | 1 | - |

| 10-12 times | 3 | 2 | 11 F | 1 | 1 | 3 | 6 L |

QB8. In the past 12 months, how often have you paid data overage fees?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

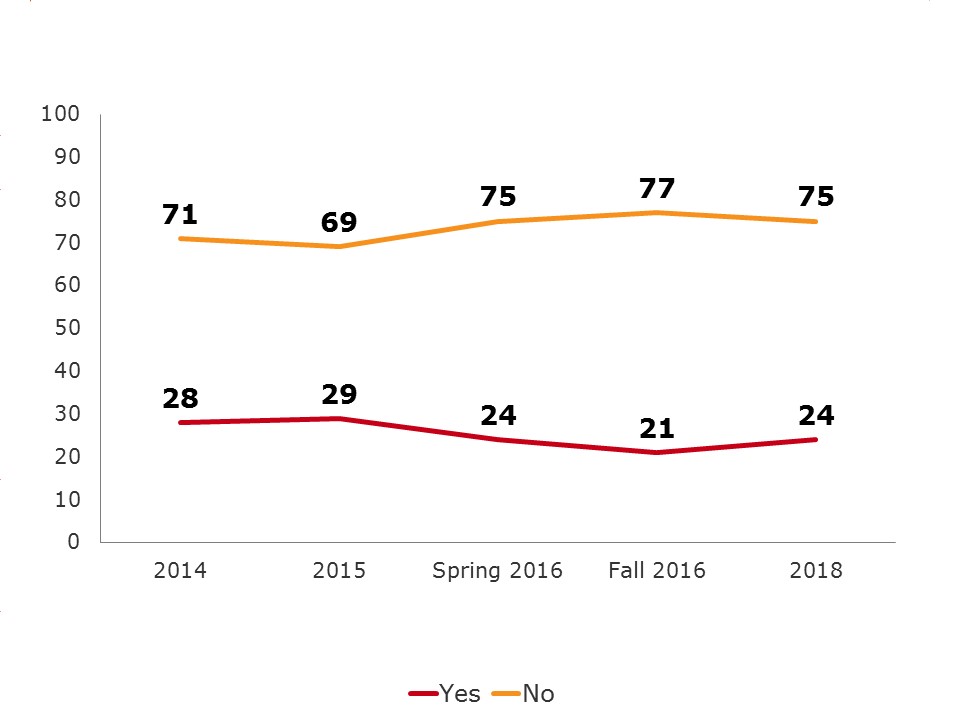

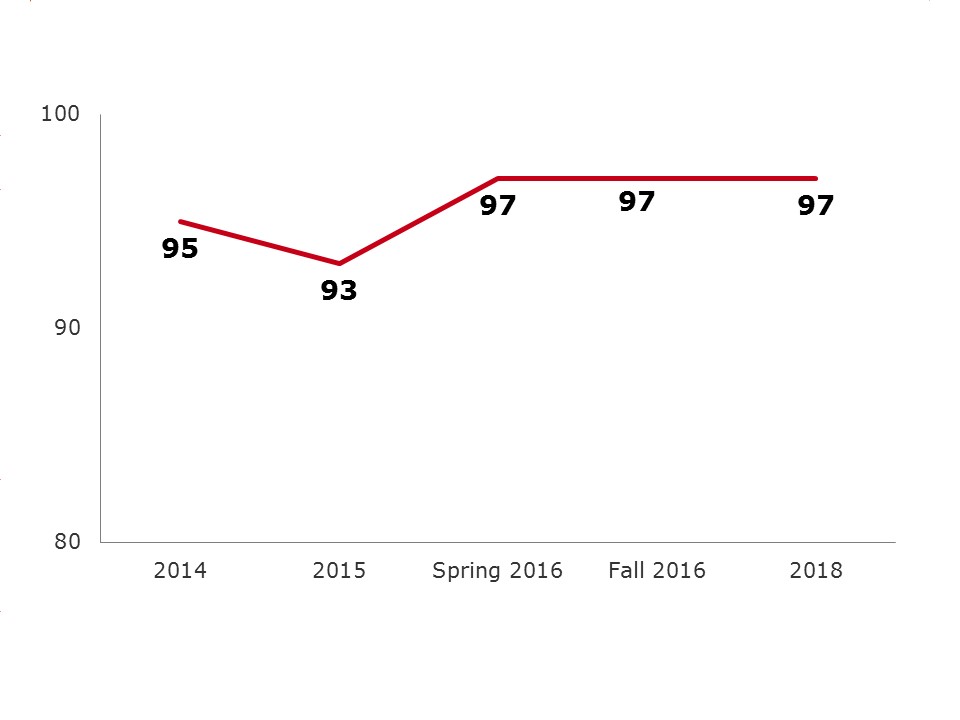

While the overall incidence of experiencing bill shock is relatively low, a small but significant portion of the population continues to experience bill shock in 2018 (24%). This suggests there continues to be room for improvement in this area.

Exhibit 4.3.1.a. Experienced bill shock

Experienced bill shock - text version

QB10/B6. During the last year, have you experienced ‘bill shock’, meaning a surprisingly high bill?

Base: Respondents who own a cell phone,2018 (n=1,111), fall 2016 (n=1,277), total respondents Spring 2016 (n=925), 2015 (n=1,005), 2014 (n=1,016)

Younger Canadians (18-54) continue to be substantially more likely to experience bill shock than their older counterparts (18-35: 36% & 35-54: 21% vs. 55+:15%). As are those who have made a complaint (61% vs. 15%), those with tab contracts (29% vs. 21%) and those who find data management difficult (62% vs. 19%). Quebec residents (16% vs. 26-31%) and Francophones (23% vs. 13%) are still the least likely to experience bill shock, as are those with individual plans (29% vs. 21%).

There are also a number of factors that appear to play a role in relation to experiencing bill shock in the last 12 months. Canadians with a wireless family plan where four people share the plan are more likely to experience bill shock ( (26% vs. 13%) and Canadians with data services included in their wireless plan are more likely to experience bill shock (83% vs. 74%).

Not unexpectedly, Canadians who experience bill shock are also more likely to take action by reducing data usage after receiving a notification of nearing their data limit (87% vs. 69%). Those with bill shock also find it more difficult to manage roaming fees while travelling (34% vs. 12%). Furthermore, those who have experienced bill shock in the last year, are more likely to report unclear explanation of contract cancellation implications (rated 1-3 on a scale from 1-7) (34% vs. 24%), find their contracts unclear and difficult to understand (rated 1-3 on a scale from 1-7) 29% vs. 14%) and are also more likely to report changes made to their contracts without being made aware of the changes (27% vs. 7%).

Exhibit 4.3.1.b. Experienced bill shock by age and region

| Experienced bill shock | Total (A) |

Age | Region | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 18-34 (D) |

35-54 (E) |

55+ (F) |

Atl (G) |

Que (H) |

Ont (I) |

Pra (J) |

BC (K) |

Terr (O) |

||

| Base=actual | (1,111) % |

(141) % |

(359) % |

(594) % |

(102) % |

(224) % |

(301) % |

(310) % |

(126) % |

(48) % |

| Yes | 24 | 36 EF | 21 F | 15 | 16 | 16 | 28 H | 26 H | 19 | 31 |

| No | 75 | 63 | 78 D | 84 D | 84 I | 83 IJO | 71 | 73 | 77 | 67 |

QB10. During the last year, have you experienced ‘bill shock, meaning a surprisingly high bill?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.3.1.c. Experienced bill shock by language and plan

| Experienced bill shock | Total (A) |

Language | Plan | |||

|---|---|---|---|---|---|---|

| English (B) |

French (C) |

Other (D) |

Family (J) |

Individual (K) |

||

| Base=actual | (1,111) % |

(741) % |

(219) % |

(144) % |

(368) % |

(713) % |

| Yes | 24 | 23 C | 13 | 35 BC | 29 K | 21 |

| No | 75 | 76 D | 87 BD | 63 | 70 | 78 J |

QB10. During the last year, have you experienced ‘bill shock, meaning a surprisingly high bill?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.3.1.d. Experienced bill shock by tab contract, manage data and complaint

Experienced bill shock |

Total (A) |

Tab Contract | Difficulty managing data | Lodged a complaint | |||

|---|---|---|---|---|---|---|---|

| Yes (B) |

No (C) |

Easy (F) |

Difficult (G) |

Made one (S) |

Did not make one (T) |

||

| Base=actual | (1,111) % |

(293) % |

(744) % |

(610) % |

(98) % |

(183) % |

(925) % |

| Yes | 24 | 29 C | 21 | 19 | 62 F | 61 T | 15 |

| No | 75 | 70 | 78 B | 80 G | 37 | 37 | 84 S |

QB10. During the last year, have you experienced ‘bill shock, meaning a surprisingly high bill?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Reasons

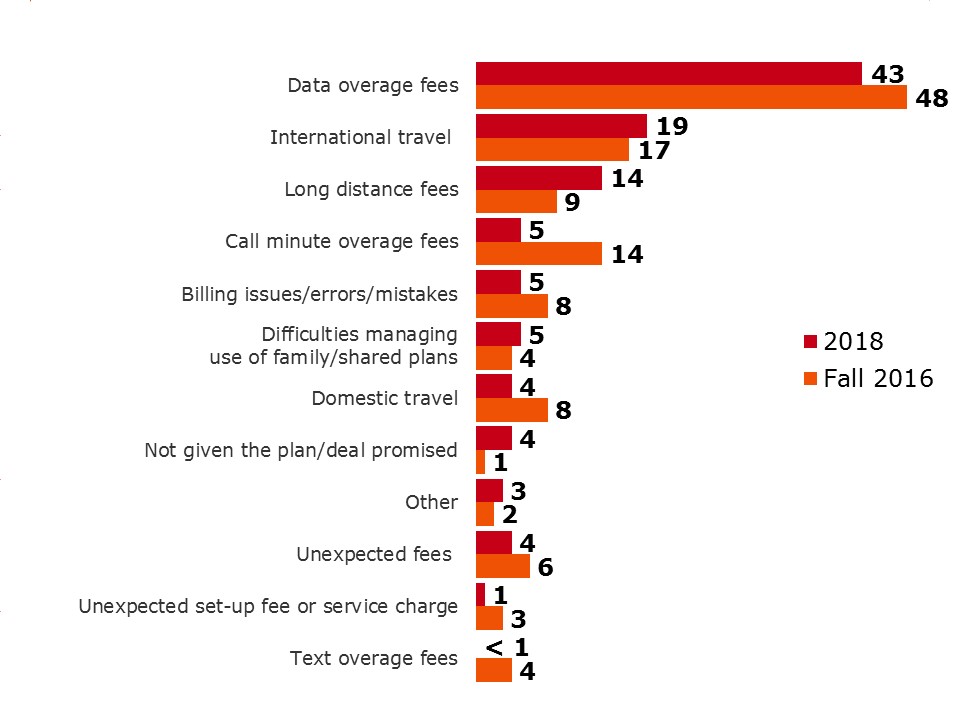

Results suggest that data overage fees are still the main reason for bill shock (43%). This is especially true for those who have a high school education or less compared to those with a college or university education (52% vs. 38-43%). However, base sizes are small which means the findings should be considered directional.

While call minute overage fees were one of the leading causes of bill shock in the Fall of 2016 (14%) it is not as common in 2018 (5%). However, long-distance fees (14%) appear to be more pertinent than in the Fall of 2016. This suggests that Canadians are still struggling to:

Exhibit 4.3.1.e. Main reason for bill shock

Main reason for bill shock - text version

QB10a. What was the main reason for the ‘bill shock’ you experienced?

Base: Those who experienced ‘bill shock’, 2018 (n=211), fall 2016 (n=250)

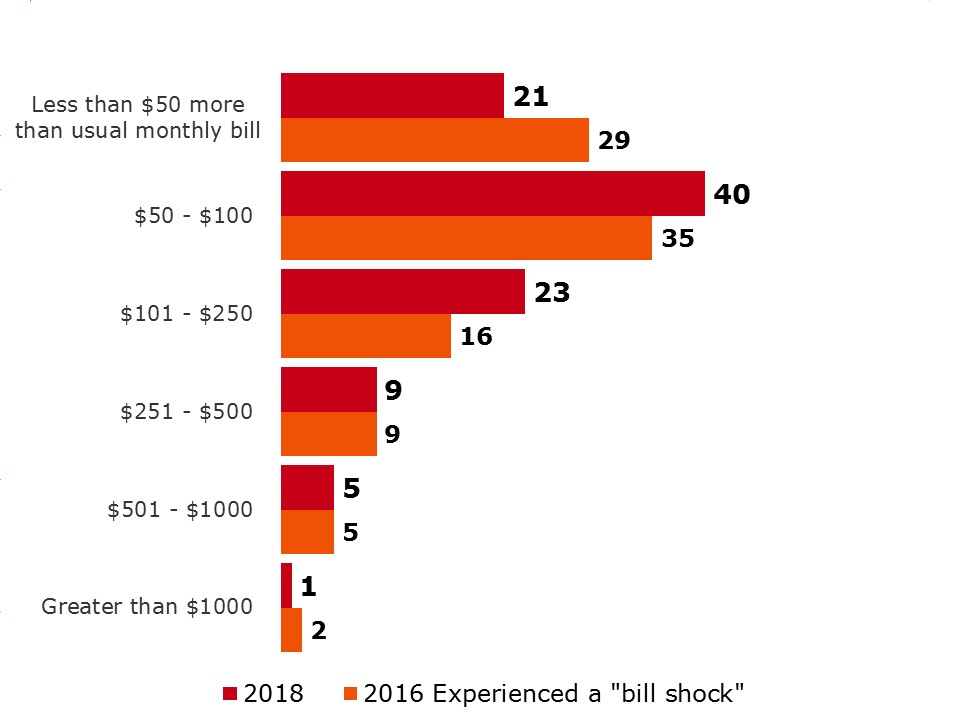

Amount

The amount of the unexpected charges varies from less than $50 to over $1,000 per billing cycle. Most of the unexpected charges (61%) however, are still $100 or less per month.

Exhibit 4.3.1.f. Amount of unexpected charges on bill among those who have experienced a “bill shock”

Amount of unexpected charges on bill among those who have experienced a “bill shock” - text version

Q10b. What was the amount of the unexpected charges on your bill?

Base: Respondents who have experienced a “bill shock”, 2018 (n=211), fall 2016 (n=285)

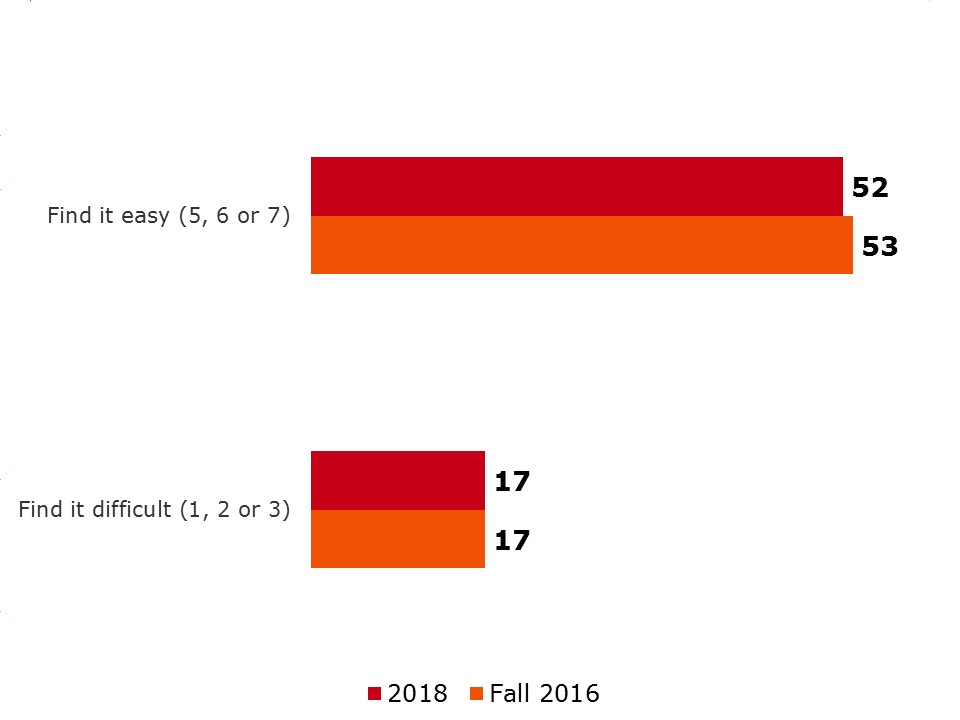

Many Canadians continue to find it challenging to manage roaming fees while travelling. Only half of Canadians (52%) find it easy (5, 6 or 7 on a scale of 1-7) which is on par with Fall 2016 findings (53%). Almost one in every five (17%) Canadians find it quite difficult (1, 2 or 3 on a scale of 1-7) to manage roaming fees.

Exhibit 4.3.2.a. Level of difficulty managing roaming charges when travelling

Level of difficulty managing roaming charges when travelling - text version

QB9. If you use your plan while traveling, you may be charged roaming fees.

How easy do you find it to manage your roaming charges when you are traveling? Please use a 7-point scale where 1 means extremely difficult and 7 means extremely easy.

Base: Respondents who own a cell phone, 2018 (n=1,111), fall 2016 (n=1,277)

Men find it easier to manage roaming charges than women, (56% vs. 48%) as do Canadians who earn $150k or more (68%) when compared to all other income groups and significantly more so compared to those earning under $40k (39%).

It also continues to be true that those with family plans also find it easier to manage roaming charges when compared to consumers with individual plans (58% vs. 50%).

Not unexpectedly and on par with 2016 findings, those who find it easy to manage data are also more likely to find it easy to manage roaming fees (61% vs. 43%) suggesting they are more savvy consumers.

Exhibit 4.3.2.b. Level of difficulty managing roaming charges when travelling by gender and plan

| Level of difficulty managing roaming charges when travelling | Total (A) |

Gender | Plan | ||

|---|---|---|---|---|---|

| Male (B) |

Female (C) |

Family (J) |

Individual (K) |

||

| Base=actual | (1,111) % |

(526) % |

(585) % |

(368) % |

(713) % |

| Find it easy (5, 6 or 7) | 52 | 56 C | 48 | 58 K | 50 |

| Find it difficult (1, 2 or 3) | 17 | 19 | 16 | 20 | 16 |

QB9. If you use your plan while traveling, you may be charged roaming fees. How easy do you find it to manage your roaming charges when you are traveling? Please use a 7-point scale where 1 means extremely difficult and 7 means extremely easy.

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.3.2.d. Level of difficulty managing roaming charges when travelling by manage data and income

Level of difficulty managing roaming charges when travelling |

Total (A) |

Manage data | Income | |||||

|---|---|---|---|---|---|---|---|---|

| Easy (B) |

Difficult (C) |

<$40K (E) |

$40K- <$60K (F) |

$60K- <$100K (G) |

$100K- <$150K (H) |

$150K+ (I) |

||

| Base=actual | (1,111) % |

(610) % |

(98) % |

(199) % |

(168) % |

(261) % |

(163) % |

(141) % |

| Find it easy (5, 6 or 7) | 52 | 61 C | 43 | 39 | 59 E | 49 | 53 E | 68 EGH |

| Find it difficult (1, 2 or 3) | 17 | 15 | 42 B | 11 | 14 | 18 | 29 EF | 19 |

QB9. If you use your plan while traveling, you may be charged roaming fees. How easy do you find it to manage your roaming charges when you are traveling? Please use a 7-point scale where 1 means extremely difficult and 7 means extremely easy.

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

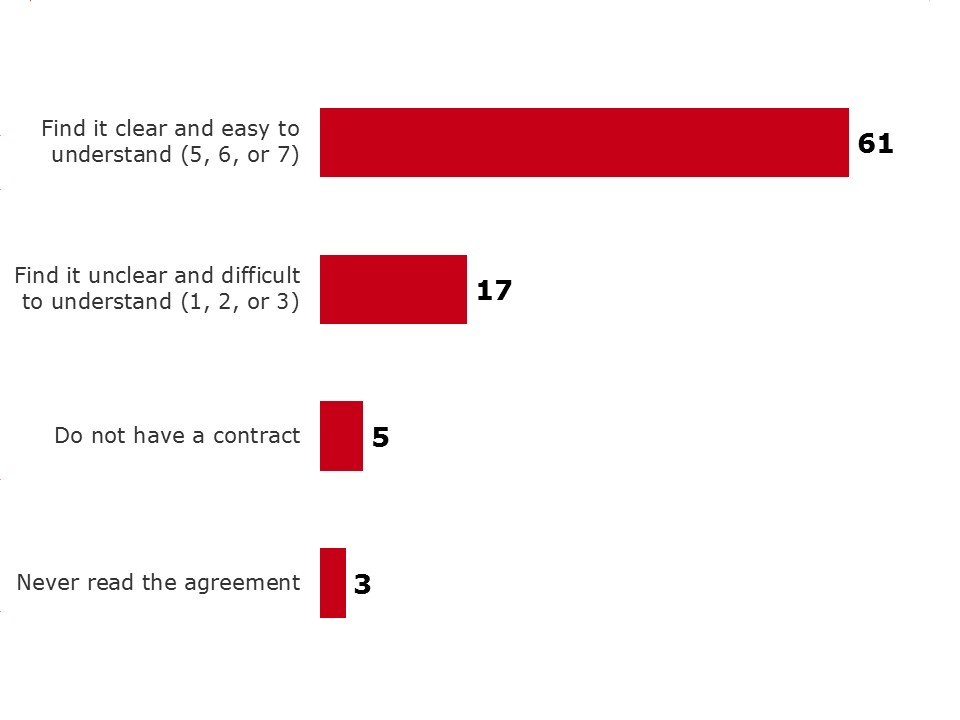

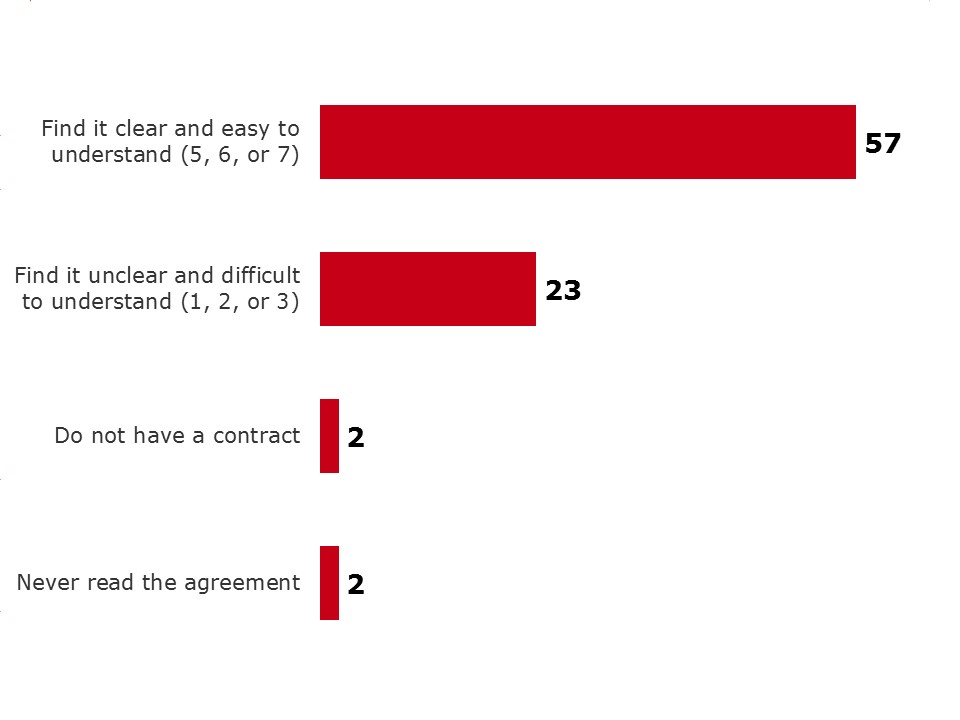

Almost one in three Canadians (29%) believes their wireless contract is extremely clear and easy to understand. In fact, almost two in three Canadians (61%) find it easy and clear (5, 6 or 7 on a scale of 1-7). This is especially true for those aged 18-34 when compared to those aged 35+ (74% vs. 55-56%). It is also true that Canadians with a university degree or higher find their contracts easier to understand when compared to those with a lower education level (55% vs. 66-67%).

Canadians living outside of B.C. find their contracts easier to understand than those who reside in B.C. (59%-66% vs. 44%). B.C.’s residents do not find their contracts to be unclear or difficult to understand but rather feel more neutral about them.

Exhibit 4.4.1.a. Level of ease of understanding wireless contract

Level of ease of understanding wireless contract - text version

WC10. Do you find your contract clear and easy to understand? Please use a 7-point scale where 1 means extremely unclear and difficult to understand and 7 means extremely clear and easy to understand.

Base: Total respondents who own a cell phone, 2018 (n=1,111)

In addition to the above, further factors influence the perception of whether or not a contract is clear and easy to understand. Canadians with unlimited data find their contracts to be less complex and easier to understand (77% vs. 59%). This might merely be a perception of a more understandable contract but the findings suggest there is room for improvement in this area. Not surprising, those who find data management easy also find their contracts easier to navigate (70% vs. 42%). Both suggesting data plays an important role when it comes to contracts.

Exhibit 4.4.1.b. Level of ease of understanding of wireless contract by age, education and data

Level of ease of understanding of wireless contract |

Total (A) |

Age | Education | Data | |||||

|---|---|---|---|---|---|---|---|---|---|

| 18-34 (D) |

35-54 (E) |

55+ (F) |

High school or less (P) |

College (Q) |

University or more (R) |

Unlimit-ed Data (D) |

Limited Data (E) |

||

| Base=actual | (1,111) % |

(141) % |

(359) % |

(594) % |

(278) % |

(314) % |

(501) % |

(122) % |

(651) % |

| Find it clear and easy to understand (5, 6 or 7) | 61 | 74 EF | 56 | 55 | 66 R | 67 R | 55 | 77 E | 59 |

| Find it unclear and difficult to understand (1, 2 or 3) | 17 | 11 | 22 D | 19 | 10 | 16 | 23 P | 11 | 21 D |

QWC10. Do you find your contract clear and easy to understand? Please use a 7-point scale where 1 means extremely unclear and difficult to understand and 7 means extremely clear and easy to understand.

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.4.1.c. Level of ease of understanding of wireless contract by region and manage data

Level of ease of understanding of wireless contract |

Total (A) |

Region | Difficulty managing data | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Atl (G) |

Que (H) |

Ont (I) |

Pra (J) |

BC (K) |

Terr (O) |

Easy (F) |

Difficult (G) |

||

| Base=actual | (1,111) % |

(102) % |

(224) % |

(301) % |

(310) % |

(126) % |

(48) % |

(610) % |

(98) % |

| Find it clear and easy to understand (5, 6, or 7) | 61 | 67 K | 65 K | 59 K | 66 K | 44 | 63 K | 70 G | 42 |

| Find it unclear and difficult to understand (1, 2, or 3) | 17 | 13 | 17 | 16 | 18 | 24 | 19 | 13 | 14 F |

QWC10. Do you find your contract clear and easy to understand? Please use a 7-point scale where 1 means extremely unclear and difficult to understand and 7 means extremely clear and easy to understand.

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher

than the corresponding result in column B.

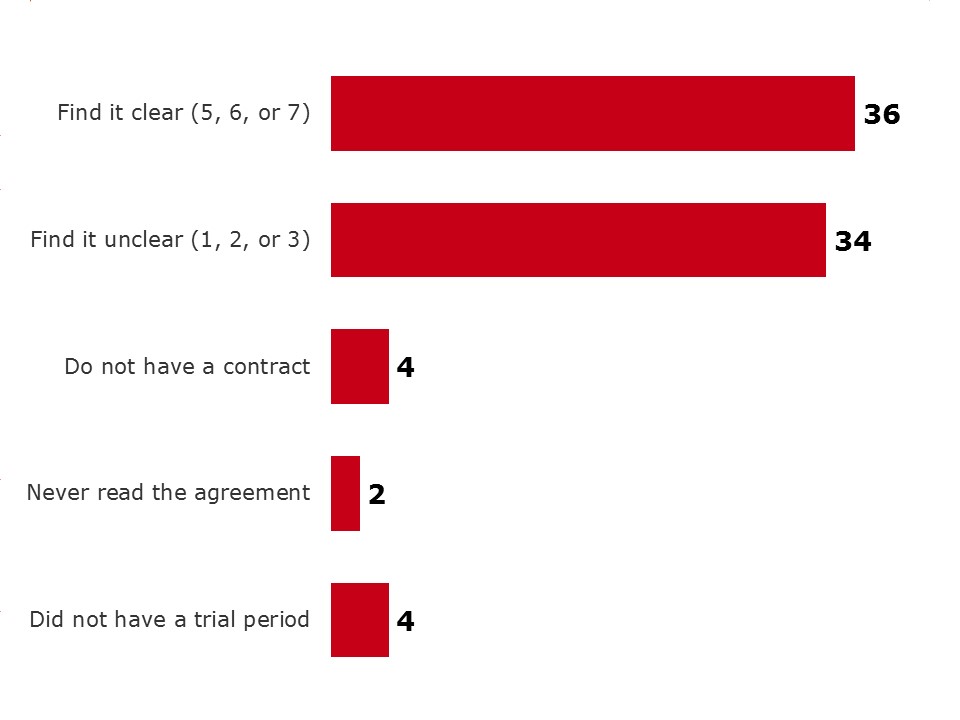

Since 2013, the Wireless Code has required service providers to include a trial period for new contracts that include an early cancellation fee. During the trial period, wireless contract holders can cancel their contract without penalty. This trial period must be a minimum of 15 days service and as of December 1st, 2017, it must permit the customer to use up to half the voice, text, and data usage amounts included in their monthly plan.

Canadians were asked how clear their explanation of the trial period was when they took out their wireless contract. Only a small number of Canadians found the explanation to be clear (36%: 5, 6 or 7 on a scale from 1-7). The remaining, found the explanation to be neither clear nor unclear (20%) or to be unclear (34%: 1, 2 or 3 on a scale from 1-7). A very small minority reported not receiving this trial period at all, which may be due to a contract not being subject to an early cancellation fee.

Exhibit 4.4.2.a. Ease of understanding explanation of the trial period

Ease of understanding explanation of the trial period - text version

WC8. The Code requires service providers to include a trial period for new contracts that include a device. During the trial period, you can cancel your contract without penalty. This trial period now has to be half of a month of service and include half the service included in your monthly plan. How clearly did your service provider explain the trial period to you?

Please use a 7-point scale where 1 means extremely unclear and 7 means extremely clear.

Base: Total respondents who own a cell phone, 2018 (n=1,111)

Interestingly, Canadians with a lower level of education tend to find the explanation of the trial period clear and easier to understand compared to those with a university degree (44% vs. 31% rated 5, 6 or 7 on a scale from 1-7). In fact, one in four Canadians with a university degree find the explanation to be extremely unclear (26%). In previous instances, Canadians with lower educations reported finding other aspects of their wireless contract more difficult and unclear which suggests that those with a lower education might think they understand the details of the trial period, but in fact, do not.

Results also suggest that the type of plan plays a role in how easy or difficult the trial period explanation is to understand. More specifically, those who have a family plan find the trial period explanation clearer than those with individual plans (42% vs. 33%) and those with unlimited data find it clearer compared to those with limited data (46% vs. 34%). Again, highlighting the important role of data when it comes to understanding contracts.

Exhibit 4.4.2.b. Ease of understanding explanation of the trial period by education, plan and data

| Ease of understanding explanation of the trial period | Total (A) |

Education | Plan | Data | ||||

|---|---|---|---|---|---|---|---|---|

| High school or less (P) |

College (Q) |

University or more (R) |

Family (J) |

Individual (K) |

Unlimited data (D) |

Limited data (E) |

||

| Base=actual | (1,111) % |

(278) % |

(314) % |

(501) % |

(368) % |

(713) % |

(122) % |

(651) % |

| Find it clear and easy to understand (5, 6 or 7) | 36 | 44 R | 38 | 31 | 42 K | 33 | 46 E | 34 |

| Find it unclear and difficult to understand (1, 2 or 3) | 34 | 26 | 33 | 38 P | 33 | 35 | 28 | 40 |

QWC8. The Code requires service providers to include a trial period for new contracts that include a device. During the trial period, you can cancel your contract without penalty. This trial period now has to be half of a month of service and include half the service included in your monthly plan. How clearly did your service provider explain the trial period to you? Please use a 7-point scale where 1 means extremely unclear and 7 means extremely clear.

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

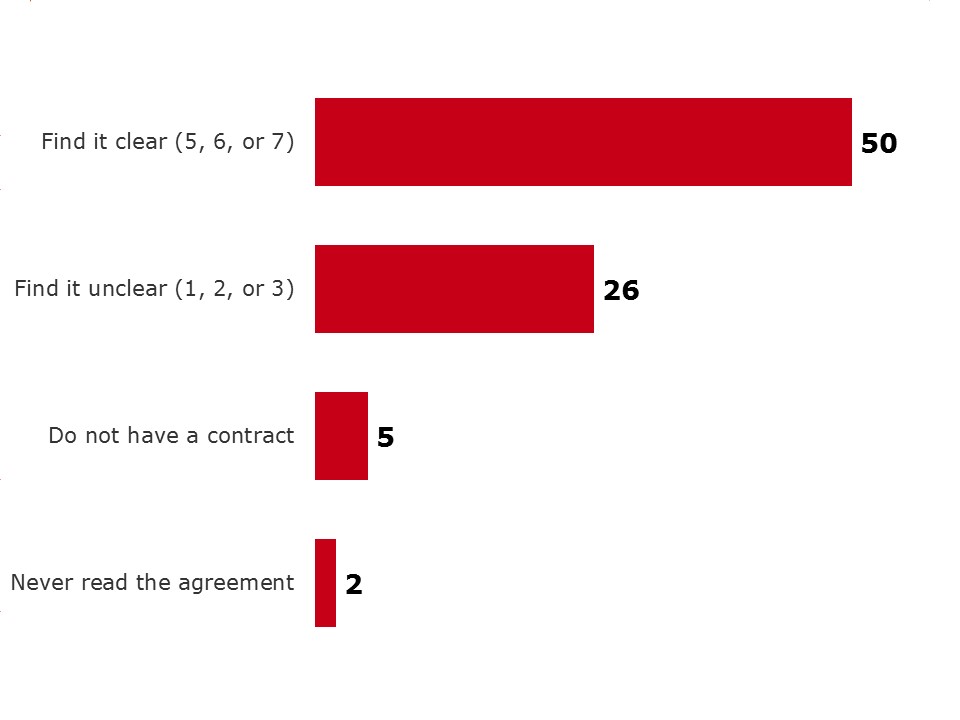

Most service providers require customers to pay a cancellation fee if they cancel their contracts before the agreed upon end date. This needs to be carefully explained to the consumer for them to be fully aware of the implications of early cancellation. While one in two Canadians who have wireless plans find the explanation to be clear, a concerning 26% report this explanation to be unclear, implying an insufficient explanation by some service providers (rated 1, 2 or 3 on a scale from 1-7). This, however, is an improvement compared to 2014, when 32% of Canadians reported their service provider’s explanation of the early cancellation fee to be unclear.

Exhibit 4.4.3.a. Clear explanation of early cancellation of contract

Clear explanation of early cancellation of contract - text version

WC9. When you signed your contract or accepted your service agreement, how clearly did your service provider explain any fees that would apply if you cancel your contract or agreement early? Please use a 7-point scale where 1 means extremely unclear and 7 means extremely clear.

Base: Total respondents who own a cell phone, 2018 (n=1,111)

Unclear explanation of cancellation fees (rated 1, 2 or 3 on a scale from 1-7) is more likely to be reported by men (30% vs. 23%), those with a university degree compared to those with only high school or less (32% vs. 18%), those who have made a complaint (39% vs. 24%) and those who find data management difficult (43% vs. 25%).

Regional skews are pertinent with the Territories reporting significantly higher levels (48%) of the explanation being unclear compared to all other regions (21-34%)

Exhibit 4.4.3.b. Clear explanation of early cancellation of contract by gender and region

| Clear explanation of early cancellation of contract | Total (A) |

Gender | Region | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Male (B) |

Female (C) |

Atl (G) |

Que (H) |

Ont (I) |

Pra (J) |

BC (K) |

Terr (O) |

||

| Base=actual | (1,111) % |

(526) % |

(585) % |

(102) % |

(224) % |

(301) % |

(310) % |

(126) % |

(48) % |

| Find it clear (5, 6, or 7) | 50 | 50 | 50 | 57 KO | 55 KO | 49 | 53 KO | 39 | 32 |

| Find it unclear (1, 2 or 3) | 26 | 30 C | 23 | 21 | 24 | 25 | 26 | 34 | 48 GHIJ |

QWC9. When you signed your contract or accepted your service agreement, how clearly did your service provider explain any fees that would apply if you cancel your contract or agreement early? Please use a 7-point scale where 1 means extremely unclear and 7 means extremely clear.

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.4.3.c. Clear explanation of early cancellation of contract by education, complaint, and data management

Clear explanation of early cancellation of contract |

Total (A) |

Education | Complaint | Difficulty managing data | ||||

|---|---|---|---|---|---|---|---|---|

| High school or less (P) |

College (Q) |

University or more (R) |

Made one (S) |

Did not make one (T) |

Easy (F) |

Difficult (G) |

||

| Base=actual | (1,111) % |

(278) % |

(314) % |

(501) % |

(183) % |

(925) % |

(610) % |

(98) % |

| Find it clear (5, 6, or 7) | 50 | 59 R | 51 | 45 | 32 | 54 S | 54 G | 39 |

| Find it unclear (1, 2 or 3) | 26 | 18 | 26 | 32 P | 39 T | 24 | 25 | 43 F |

QWC9. When you signed your contract or accepted your service agreement, how clearly did your service provider explain any fees that would apply if you cancel your contract or agreement early? Please use a 7-point scale where 1 means extremely unclear and 7 means extremely clear.

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

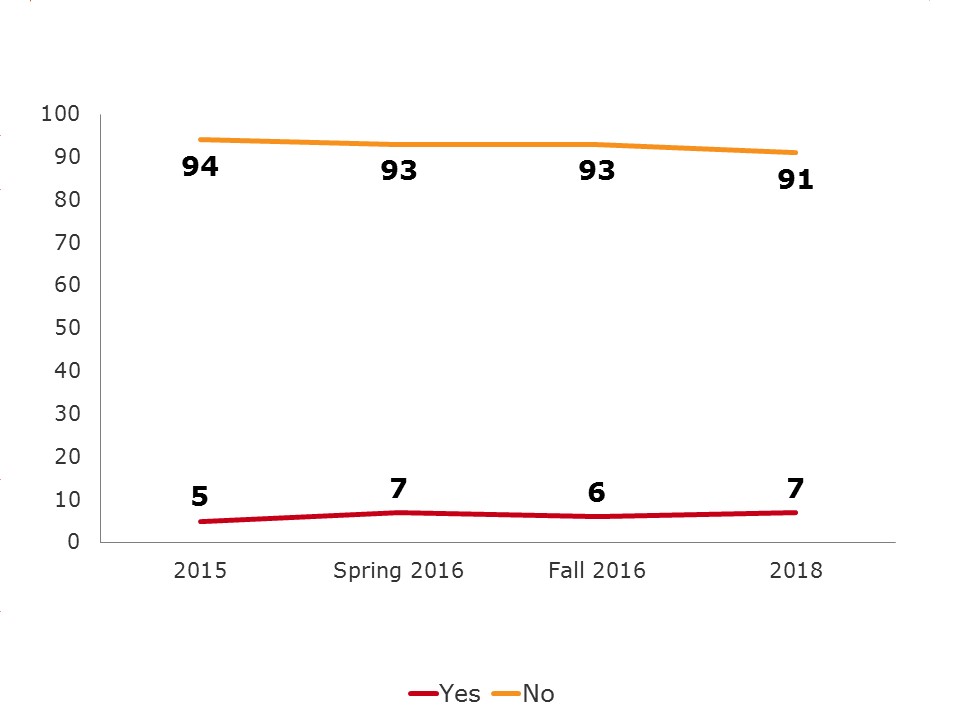

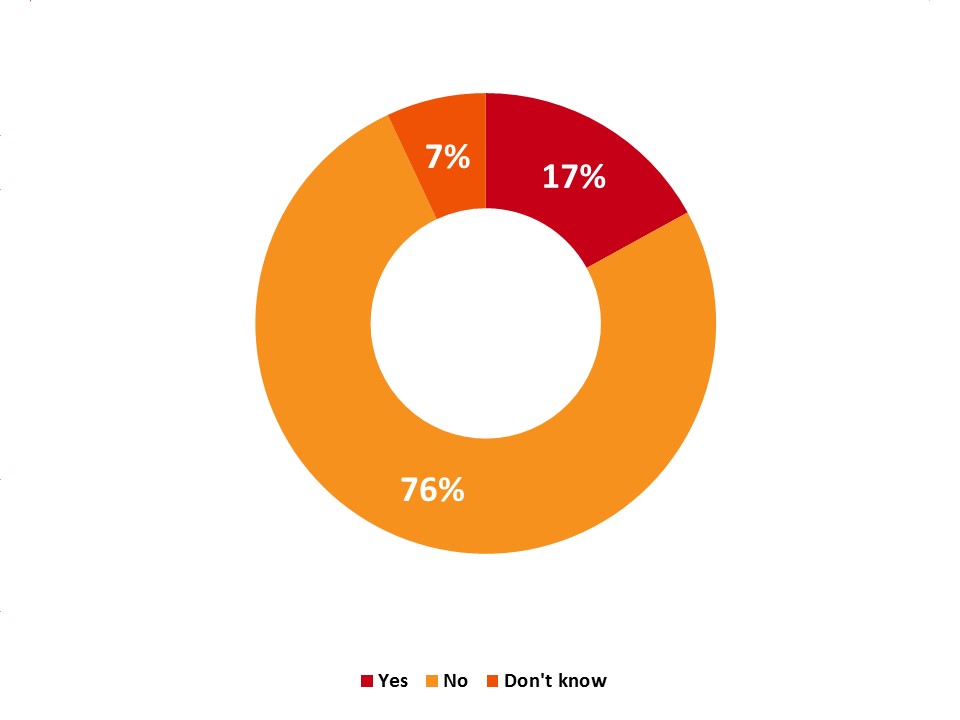

In only a small number of instances (12%) changes to wireless services were made without expressly making the consumer aware of the new terms and conditions. This tends to be the case for younger Canadians (18-34 and 35 to 54 year olds) (17% and 13% respectively) compared to older Canadians (7%). Households with an income of between $40k and $60k are less likely (5%) to believe they have experienced this compared to other income groups (12-16%).

Exhibit 4.5.1.a. Changes to contract without disclosure of changes in terms and conditions

Changes to contract without disclosure of changes in terms and conditions - text version

WC11. Have you ever become aware that your service provider changed your plan without expressly making you aware of how the terms and conditions had changed?

Base: Total respondents who own a cell phone, 2018 (n=1,111)

Changes to wireless services without expressly making the consumer aware of the new terms and conditions is reported more often by those who have made a complaint in the last 12 months (30% vs. 8%) and one can expect that some of these complaints might be related to the unexpected service changes.

There is also a higher incidence of tab contract users reporting unexpected changes (16% vs. 10%) and it is also more likely to have occurred among consumers who find data management difficult (27% vs. 8%).

Exhibit 4.5.1.b. Changes to contract without disclosure of changes in terms and conditions by Age and Income

| Changes to contract without disclosure | Total (A) |

Age | Income | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 18-34 (D) |

35-54 (E) |

55+ (F) |

<$40K (E) |

$40K- <$60K (F) |

$60K- <$100K (G) |

$100K- <$150K (H) |

$150K+ (I) |

||

| Base=actual | (1,111) % |

(141) % |

(359) % |

(594) % |

(199) % |

(168) % |

(261) % |

(163) % |

(141) % |

| Yes | 12 | 17 F | 13 F | 7 | 16 F | 5 | 12 | 14 F | 15 F |

QWC11. Have you ever become aware that your service provider changed your plan without expressly making you aware of how the terms and conditions had changed?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.5.1.c. Changes to contract without disclosure of changes in terms and conditions by Complaint, Tab and Manage data

| Changes to contract without disclosure | Total (A) |

Lodged Complaint | Tab contracts | Manage data | |||

|---|---|---|---|---|---|---|---|

| Yes (S) |

No (T) |

Yes (B) |

No (C) |

Easy (F) |

Difficult (G) |

||

| Base=actual | (1,111) % |

(183) % |

(925) % |

(293) % |

(744) % |

(610) % |

(98) % |

| Yes | 12 | 30 T | 8 | 16 C | 10 | 8 | 27 F |

QWC11. Have you ever become aware that your service provider changed your plan without expressly making you aware of how the terms and conditions had changed?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

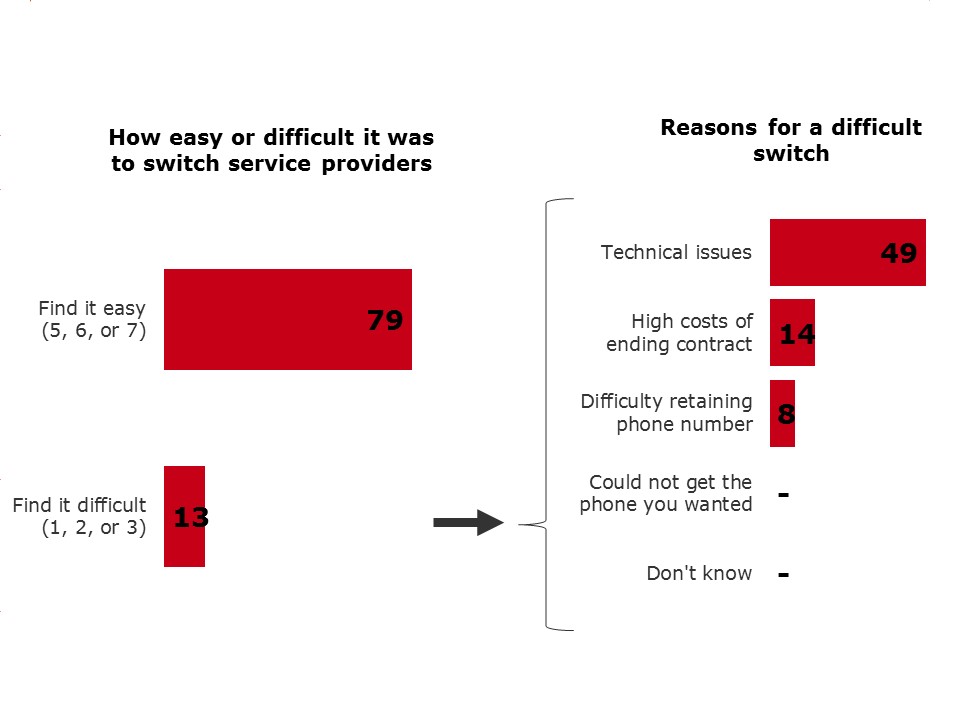

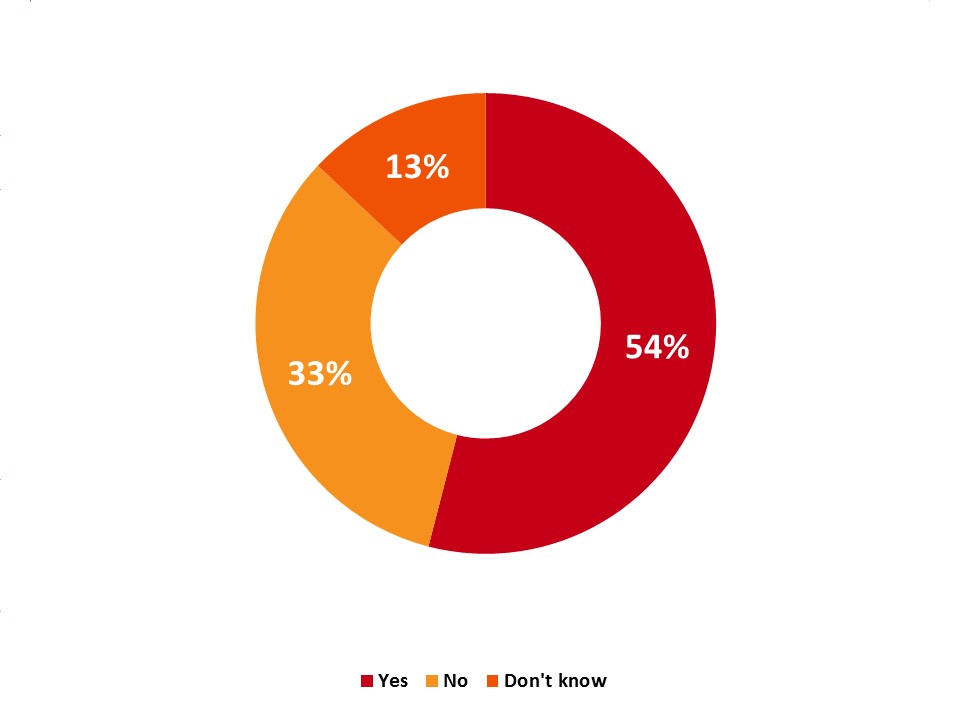

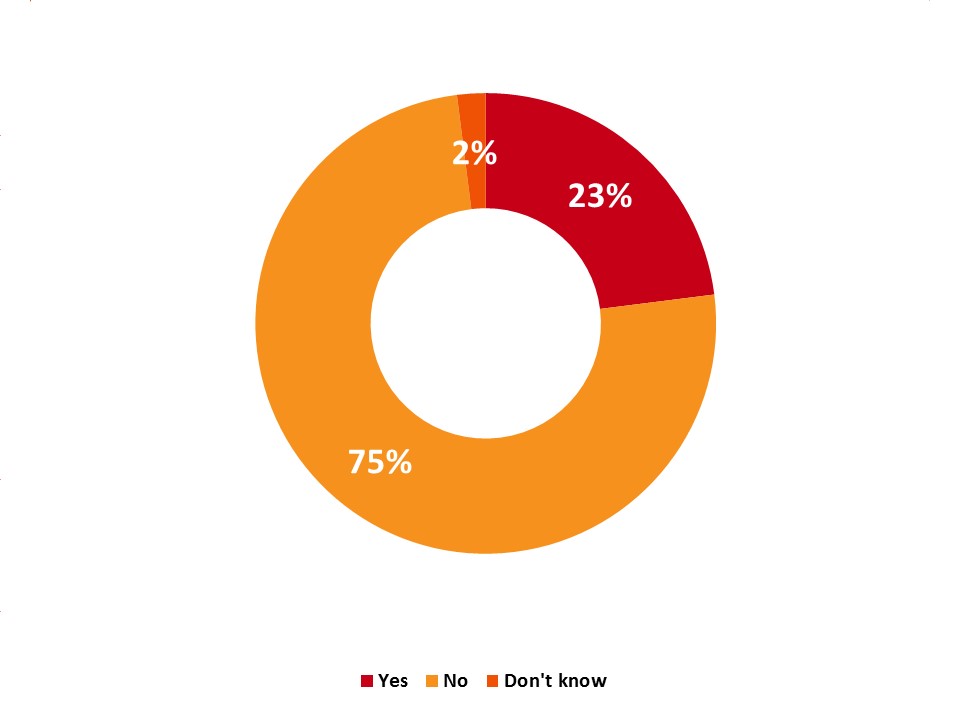

A relatively small number of Canadian cell phone users have switched service providers in the last two years (16%) with the main reason being a better deal (49%) and dissatisfaction with their service provided only mentioned by one in five switchers (19%). Most switchers found it easy to do so (79%) (rated 5, 6 or 7 on a scale from 1-7) and the minority (13%) who found it difficult (1, 2 or 3 on a scale from 1-7) reported technical issues to be the main reason for their struggle (49%).

Exhibit 4.5.2.a. Switching wireless service providers and reasons for it

Switching wireless service providers and reasons for it - text version

WC16. Have you changed wireless service providers in the last two years?

Base: Total respondents who own a cell phone, 2018 (n=1,111)

WC12. Why did you change service provider?

Base: Total respondents who changed their service provider in P2Y, 2018 (n=152)

Exhibit 4.5.2.b. Ease of switching and reason for difficulty in switching providers

Ease of switching and reason for difficulty in switching providers - text version

WC13 How easy or difficult was it to switch service providers? Please use a 7-point scale where 1 means extremely difficult and 7 means extremely easy.

Base: Total respondents who changed their service provider in P2Y, 2018 (n=152)

WC14. Was there a reason why switching providers was difficult for you?

Base: Total respondents who find it difficult to switch, 2018 (n=19)

Switchers are more likely to be younger (18-54) (19% vs. 10%) and/or university graduates (19% vs. 12-14%). While there are no differences between regions, within the Prairies, those residing in Manitoba are more likely to switch than those living in Saskatchewan (21% vs. 6%)[4].

Exhibit 4.5.2.c. Switching wireless service providers by region and education

| Switching wireless service providers | Total (A) |

Region | Education | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Atl (G) |

Que (H) |

Ont (I) |

Pra (J) |

BC (K) |

Terr (O) |

High school or less (P) |

College (Q) |

University or more (R) |

||

| Base=actual | (1,111) % |

(102) % |

(224) % |

(301) % |

(310) % |

(126) % |

(48) % |

(278) % |

(314) % |

(501) % |

| Yes | 16 | 19 | 16 | 18 L | 13 | 11 | 15 | 12 | 14 | 19 P |

WC16. Have you changed wireless service providers in the last two years?Base: Total respondents who own a cell phone, 2018 (n=1,111)

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.5.2.d. Switching wireless service providers by age

| Switching wireless service providers | Total | Age | ||||

|---|---|---|---|---|---|---|

| 18-34 (D) |

35-54 (E) |

55+ (F) |

||||

| Base=actual | (1,111) % |

(141) % |

(359) % |

(594) % |

||

| Yes | 16 | 19 F | 19 F | 10 E | ||

WC16. Have you changed wireless service providers in the last two years?

Base: Total respondents who own a cell phone, 2018 (n=1,111) Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B

The rapid decline in incidence of Canadians making complaints about their wireless services stabilised in 2018. However, despite a slight, albeit insignificant increase in complaints between Fall 2016 and 2018 (1%) compared to 2014, eight per cent fewer Canadians have made complaints since 2014.

Exhibit 4.6.1.a. Wireless service complaint made in the past 12 months

Wireless service complaint made in the past 12 months - text version

QB11a/QB11/QB4 Have you made a complaint about your wireless services in the past 12 months?

Base: Respondents who own a cell phone: 2018 (n=1,111), fall 2016 (n=1,277), total respondents, winter 2016 (n=925), 2015 (n=1,005),

2014 (n=1,016)

Quebeckers continue to be least likely to make complaints (8% vs 15-23%) compared to those in other regions of Canada. This is likely due to the provincial consumer protection legislation that Quebec has had in place since 2009 - Quebec’s Bill 60.

Canadians with higher educations (college or university) (21% each) are more likely to have complained to their service provider in the last 12 months, compared to those with a high school education or lower (10%). Similarly, English speaking Canadians are more likely to have complained compared to Francophones (19% vs. 9%) as did those with a family plan (23% vs. 16%).

Not unexpectedly, those who find managing data difficult are still more likely to make a complaint (43% vs. 16%).

Exhibit 4.6.1.b. Wireless service complaint made in the past 12 months by region, education

| Wireless service complaint made in P12M | Total (A) |

Region | Education | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Atl (G) |

Que (H) |

Ont (I) |

Pra (J) |

BC (K) |

Terr (O) |

High school or less (P) |

College (Q) |

University or more (R) |

||

| Base=actual | (1,111) % |

(102) % |

(224) % |

(301) % |

(310) % |

(126) % |

(48) % |

(278) % |

(314) % |

(501) % |

| Yes | 18 | 16 | 8 | 22 H | 20 H | 23 H | 15 | 10 | 21 P | 21 P |

QB11a. Have you made a complaint about your wireless services in the past 12 months?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Exhibit 4.6.1.c. Wireless service complaint made in the past 12 months by language, difficulty managing data and plan

| Wireless service complaint made in P12M | Total (A) |

Language | Manage data | Plan | ||||

|---|---|---|---|---|---|---|---|---|

| English (B) |

French (F) |

Other (G) |

Easy (F) |

Difficult (G) |

Family (J) |

Individual (K) |

||

| Base=actual | (1,111) % |

(741) % |

(219) % |

(144) % |

(610) % |

(98) % |

(211) % |

(888) % |

| Yes | 18 | 19 C | 9 | 24 C | 16 | 43 F | 23 K | 16 |

QB11a. Have you made a complaint about your wireless services in the past 12 months?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

Reason for Complaints

In addition to the decline in complaints, the actual reasons for the complaint are changing. When comparing the Fall of 2016 with the 2018 results, we see a significant decrease in three of the four primary reasons that Canadians complained about their wireless services: Incorrect charges on their bill (45% vs. 17%), inadequate quality of service (25% vs. 16%) and misleading information about the terms of contract (23% vs. 12%). The fourth reasons i.e. data charges also see a decline albeit not significant (32% vs. 29%) and continues to be the primary reason for complaints. This supports the notion that the Wireless Code is making a significant difference in the lives of wireless users with legislation working for consumers and again, highlights the importance of data in wireless contracts moving forward.

Exhibit 4.6.1.d. Reason for complaints

Reason for complaints - text version

QB11b. What was your complaint about?

Base: Respondents who made a complaint about the wireless services in the past 12 months, 2018 (n=183), Fall 2016 (n=203)

Complaint Issued to Service Provider

Consistent with earlier findings, more than 9 in 10 Canadians who make a complaint make the complaint to their service provider (97%)[5]. Five percent of these complaints are escalated to the CCTS, which is mandated to review complaints from customers who are unsatisfied with how their complaint was addressed by their service provider.

Exhibit 4.6.1.e. Complaints to wireless service provider

Complaints to wireless service provider - text version

WC7. Who did you complain to? Was it your service provider, the Commission for Complaints for Telecom-Television Services, also knowns as the CCTS, or both?

Base: Total respondents who made a complaint about the wireless services in the P12M, 2018 (n=183)

QB11c. Did you complain to your service provider?

Base: Those who made a complaint, Fall 2016 (n=203)

QB4a. Who did you complain to?

Base: Those who made a complaint winter 2016 (n=179), 2015 (n=222), 2014 (n=258)

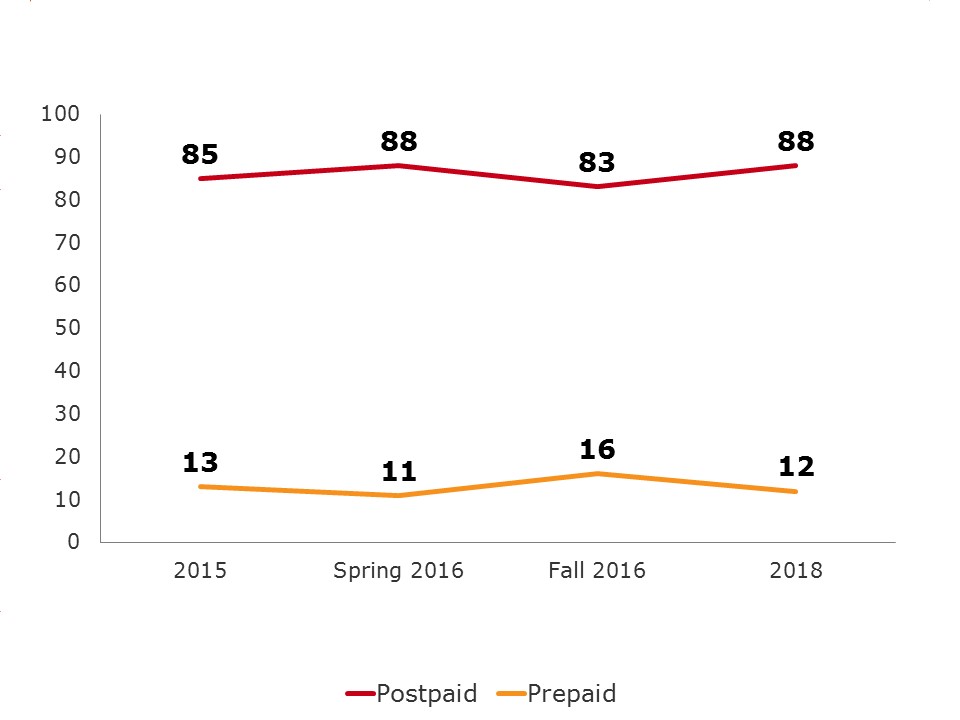

Pre-paid or Post-paid

Most Canadians continue to purchase post-paid services in 2018 (88%), in fact, only 1 in 10 cell phone owners used prepaid or pay-as-you-go plans. A very small minority have both post-paid and pre-paid services (1%).

Exhibit 4.7.1.a. Type of service plan

Type of service plan - text version

QB1c. Is it a monthly plan, or a prepaid or pay-as-you-go plan?

Base: Respondents who own a cell phone, 2018 (n=1,111), fall 2016 (n=1,277), total respondents Spring 2016 (n=925), 2015 (n=1,005)

Where we saw gender and income skews in the Fall of 2016, that is no longer the case. We do however, find that older Canadians (55+) are more likely to choose pre-paid/pay-as-you-go (14% vs. 9-10%). In addition to that, wireless consumers who have made a complaint in the last 12 months are more likely to have a monthly or post-paid plan (93% vs. 85%).

Exhibit 4.7.1.b. Type of service plan by age and complaint

| Type of service plan | Total | Age | Lodged Complaint | |||

|---|---|---|---|---|---|---|

| 18-34 (D) |

35-54 (E) |

55+ (F) |

Yes (S) |

No (T) |

||

| Base=actual | (1,111) % |

(141) % |

(359) % |

(594) % |

(183) % |

(925) % |

| Monthly/postpaid | 87 | 90 | 89 F | 83 | 93 T | 85 |

| Prepaid/pay-as-you-go | 11 | 10 | 9 | 14 E | 6 | 12 |

QB1c. And, is it a monthly plan, or a prepaid or pay-as-you-go plan?

Note: Letters denote statistically significant difference. For example, if there is a B then the result is significantly higher than the corresponding result in column B.

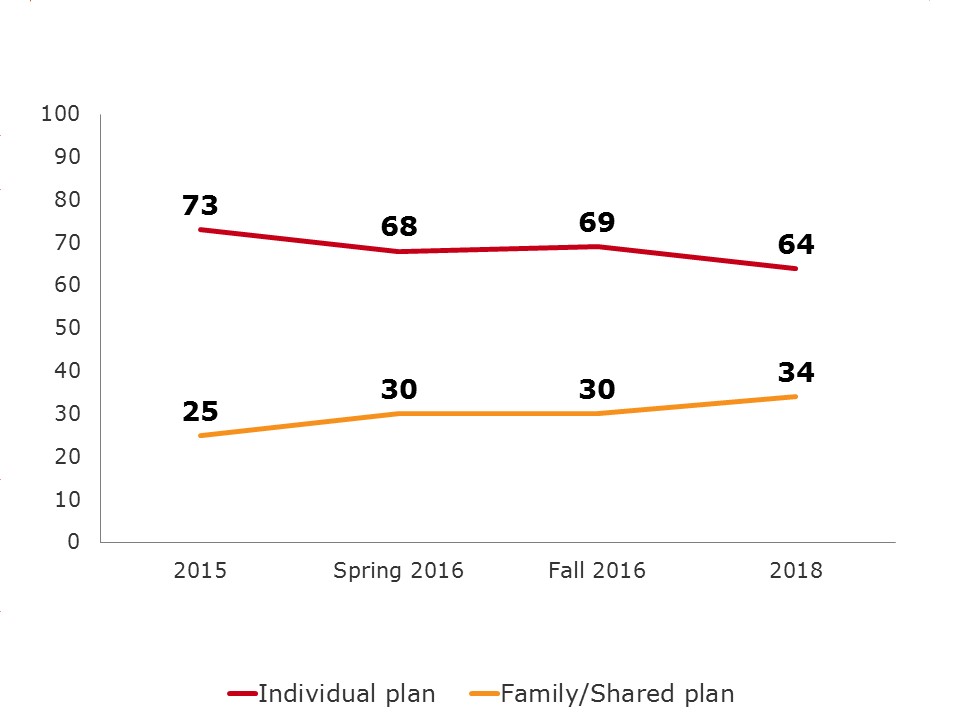

Individual or Family/Shared Plan

Canadians are increasingly taking advantage of family/shared plans. Since 2015, there has been a significant increase in the use of family/shared plans (up 9%) with the majority of these plans shared by 2 people (56% vs. 7-19%).

Exhibit 4.7.1.c. Individual or family/shared plan

Individual or family/shared plan - text version

QB1a. Is it an individual plan or a family or shared plan?

Base: Respondents who own a cell phone, 2018 (n=1,111), fall 2016 (n=1,277)

QB9a. About the contract or plan for your personal wireless device…Is it an individual plan or a family plan?

Base: Total Respondents winter 2016 (n=925), 2015 (n=1,005)

Exhibit 4.7.1.d. Number of family members sharing the plan

| Number of family members sharing the plan |

Total |

|---|---|

| Base=actual | (368) % |

| 2 | 56 |

| 3 | 19 |

| 4 | 17 |

| 5+ | 7 |

QWC2. How many family members are on your shared plan?

Where the Fall 2016 results showed a prevalence for family plans amongst middle aged Canadians as well as higher income families, it is not the case in 2018. All demographic groups now equally opt for family or shared plans. We do however find that those with family plans are more likely to have made a complaint in the last 12 months than not (43% vs. 32%). The reverse is also true, those who have made a compliant in the last 12 months are more likely to have a family plan compared to those who have not complained (23% vs. 16%).

Exhibit 4.7.1.e. Individual or family/shared plan by complaint